Market Returns

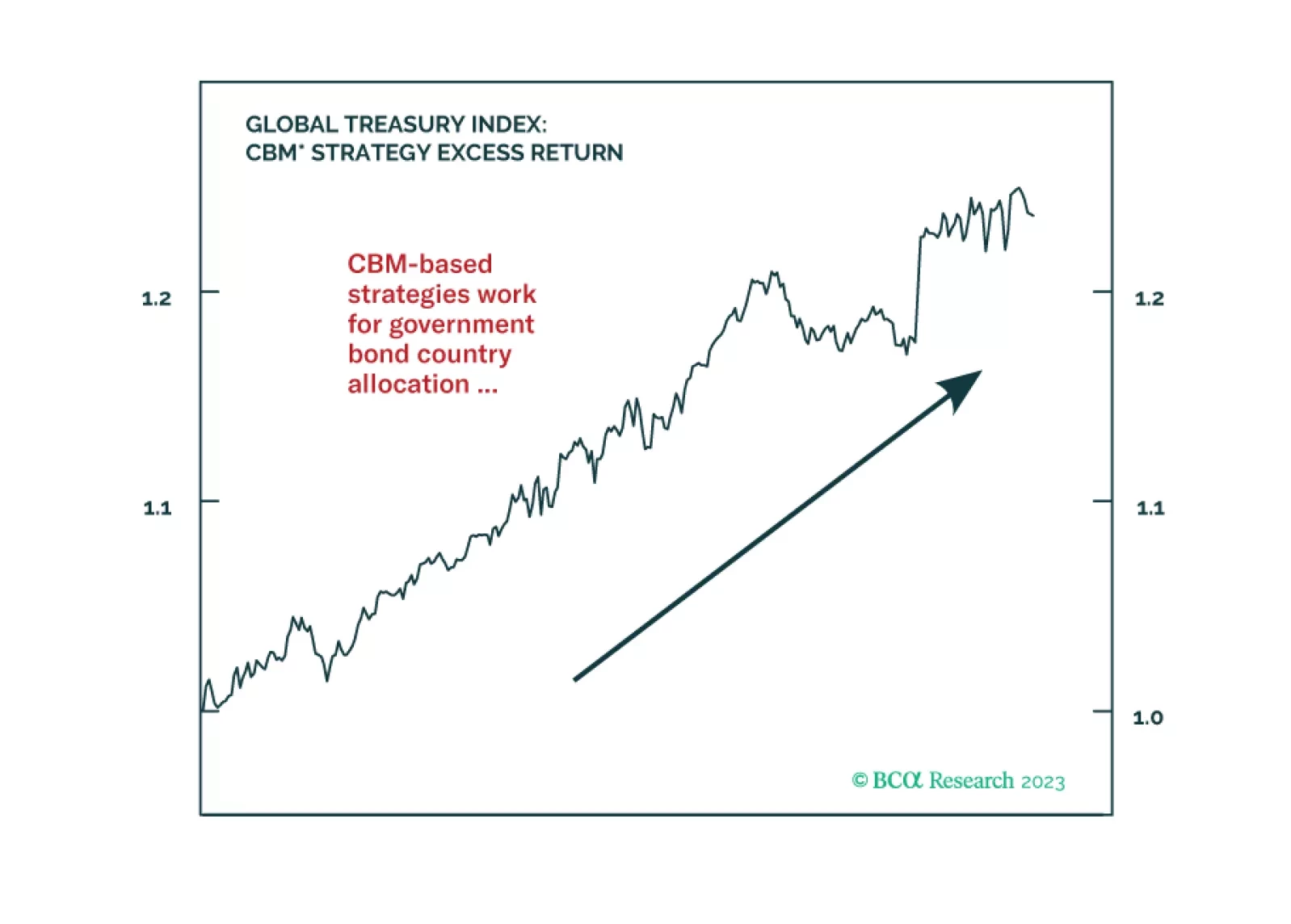

In this Special Report, we introduce two strategies that use our Central Bank Monitors for global fixed income country allocations and currency trades. We find that using the Monitors in country selection helps improve the performance of a developed markets government bond portfolio. The CBMs can also help substantially minimize the drawdowns on a standard FX carry strategy.

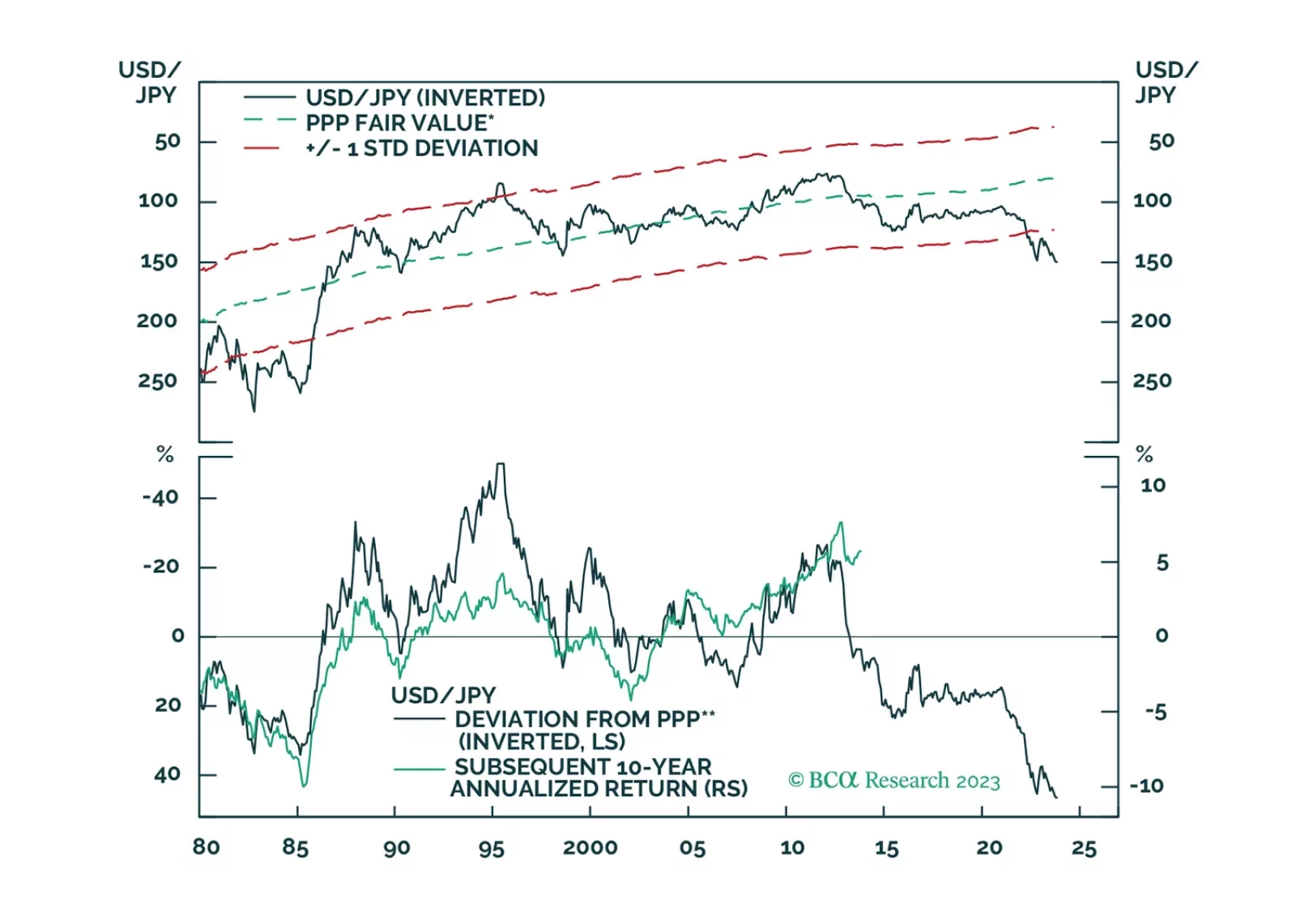

There is a high probability that the global economy will tip into recession in the second half of 2024. A long yen position is an excellent hedge against that risk.

US monetary policy is restrictive, as evidenced by a falling jobs-workers gap. The reason that unemployment has not risen is because labor demand still exceeds supply. That will change in the second half of 2024 when the US economy succumbs to recession. Investors should increasingly favor bonds over stocks.

In this update to the two Special Reports on FX hedging of global equity portfolios with nine different home currencies, published in 2017, we show that BCA’s proprietary dynamic FX hedging strategies have consistently added value to global equity portfolios. We value quant models as an important input in our decision-making process, but we do not suggest any investor to slavishly follow them, because models cannot capture all the important fundamental changes, as demonstrated in the details of this report.

We do not see a 1990s type of backdrop but we do see a departure from the 2010s. Structural forces make it unlikely that we will return to the 1990s heydays for LSE. However, evolving cyclical forces provide tailwinds over the next market cycle. In this Special Report we provide a quantitative assessment of what investors can expect.

While Chinese stocks have low valuations and are oversold, their attractiveness is dampened by uncertainties in the magnitude of stimulus and the dismal outlook for corporate profits in the next six to nine months.

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

In part 2 of this series, we discuss mainstream EM equity valuations and present the results of our cross-country analysis. The goal is to identify overweights and underweights within an EM equity portfolio.