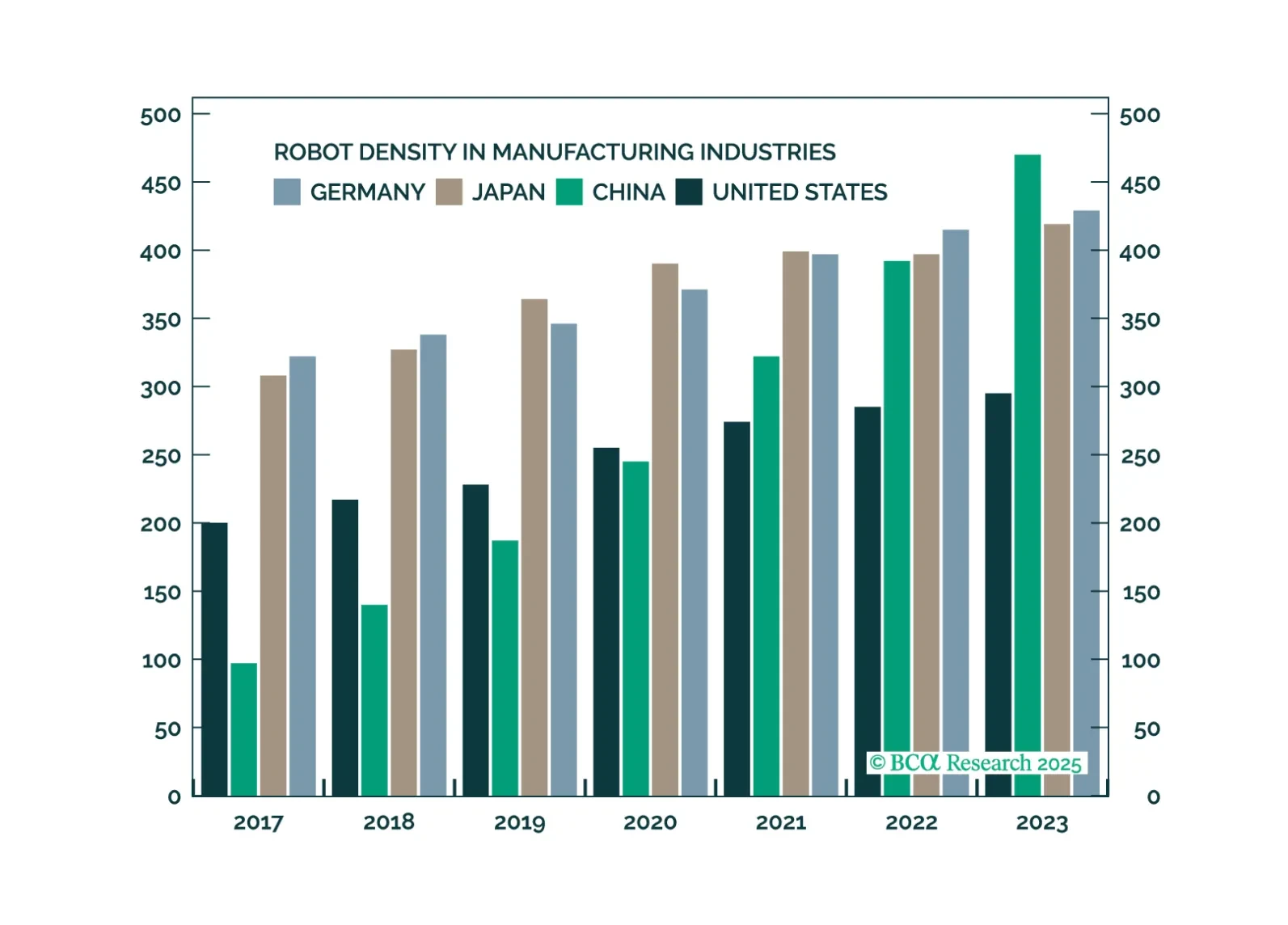

Manufacturing

Robotics is on the cusp of a new, powerful uptrend, powered by reshoring and technological breakthroughs that make robots more capable and affordable.

After considering some of the most common bullish arguments, we stand by our recession view and reiterate our defensive asset allocation recommendations.

A weakening economy will apply downward pressure to Treasury yields, but the Trump term premium will keep long-dated yields higher than they would otherwise be. This makes Treasury curve steepeners the most attractive trade in US fixed income.

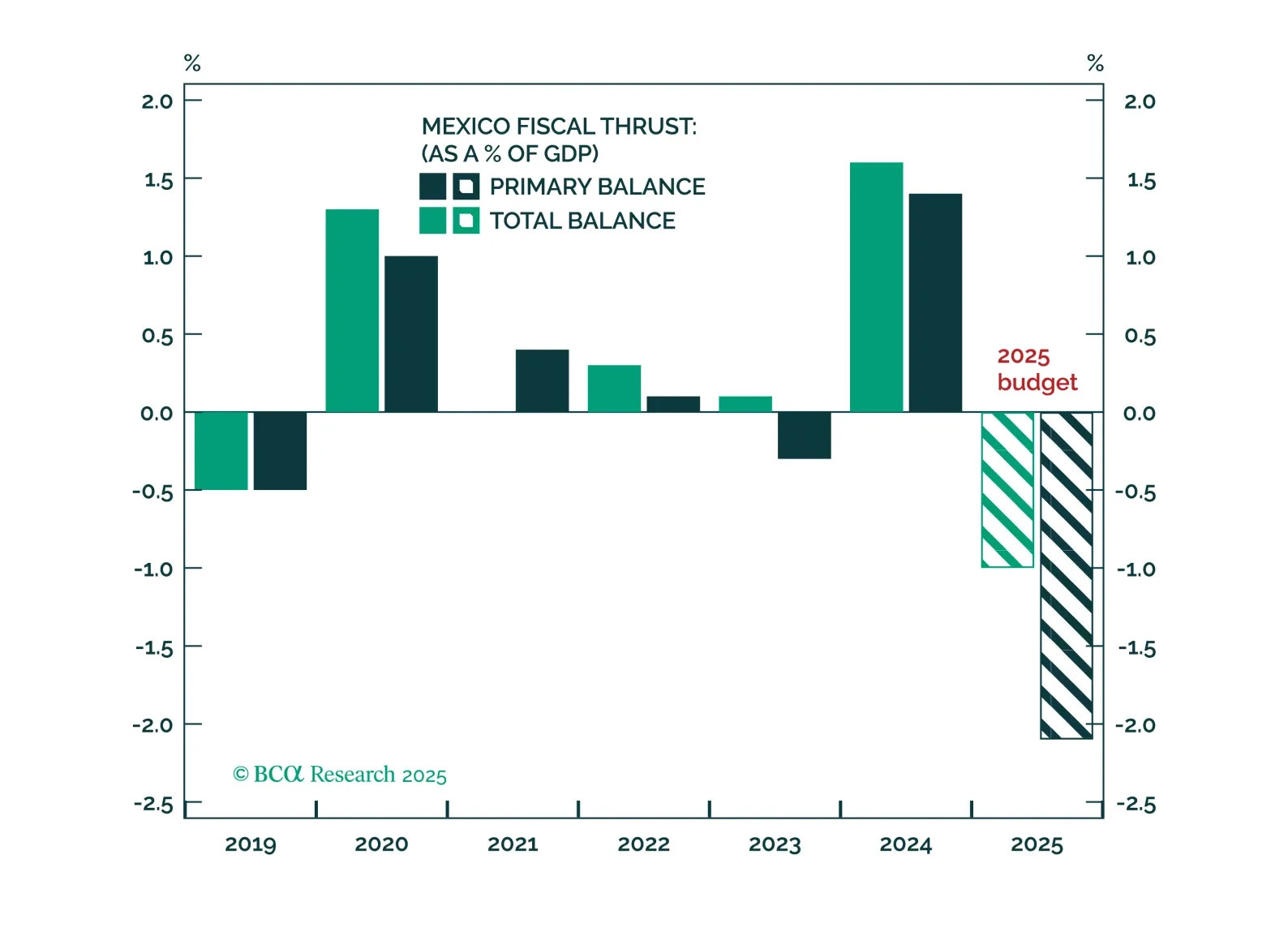

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

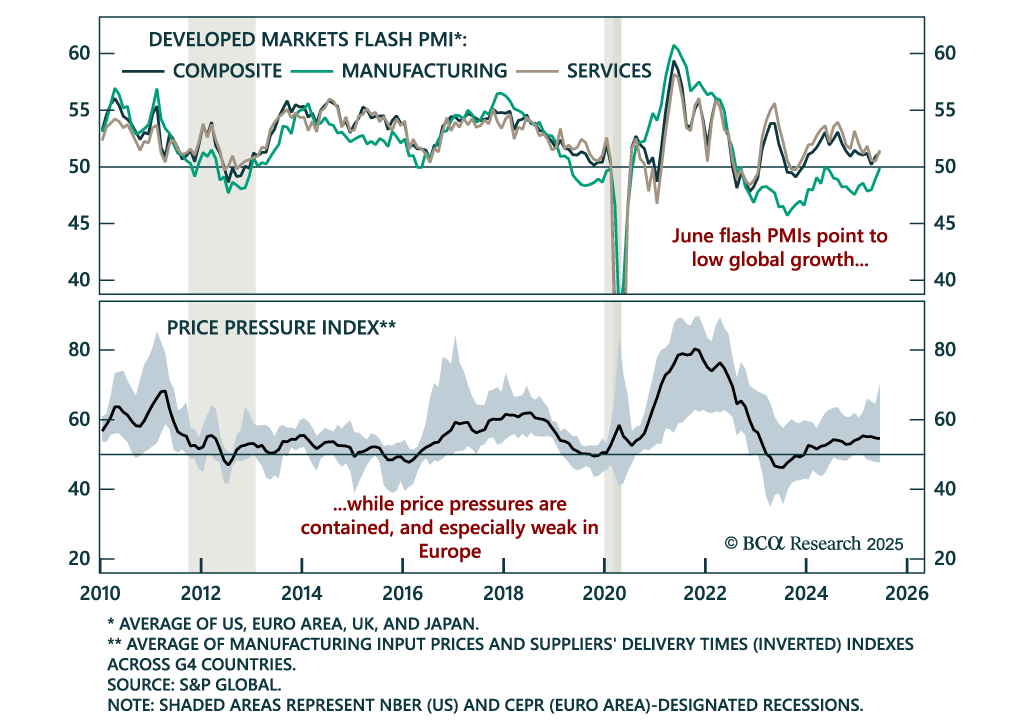

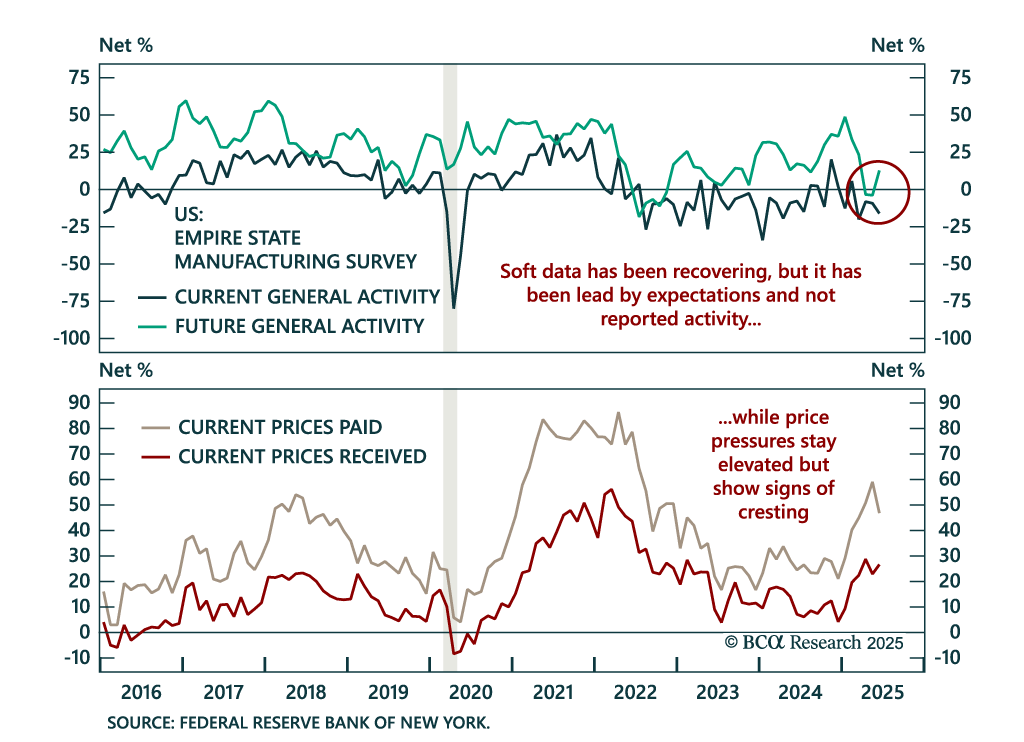

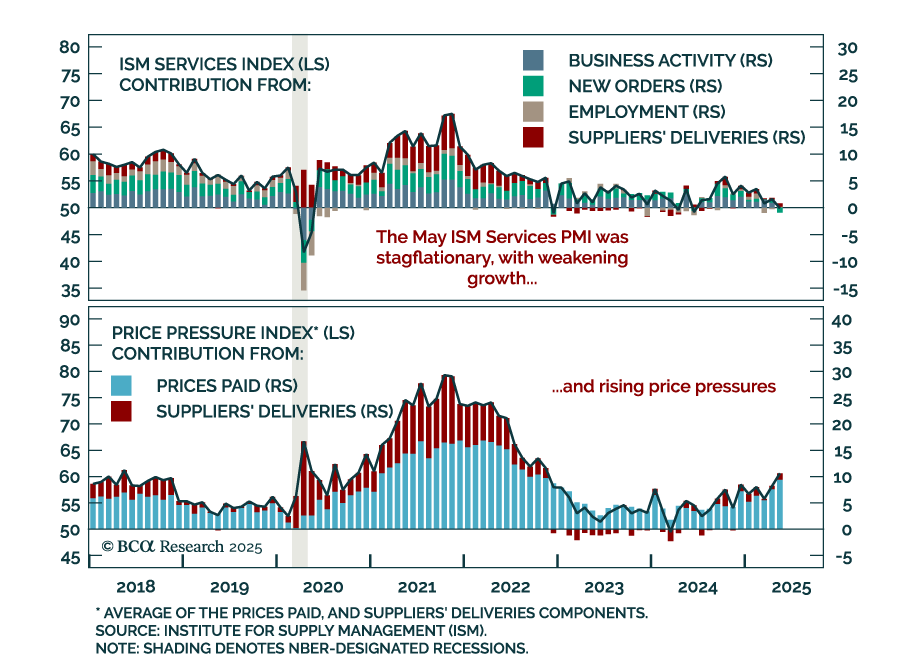

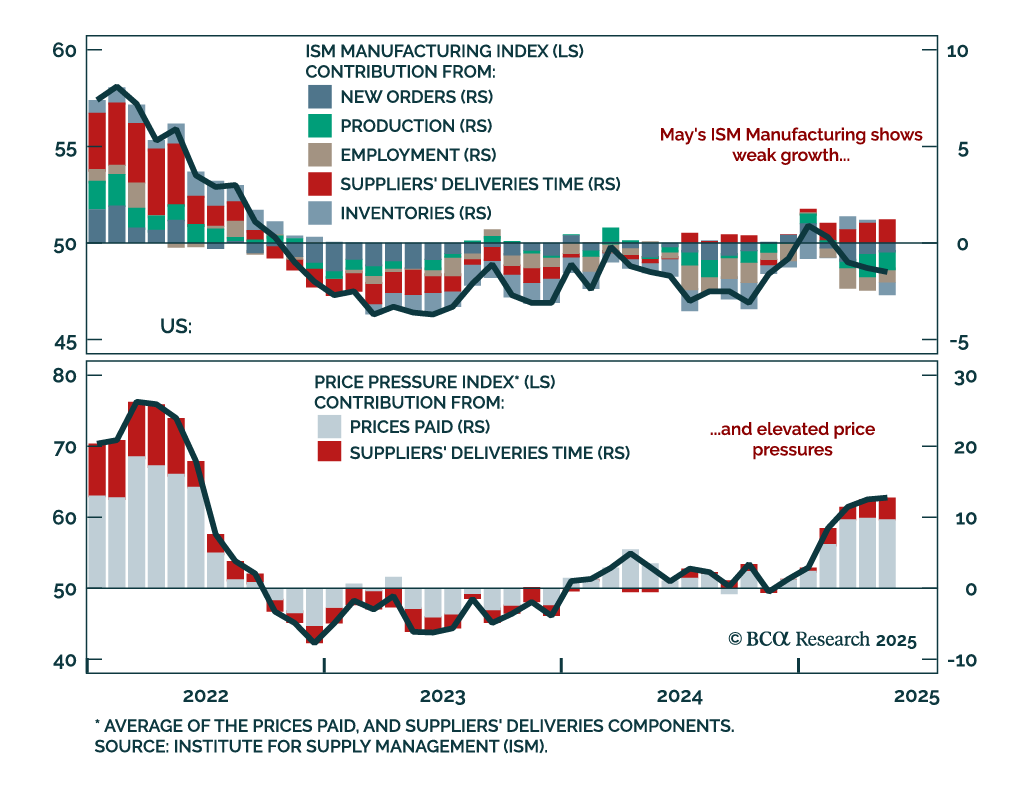

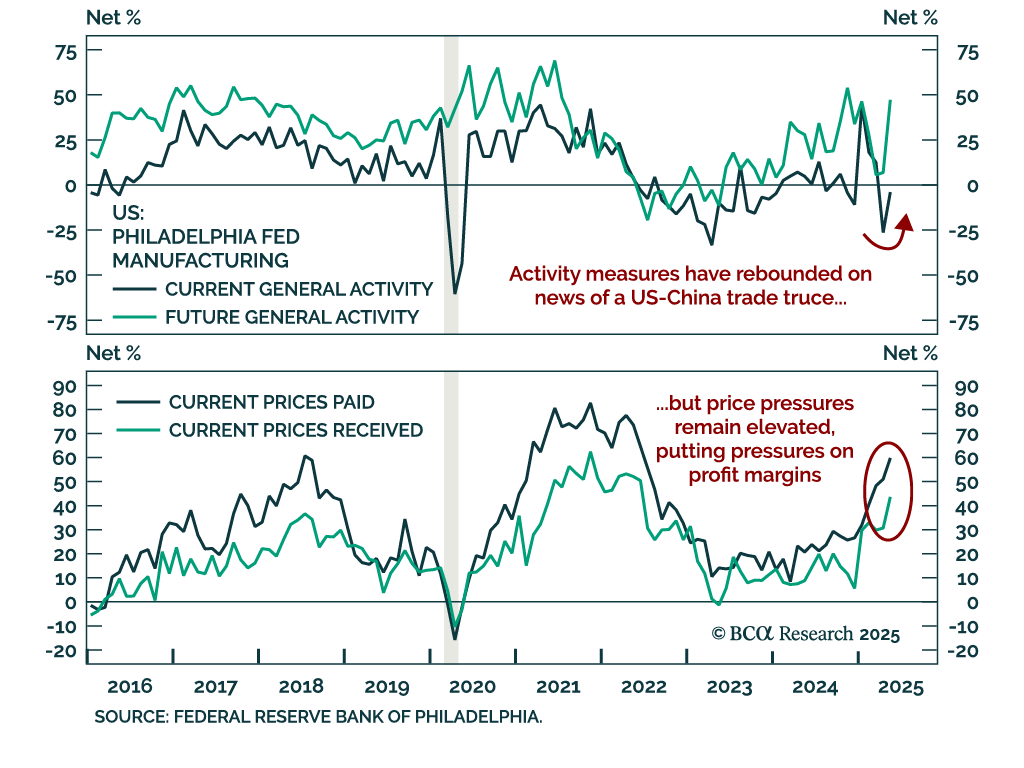

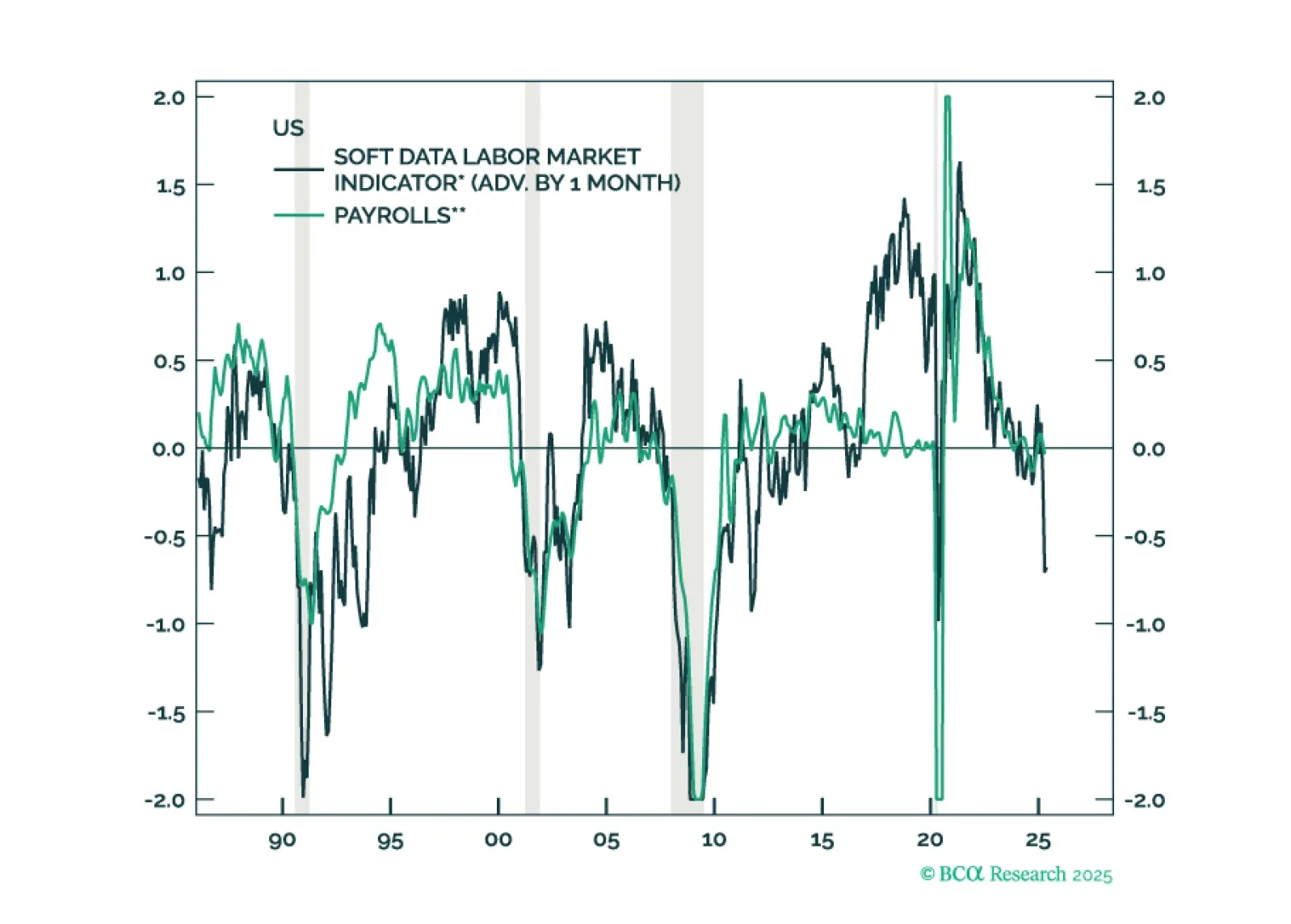

It may take several months for the tariff shock and policy uncertainty to filter through the real economy, but survey-based data are already sending a warning. Equities have priced in a lot of good news, and investors are too sanguine about the risk of a US recession.