Mid East Conflict

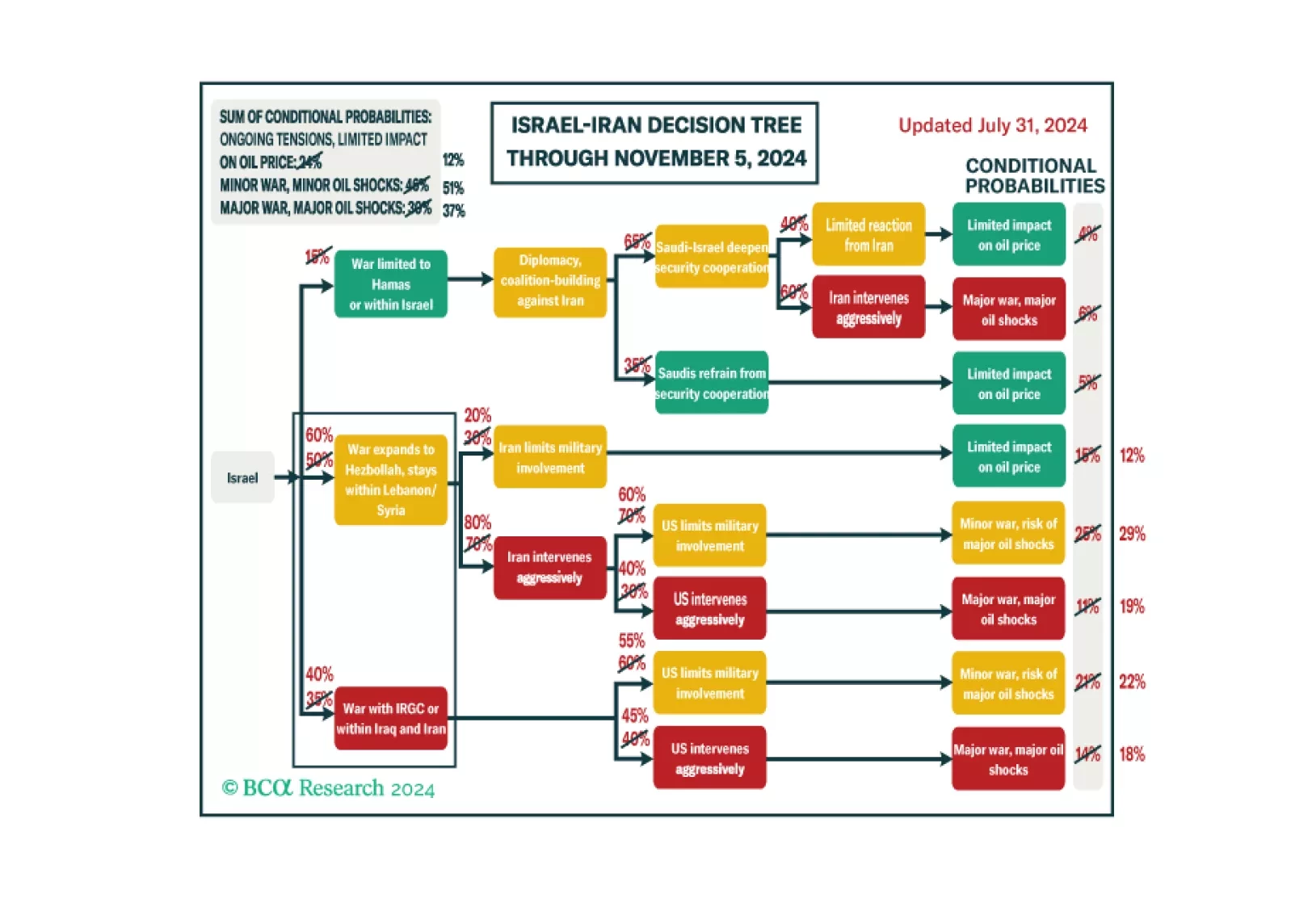

The war in the Middle East is expanding, upgrading our subjective odds of a major oil supply shock to 37% and underscoring our 60% odds of Republican victory in November. Volatility should spike again as investors contemplate the prospect of rising oil prices amid slowing US and global growth. Tactically investors should stay overweight energy stocks relative to other cyclicals and favor oil producers in the Americas rather than Middle East.

Investors should reduce risk, increase allocation to safe havens, and brace for oil price volatility and supply disruptions stemming from the Middle East over the next zero-to-12 months.

The Israeli-Arab crisis is more likely to expand and cause oil disruptions than market consensus holds. Close long dollar trades and go long energy and defense stocks relative to cyclicals.

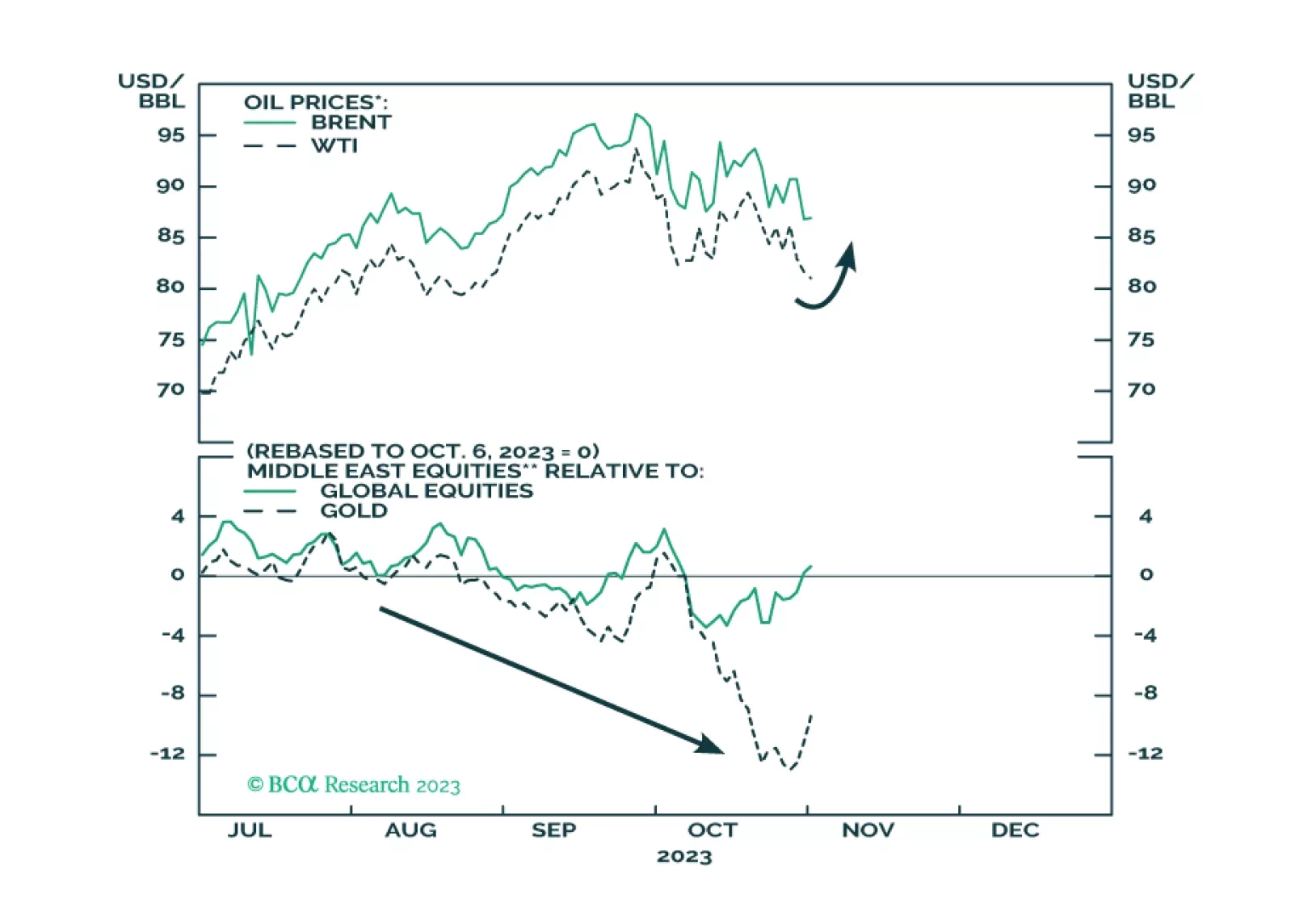

Volatility will remain the key dynamic in oil markets in the aftermath of the surprise Hamas attacks against Israel on October 7. The risk of a major oil supply shock has gone up, but meanwhile supply constraints will remain at variance with global growth problems stemming from restrictive monetary policy over the next 12 months. Favor bonds over stocks, large caps over small caps, defense and energy stocks over other cyclicals, and US equities relative to global equities.