Manufacturing

Preliminary PMI estimates suggest that US economic leadership remained intact in June, despite previous signs that it was passing the global growth baton to the rest of the world. US manufacturing, services and composite PMIs all surpassed expectations as…

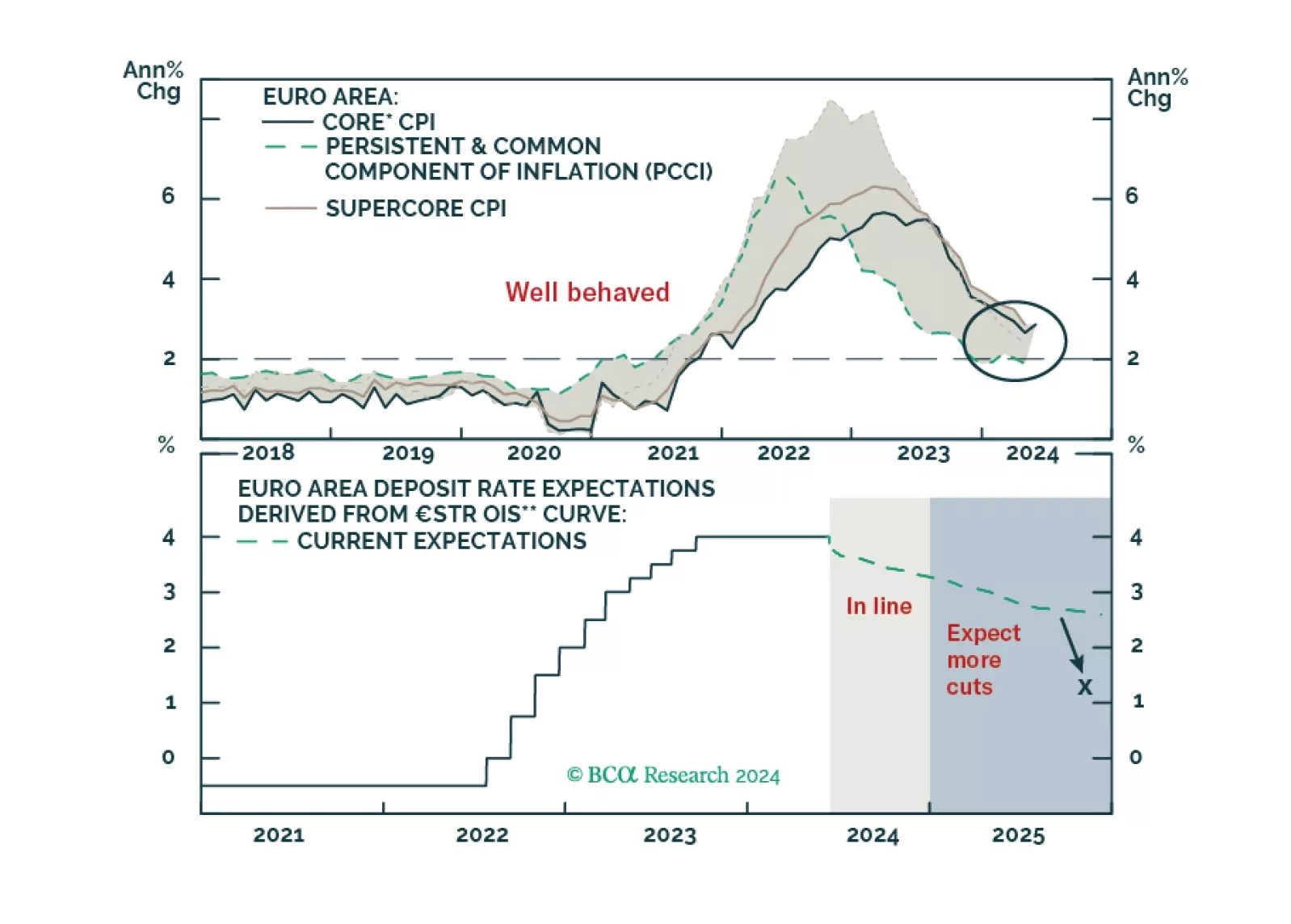

The ECB delivered its first rate cut in June, moderating the degree of restriction rather than pivoting outright to easy monetary policy settings. Indeed, the rate cut was accompanied by an upward revision of inflation and growth forecasts. Since then,…

The heart of the US manufacturing sector is still pulsing. Industrial production surpassed expectations in May, growing by 0.9% m/m after having stagnated in April. Notably, the pro-cyclical manufacturing production index rebounded from April’s surprise…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions and they surprised to the upside in May. Notably, electronics exports, which are particularly sensitive to…

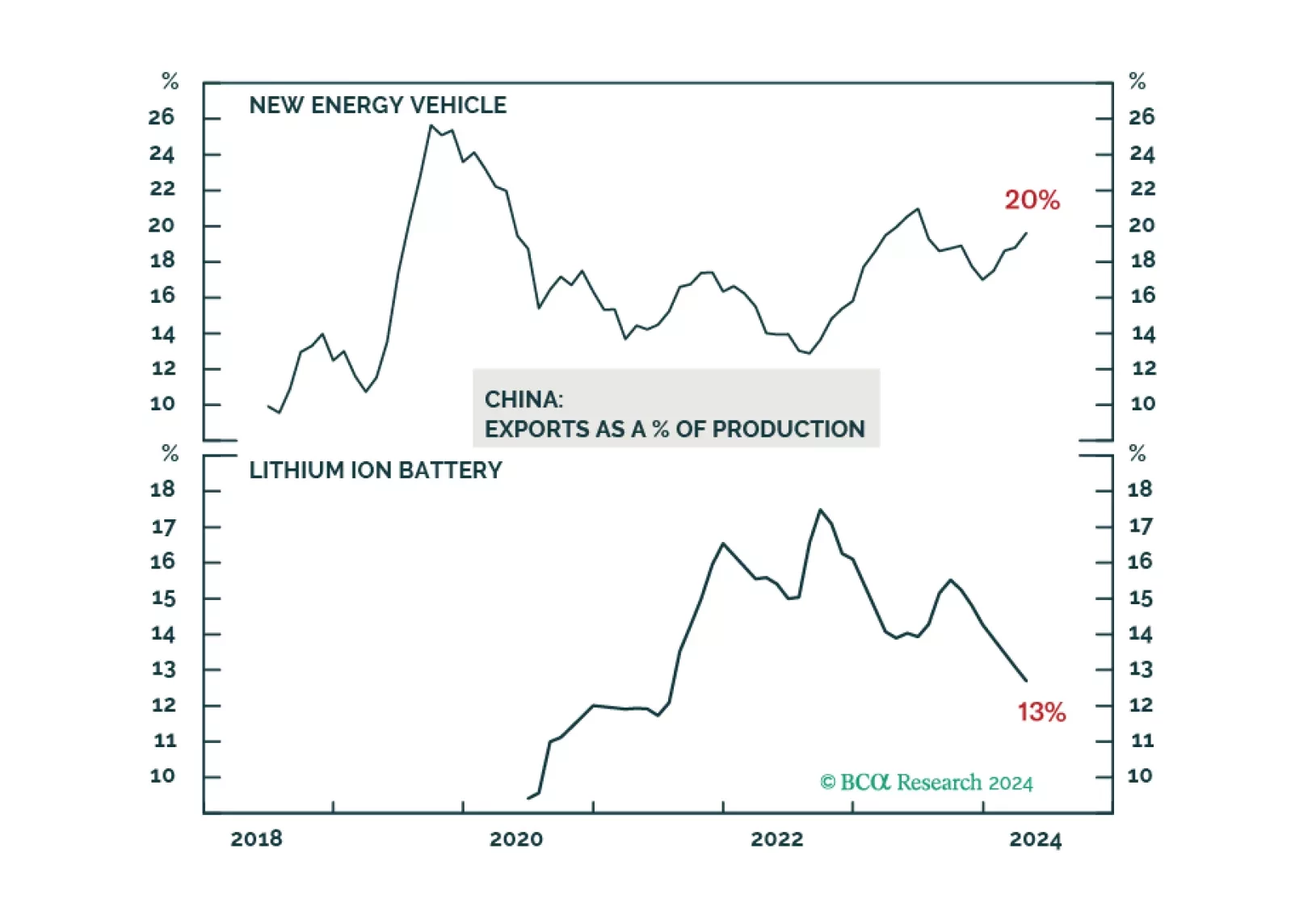

On Wednesday, the European Commission announced it would impose tariffs ranging between 17% and 38% on imports of Chinese EVs starting next month. These duties will be applied on top of existing 10% across-the-board tariffs on all Chinese EV imports, and…

The issue of "industrial overcapacity" in China may be a misconception. Overcapacity in the old-economy sectors has largely diminished, while China's dominance in the global green-energy market reflects its technological advancements and innovations.

Sweden is a small export-oriented economy and its high sensitivity to global trade makes it a good bellwether of global growth developments. The headwinds from high borrowing costs are relatively more pronounced in Sweden where a large share of households…

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

Our colleagues at Global Investment Strategy have shown that postwar US (and global) manufacturing cycles have tended to last 3 years, divided equally between an 18-month up leg and an 18-month down leg. This framework has been a useful gauge for the…