Manufacturing

China’s economic malaise extended through the month of July. The contraction in property investment worsened (-10.2% YTD y/y) and disappointed expectations of a slower pace of decline. Residential property sales remained dismal (-25.9% YTD y/y). Industrial…

"There's no supply chain in the world that's more critical to us than China." — Tim Cook, CEO of Apple, March 2024 According to BCA Research’s China Investment Strategy and Emerging Market Strategy services, while high-profile multinational companies…

The Reserve Bank of New Zealand unexpectedly embarked on an easing pivot in August, cutting the Official Cash Rate by 25 bps to 5.25%. The central bank also signaled further rate cuts by lowering its rate benchmark forecast to 4.92% by December 2024 and 3.85%…

US producer prices rose by a softer-than-expected 0.1% m/m in July, from 0.2% in June. The core measure remained unchanged, the tamest reading in four months. Notably, the index for final demand services fell 0.2% m/m. Our US Bond strategists have…

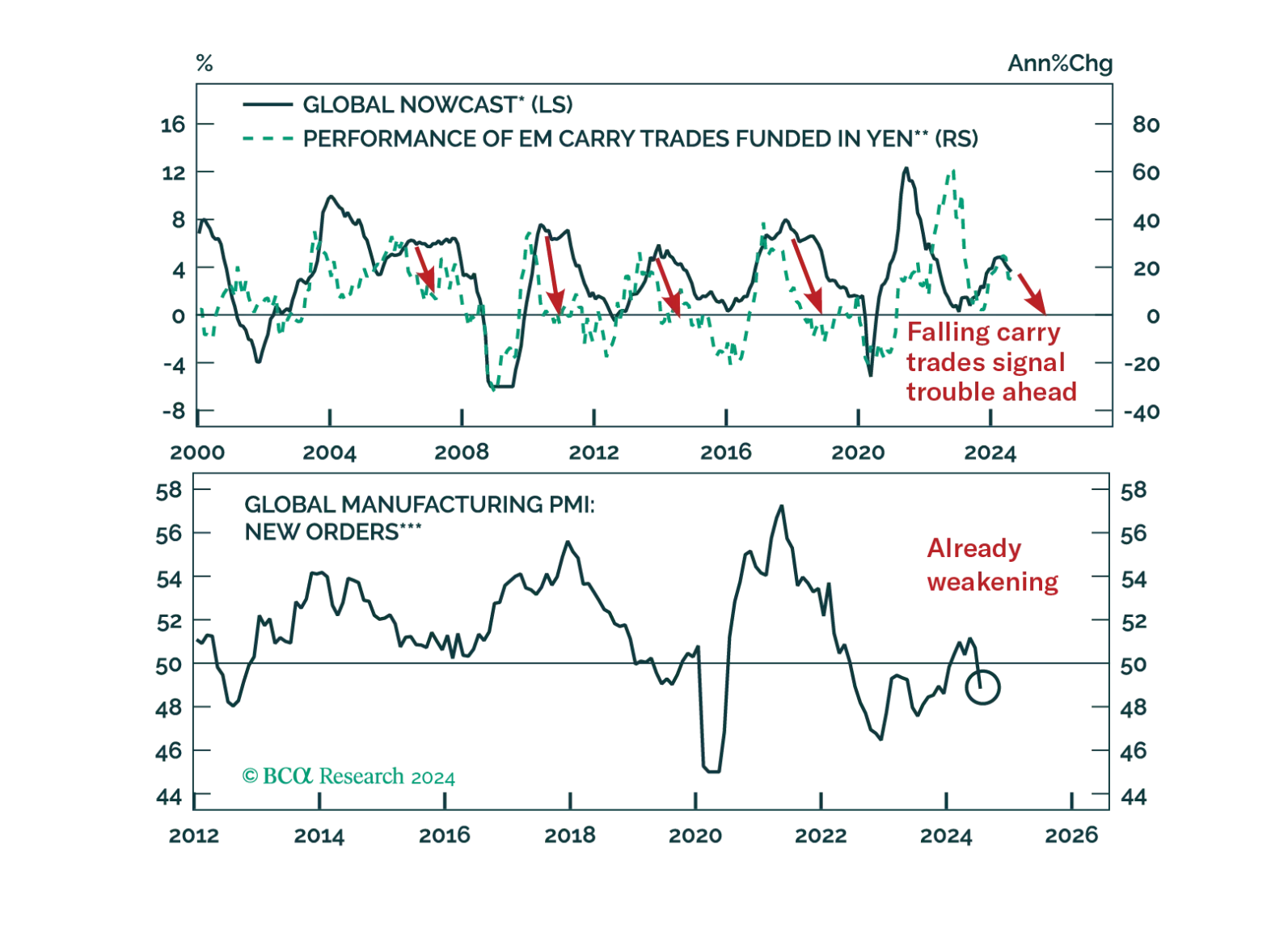

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

German Industrial production and factory orders continued their slump in June. The usual powerhouse of the Euro Area economy has been trailing its peers throughout 2024. While both industrial production and factory orders surprised to the upside in June,…

Over the past few weeks, global equities have been hit by rising scepticism over the bullish AI narrative and increasing concerns over global growth. Stocks should stabilize in the near term, but the medium-term direction is to the downside. We expect the S&P 500 to drop to 3750 in 2025 and the 10-year Treasury yield to fall to 3%.

After briefly breaking a 27-month streak of negative sentiment back in June, the Eurozone Sentix Economic index disappointed in August. The overall index worsened from July’s negative reading to -13.9, below expectations of a milder deterioration. The…

The ISM services PMI surprised positively in July. The headline index expanded 2.6 ppts to 51.4, reversing May’s fastest pace of contraction in four years. Notably, the business activity subcomponent increased 4.9 ppts to 54.5, new orders and new export…

The ISM Manufacturing PMI disappointed in July. The headline index declined at a faster pace, from 48.5 to 46.8, disappointing expectations and extending a four-month contraction streak. Details were uninspiring. New orders dipped to 47.4 from 49.3,…