Mega Themes

Highlights Global equities are poised to deliver mid-to-high single-digit returns this year, with the outlook turning bleaker in 2023 and beyond. Non-US markets are likely to outperform. We examine the four pillars that have historically underpinned stock market performance. Pillar 1: Technically, the outlook for equities is modestly bullish, as investor sentiment is nowhere near as optimistic as it usually gets near market tops. Pillar 2: The outlook for economic growth and corporate earnings is modestly bullish as well. While global growth is slowing, it will remain solidly above trend in 2022. Pillar 3: Monetary and financial conditions are neutral. The Fed and a number of other central banks are set to raise rates and begin unwinding asset purchases this year. However, monetary policy will remain highly accommodative well into 2023. Pillar 4: Valuations are bearish in the US and neutral elsewhere. Investors should avoid tech stocks in 2022, focusing instead on banks and deep cyclicals, which are more attractively priced. The Bedrock For Equities In assessing the outlook for the stock market, our research has focused on four pillars: 1) Sentiment and other technical factors, which are most pertinent for stocks over short-term horizons of about three months; 2) cyclical fluctuations in economic growth and corporate earnings, which tend to dictate the path for stocks over medium-term horizons of about 12 months; 3) monetary and financial conditions, which are also most relevant over medium-term horizons; and finally 4) valuations, which tend to drive stocks over the long run. In this report, we examine all four pillars, concluding that global equities are likely to deliver mid-to-high single-digit returns this year, with the outlook turning bleaker in 2023 and beyond. Pillar 1: Sentiment And Other Technical Factors (Modestly Bullish) Chart 1US Equities: Breadth Is A Concern

US Equities: Breadth Is A Concern

US Equities: Breadth Is A Concern

Scaling The Wall Of Worry Stocks started the year on a high note, before tumbling on Wednesday following the release of the Fed minutes. Market breadth going into the year was quite poor. Even as the S&P 500 hit a record high on Tuesday, only 57% of NYSE stocks and 38% of NASDAQ stocks were trading above their 200-day moving averages compared to over 90% at the start of 2021 (Chart 1). The US stock market had become increasingly supported by a handful of mega-cap tech stocks, a potentially dangerous situation in an environment where bond yields are rising and stay-at-home restrictions are apt to ease (more on this later). That said, market tops often occur when sentiment reaches euphoric levels. That was not the case going into 2022 and it is certainly not the case after this week's sell-off. The number of bears exceeded the number of bulls in the AAII survey this week and in six of the past seven weeks (Chart 2). The share of financial advisors registering a bullish bias declined by 25 percentage points over the course of 2021 in the Investors Intelligence poll. Option pricing is far from complacent. The VIX stands at 19.6, above its post-GFC median of 16.7. According to the Minneapolis Fed’s market-based probabilities model, the market was discounting a slightly negative 12-month return for the S&P 500 as of end-2021, with a 3.6 percentage-point larger chance of a 20% decline in the index than a 20% increase (Chart 3). Chart 3Option Pricing Is Not Pointing To Elevated Complacency

Option Pricing Is Not Pointing To Elevated Complacency

Option Pricing Is Not Pointing To Elevated Complacency

Chart 2Sentiment Is Not Exceptionally Bullish, Despite The S&P 500 Trading Close To All-Time Highs

Sentiment Is Not Exceptionally Bullish, Despite The S&P 500 Trading Close To All-Time Highs

Sentiment Is Not Exceptionally Bullish, Despite The S&P 500 Trading Close To All-Time Highs

Equities do best when sentiment is bearish but improving (Chart 4). With bulls in short supply, stocks can continue to climb the proverbial wall of worry. Whither The January Effect? Historically, stocks have fared better between October and April than between May and September (Chart 5). One caveat is that the January effect, which often saw stocks rally at the start of the year, has disappeared. In fact, the S&P 500 has fallen in January by an average annualized rate of 5.2% since 2000 (Table 1). Other less well-known calendar effects – such as the tendency for stocks to underperform on Mondays but outperform on the first trading day of each month – have persisted, however.

Chart 4

Chart 5

Table 1Calendar Effects

The Four Pillars Of The Stock Market

The Four Pillars Of The Stock Market

Bottom Line: January trading may be choppy, but stocks should rise over the next few months as more bears join the bullish camp. Last year’s losers are likely to outperform last year’s winners. Pillar 2: Economic Growth And Corporate Earnings (Modestly Bullish) Economic Growth And Earnings: Joined At The Hip The business cycle is the most important driver of stocks over medium-term horizons of about 12 months. The reason is evident in Chart 6: Corporate earnings tend to track key business cycle indicators such as the ISM manufacturing index, industrial production, business sales, and global trade. Chart 6The Business Cycle Is The Most Important Driver Of Stocks Over Medium-Term Horizons

The Business Cycle Is The Most Important Driver Of Stocks Over Medium-Term Horizons

The Business Cycle Is The Most Important Driver Of Stocks Over Medium-Term Horizons

Chart 7PMIs Signaling Above-Trend Growth

PMIs Signaling Above-Trend Growth

PMIs Signaling Above-Trend Growth

Global growth peaked in 2021 but should stay solidly above trend in 2022. Both the service and manufacturing PMIs remain in expansionary territory (Chart 7). The forward-looking new orders component of the ISM exceeded 60 for the second straight month in December. The Bloomberg consensus is for real GDP to rise by 3.9% in the G7 in 2022, well above the OECD’s estimate of trend G7 growth of 1.4% (Chart 8). Global earnings are expected to increase by 7.1%, rising 7.5% in the US and 6.7% abroad (Chart 9). Our sense is that both economic growth and earnings will surprise to the upside in 2022. Chart 9Analysts Expect Single-Digit Earnings Growth

Analysts Expect Single-Digit Earnings Growth

Analysts Expect Single-Digit Earnings Growth

Chart 8

Plenty Of Pent-Up Demand For Both Consumer And Capital Goods US households are sitting on $2.3 trillion in excess savings (Chart 10). Around half of these savings will be spent over the next few years, helping to drive demand. Households in the other major advanced economies have also buttressed their balance sheets. Chart 10Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

Plenty Of Pent-Up Demand

After two decades of subdued corporate investment, capital goods orders have soared. This bodes well for capex in 2022. Inventories remain at rock-bottom levels, which implies that output will need to exceed spending for the foreseeable future (Chart 11). On the residential housing side, both the US homeowner vacancy rate and the inventory of homes for sale are near multi-decade lows. Building permits are 11% above pre-pandemic levels (Chart 12). Chart 11Business Investment Should Be Strong In 2022

Business Investment Should Be Strong In 2022

Business Investment Should Be Strong In 2022

Chart 12Residential Construction Will Remain Well Supported

Residential Construction Will Remain Well Supported

Residential Construction Will Remain Well Supported

Chart 13China's Credit Impulse Has Bottomed

China's Credit Impulse Has Bottomed

China's Credit Impulse Has Bottomed

Chinese Growth To Rebound, Europe To Benefit From Lower Natural Gas Prices Chinese credit growth decelerated last year. However, the 6-month credit impulse has bottomed, and the 12-month impulse is sure to follow (Chart 13). Chinese coal prices have collapsed following the government’s decision to instruct 170 mines to expand capacity (Chart 14). China generates 63% of its electricity from coal. Lower energy prices and increased stimulus should support Chinese industrial activity in 2022. Like China, Europe will benefit from lower energy costs. Natural gas prices have fallen by nearly 50% from their peak on December 21st. A shrinking energy bill will support the euro (Chart 15). Chart 14Coal Prices Are Renormalizing In China

Coal Prices Are Renormalizing In China

Coal Prices Are Renormalizing In China

Chart 15A Shrinking Energy Bill Will Support The Euro

A Shrinking Energy Bill Will Support The Euro

A Shrinking Energy Bill Will Support The Euro

Chart 16

Omicron Or Omicold? While the Omicron wave has led to an unprecedented spike in new cases across many countries, the economic fallout will be limited. The new variant is more contagious but significantly less lethal than previous ones. In South Africa, it blew through the population without triggering a major increase in mortality (Chart 16). Preliminary data suggest that exposure to Omicron confers at least partial immunity against Delta. The general tendency is for viral strains to become less lethal over time. After all, a virus that kills its host also kills itself. Given that Omicron is crowding out more dangerous strains such as Delta, any future variant is likely to emanate from Omicron; and odds are this new variant will be even milder than Omicron. Meanwhile, new antiviral drugs are starting to hit the market. Pfizer claims that its new drug, Paxlovid, cuts the risk of hospitalization by almost 90% if taken within five days from the onset of symptoms. Bottom Line: While global growth has peaked and the pandemic remains a risk, growth should stay well above trend in the major economies in 2022, fueling further gains in corporate earnings and equity prices. Pillar 3: Monetary And Financial Factors (Neutral) Chart 17The Overall Stance Of Monetary Policy Will Not Return To Pre-Pandemic Levels For At Least Another 12 Months

The Overall Stance Of Monetary Policy Will Not Return To Pre-Pandemic Levels For At Least Another 12 Months

The Overall Stance Of Monetary Policy Will Not Return To Pre-Pandemic Levels For At Least Another 12 Months

Tighter But Not Tight Monetary and financial factors help govern the direction of equity prices both because they influence economic growth and also because they affect the earnings multiple at which stocks trade. There is little doubt that a number of central banks, including the Federal Reserve, are looking to dial back monetary stimulus. However, there is a big difference between tighter monetary policy and tight policy. Even if the FOMC were to raise rates three times in 2022, as the market is currently discounting, the fed funds rate would still be half of what it was on the eve of the pandemic (Chart 17). Likewise, even if the Fed were to allow maturing assets to run off in the middle of this year, as the minutes of the December FOMC meeting suggest is likely, the size of the Fed’s balance sheet will probably not return to pre-pandemic levels until the second half of this decade. A Higher Neutral Rate We have argued in the past that the neutral rate of interest in the US is higher than widely believed. This implies that the overall stance of monetary policy remains exceptionally stimulative. Historically, stocks have shrugged off rising bond yields, as long as yields did not increase to prohibitively high levels (Table 2). Table 2As Long As Bond Yields Don’t Rise Into Restrictive Territory, Stocks Will Recover

The Four Pillars Of The Stock Market

The Four Pillars Of The Stock Market

If the neutral rate ends up being higher than the Fed supposes, the danger is that monetary policy will stay too loose for too long. The question is one of timing. The good news is that inflation should recede in the US in 2022, as supply-chain bottlenecks ease and spending shifts back from goods to services. The bad news is that the respite from inflation will not last. As discussed in Section II of our recently-published 2022 Strategy Outlook, inflation will resume its upward trajectory in mid-2023 on the back of a tightening labor market and a budding price-wage spiral. This second inflationary wave could force the Fed to turn much more aggressive, spelling the end of the equity bull market. Bottom Line: While the Fed is gearing up to raise rates and trim the size of its balance sheet, monetary policy in the US and in other major economies will remain highly accommodative in 2022. US policy could turn more restrictive in 2023 as a second wave of inflation forces a more aggressive response from the Fed. Pillar 4: Valuations (Bearish In The US; Neutral Elsewhere) US Stocks Are Looking Pricey… While valuations are a poor timing tool in the short run, they are an excellent forecaster of stock prices in the long run. Chart 18 shows that the Shiller PE ratio has reliably predicted the 10-year return on equities. Today, the Shiller PE is consistent with total real returns of close to zero over the next decade.

Chart 18

Investors’ allocation to stocks has also predicted the direction of equity prices (Chart 19). According to the Federal Reserve, US households held a record high 41% of their financial assets in equities as of the third quarter of 2021. If history is any guide, this would also correspond to near-zero long-term returns on stocks. Chart 19Valuations Matter For Long-Term Returns (II)

Valuations Matter For Long-Term Returns (II)

Valuations Matter For Long-Term Returns (II)

… But There Is More Value Abroad Valuations outside the US are more reasonable. Whereas US stocks trade at a Shiller PE ratio of 37, non-US stocks trade at 20-times their 10-year average earnings. Other valuation measures such as price-to-book, price-to-sales, and dividend yield tell a similar story (Chart 20). Chart 20AUS Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (I)

Chart 20BUS Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

US Stocks Are Trading At A Significant Premium To Their Non-US Peers (II)

Cyclicals And Banks Overrepresented Abroad Our preferred sector skew for 2022 favors non-US equities. Increased capital spending in developed economies and incremental Chinese stimulus should boost industrial stocks and other deep cyclicals, which are overrepresented outside the US (Table 3). Banks are also heavily weighted in overseas markets; they should also do well in response to faster-than-expected growth and rising bond yields (Chart 21). Table 3Deep Cyclicals And Financials Are Overrepresented Outside The US

The Four Pillars Of The Stock Market

The Four Pillars Of The Stock Market

Chart 21Rising Bond Yields Will Help Bank Shares

Rising Bond Yields Will Help Bank Shares

Rising Bond Yields Will Help Bank Shares

Bottom Line: Valuations are more appealing outside the US, and with deep cyclicals and banks set to outperform tech over the coming months, overseas markets are the place to be in 2022. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Global Investment Strategy View Matrix

Image

Special Trade Recommendations

Image

Current MacroQuant Model Scores

Image

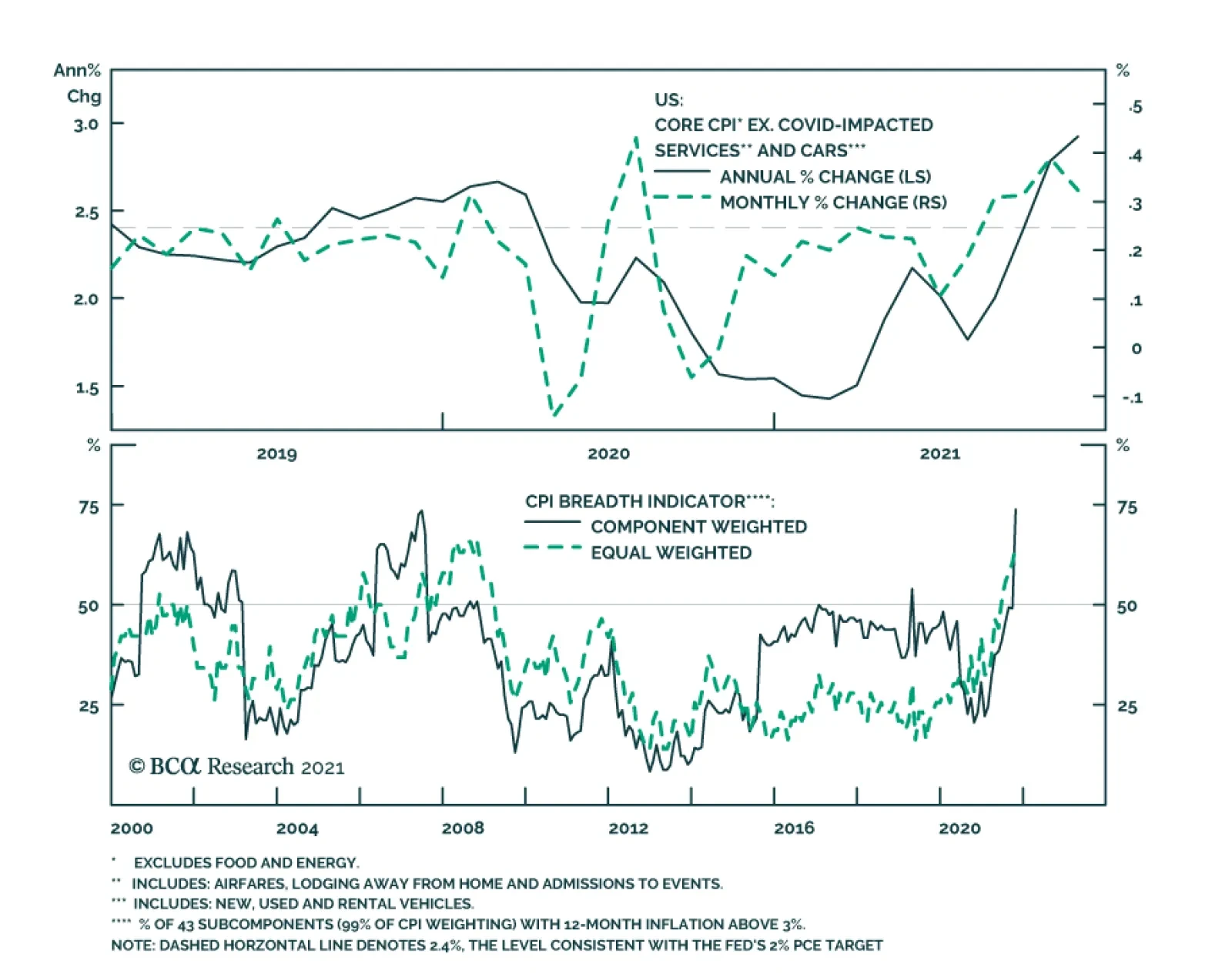

Highlights For the time being, US core inflation will not drop anywhere close to the Fed’s target range. The Fed will continue tightening until something breaks. US bond yields and the US dollar are heading higher. The S&P500 will need to drop meaningfully for the Fed to stop tightening. The Fed’s tightening and the US dollar’s persistent strength amid the lack of recovery in the Chinese business cycle will eventually produce a drawdown in commodity prices in the coming months. Absolute-return investors should stay defensive on EM risk assets and asset allocators should continue to underweight EM versus DM in global equity and credit portfolios. Feature We are starting the year with a review of a few macro pillars of our view that will shape global financial markets in the coming months. US Core Inflation Will Prove Sticky… Chart 1Average Of All Core US Inflation Measures

Average Of All Core US Inflation Measures

Average Of All Core US Inflation Measures

The average of seven various US core inflation measures – core CPI, core PCE, trimmed-mean CPI, median CPI, sticky core CPI, trimmed-mean PCE and market-based core PCE – has surged to 4% (Chart 1). Although the core inflation rate could decline in 2022 as supply bottlenecks ease and base effects become more favorable, it is unlikely to drop below 3%. Instead, it will remain well above the Fed’s inflation target. If the Fed adheres to its mandate, it will have to hike rates until inflation heads toward 2%. US core inflation will not drop toward 2% unless the economy slows materially. Consumer and business inflation expectations have risen substantially. US consumer inflation expectations for one and three years ahead have risen to 4-6%, and US non-farm businesses have been able to raise prices by 4.5% y/y in Q3 (Chart 2). We can say the genie – inflation and inflation expectations – is out of bottle and it will be hard to put it back in. Importantly, labor market shortages will persist, and employee wage demand will be strong. Employees’ current wage growth expectations are based on their inflation expectations in the next one to three years, not the next decade. Even though longer term inflation expectations remain somewhat muted, they will not prevent high wage growth. Critically, inflation has “eaten” into employee income: real wage growth – adjusted for headline consumer price inflation – has been negative in 2021 (Chart 3). Consistently, employees know their compensation has lagged inflation and will be demanding significant wage hikes in 2022. Chart 3Inflation Is "Eating" Into Wages In The US

Inflation Is "Eating" Into Wages In The US

Inflation Is "Eating" Into Wages In The US

Chart 2US Inflation Expectations Have Risen Sharply

US Inflation Expectations Have Risen Sharply

US Inflation Expectations Have Risen Sharply

In short, a wage-price spiral of moderate proportions is unfolding. Given tight labor market conditions, businesses will have no choice but raise wages considerably and then try to pass the higher costs on to their consumers. … Prompting Higher US Bond Yields … Despite the surge in core inflation to a 30-plus year high, US bond yields have remained low. The long end of the US yield curve has continued to be suppressed even as the market participants raised their rate hike expectations. Not only has the expected terminal Fed funds target rate not risen much, but also the bond term premium has remained negative. The bond term premium is akin to the equity risk premium. Pronounced uncertainty about the US inflation outlook as well as elevated bond volatility warrant a higher bond term premium (Chart 4). … Which Will Push The US Dollar Higher… Rising US interest rate expectations will lead to a stronger greenback. Our US Dollar Liquidity Indicator points to continued firmness in the broad trade-weighted US dollar ( the latter is shown inverted in this chart) (Chart 5). Chart 5US Dollar Liquidity And The US Dollar

US Dollar Liquidity And The US Dollar

US Dollar Liquidity And The US Dollar

Chart 4Inflation Uncertainty And High Bond Volitility Herald A Higher Term Premium

Inflation Uncertainty And High Bond Volitility Herald A Higher Term Premium

Inflation Uncertainty And High Bond Volitility Herald A Higher Term Premium

Our framework for the relationship between currencies and their interest rates is as follows: Scenario 1: When inflation is high or rising fast, the central bank is willing to hike rates and the economy can withstand higher borrowing costs, the currency will appreciate. Scenario 2: When inflation is high or rising fast and the central bank is unwilling to hike rates, the currency will depreciate. This is the case when the central bank falls behind the curve. Scenario 3: When the central bank is tightening but the economy cannot handle higher borrowing costs, the currency will depreciate. The US economy is presently able to handle higher interest rates. Hence, the US dollar is currently driven by the dynamics described in Scenario 1, i.e., rising interest rates will support the greenback. Chart 6US Household Finances Are Healthy

US Household Finances Are Healthy

US Household Finances Are Healthy

Our rationale is that US interest rate sensitive sectors like housing and car sales have been restrained by supply shortages – not weak demand. In fact, there is large pent-up demand for both housing and autos and a reasonable rise in borrowing costs will not thwart this demand. Besides, US household debt and debt servicing costs have declined substantially in the past 10 years (Chart 6). US households are no longer highly indebted. This development – along with robust wage gains – will allow households to borrow more and service their debt. Finally, unlike in many other Anglo-Saxon countries, in the US it is long-term rates – rather than short ones – that matter for household debt servicing. Mortgages make up 70% of household debt in the US and the mortgage rate is tied to the 30-year bond yield. In many other advanced and emerging economies, mortgage rates are more influenced by the central bank policy rate than long-term bond yields. As a result, the US economy will be able to endure monetary tightening by the Fed better than other developed and emerging economies can handle rate hikes from their central banks. Specifically, mainstream EM economies (EM ex-China, Korea and Taiwan) will slow markedly as and if their central banks hike rates further (Chart 7). There is, however, a caveat: Even though Main Street America will be able to withstand a reasonable amount of rate hikes, Wall Street might not be able ride out these rate hikes. The difference is the starting point – US equity valuations are very high. … And Will Herald A US Equity Correction And Sector Rotation The spike in US core inflation is likely to engender a negative correlation between US share prices and bond yields, as was the case in 1966. We first made this argument in last year’s Special Report titled A Paradigm Shift In The Stock-Bond Relationship (Chart 8). Chart 7Mainstream EM: Monetary Tightening Will Dampen Growth

Mainstream EM: Monetary Tightening Will Dampen Growth

Mainstream EM: Monetary Tightening Will Dampen Growth

Chart 8S&P500 And Bond Yields Correlation Will Turn Negative

S&P500 And Bond Yields Correlation Will Turn Negative

S&P500 And Bond Yields Correlation Will Turn Negative

The current episode in the US is akin to the second half of the 1960s when US core inflation and bond yields rose after decades of lingering at very low levels. Starting in 1966, US share prices became negatively correlated with US Treasury yields (Chart 9 – bond yields are shown inverted). Going forward, the S&P 500 will often take its cue from US bond yields: stocks will rally when bond yields decline, and tumble when bond yields rise. Given that we expect US Treasury yields to rise in the coming months (10-year yields will move well above 2%), the S&P 500 is likely to correct. The key risk to this view is the massive amount of cash on the sidelines, and widespread investor willingness to buy any dip in US equities. The absolute level of US retail money market funds currently stands at a formidable $1 trillion (Chart 10, top panel). However, this just represents a mere 2% of the US equity market cap (Chart 10, bottom panel). Hence, if institutional investors begin selling stocks, retail investors might not be able to support the market. Chart 9Early 2020s = Late 1960s?

Early 2020s = Late 1960s?

Early 2020s = Late 1960s?

Chart 10Cash on Sidelines: A Lot Or Not So Much?

Cash on Sidelines: A Lot Or Not So Much?

Cash on Sidelines: A Lot Or Not So Much?

Chart 11EM Relative Equity Performance Is Correlated With The USD, Not Bond Yields

EM Relative Equity Performance Is Correlated With The USD, Not Bond Yields

EM Relative Equity Performance Is Correlated With The USD, Not Bond Yields

Furthermore, rising US bond yields will cause US value stocks to outperform US growth stocks. Will EM stocks outperform US or DM ones as US bond yields rise? The top panel of Chart 11 illustrates that there has been no stable correlation between US bond yields and EM versus DM relative equity performance. Yet, there is a strong relationship between EM relative equity performance and the US dollar (Chart 11, bottom panel). If the broad trade-weighted US dollar rallies, EM stocks will underperform their DM counterparts (the greenback is shown inverted in the bottom panel of Chart 11). A sell-off in US stocks and bonds and the greenback’s rally will tighten US financial conditions considerably. The Fed is putting a lot of weight on financial conditions, especially when they are becoming restrictive. As US financial conditions tighten, the Fed will likely pivot, i.e., soften its hawkish stance. The Fed would likely argue that tight financial conditions will slow growth, which will in turn bring down inflation. Such a Fed pivot will potentially mark the end of a US dollar rally, enable American share prices to rise again, and EM stocks to start outperforming. However, we are not there yet. Bottom Line: For the time being, US core inflation will not drop anywhere close to the Fed’s target range. Hence, the Fed will continue tightening until something breaks. It will take a meaningful drop in the S&P500 (~20%) to make the Fed stop tightening. Commodity Prices Commodity prices have been caught between two opposing forces: US inflation and China’s slowdown. Worries about US inflation have made investors buy inflation hedges, and commodities are traditionally viewed as an inflation hedge. Yet, there is a caveat: Inflation is proliferating in the US but not in China. On the contrary, Chinese imports of key commodities contracted dramatically in H2 2021 (Chart 12). We are surprised that commodity prices have been so resilient despite shrinking Chinese commodity imports. Our sense is that commodity prices have been held up by two forces: strong global manufacturing activity and financial demand from investors. As for the green revolution, we believe it will be a major bullish force for select commodities in a couple of years. At the moment, however, it is not large enough to offset the slowdown in the Chinese economy. It might take investor concerns about US demand and/or a slowdown in global manufacturing to trigger a relapse in commodity prices. Rising US interest rates and a continued dollar rally will eventually result in a meaningful drawdown in commodity prices. Chart 13 demonstrates that the declines in the Swedish manufacturing PMI new orders-to-inventory ratio and the Swedish krona/Swiss franc cross rate point to downside risks in raw materials prices. Chart 12Chinese Imports Of Key Commodities Have Shrunk

Chinese Imports Of Key Commodities Have Shrunk

Chinese Imports Of Key Commodities Have Shrunk

Chart 13A Red Flag For Commodities From Industrial Sweden

A Red Flag For Commodities From Industrial Sweden

A Red Flag For Commodities From Industrial Sweden

Bottom Line: Commodity prices have so far ignored China’s slowdown. However, the Fed’s tightening and the US dollar’s persistent strength amid the lack of recovery in the Chinese business cycle will eventually produce a drawdown in resource prices in the coming months. Investment Strategy For EM Chart 14EM Equities: No Profit Growth, No Bull Market

EM Equities: No Profit Growth, No Bull Market

EM Equities: No Profit Growth, No Bull Market

EM share prices have been falling in absolute terms despite the strength in the S&P 500. The EM equity index will drop further due to the dismal EM profit outlook and the continued de-rating of Chinese TMT stocks. In absolute terms, the EM equity index is at the same level as it was in 2011 because EM EPS in USD has not expanded at all since 2011 (Chart 14). Investors are reluctant to pay high multiples for EM companies because they have produced zero earnings growth over the past 10 years. Besides, higher US bond yields and continued strength in the US dollar will lead to higher EM sovereign and corporate bond yields. EM non-TMT share prices typically wobble when EM US dollar borrowing costs rise (Chart 15). Chart 15Rising EM USD Borrowing Costs Are Bearish For EM Non-TMT Stocks

Rising EM USD Borrowing Costs Are Bearish For EM Non-TMT Stocks

Rising EM USD Borrowing Costs Are Bearish For EM Non-TMT Stocks

We continue to recommend underweighting EM in a global equity portfolio. EM always underperforms DM when the greenback rallies. We maintain our short positions in a basket of EM currencies versus the US dollar. Rising US bond yields and a firm greenback will continue weighing on EM fixed income markets – both local currency and US dollar ones. Fixed-income investors should favor US corporate credit over EM corporate and sovereign credit, quality adjusted. In local rates, we are betting on yield curve inversion in Russia and Mexico, receiving rates in China and Malaysia and paying rates in the Czech Republic. For the full list of our fixed-income, currency and equity recommendations, please refer to the tables below. These are also available on our website. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Equities Recommendations Currencies, Credit And Fixed-Income Recommendations

Highlights Demand in the major economies remains well below its pre-pandemic trend. Meaning that relative to potential output, demand is lukewarm, at best. Inflation is hot, not because of strong overall demand, but because of the surging demand for goods. If the spending on goods cools, then inflation will also cool. We expect this ‘good’ resolution of inflation to unfold, because there are only so many goods that any person can buy. Underweight personal goods versus consumer services. Bond yields have the scope to rise by just 50-100 bps before pulling the bottom out of the $300 trillion global real estate market and the $100 trillion global equity market. Long-term investors should continue to own US T-bonds and focus their equity investments in long-duration (growth) stocks, sectors, and stock markets… …because the ultimate low in bond yields is yet to come. Feature Chart of the WeekWill Bond Yields Stay Chilled With Inflation So Hot?

Will Bond Yields Stay Chilled With Inflation So Hot?

Will Bond Yields Stay Chilled With Inflation So Hot?

2022 begins with an investment conundrum. Why have long bond yields been so chilled when inflation is running so hot? (Chart I-1) While US and UK inflation have ripped to 6.9 percent and 5.1 percent respectively, the 30-year T-bond yield and 30-year gilt yield remain a relative oasis of calm – standing at 2.1 percent and 1.2 percent respectively. 10-year yields have also stayed relatively calm. Moreover, as long-duration bonds set the valuations of long-duration stocks, a calm bond market has meant a calm stock market. What can explain this apparent conundrum of chilled yields in the face of the hottest inflation in a generation? Long Bond Yields Are Tracking Demand, Not Inflation Chart I-2 answers the conundrum. The long bond yield is taking its cue not from hot inflation, but from economic demand, which is far from overheating. Quite the contrary, US real GDP and consumption are struggling to reach their pre-pandemic trends. Meanwhile, UK real GDP languishes 5 percent below its pre-pandemic trend (Chart I-3), and other major economies tell similar stories. Chart I-2Long Bond Yields Are Tracking Demand

Long Bond Yields Are Tracking Demand

Long Bond Yields Are Tracking Demand

Chart I-3Demand Is Lukewarm, At Best

Demand Is Lukewarm, At Best

Demand Is Lukewarm, At Best

Some people mistake the strong economic growth in recent quarters for overheating demand. In fact, this robust growth is just the natural snap-back after the pandemic induced collapse in early-2020. Meaning that the strong growth is unsustainable, just as the bounce that a ball experiences after a big drop is unsustainable. Demand in the major economies remains well below its pre-pandemic trend. To repeat, demand in the major economies remains well below its pre-pandemic trend. As this pre-pandemic trend is a good gauge of potential output, economic demand is lukewarm, at best. And this explains why long bond yields have remained chilled. Inflation Is Tracking The Displacement Of Demand Yet solving the first conundrum simply raises a second conundrum. If overall demand is lukewarm, then why is inflation so hot? (Chart I-4). The answer is that inflation is being fuelled by the displacement of demand into goods from services (Chart I-5). Chart I-4Hot Inflation Is Not Reflecting Lukewarm Overall Demand

Hot Inflation Is Not Reflecting Lukewarm Overall Demand

Hot Inflation Is Not Reflecting Lukewarm Overall Demand

Chart I-5Hot Inflation Is Reflecting The Hot Demand For Goods

Hot Inflation Is Reflecting The Hot Demand For Goods

Hot Inflation Is Reflecting The Hot Demand For Goods

If a dollar spent on goods is displaced from a dollar spent on services, then overall demand will be unchanged. However, what happens to the overall price level depends on the relative price elasticities of demand for goods and services. If the price elasticities are the same, then overall prices will also be unchanged, because a higher price for goods will be exactly countered by a lower price for services. But if the price elasticities are very different, then overall prices can rise sharply because the higher price for goods will dominate overall inflation. All of which solves our second conundrum. Spending on services that require close contact with strangers – using public transport, going to the dentist, cinema, or recreational activities that involve crowds – are suffering severe shortfalls compared to pre-pandemic times. Some people say that this is due to supply shortages, yet the trains and buses are running empty and there is no shortage of dentists, cinema seats, or even (English) Premier League tickets. Indeed, the Premier League team that I support (which I will not name) has been sending me begging emails to attend matches! Surging inflation is no longer a reliable reflection of overall demand. If somebody doesn’t use public transport, or go to the cinema or crowded events because he is worried about the health risk, then lowering the price will not lure that person back. In fact, the person might interpret the lower price as a signal of greater risk, and might become more averse. In other words, the price elasticity of demand for certain services has flipped from its usual negative to zero, or even positive. This creates a major problem for central banks, because if the price elasticity of services demand has changed, then surging inflation is no longer a reliable reflection of overall demand, which remains below its potential. Instead, surging inflation is largely reflecting the surging demand for goods. Two Ways That Inflation Can Resolve: One Good, One Bad It follows that if the spending on goods cools, then inflation will also cool. We expect this ‘good’ resolution of inflation to unfold, because there are only so many goods that any person can buy. Durables, by their very definition, last a long time. Even clothes and shoes, though classified as nondurables, are in fact quite durable. Meaning that are only so many cars, iPhone 13s, gadgets, clothes and shoes that any person can own before reaching saturation. We recommend that equity investors play this inevitable normalisation by underweighting personal goods versus consumer services. Still, the resolution of inflation could also take a ‘bad’ form. If inflation persisted, then bond yields could lose their chill as they flipped their focus from lukewarm demand to hot inflation. Given that long-duration bonds set the valuations of long-duration stocks, and given that stock valuations are already stretched versus bonds, this would quickly inflict pain on stock investors (Chart I-6). Chart I-6The US Stock Market = The 30-Year T-Bond Price Multiplied By Profits

The US Stock Market = The 30-Year T-Bond Price Multiplied By Profits

The US Stock Market = The 30-Year T-Bond Price Multiplied By Profits

More significantly, it would also quickly inflict pain on the all-important real estate market. Through the past ten years, world prime residential prices are up by 70 percent while rents are up by just 25 percent1 (Chart I-7). Meaning that the bulk of the increase in global real estate prices is due to skyrocketing valuations. The culprit is the structural collapse in global bond yields (Chart I-8). Chart I-7The Bulk Of The Increase In Global Real Estate Prices Is Due To Valuation Expansion…

The Bulk Of The Increase In Global Real Estate Prices Is Due To Valuation Expansion...

The Bulk Of The Increase In Global Real Estate Prices Is Due To Valuation Expansion...

Chart I-8…And The Culprit For The Richest Ever Valuation Of Global Real Estate Is The Structural Collapse In Global Bond Yields

...And The Culprit For The Richest Ever Valuation Of Global Real Estate Is The Structural Collapse In Global Bond Yields

...And The Culprit For The Richest Ever Valuation Of Global Real Estate Is The Structural Collapse In Global Bond Yields

This means that bond yields have the scope to rise by just 50-100 bps before pulling the bottom out of the $300 trillion global real estate market. Given that this dwarfs the $90 trillion global economy, the massive deflationary backlash would annihilate any lingering inflation. Some people counter that in an inflationary shock, stocks and property – as the ultimate real assets – ought to perform well even as bond yields rise. However, when valuations start off stretched as now, the initial intense headwind from deflating valuations would obliterate the tailwind from inflating incomes. The scope for higher bond yields is limited by the fragility of stock market and real estate valuations. With the scope for higher yields limited by the fragility of stock market and real estate valuations, and with the ultimate low in yields yet to come, long-term investors should continue to own US T-bonds. And they should focus their equity investments in long-duration (growth) stocks, sectors, and stock markets. Fractal Trading Update Owing to the holidays, we are waiting until next week to initiate new trades. We will also add a new feature – a ‘watch list’ of investments that are approaching potential turning points, but are not yet at peak fragility. We believe that this enhancement will help to prepare future trades. Stay tuned. Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Footnotes 1 Based on Savills Prime Index: World Cities – Capital Values, and World Cities – Rents and Yields, June 2011 through June 2021. Fractal Trading System Fractal Trades

Image

6-Month Recommendations Structural Recommendations Closed Fractal Trades Indicators To Watch - Bond Yields Chart II-1Indicators To Watch - Bond Yields - ##br##Euro Area

Indicators To Watch - Bond Yields - Euro Area

Indicators To Watch - Bond Yields - Euro Area

Chart II-2Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Indicators To Watch - Bond Yields - Europe Ex Euro Area

Chart II-3Indicators To Watch - Bond Yields - ##br##Asia

Indicators To Watch - Bond Yields - Asia

Indicators To Watch - Bond Yields - Asia

Chart II-4Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Bond Yields - Other Developed

Indicators To Watch - Interest Rate Expectations Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Long-only investors with a minimum horizon of two years should buy the interactive entertainment sector. Hedge fund investors with a minimum horizon of two years should go long interactive entertainment versus technology. Despite a trebling of sales since 2014, interactive entertainment comprises just 0.2 percent of world GDP, and just 0.3 percent of US consumer spending, providing scope for substantial further growth. Looking ahead, we identify four specific drivers of growth: cloud gaming, e-sports, 5G, and ‘gaming as a service’. After this year’s sell-off, the sector’s relative valuation has fallen below its long-term average. Even more striking, the sector now trades at a record 20 percent discount to the tech sector. Yet we think we can do better than the sector index and reveal our preferred basket of interactive entertainment stocks. Feature In the future, a typical day will be divided into three. A third we will spend sleeping and dreaming; a third we will spend in reality; and a third we will spend in virtual reality. Parents of teenagers may already recognise this pattern, and will certainly do so over the coming holiday season! But many people in their twenties and thirties are also spending more of their time in the virtual world entered through the portal of interactive entertainment (meaning video gaming, and we will use these terms interchangeably throughout this report). Since 2014, interactive entertainment has experienced explosive growth. Since 2014, interactive entertainment has experienced explosive growth. Sales have trebled, outperforming even the tech sector whose sales have doubled, and far outperforming the total stock market’s sales (and global GDP) which are up a sedate 30 percent (Chart I-1 and Chart I-2). Yet despite this explosive growth, interactive entertainment comprises just 0.2 percent of world GDP, and just 0.3 percent of US consumer spending, providing scope for substantial further growth (Chart I-3 and Chart I-4). Chart I-1Since 2014, Interactive Entertainment’s Sales Have Almost Trebled…

Since 2014, Interactive Entertainment's Sales Have Trebled...

Since 2014, Interactive Entertainment's Sales Have Trebled...

Chart I-2…And Its Profits Have More Than ##br##Trebled

...And Its Profits Have Quadrupled

...And Its Profits Have Quadrupled

Chart I-3

Chart I-4…And 0.3 Percent Of US Consumer Spending

...And 0.3 Percent Of US Consumer Spending

...And 0.3 Percent Of US Consumer Spending

Meanwhile, the interactive entertainment sector’s profit margin has also trended higher, to 14 percent. This compares with 16 percent for tech, and around 10 percent for the total stock market (Chart I-5). Chart I-5Interactive Entertainment’s Profit Margin Has Trended Higher

Interactive Entertainment's Profit Margin Has Trended Higher

Interactive Entertainment's Profit Margin Has Trended Higher

The combination of explosive sales growth and higher margins has resulted in spectacular profit growth. Interactive entertainment profits have skyrocketed by 250 percent, outperforming tech profits which are up 150 percent, and far outperforming total stock market profits which are up 50 percent. We expect this strong outperformance in profits to continue. Cloud Gaming, E-Sports, 5G, And ‘Gaming As A Service’ Will Drive Sales Growth Looking ahead, we identify four specific drivers of growth: cloud gaming, e-sports, 5G, and ‘gaming as a service’. Cloud gaming (gaming-on-demand) streams high quality interactive content that is running on remote servers, akin to how remote desktops work. Thereby, gamers can play using just a device and an internet connection. Cloud gaming displaces physical disks, powerful hardware, and the need to download games onto a platform – analogous to how the on-demand streaming of media and entertainment has displaced DVDs and cable TV. Cloud gaming benefits both content developers and players. Developers do not have to worry about piracy, illegal downloads or digital rights management. Players benefit from a high (and equal) server processing power, creating a level-playing field in games. Which brings us nicely to the second driver of growth: e-sports. E-sports refers to competitive video gaming, a sector which is experiencing massive growth. 175 colleges and universities have already become members of the National Association of Collegiate Esports (NACE), offering varsity e-sports programs, and recognizing student gamers through scholarship awards. E-sports are hugely popular not only for their competitive element but also for their opportunity for social engagement, albeit virtually. The third major driver of interactive entertainment profits is the widespread rollout of 5G cellular networks, which makes cloud gaming accessible to mobile devices, rather than just to consoles and PCs. Mobile gaming revenues have become the most powerful engine of growth. This is significant because revenues from mobile gaming have now overtaken the combined revenues from the console and PC platforms. As such, mobile gaming revenues have become the most powerful engine of growth (Chart I-6 and Chart I-7).

Chart I-6

Chart I-7

The fourth driver of profits is the ‘gaming as a service’ (GaaS) revenue model, which is analogous to the software industry’s standard ‘software as a service’ (SaaS) revenue model. Instead of a one-time sale, revenue comes from a continuous stream of in-game sales and subscriptions. For example, Activision Blizzard’s doubling of revenues since 2014 has come mostly from in-game subscriptions. Product sales now comprise less than 30 percent of total revenues (Chart I-8).

Chart I-8

As well as being a major contributor to strong sales growth, GaaS boosts profit margins by lengthening the sales derived from the fixed costs of developing a given game. But Isn’t Video Gaming An Unhealthy Addiction? In 2018, the World Health Organization recognized 'gaming disorder' as an addictive behaviour and has officially defined it in the 11th Revision of the International Classification of Diseases (ICD-11). Then in August this year, the Chinese government imposed harsh restrictions on video gaming for minors. Under-18s can play video games for a maximum of three hours a week, one hour each on Friday, Saturday, and Sunday. These developments beg the question, is the interactive entertainment sector exposed to significant regulatory risks? The crackdown and regulation of illicit activities should be welcomed, not feared. China’s crackdown on video gaming for minors is consistent with its other crackdowns – for example, on cryptocurrencies – that decree that ‘the Chinese government knows what’s best for its people.’ However, libertarian western economies are unlikely to follow suit. In any case, even the World Health Organization concedes that gaming disorder affects only a small proportion of people. Another regulatory issue is so-called ‘gamblification’. Popularly known as loot boxes, or mystery boxes, the contents of some in-game virtual goods are unknown to gamers who purchase them in the hopes of attaining rare items that boast high in-game utility. The features resemble gambling and raise concerns of predatory monetization. Calls for regulatory action refer to gamblification as a contributing cause to gaming disorder. Still, such features are not significant enough in most games to change the structural outlook. A final putative concern is that in-game tradable virtual currencies create a haven for cyber criminals and money launderers. The solution could be know-your-customer (KYC) and anti-money laundering (AML) regulations akin to those in the online gambling/betting industry. Ultimately, just as in the cryptocurrency space, and indeed the internet space, the crackdown and regulation of illicit activities should be welcomed, not feared. As such, it strengthens rather than weakens the structural outlook. The Investment Case This year’s sell-off in the interactive entertainment sector provides a good entry point for long-term investors (Chart I-9). The sell-off was exacerbated by two bits of bad news: first, the revelation of a toxic and sexist workplace culture at Activision Blizzard – since when the company has suffered a wave of bad publicity, numerous resignations, and a 40 percent plunge in its stock price; then, the Chinese crackdown on video gaming for minors. Chart I-9Interactive Entertainment’s Recent Sell-Off Provides A Good Long-Term Entry Point

Interactive Entertainment's Recent Sell-Off Provides A Good Long-Term Entry Point

Interactive Entertainment's Recent Sell-Off Provides A Good Long-Term Entry Point

Both items of bad news seem well discounted. The sector’s relative valuation to the market has fallen below its long-term average. Even more striking, the sector now trades at a record 20 percent discount to the tech sector (Chart I-10 and Chart I-11). Chart I-10Interactive Entertainment Now Trades At A 20 Percent Discount To Technology…

Interactive Entertainment Now Trades At A 20 Percent Discount To Technology...

Interactive Entertainment Now Trades At A 20 Percent Discount To Technology...

Chart I-11…And Its Relative Valuation To The Market Is Below The Long-Term Average

...And Its Relative Valuation To The Market Is Below The Long-Term Average

...And Its Relative Valuation To The Market Is Below The Long-Term Average

Given that the structural outlook for the sector’s sales and profits remains intact, long-only investors with a minimum horizon of two years should buy the interactive entertainment sector (Table I-1). Hedge fund investors with a minimum horizon of two years should go long interactive entertainment versus technology.

Chart I-

Yet we think we can do better than the sector index by filtering out the riskiest stocks, based on overvaluation, commercial risk, and regulatory risk. For example, we exclude the Chinese stocks that are most exposed to the Chinese government crackdown and future whims. Long-only investors with a minimum horizon of two years should buy the interactive entertainment sector. On this basis, our interactive entertainment basket comprises: (Table I-2).

Chart I-

Nintendo Activision Blizzard Electronic Arts Zynga Konami Capcom Square Enix This is the final Counterpoint report of the year. We wish you all a very happy and restful holiday season. Dhaval Joshi Chief Strategist dhaval@bcaresearch.com Mohamed El Shennawy Research Associate mohamede@bcaresearch.com

Highlights Our three strategic themes over the long run: (1) great power rivalry (2) hypo-globalization (3) populism and nationalism. The implications are inflationary over the long run. Nations that gear up for potential conflict and expand the social safety net to appease popular discontent will consume a lot of resources. Our three key views for 2022: (1) China’s reversion to autocracy (2) America’s policy insularity (3) petro-state leverage. The implications are mostly but not entirely inflationary: China will ease policy, the US will pass more stimulus, and energy supply may suffer major disruptions. Stay long gold, neutral US dollar, short renminbi, and short Taiwanese dollar. Stay tactically long global large caps and defensives. Buy aerospace/defense and cyber-security stocks. Go long Japanese and Mexican equities – both are tied to the US in an era of great power rivalry. Feature Chart 1US Resilience

US Resilience

US Resilience

Global investors have not yet found a substitute for the United States. Despite a bout of exuberance around cyclical non-US assets at the beginning of 2021, the year draws to a close with King Dollar rallying, US equities rising to 61% of global equity capitalization, and the US 30-year Treasury yield unfazed by inflation fears (Chart 1). American outperformance is only partly explained by its handling of the lingering Covid-19 pandemic. The US population was clearly less restricted by the virus (Chart 2). But more to the point, the US stimulated its economy by 25% of GDP over the course of the crisis, while the average across major countries was 13% of GDP. Americans are still more eager to go outdoors and the government has been less stringent in preventing them (Chart 3).

Chart 2

Chart 3Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Social Restrictions Short Of Lockdown

Going forward, the pandemic should decline in relevance, though it is still possible that a vaccine-resistant mutation will arise that is deadlier for younger people, causing a new round of the crisis. The rotation into assets outside the US will be cautious. Across the world, monetary and credit growth peaked and rolled over this year, after the extraordinary effusion of stimulus to offset the social lockdowns of 2020 (Chart 4). Government budget deficits started to normalize while central banks began winding down emergency lending and bond-buying. More widespread and significant policy normalization will get under way in 2022 in the face of high core inflation. Tightening will favor the US dollar, especially if global growth disappoints expectations. Chart 4Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Waning Monetary And Credit Stimulus

Chart 5Global Growth Stabilization

Global Growth Stabilization

Global Growth Stabilization

Global manufacturing activity fell off its peak, especially in China, where authorities tightened monetary, fiscal, and regulatory policy aggressively to prevent asset bubbles from blowing up (Chart 5). Now China is easing policy on the margin, which should shore up activity ahead of an important Communist Party reshuffle in fall 2022. The rest of the world’s manufacturing activity is expected to continue expanding in 2022, albeit less rapidly. This trend cuts against US outperformance but still faces a range of hurdles, beginning with China. In this context, we outline three geopolitical themes for the long run as well as three key views for the coming 12 months. Our title, “The Gathering Storm,” refers to the strategic challenge that China and Russia pose to the United States, which is attempting to form a balance-of-power coalition to contain these autocratic rivals. This is the central global geopolitical dynamic in 2022 and it is ultimately inflationary. Three Strategic Themes For The Long Run The international system will remain unstable in the coming years. Global multipolarity – or the existence of multiple, competing poles of political power – is the chief destabilizing factor. This is the first of our three strategic themes that will persist next year and beyond (Table 1). Our key views for 2022, discussed below, flow from these three strategic themes. Table 1Strategic Themes For 2022 And Beyond

2022 Key Views: The Gathering Storm

2022 Key Views: The Gathering Storm

1. Great Power Rivalry Multipolarity – or great power rivalry – can be illustrated by the falling share of US economic clout relative to the rest of the world, including but not limited to strategic rivals like China. The US’s decline is often exaggerated but the picture is clear if one looks at the combined geopolitical influence of the US and its closest allies to that of the EU, China, and Russia (Chart 6).

Chart 6

China’s rise is the most destabilizing factor because it comes with economic, military, and technological prowess that could someday rival the US for global supremacy. China’s GDP has surpassed that of the US in purchasing power terms and will do so in nominal terms in around five years (Chart 7).

Chart 7

True, China’s potential growth is slowing and Chinese financial instability will be a recurring theme. But that very fact is driving Beijing to try to convert the past 40 years of economic success into broader strategic security. Chart 8America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

America's Global Role Persists (If Lessened)

Since China is capable of creating an alternative political order in Asia Pacific, and ultimately globally, the United States is reacting. It is penalizing China’s economy and seeking to refurbish alliances in pursuit of a containment policy. The American reaction to the loss of influence has been unpredictable, contradictory, and occasionally belligerent. New isolationist impulses have emerged among an angry populace in reaction to gratuitous wars abroad and de-industrialization. These impulses appeared in both the Obama and Trump administrations. The Biden administration is attempting to manage these impulses while also reinforcing America’s global role. The pandemic-era stimulus has enabled the US to maintain its massive trade deficit and aggressive defense spending. But US defense spending is declining relative to the US and global economy over time, encouraging rival nations to carve out spheres of influence in their own neighborhoods (Chart 8). Russia’s overall geopolitical power has declined but it punches above its weight in military affairs and energy markets, a fact which is vividly on display in Ukraine as we go to press. The result is to exacerbate differences in the trans-Atlantic alliance between the US and the European Union, particularly Germany. The EU’s attempt to act as an independent great power is another sign of multipolarity, as well as the UK’s decision to distance itself from the continent and strengthen the Anglo-American alliance. If the US and EU do not manage their differences over how to handle Russia, China, and Iran then the trans-Atlantic relationship will weaken and great power rivalry will become even more dangerous. 2. Hypo-Globalization The second strategic theme is hypo-globalization, in which the ancient process of globalization continues but falls short of its twenty-first century potential, given advances in technology and governance that should erode geographic and national boundaries. Hypo-globalization is the opposite of the “hyper-globalization” of the 1990s-2000s, when historic barriers to the free movement of people, goods, and capital seemed to collapse overnight. Chart 9From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

From 'Hyper-Globalization' To Hypo-Globalization

The volume of global trade relative to industrial production peaked with the Great Recession in 2008-10 and has declined slowly but surely ever since (Chart 9). Many developed markets suffered the unwinding of private debt bubbles, while emerging economies suffered the unwinding of trade manufacturing. Periods of declining trade intensity – trade relative to global growth – suggest that nations are turning inward, distrustful of interdependency, and that the frictions and costs of trade are rising due to protectionism and mercantilism. Over the past two hundred years globalization intensified when a broad international peace was agreed (such as in 1815) and a leading imperial nation was capable of enforcing law and order on the seas (such as the British empire). Globalization fell back during times of “hegemonic instability,” when the peace settlement decayed while strategic and naval competition eroded the global trading system. Today a similar process is unfolding, with the 1945 peace decaying and the US facing the revival of Russia and China as regional empires capable of denying others access to their coastlines and strategic approaches (Chart 10).1 Chart 10Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Hypo-Globalization And Hegemonic Instability

Chart 11Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

Hypo-Globalization: Temporary Trade Rebound

No doubt global trade is rebounding amid the stimulus-fueled recovery from Covid-19. But the upside for globalization will be limited by the negative geopolitical environment (Chart 11). Today governments are not behaving as if they will embark on a new era of ever-freer movement and ever-deepening international linkages. They are increasingly fearful of each other’s strategic intentions and using fiscal resources to increase economic self-sufficiency. The result is regionalization rather than globalization. Chinese and Russian attempts to revise the world order, and the US’s attempt to contain them, encourages regionalization. For example, the trade war between the US and China is morphing into a broader competition that limits cooperation to a few select areas, despite a change of administration in the United States. The further consolidation of President Xi Jinping’s strongman rule will exacerbate this dynamic of distrust and economic divorce. Emerging Asia and emerging Europe live on the fault lines of this shift from globalization to regionalism, with various risks and opportunities. Generally we are bullish EM Asia and bearish EM Europe. 3. Populism And Nationalism A third strategic theme consists of populism and nationalism, or anti-establishment political sentiment in general. These forces will flare up in various forms across the world in 2022 and beyond. Even as unemployment declines, the rise in food and fuel inflation will make it difficult for low wage earners to make ends meet. The “misery index,” which combines unemployment and inflation, spiked during the pandemic and today stands at 10.8% in the US and 11.4% in the EMU, up from 5.2% and 8.1% before the pandemic, respectively (Chart 12). Large budget deficits and trade deficits, especially in the US and UK, feed into this inflationary environment. Most of the major developed markets have elected new governments since the pandemic, with the notable exception of France and Spain. Thus they have recapitalized their political systems and allowed voters to vent some frustration. These governments now have some time to try to mitigate inflation before the next election. Hence policy continuity is not immediately in jeopardy, which reduces uncertainty for investors. By contrast, many of the emerging economies face higher inflation, weak growth, and are either coming upon elections or have undemocratic political systems. Either way the result will be a failure to address household grievances promptly. The misery index is trending upward and governments are continually forced to provide larger budget deficits to shore up growth, fanning inflation (Chart 13). Chart 12DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

DM: Political Risk High But New Governments In Place

Chart 13EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

EM: Political Risk High But Governments Not Recapitalized

Chart 14EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

EM Populism/Nationalism Threatens Negative Surprises In 2022

Just as social and political unrest erupted after the Great Recession, notably in the so-called “Arab Spring,” so will new movements destabilize various emerging markets in the wake of Covid-19. Regime instability and failure can lead to big changes in policies, large waves of emigration, wars, and other risks that impact markets. The risks are especially high unless and until Chinese imports revive. Investors should be on the lookout for buying opportunities in emerging markets once the bad news is fully priced. National and local elections in Brazil, India, South Korea, the Philippines, and Turkey will serve as market catalysts, with bad news likely to precede good news (Chart 14). Bottom Line: These three themes – great power rivalry, hypo-globalization, and populism/nationalism – are inflationary in theory, though their impact will vary based on specific events. Multipolarity means that governments will boost industrial and defense spending to gear up for international competition. Hypo-globalization means countries will attempt to put growth on a more reliable domestic foundation rather than accept dependency on an unreliable international scene, thus constraining supplies from abroad. Populism and nationalism will lead to a range of unorthodox policies, such as belligerence abroad or extravagant social spending at home. Of course, the inflationary bias of these themes can be upset if they manifest in ways that harm growth and/or inflation expectations, which is possible. But the general drift will be an inflationary policy setting. Inflation may subside in 2022 only to reemerge as a risk later. Three Key Views For 2022 Within this broader context, our three key views for 2022 are as follows: 1. China’s Reversion To Autocracy As President Xi Jinping leads China further down the road of strongman rule and centralization, the country faces a historic confluence of internal and external risks. This was our top view in 2021 and the same dynamic continues in 2022. The difference is that in 2021 the risk was excessive policy tightening whereas this coming year the risk is insufficient policy easing. Chart 15China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China Eases Fiscal Policy To Secure Recovery In 2022

China’s economy is witnessing a secular slowdown, a deterioration in governance, property market turmoil, and a rise in protectionism abroad. The long decline in corporate debt growth points to the structural slowdown. Animal spirits will not improve in 2022 so government spending will be necessary to try to shore up overall growth. The Politburo signaled that it will ease fiscal policy at the Central Economic Work Conference in early December, a vindication of our 2021 view. Neither the combined fiscal-and-credit impulse nor overall activity, indicated by the Li Keqiang Index, have shown the slightest uptick yet (Chart 15). Typically it takes six-to-nine months for policy easing to translate to an improvement in real economic activity. The first half of the year may still bring economic disappointments. But policymakers are adjusting to avoid a crash. Policy will grow increasingly accommodative as necessary in the first half of 2022. The key political constraint is the Communist Party’s all-important political reshuffle, the twentieth national party congress, to be held in fall 2022 (usually October). While Xi may not want the economy to surge in 2022, he cannot afford to let it go bust. The experience of previous party congresses shows that there is often a policy-driven increase in bank loans and fixed investment. Current conditions are so negative as to ensure that the government will provide at least some support, for instance by taking a “moderately proactive approach” to infrastructure investment (Chart 16). Otherwise a collapse of confidence would weaken Xi’s faction and give the opposition faction a chance to shore up its position within the Communist Party. Chart 16China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

China Aims For Stability, Not Rapid Growth, Ahead Of 20th National Party Congress

Party congresses happen every five years but the ten-year congresses, such as in 2022, are the most important for the country’s overall political leadership. The party congresses in 1992, 2002, and 2012 were instrumental in transferring power from one leader to the next, even though the transfer of power was never formalized. Back in 2017 Xi arranged to stay in power indefinitely but now he needs to clinch the deal, lest any unforeseen threat emerge from at home or abroad. Xi’s success in converting the Communist Party from “consensus rule” to his own “personal rule” will be measurable by his success in stacking the Politburo and Politburo Standing Committee with factional allies. He will also promote his faction across the Central Committee so as to shape the next generations of party leaders and leave his imprint on policy long after his departure. The government will be extremely sensitive to any hint of dissent or resistance and will move aggressively to quash it. Investors should not be surprised to see high-level sackings of public officials or private magnates and a steady stream of scandals and revelations that gain prominence in western media. The environment is also ripe for strange and unexpected incidents that reveal political differences beneath the veneer of unity in China: defections, protests, riots, terrorist acts, or foreign interference. Most incidents will be snuffed out quickly but investors should be wary of “black swans” from China in 2022. Chinese government policies will not be business friendly in 2022 aside from piecemeal fiscal easing. Everything Beijing does will be bent around securing Xi’s supremacy at all levels. Domestic politics will take precedence over economic concerns, especially over the interests of private businesses and foreign investors, as is clear when it comes to managing financial distress in the property sector. Negative regulatory surprises and arbitrary crackdowns on various industrial sectors will continue, though Beijing will do everything in its power to prevent the property bust from triggering contagion across the economic system. This will probably work, though the dam may burst after the party congress. Relations with the US and the West will remain poor, as the democracies cannot afford to endorse what they see as Xi’s power grab, the resurrection of a Maoist cult of personality, and the betrayal of past promises of cooperation and engagement. America’s midterm election politics will not be conducive to any broad thaw in US-China relations. While China will focus on domestic politics, its foreign policy actions will still prove relatively hawkish. Clashes with neighbors may be instigated by China to warn away any interference or by neighbors to try to embarrass Xi Jinping. The South and East China Seas are still ripe for territorial disputes to flare. Border conflicts with India are also possible. Taiwan remains the epicenter of global geopolitical risk. A fourth Taiwan Strait Crisis looms as China increases its military warnings to Taiwan not to attempt anything resembling independence (Chart 17A). China may use saber-rattling, economic sanctions, cyber war, disinformation, and other “gray zone” tactics to undermine the ruling party ahead of Taiwan’s midterm elections in November 2022 and presidential elections in January 2024. A full-scale invasion cannot be ruled out but is unlikely in the short run, as China still has non-military options to try to arrange a change of policy in Taiwan.

Chart 17

Chart 17BMarket-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

Market-Based Risk Indicators Say China/Taiwan Risk Has Not Peaked

China has not yet responded to the US’s deployment of a small number of troops in Taiwan or to recent diplomatic overtures or arms sales. It could stage a major show of force against Taiwan to help consolidate power at home. China also has an interest in demonstrating to US allies and partners that their populations and economies will suffer if they side with Washington in any contingency. Given China’s historic confluence of risks, it is too soon for global investors to load up on cheap Chinese equities. Volatility will remain high. Weak animal spirits, limited policy easing, high levels of policy uncertainty, regulatory risk, ongoing trade tensions, and geopolitical risks suggest that investors should remain on the sidelines, and that a large risk premium can persist throughout 2022. Our market-based geopolitical risk indicators for both China and Taiwan are still trending upwards (Chart 17B). Global investors should capitalize on China’s policy easing indirectly by investing in commodities, cyclical equity sectors, and select emerging markets. 2. America’s Policy Insularity Our second view for 2022 centers on the United States, which will focus on domestic politics and will thus react or overreact to the many global challenges it faces. The US faces the first midterm election after the chaotic and contested 2020 presidential election. Political polarization remains at historically high levels, meaning that social unrest could flare up again and major domestic terrorist incidents cannot be ruled out. So far the Biden administration has focused on the domestic scene: mitigating the pandemic and rebooting the economy. Biden’s signature “Build Back Better” bill, $1.75 trillion investment in social programs, has passed the House of Representatives but not the Senate. The spike in inflation has shaken moderate Democratic senators who are now delaying the bill. We expect it to pass, since tax hikes were dropped, but our conviction is low (65% subjective odds), as a single defection would derail the bill. The implication would be inflationary since it would mark a sizable increase in government spending at a time when the output gap is already virtually closed. Spending would likely be much larger than the Congressional Budget Office estimate, shown in Chart 18, because the bill contains various gimmicks and hard-to-implement expiration clauses. Equity markets may not sell if the bill fails, since more fiscal stimulus would put pressure on the Federal Reserve to hike rates faster.

Chart 18

Chart 19

Whether the bill passes or fails, Biden’s legislative agenda will be frozen thereafter. He will have to resort to executive powers and foreign policy to lift his approval rating and court the median voter ahead of the midterm elections. Currently Democrats are lined up to lose the House and probably also the Senate, where a single seat would cost them their majority (Chart 19). The Senate is still in play so Biden will be averse to taking big risks. For the same reason, Biden’s foreign policy goal will be to stave off various bubbling crises. Restoring the Iranian nuclear deal was his priority but Russia has now forced its way to the top of the agenda by threatening a partial reinvasion of Ukraine. In this context Biden will not have room for maneuver with China. Congress will be hawkish on China ahead of the midterms, and Xi Jinping will be reviving autocracy, so Biden will not be able to improve relations much. Biden’s domestic policy could fuel inflation, while his domestic-focused foreign policy will embolden strategic rivals, which increases geopolitical risks. 3. Petro-State Leverage A surge in gasoline prices at the pump ahead of the election would be disastrous for a Democratic Party that is already in disarray over inflation (Chart 20). Biden has already demonstrated that he can coordinate an international release of strategic oil reserves this year. Oil and natural gas producers gain leverage when the global economy rebounds, commodity prices rise, and supply/demand balances tighten. The frequency of global conflicts, especially those involving petro-states, tend to rise and fall in line with oil prices (Chart 21). Chart 20Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Inflation Constrains Biden Ahead Of Midterms

Chart 21