Manufacturing

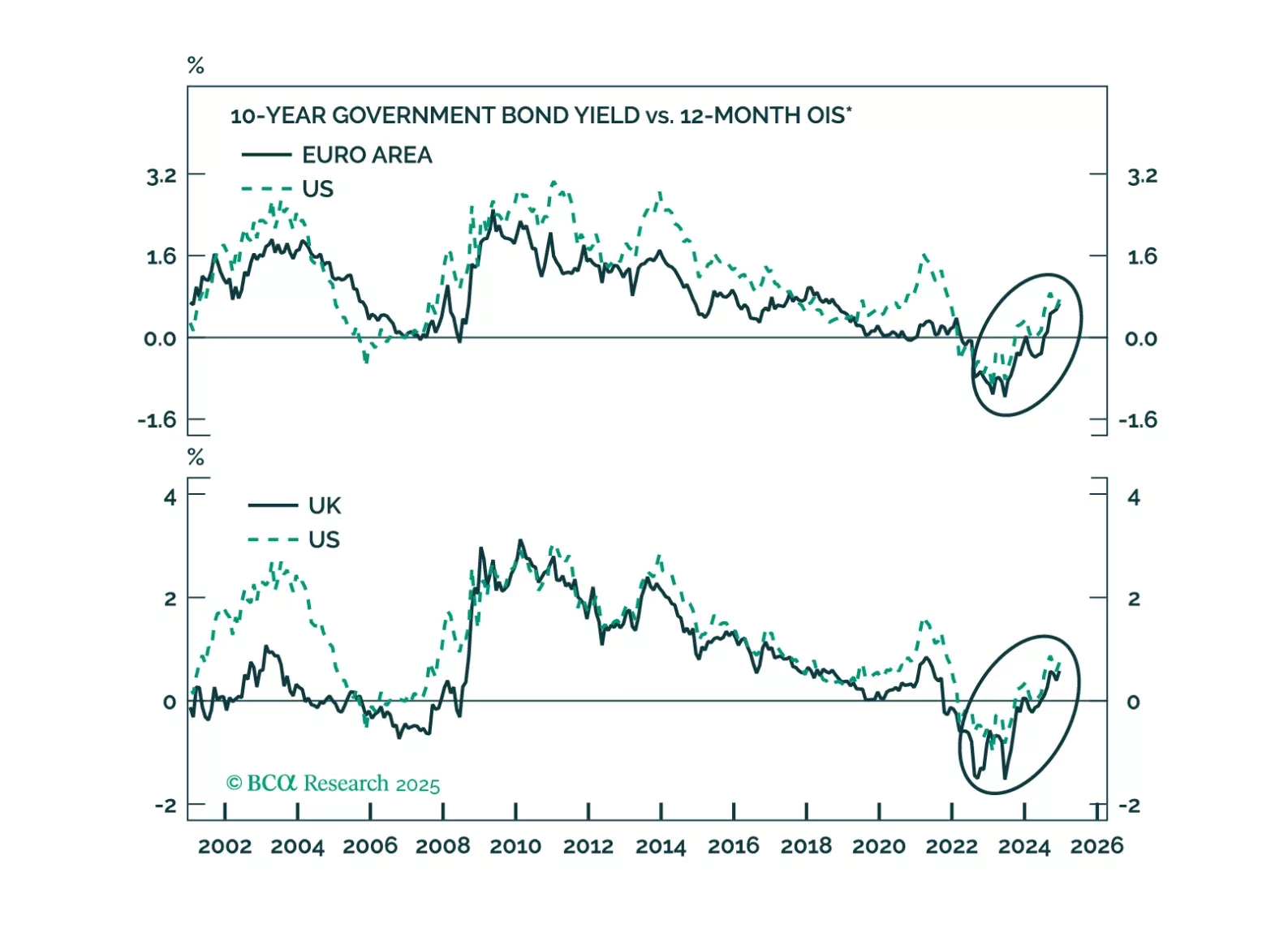

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

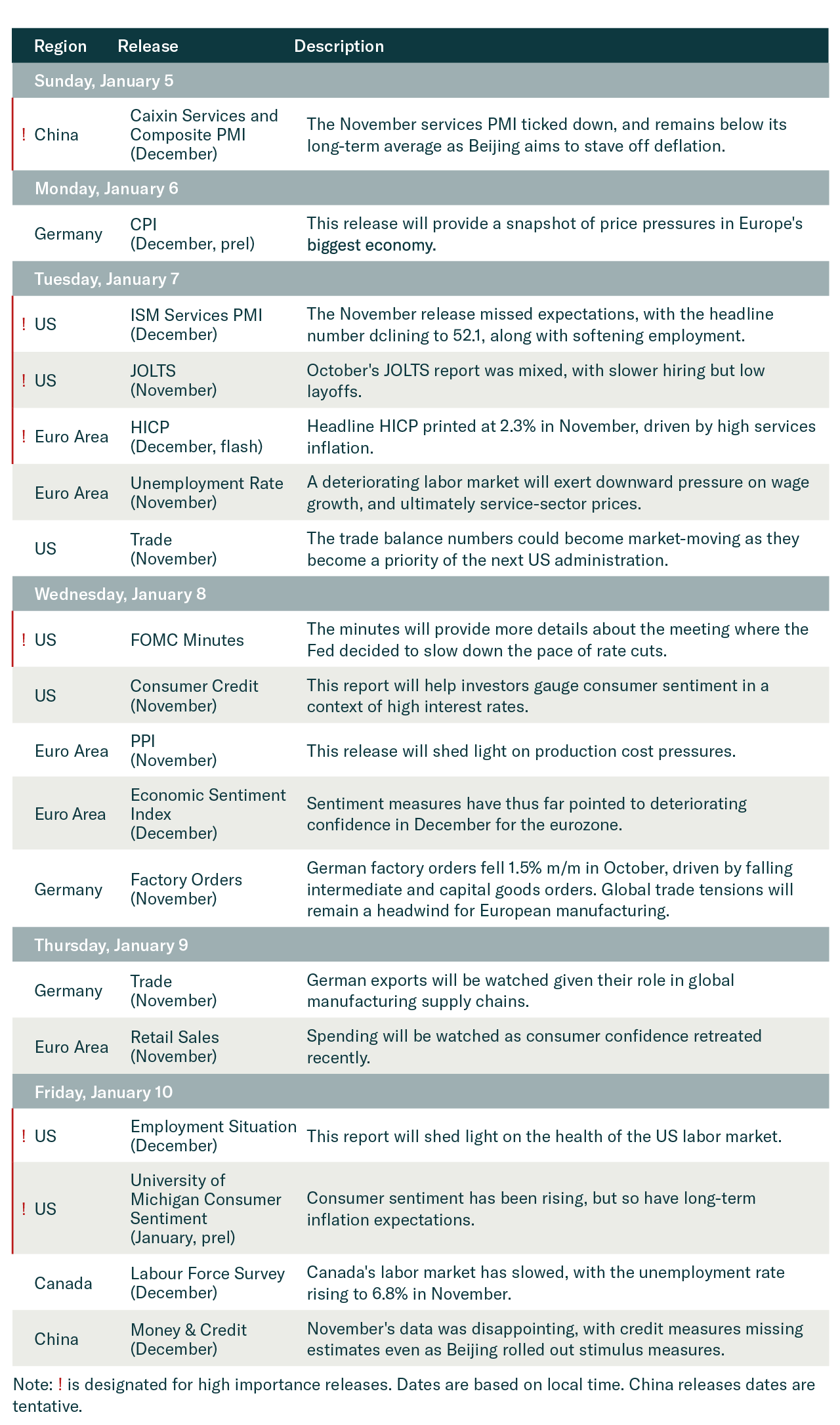

November factory orders in Germany widely missed estimates, falling by 5.4% m/m, worsening the 1.5% October decline. Excluding major orders, which often distort the overall picture, core new orders fell 1.7% y/y after growing 5.7% in October. The European…

The December ISM Services PMI beat estimates, increasing to 54.1 from 52.1 in November. All subcomponents increased except for employment, which nonetheless remains in expansion. The prices paid component was especially strong, increasing to 64.4 from…

December euro area inflation met expectations, with headline HICP printing at 2.4% y/y from 2.2% in November, and core steady at 2.7%, above the ECB’s target. Services inflation remains elevated at 4.0% y/y, up from 3.9% a month prior. While services…

Job openings once again beat expectations in November, increasing to 8.1m from 7.8m in October. However, hires and quits decreased and layoffs increased. The gap between quits and layoffs, a leading indicator of labor market demand, ticked down. The jobs gap,…

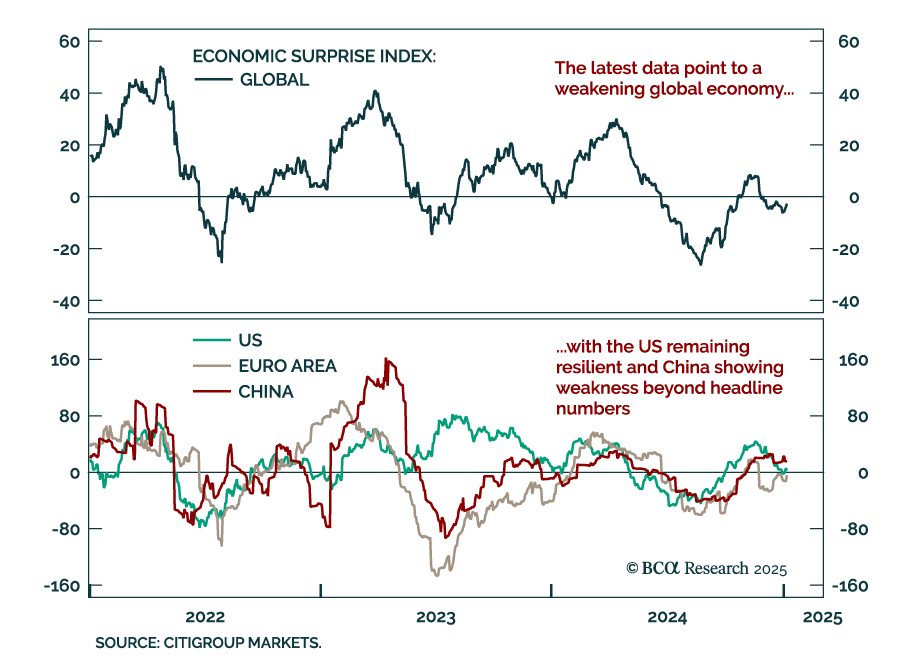

Economic data released over the holiday period extended recent trends, reflecting a softening global economy with resilient US growth, and an ailing manufacturing sector. The December global manufacturing PMI declined to 49.6 after reaching the 50 level…

US November housing data was mixed, but still reflected a weak picture. Housing starts were down 1.8% m/m, below expectations of a 2.6% increase. However, building permits were stronger than expected, increasing 6.1%. Units under construction remain in free…

December flash PMIs for the core advanced economies showed service sector growth picking up. Manufacturing keeps contracting, and the US continues to outperform its DM peers. The US composite index beat expectations and increased to 56.6 from 54.9.…

The December Empire Manufacturing index missed expectations, slowing to 0.2 from 31.2 in November. Most cyclical components eased, suggesting last month's surge was a post-election blip. The new orders subcomponent decreased, leaving the new…