Manufacturing

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

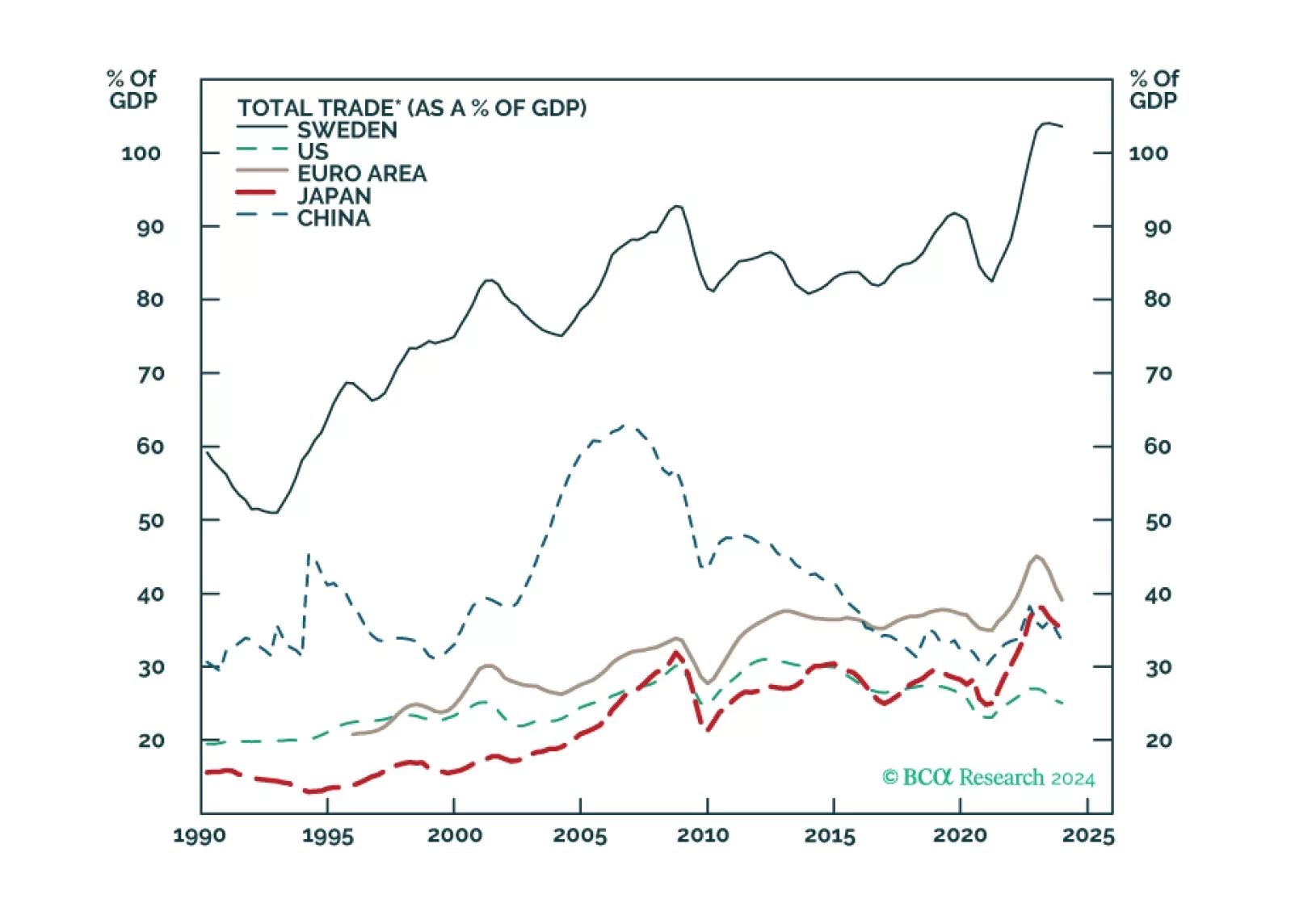

In this joint Foreign Exchange Strategy and Global Investment Strategy Special Report, we assess economic activity in Sweden, a highly cyclical and trade-oriented economy, and its implications for the global growth outlook.

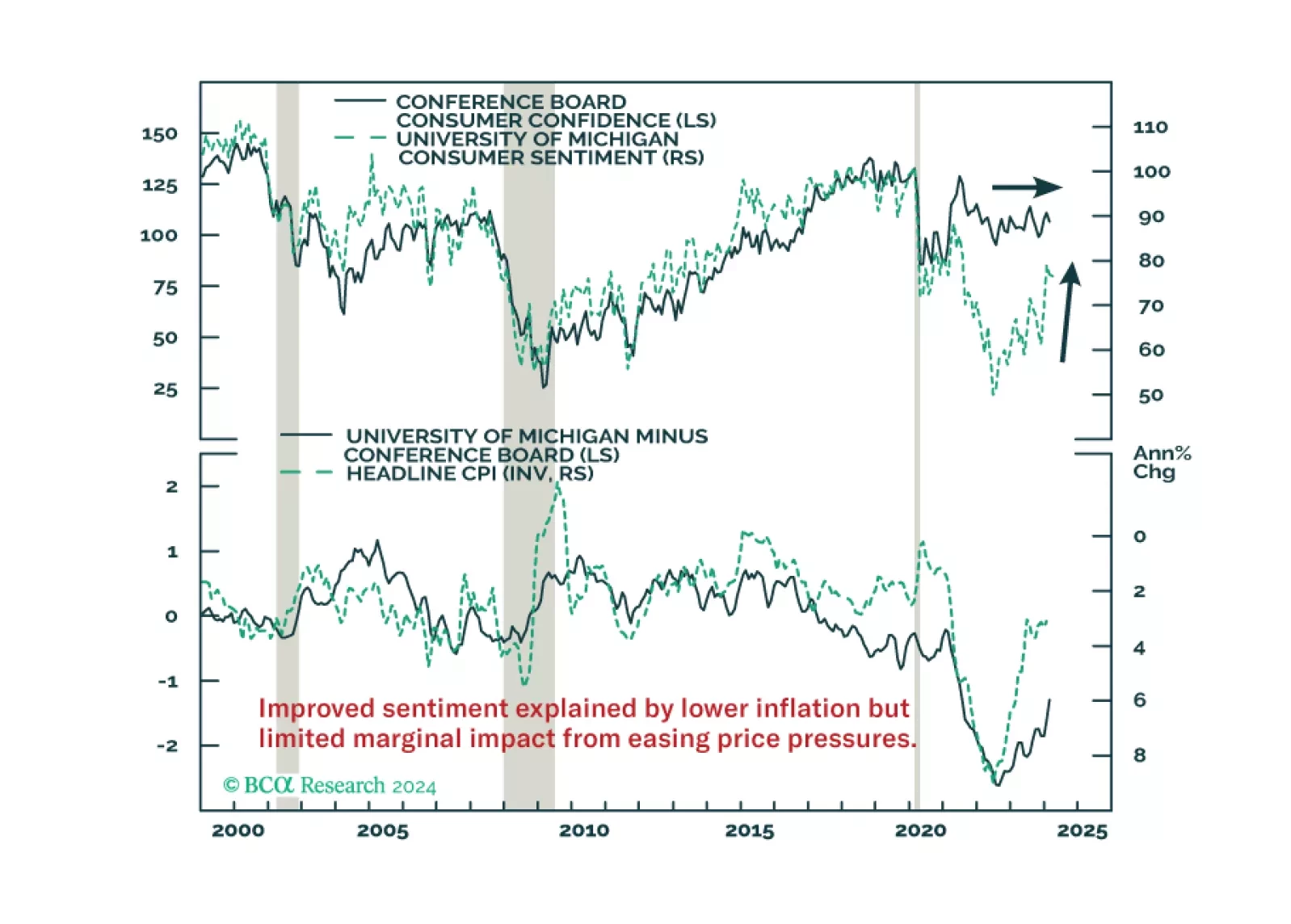

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.

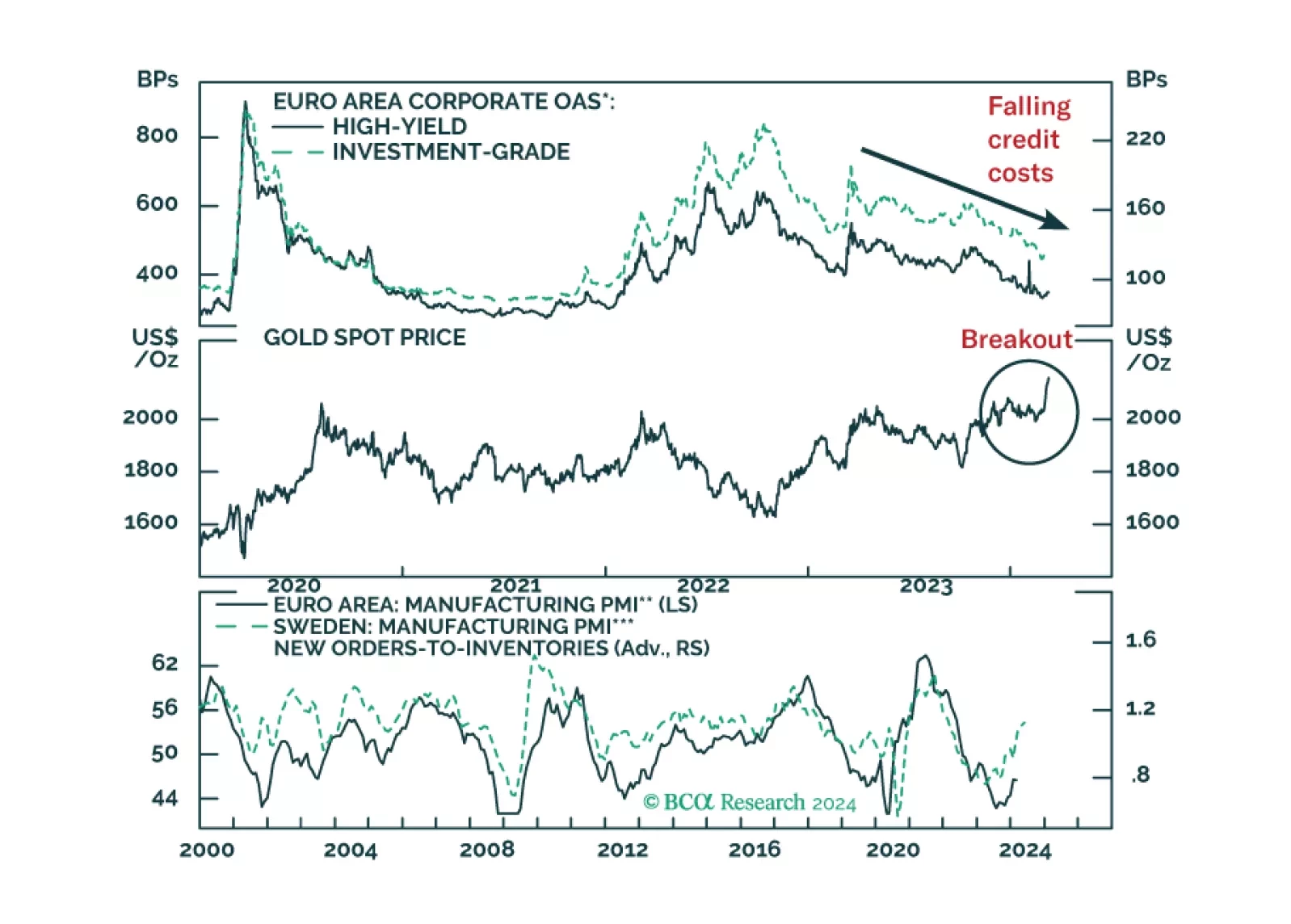

We are pushing back the anticipated start date for a Eurozone recession and assessing how it affects our equity stance.