Latin America

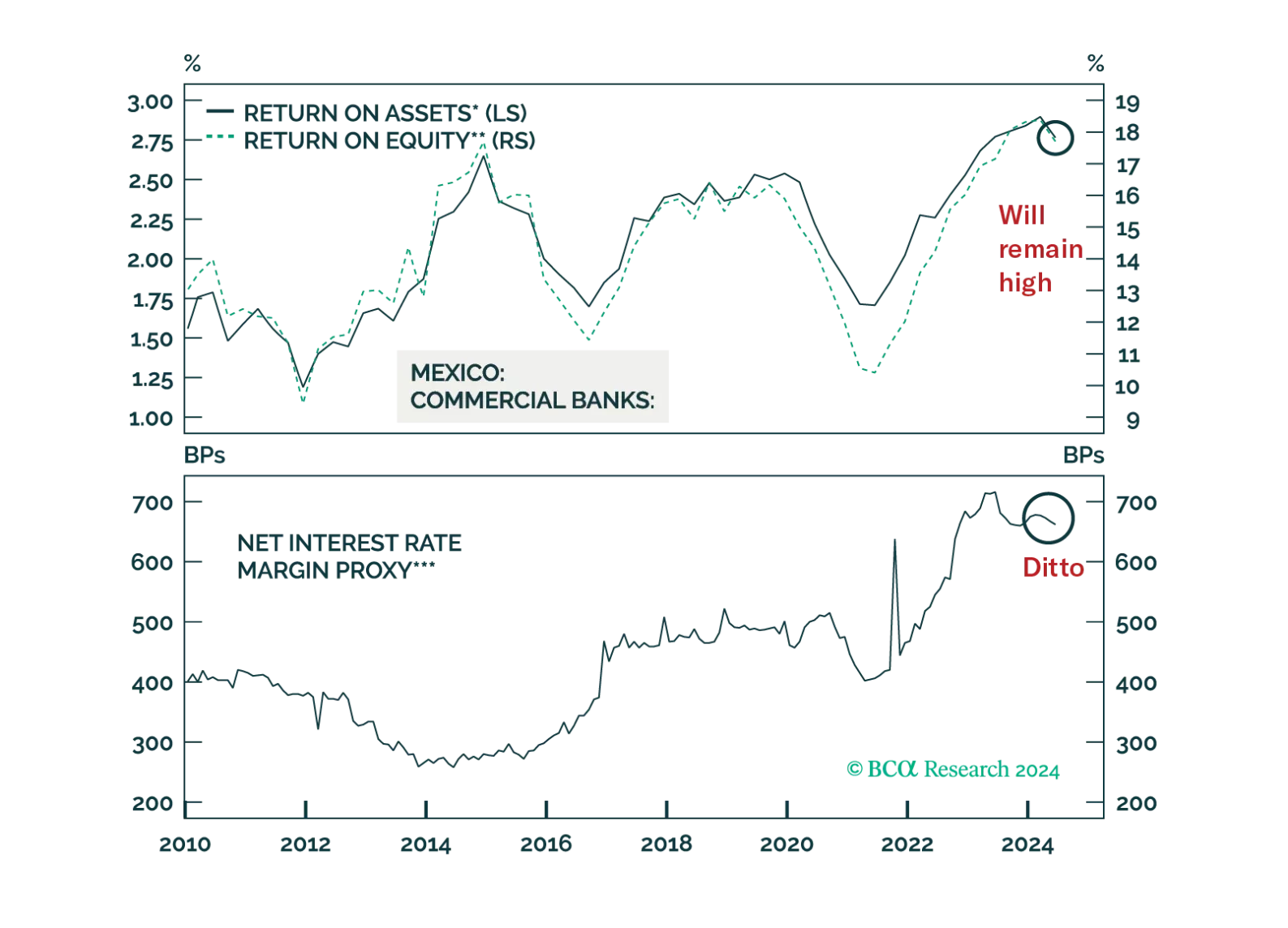

The politically induced selloff in Mexican markets has gone too far. In our view, investor fears about the constitutional changes are largely unwarranted. These reforms will have little to no ramifications for the economy in the foreseeable future, and it is not clear to what extent they can undermine Mexican democracy. Moreover, the market riot is not justified by the country’s decent macro shape. All in all, Mexican markets will resume their outperformance versus their EM peers sooner rather than later.

The Central Bank of Brazil (BCB) raised interest rates last week. Is this the commencement of a major tightening cycle that will persist well into next year? Despite this move, we maintain that the BCB will cut interest rates substantially next year. We believe the Lula-nominated board members are playing the long game: voting to hike rates until year-end to establish credibility with financial markets in order to get a pass at easing monetary policy in early 2025.

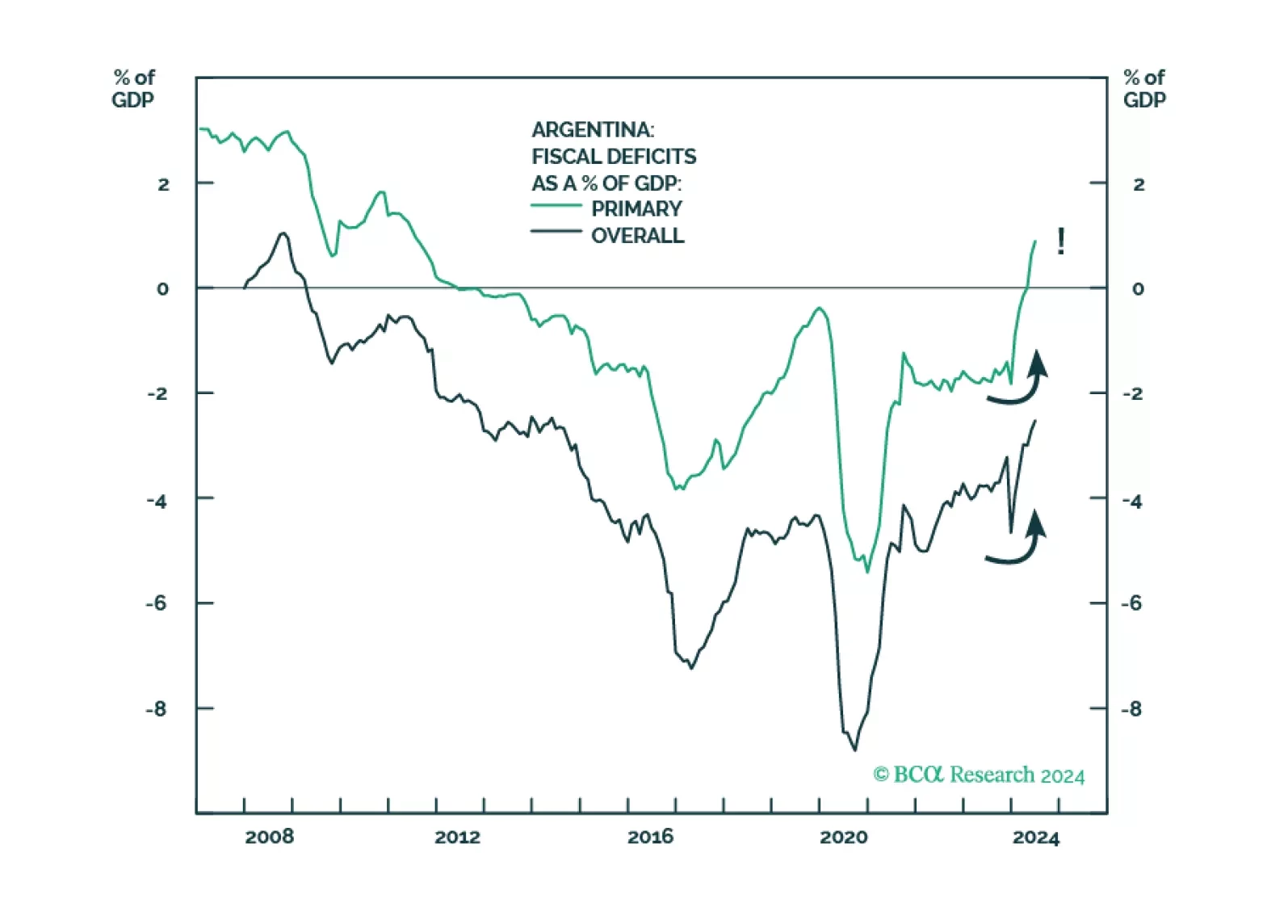

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

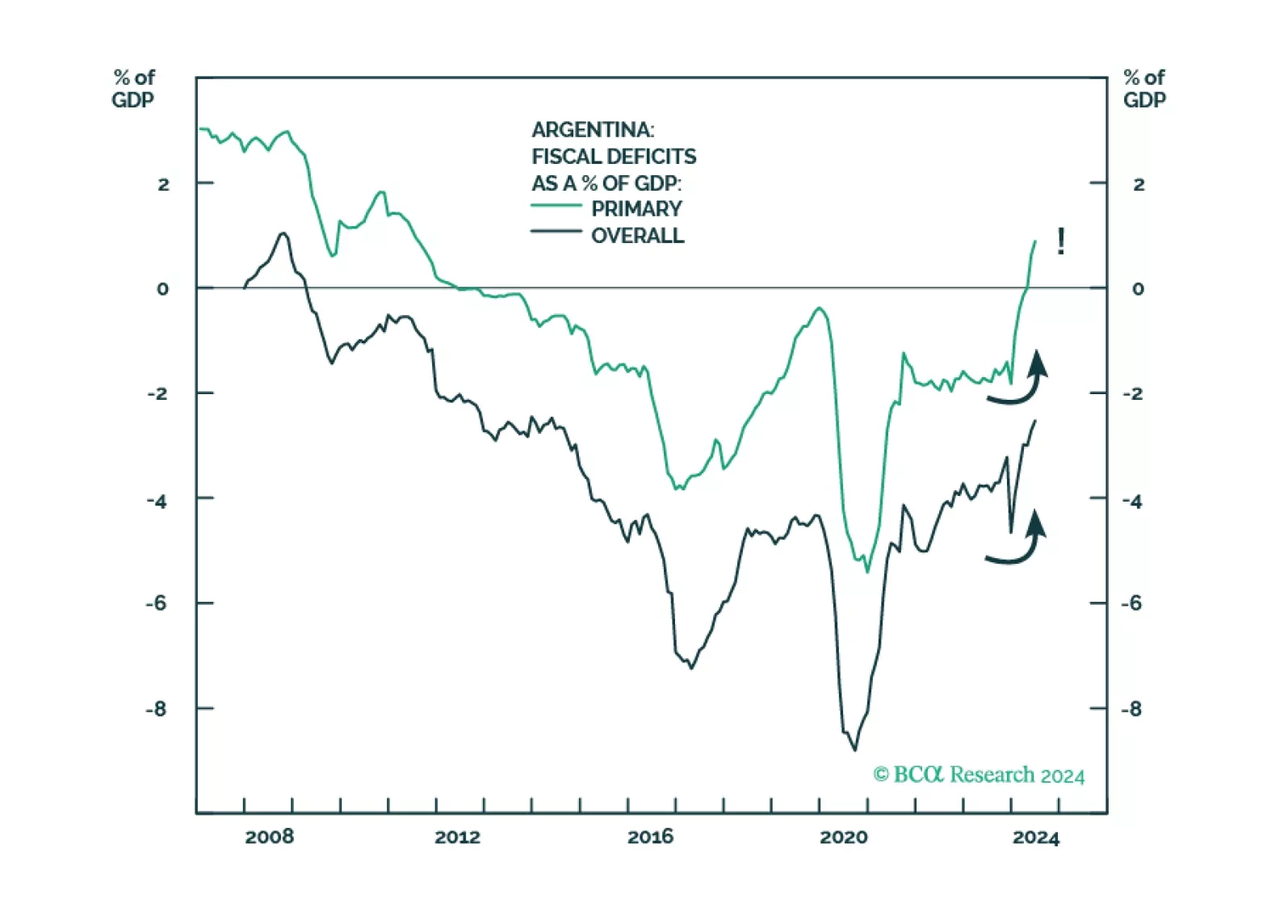

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

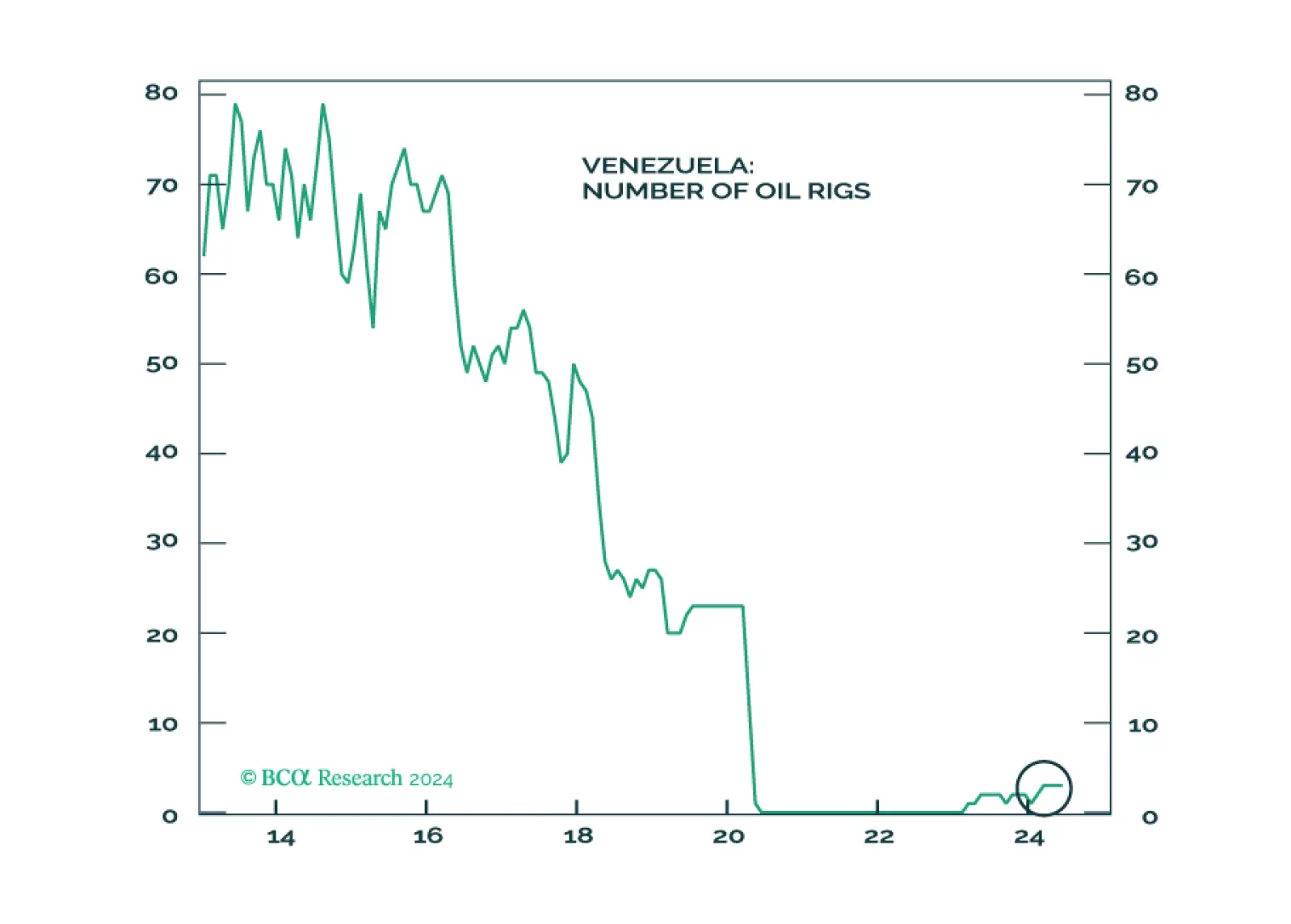

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

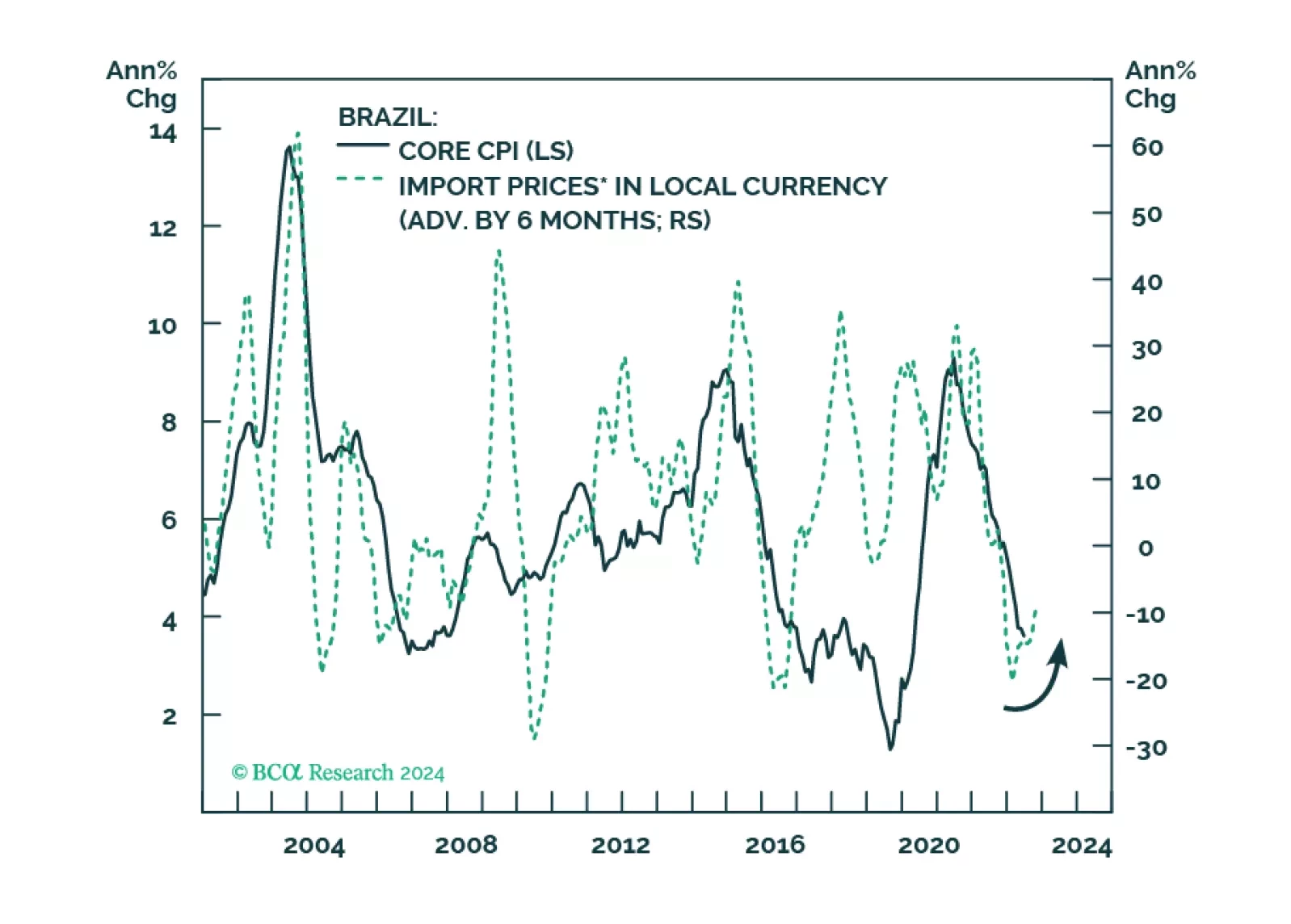

Brazil’s two macro demons – a rising public debt-to-GDP ratio and inflation – have resurfaced and will worsen over the coming months. Yet, President Lula will pay lip service to fiscal concerns without enacting meaningful cutbacks. In addition, a politicized COPOM will cut rates aggressively next year and fall behind the inflation curve. All in all, the selloff in Brazilian markets still has legs.