Marine

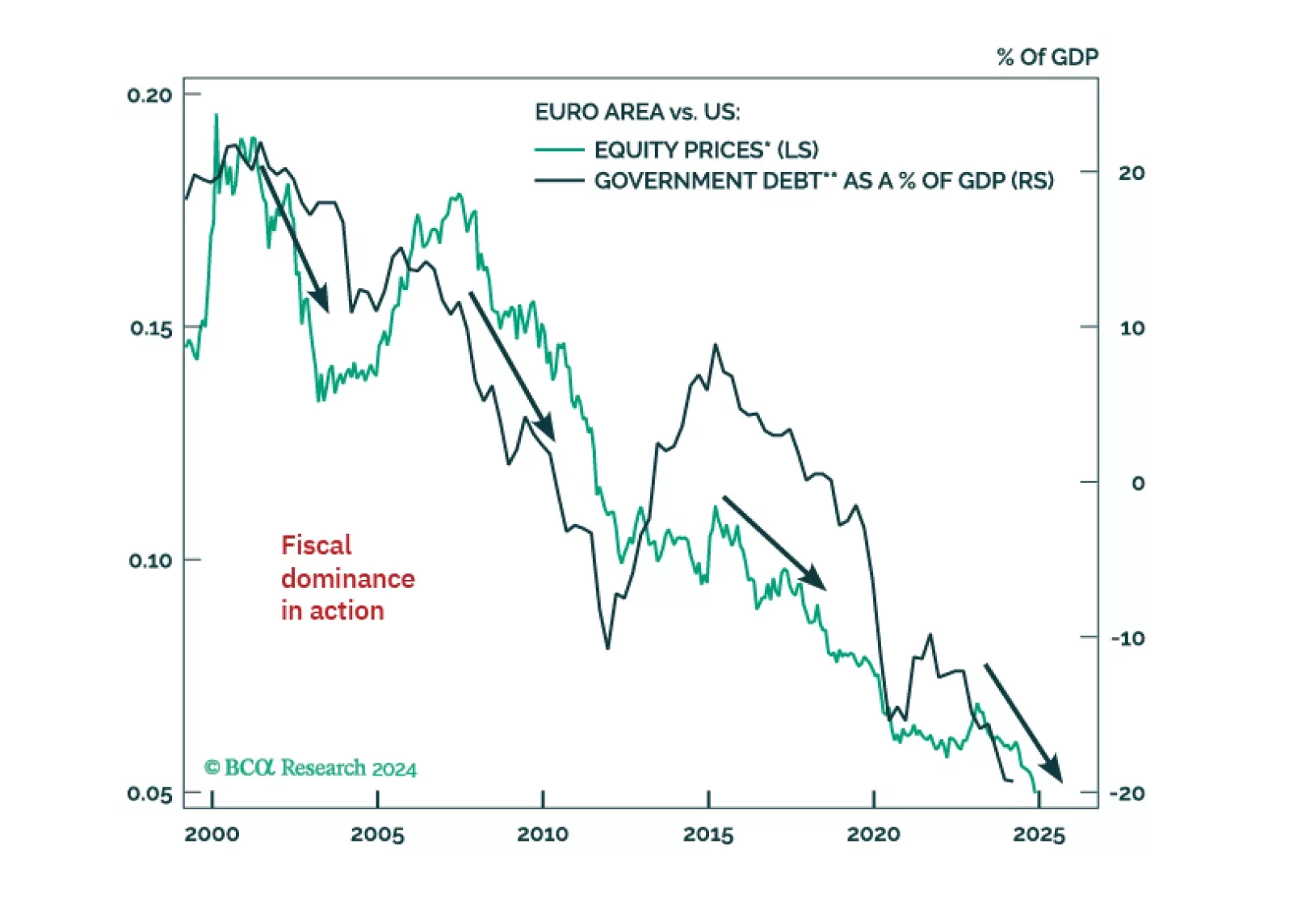

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

The 10-year Treasury yield rose in the aftermath of the Fed’s jumbo rate cut on Wednesday. Our US Bond strategists noted that this move reflects the fact that the downward revisions to the dots still fall short of the magnitude of cuts embedded in the…

The sharp recovery in global shipping rates indicates that the recovery in the global trade cycle has legs. The Harpex Shipping Index, which measures the cost of chartering a container ship is now a stone-throw away from its pre-COVID-19 highs. This is a…

Highlights The global shipping-fuels market will tighten as UN-mandated fuel standards kick in next year. This will keep ship fuels, known as bunkers, and other distillate prices – e.g., diesel and jet fuel – elevated relative to other refined products like gasoline. In turn, this will boost demand for lighter, sweeter crudes – particularly Brent and similar grades – that allow refiners to raise distillate yields, as they scramble to meet higher demand for low-sulfur ship-fuel next year. After pipeline expansions in the Permian Basin come on line later this year, WTI exports should provide the marginal light-sweet barrel refiners will need to raise distillate output next year. Light-sweet exports from the U.S. will find a ready home in the Atlantic Basin and Asia, as demand for shipping fuels – along with other distillates– rises. Still, the ramp in WTI exports from the U.S. will be hampered by a lack of deep-water ports that can accommodate very large crude carriers (VLCCs) used to ship crude oil globally. As a result, we expect the light-sweet crude market ex-U.S. to tighten. Given this expectation, we are extending our long July 2019 Brent vs. short July 2020 Brent recommendation – up 240.2% since inception January 3 – to long 2H19 Brent vs. short 2H20 Brent. Highlights Energy: Overweight. In line with our expectation, OPEC is showing no sign of agreeing to raise production less than two months after initiating output cuts to drain inventories. Separately, Muhammadu Buhari was re-elected for a second four-year term as Nigeria’s president. The main opposition party rejected the results, following record-low voter turnout, after elections were unexpectedly delayed by one week, according to the BBC. Base Metals/Bulks: Neutral. The prompt March copper contract on the CME’s COMEX is attempting to fill a gap just above $2.95/lb, which opened in July 2018 as U.S. – China trade tensions rose. Positive signals from Sino – U.S. trade talks are supporting prices. Precious Metals: Neutral. Palladium traded to a record high of $1,536.50/oz Monday, pushing it more than $200/oz over gold. Platinum prices also rallied, as South African miners were notified by labor unions of intended strikes next week. Russia’s leading producer, Norilsk Nickel, which accounts for 40% of global palladium production, expects an 800k-ounce physical deficit in 2019, according to Reuters. Ags/Softs: Underweight. U.S. President Donald Trump said he would delay increasing U.S. tariffs on Chinese imports. Trump also said he expects to meet China’s President Xi Jinping to conclude the trade deal they’ve been negotiating if both sides continue to make progress. Feature Maritime shipping represents ~ 80% of international trade, and is responsible for roughly 90% of the total sulfur emissions from the transportation sector. In 2008, the UN’s International Maritime Organization (IMO) adopted a new regulation to reduce the cap for sulfur content of ships’ fuel oil – known as bunker fuel – to 3.5% from 4.5% in 2012, and to 0.5% from 3.5% in 2020 (Chart 1).1 Chart of the WeekReducing Marine Sulfur Pollution Requires Higher-Priced Low-Sulfur Fuels Around 50% of the cost of shipping is fuel costs. This amounts to more than 4mm b/d of bunker fuel (~ 3.5mm b/d of High-Sulfur Fuel Oil, or HSFO, and ~ 0.8mm b/d of marine gasoil, known as MGO). Hence, the IMO 2020 regs threaten demand of ~ 3.5mm b/d of HSFO. As the January 1, 2020, IMO deadline approaches, uncertainty surrounding the new regs remains elevated. On the demand side, shippers have the option to install abatement technology (i.e., scrubbers); burn IMO 2020-compliant fuels like MGO; use liquefied natural gas (LNG) as a fuel on ships; or do nothing, i.e., not comply with the regulation. Refiners on the supply side have to adjust via a combination of increasing MGO and Low-Sulfur Fuel Oil (LSFO) production; modifying their crude slates, which will favor lighter, sweeter crudes like Brent and WTI; building additional refining capacity; or running their units harder – i.e., increase refinery utilization rates – to produce more fuel. Demand for bunkers is the only part of the HSFO market that is growing. IMO 2020 removes the all-important shipping consumer of residual fuel oil, which will have a major impact on simple refineries, and will force a dramatic reconfiguration of the shipping and refining industries. To date, shippers and refiners have been slow to implement required changes as market participants have an incentive to move last.2 We agree with a recent McKinsey analysis, which notes the simplest solution for shippers is to switch to MGO.3 We also could see an uptick in demand for LSFO with sulfur content below the 0.5% limit for blending purposes. This would push demand for the lower-sulfur fuels and prices up. It also would pressure HSFO prices lower over the short term, to the point where this fuel can compete in the utility sector as a fuel, or in the refining sector as a charging stock for complex refiners. The IEA expects MGO consumption to rise from 0.8mm b/d to 1.7mm b/d in 2020.4 Complex Refiners, Light-Sweet Crude Producers Benefit Moving to LSFO and MGO shifts the burden of IMO 2020 to the refining market. According to the IEA, around 80% of the sulfur content in crude is removed from the final product. Once IMO 2020 is implemented, this will rise to 90%. In the lead-up to the IMO 2020 deadline, refiners are adjusting their crude slates to minimize residual fuel and maximize distillate output. As a result, demand for light-sweet crudes like Brent and WTI – the crude being produced in ever-rising quantities in the U.S. shales – will increase. At the same time, heavier crudes exported by Venezuela and GCC states will see demand fall, which means the spread between these crudes will favor the lighter, sweeter barrel, all else equal.5 Simple refineries incapable of cracking the complex heavy-sour crudes favored by U.S. Gulf Coast refiners will either have to upgrade, close, or use low-sulfur crude as a charging-stock input. According to McKinsey, the switch to marine gasoil will lead to an increase of 1.5mm b/d of distillate demand. This represents ~ 2.2 to 2.7mm b/d of increased demand for light-sweet oil. The IEA estimates diesel prices could rise by 20 – 30%, as a result.6 This increased demand for low-sulfur bunkers – MGO in particular –will keep prices for distillates generally well supported over the next year or so at the expense of HSFO. S&P Global Platts reported this week the first physical trade for U.S. Gulf Coast 0.5% MGO was done in its official trading window at $67.70/bbl, a $3.75/bbl premium to HSFO.7 IMO 2020 will keep distillates the star performers for refiners. Distillate crack spreads – most visible in the ultra-low-sulfur diesel (ULSD) cracks employing the CME’s NY Harbor ULSD futures vs. WTI and Brent – recently were trading $16/bbl over gasoline cracks using the Exchange’s RBOB futures (Charts 2A and 2B). We expect these cracks to remain wide, to incentivize more distillate-production capacity. Chart 2ABrent Diesel And Gasoline Cracks Likely Trade > $14/bbl Wide Chart 2BBrent Diesel Cracks Will Remain Elevated Following IMO 2020 Prices for other distillates also will be supported by IMO 2020 – e.g., jet fuel – over the coming year, given the high correlation of products within this cut of the barrel. These distillate prices also are highly correlated with Brent and WTI prices, as can be seen in Chart 3, and in Tables 1 and 2. These high correlations likely will persist as IMO 2020 is implemented, and hedgers seek out liquid markets in which to shed their price risk.8 Chart 3Global Distillate Prices Will Be Supported by IMO 2020Table 1Distillate Fuels’ Correlations Remain High Around The WorldTable 2Percent Changes In Distillates Also Are Highly Correlated Baker & O’Brien, an energy consultancy based in Dallas, Texas, expects a number of factors – ranging from non-compliance with IMO 2020; increased use of scrubbers to capture sulfur-oxide emissions; blending to make IMO 2020-compliant marine fuel; upgrades by refiners and changes in their crude slates – will lead to lower prices once the market adjusts to the new regs.9 We do not disagree, but the timing on this likely hinges on how quickly U.S. light-sweet crude oil exports ramp up. Investment Implications WTI exports – actually LTO exports from U.S. shales – will provide the marginal light-sweet barrel refiners will need to raise distillate output next year. As a result, LTO exports from the U.S. will find a ready home in the Atlantic Basin and Asia, as demand for low-sulfur shipping fuels increases. However, this will not happen overnight. At present WTI exports from the U.S. are hampered by a lack of deep-water ports that can accommodate the VLCCs used to ship crude oil. The 2mm b/d of expanded pipeline capacity out of the Permian by the end of this year will move the U.S. crude-oil bottleneck from the Permian to the U.S. Gulf.10 So, as refiners prepare this year for the IMO 2020 regs effective January 1, 2020, the light-sweet crude market ex-U.S. – particularly Brent– will tighten. This already is visible in the backwardation we were expecting at the beginning of this year, when we recommended getting long July 2019 Brent vs. short July 2020 Brent, which is up 240.2% since inception on January 3. Given our expectation for a tighter light-sweet crude market ex-U.S., we are liquidating our existing Brent 2019 long position vs. a short position in July 2020 at tonight’s close, and replacing it with a long 2H19 Brent vs. a short 2H20 Brent position.11 Bottom Line: The implementation of IMO 2020 will tighten marine fuels markets globally, as refiners increase their demand for light-sweet crude oil and shippers most likely increase their demand for MGO and lower-sulfur fuels generally. Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Footnotes 1 The regulation is part of Annex VI to the International Convention for the Prevention of Pollution from Ships (MARPOL). Following the adoption of the regulation in 2008, a provision was kept in order to review the compliant fuel availability and possibly push the implementation to 2025. In October 2016, the IMO’s Marine Environment Protection Committee confirmed the final implementation date (January 1, 2020) following a positive assessment of the availability for shippers of compliant fuels. Any amendment to MARPOL needs to be circulated for a minimum of six months, and can only be implemented 16 months after adoption, therefore, no legal amendment to the current January 2020 date are possible. Please see https://www.iea.org/etp/tracking2017/internationalshipping/ 2 The slow response by refiners can be explained by: (1) the fact that a switch to LSFO or MGO prior to the actual deadline would lead to a financial loss due to the current high price of LSFO and MGO vs. HSFO; (2) abatement technology requires large upfront investments (i.e. capital cost of new processing units, storage tanks, loss of revenue from laying ships in dry dock while they are retrofitted, and a permanent loss of deck space and loading capacity to the new equipment); and (3) the unpredictability of fuel prices and the endogenous relationship between other shippers and the behavior of prices. In other words, trying to get out in front of the official implementation of IMO 2020 leads to unnecessary financial burdens and to competitive disadvantage. Please see Halff, Antoine, Lara Younes, Tim Boersma (2019), “The Likely Implications of the new IMO standards on the shipping industry.” Energy Policy, 126: 277 - 286. 3 Please see “IMO 2020 and the outlook for marine fuels,” published by McKinsey & Company, September 2018. S&P Global Platts reaches a similar conclusion in a report entitled “Turning tides, the future of fuel oil after IMO 2020,” which was released this month. Platts notes, “The IMO’s lower sulphur cap is set to take away the bulk of marine fuel oil demand from the start of next year. Most ship owners and operators will switch to burning new low-sulfur bunker blends, translating into an almost overnight shift of 3 million b/d of demand.” 4 The IEA expects 30% of the current HSFO bunker demand will switch to marine gasoil (MGO), 30% of the HSFO bunker demand will switch to the new ultra low 0.5% sulphur fuel (ULSFO), and 40% of HSFO bunker demand will remain.) In the IEA’s modeling, this could push prices up by as much as 30%. Please see “Oil 2018: Analysis and forecasts to 2023” published by the IEA. It is available at iea.org 5 Please see “IMO 2020 and the Brent – Dubai Spread,” published by The Oxford Institute For Energy Studies in September 2018. Of course, reducing the export of heavy-sour crudes, as has been done by the Gulf Arab members of OPEC will keep the Brent – Dubai spread tighter than pure economics would dictate. 6 Please see sources in footnotes 3 and 4. 7 This trade was done in the Platts Market on Close assessment. Please see “USGC Marine Fuel 0.5% has first physical trade in Platts MOC process,” published by S&P Global Platts February 26, 2019. 8 These are short-term correlations, which use daily data from 2017 to now. We present correlations in levels and in percent-changes, given these are cointegrated variables. Please see section 3.3 of “Correlation, regression, and cointegration of nonstationary economic time series,” by Soren Johansen, published November 6, 2007, by the Center for Research in Econometric Analysis of Time Series at the University of Aarhus. 9 Please see “The Thunder Rolls – IMO 2020 And The Need For Increased Global Oil Refinery Runs (Part 3)” published by Baker & O’Brien, December 11, 2018. 10 An additional 1mm b/d of new takeaway is scheduled for 1H21, following a final investment decision from an Exxon-led group that will move Permian Basin LTO to the U.S. Gulf. This came one day after Exxon FID’d a 250k b/d buildout of its Beaumont refinery in Houston, which will increase capacity by more than 65%, Natural Gas Intelligence reported January 30. 11 Please see EIA’s This Week in Petroleum report titled “Upcoming changes in marine fuel sulfur limits will affect crude oil and petroleum product markets,” published January 16, 2019. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in Summary of Closed Trades