Manufacturing

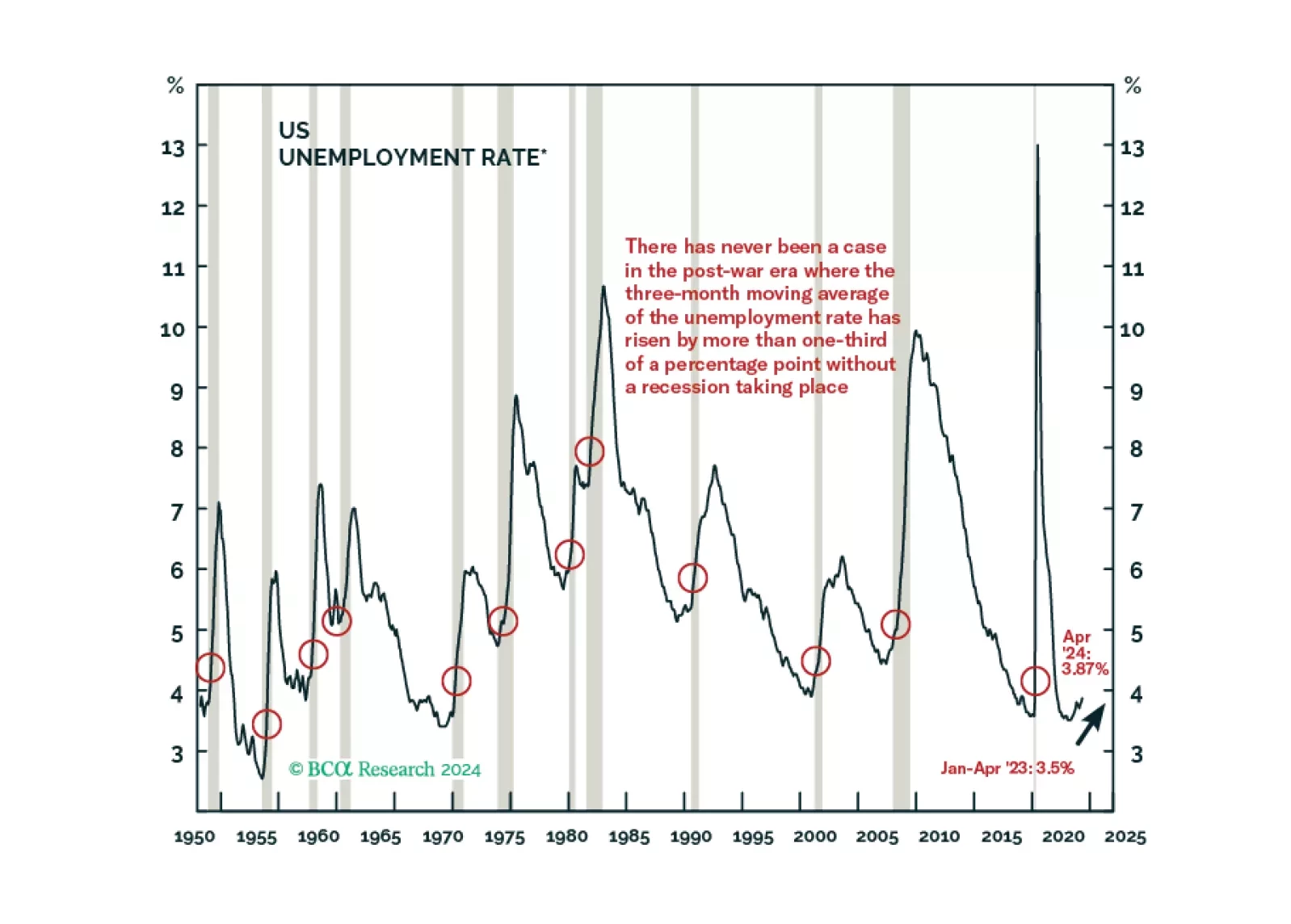

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.

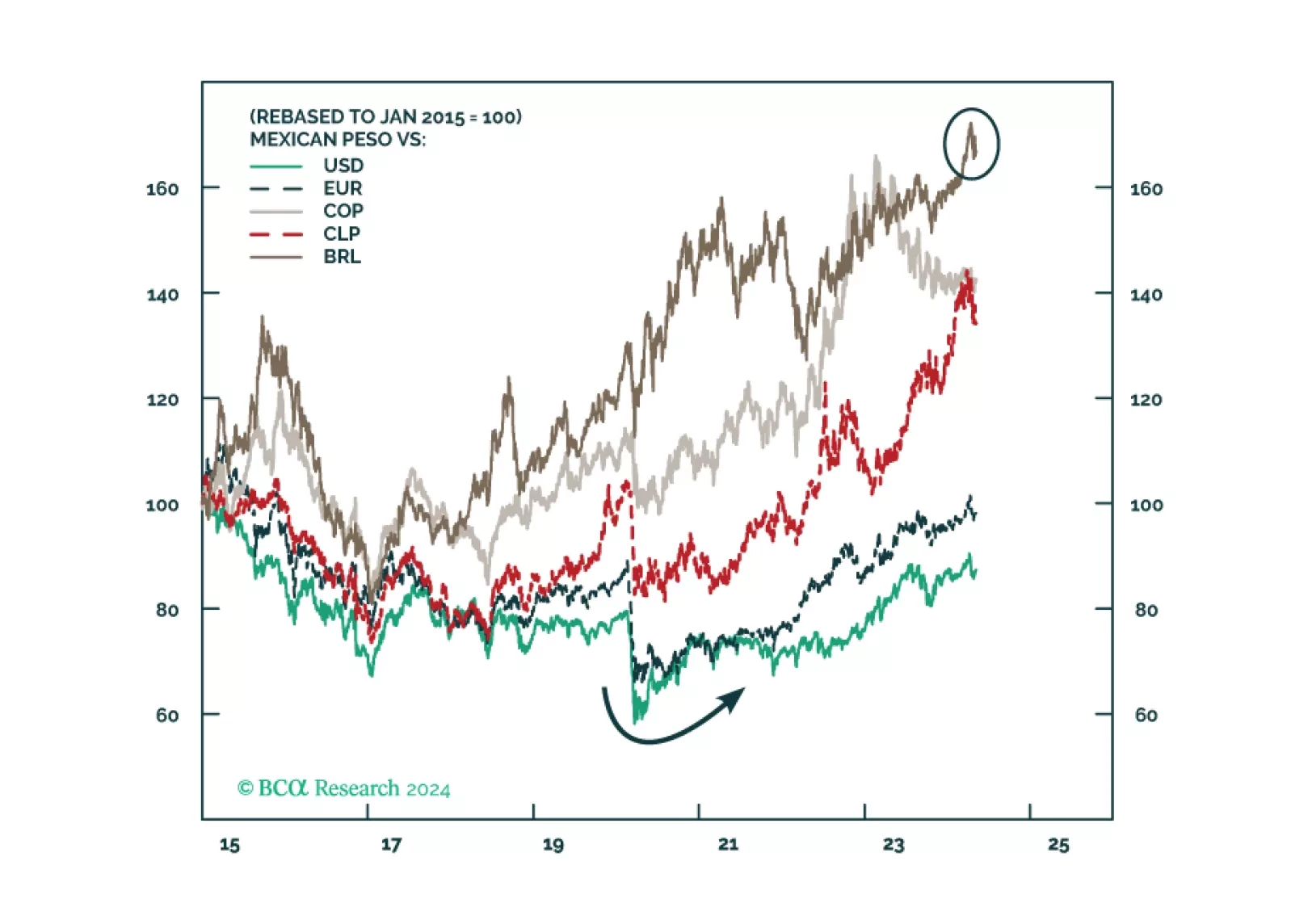

Mexico’s election and the US election pose short-term and potentially medium-term risks to Mexican financial assets. But unless the ruling party wins a double supermajority, we remain structurally overweight Mexico relative to global stocks excluding the United States.

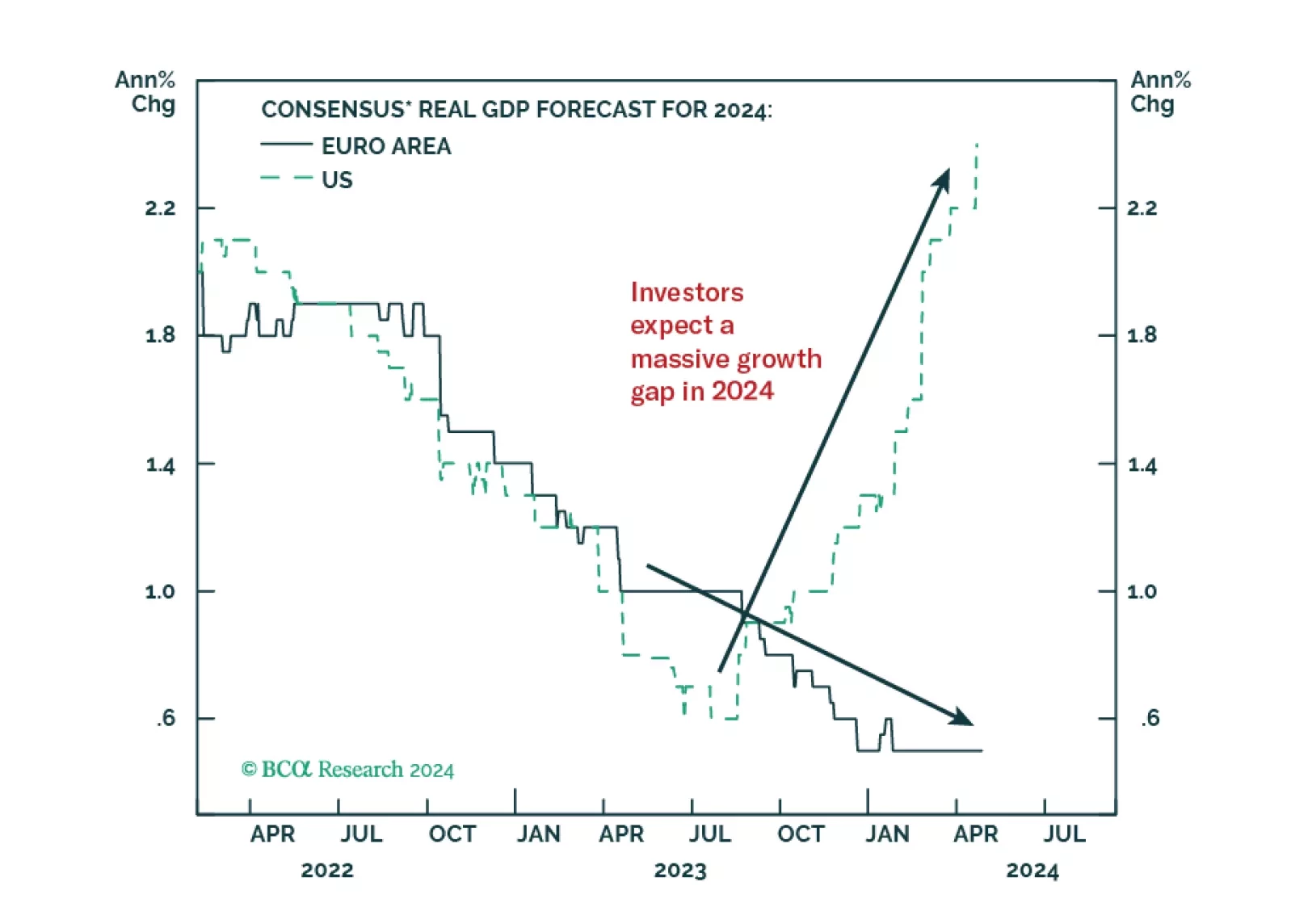

Investors anticipate a record growth gap between the US and the Eurozone in 2024. Does this skewed expectation create market opportunities?

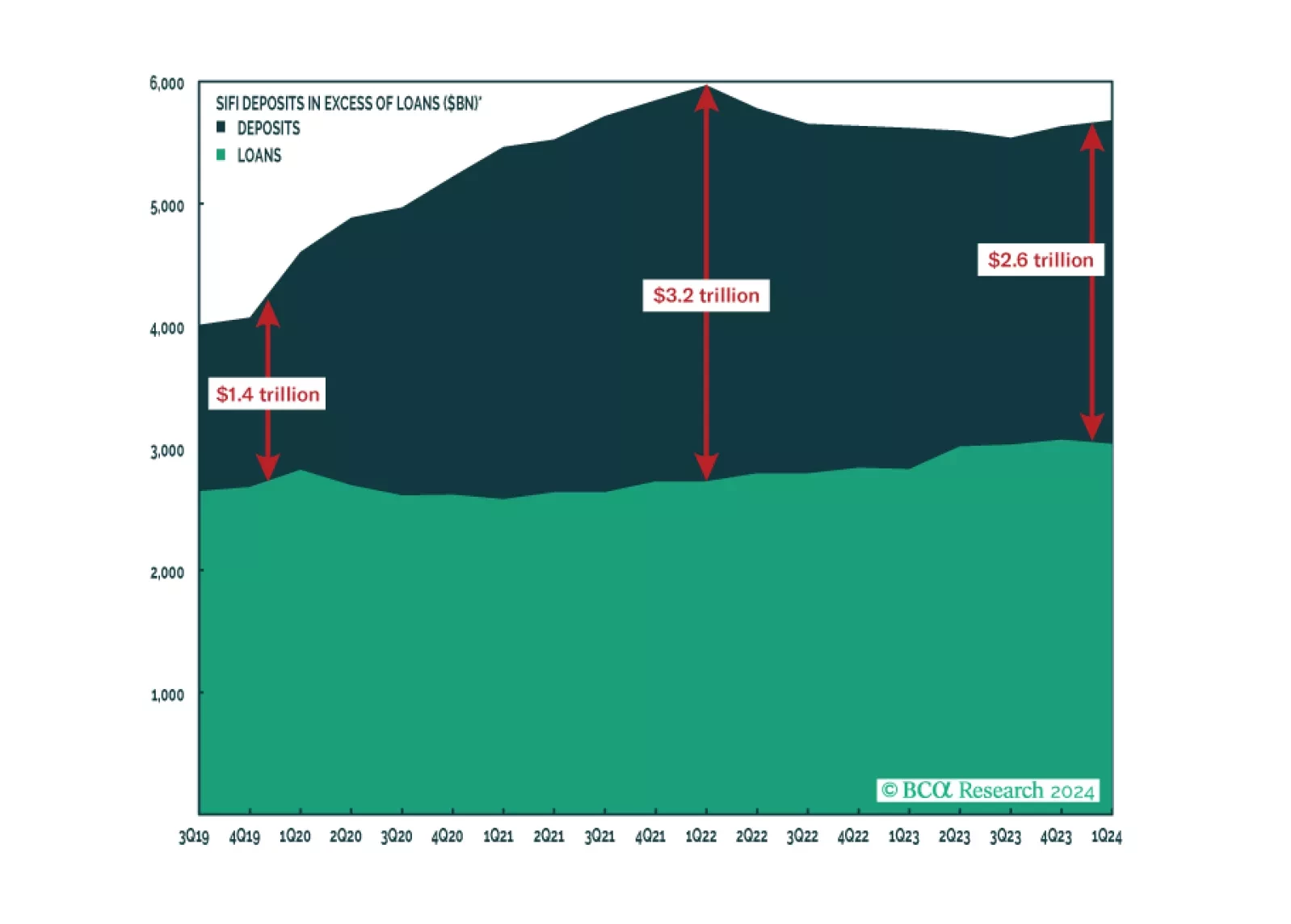

The latest edition of our Big Bank Beige Book suggests the expansion remains intact, though weakness in C’s private-label credit card portfolio could be a harbinger of distress among lower-income consumers. We remain tactically neutral with a bias to turn defensive once clearer signs of a recession emerge.