Manufacturing

The US manufacturing cycle has followed a surprisingly stable pattern for over seven decades. History suggests that this cycle tends to last for about 36 months, with a down leg spanning 18 months, followed by an up leg approximately spanning another 18…

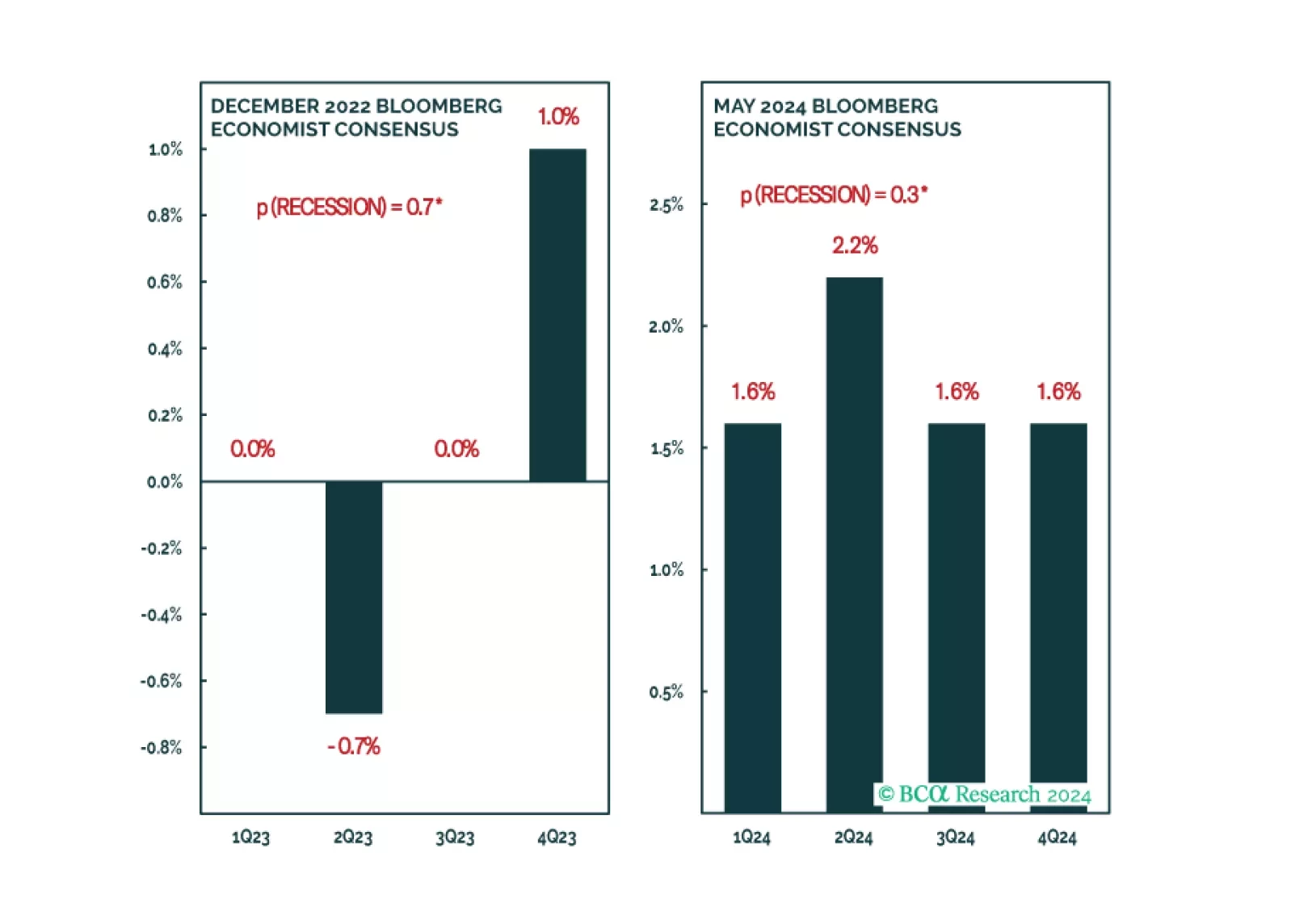

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

There is a path to a soft landing, but it is a narrow one. We estimate that there is only a 20% chance that the US will avoid a recession before the end of 2025. We are currently neutral on global equities, but expect to downgrade stocks to underweight during the summer.

UK retail sales plunged 2.3% m/m in April from a downwardly revised 0.2% m/m contraction in March, significantly undershooting expectations of a 0.5% m/m decline. Household goods as well as clothing and footwear stores led the shortfall. Retailers have…

Negotiated wages rose 4.7% y/y in Q1, from 4.5% y/y in Q4 in the Eurozone. Meanwhile, preliminary estimates for the Eurozone Composite PMI surprised to the upside in May. Although wage growth is the main driver of services inflation and Euro Area economic…

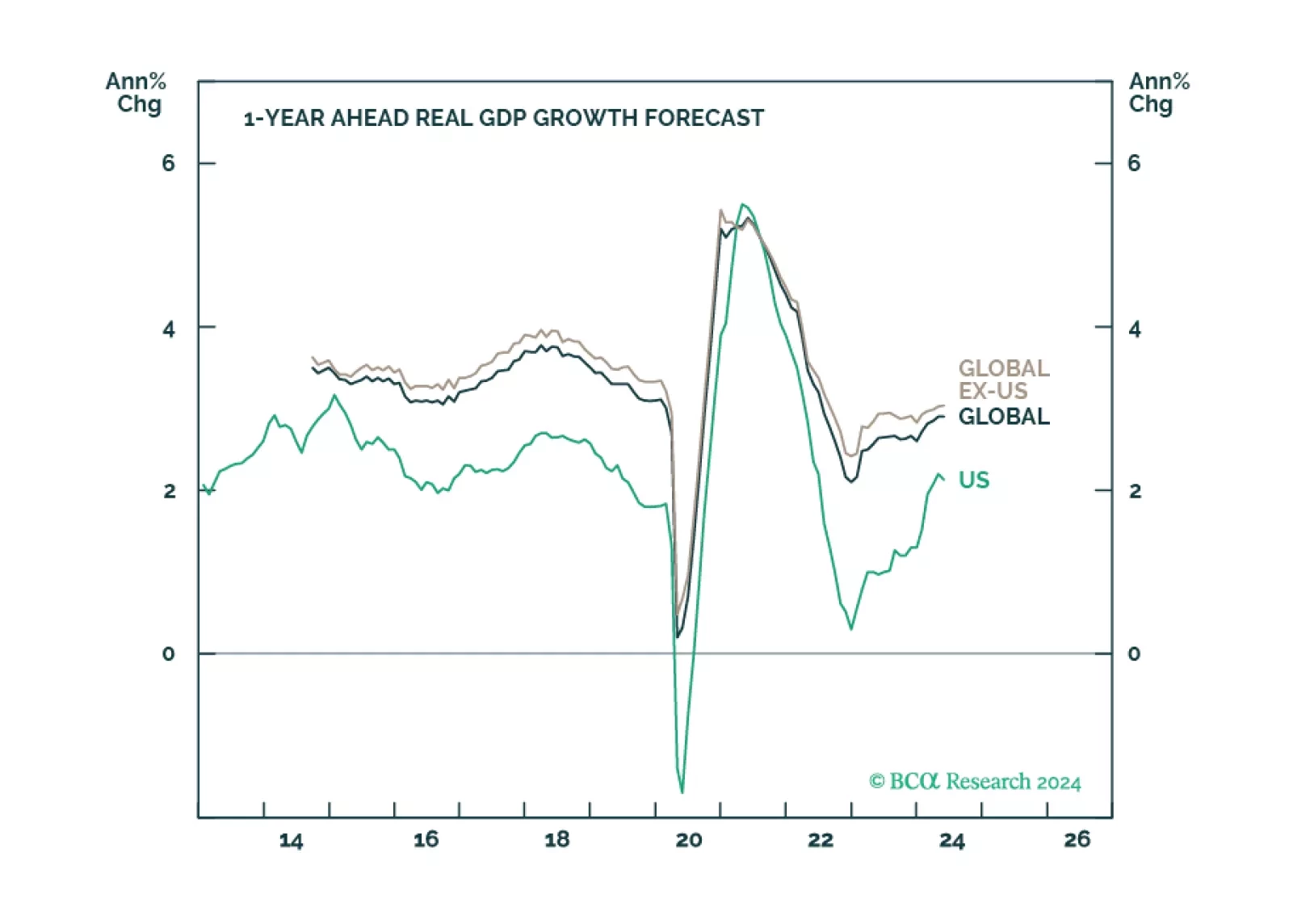

Preliminary estimates suggest that manufacturing activity generally improved across DM economies in May. Manufacturing PMIs for the US, the Eurozone, Japan and the UK all improved from their April levels. Notably, manufacturing activity started growing…

Industrial metals have outperformed the broad commodity complex this year and raced above the broad commodity complex even more meaningfully since the beginning of April. Our Commodity and Energy strategists have highlighted that the overrepresentation of…

Emerging market stocks have outperformed their global counterparts by 4 percentage points in USD terms since February according to MSCI indices. They have gotten a boost from the bounce in the global manufacturing cycle. The MSCI Emerging Market index moves…

US industrial production stalled in April against expectations of a moderate pace of growth (0.1% m/m) and March’s growth rate was revised lower from 0.4% m/m to 0.1% m/m. Notably, pro-cyclical manufacturing production unexpectedly contracted 0.3% m/m from a…

Investor and business sentiment continues to improve in the Eurozone. The ZEW Expectations series for the Eurozone (+3.1 to 47 in May) and Germany (+4.2 to 47.1, above expectations) strengthened to 27-month highs. Moreover, the spread between the expectations…