Middle East

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.

Every year we highlight five low-odds scenarios that would have a major impact on global financial markets if they happened. This year we contemplate a total reversal of Chinese policy, a US-Iran nuclear deal, a breakdown of NATO, US military action across the Americas, and an internationally coordinated FX intervention.

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

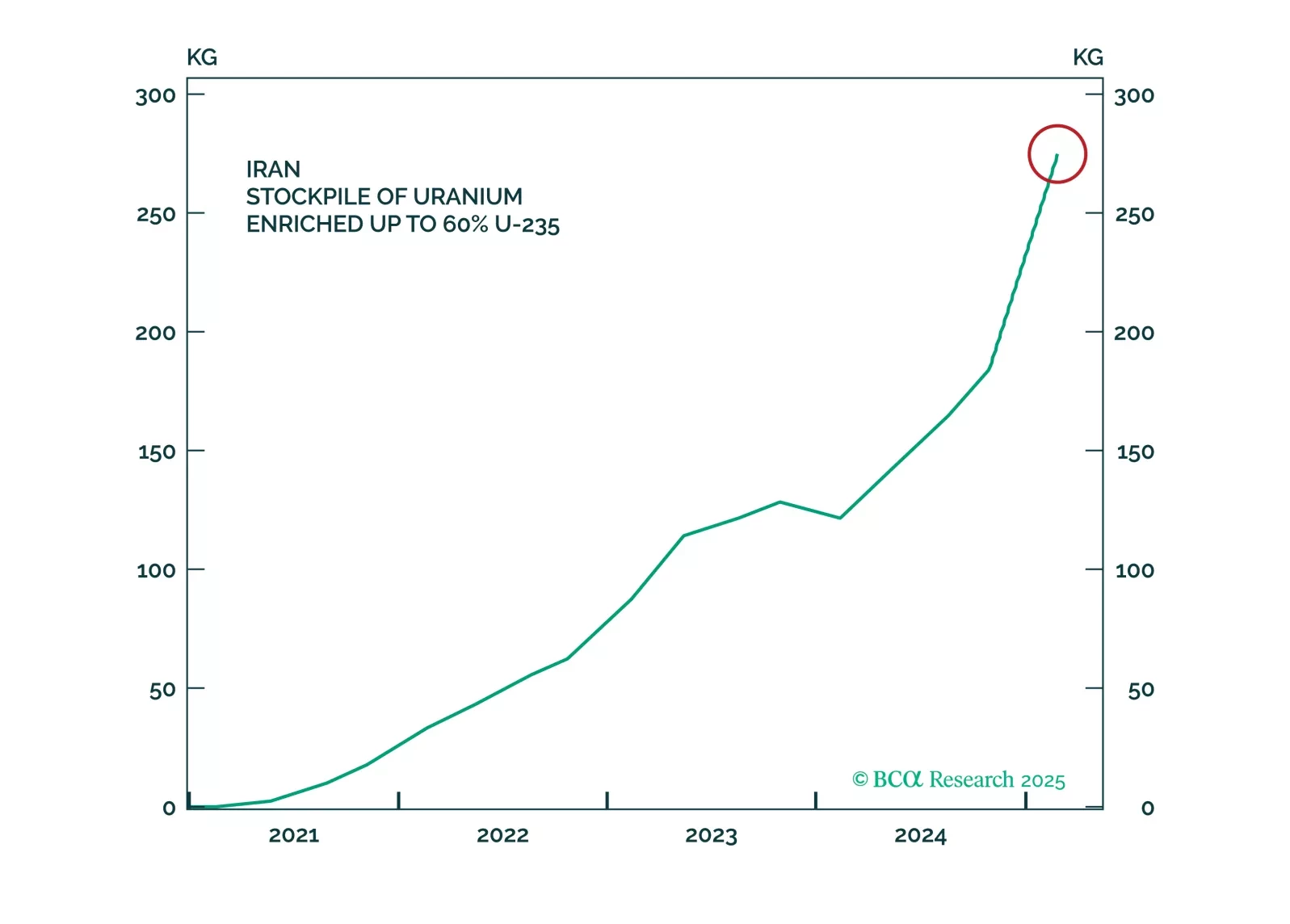

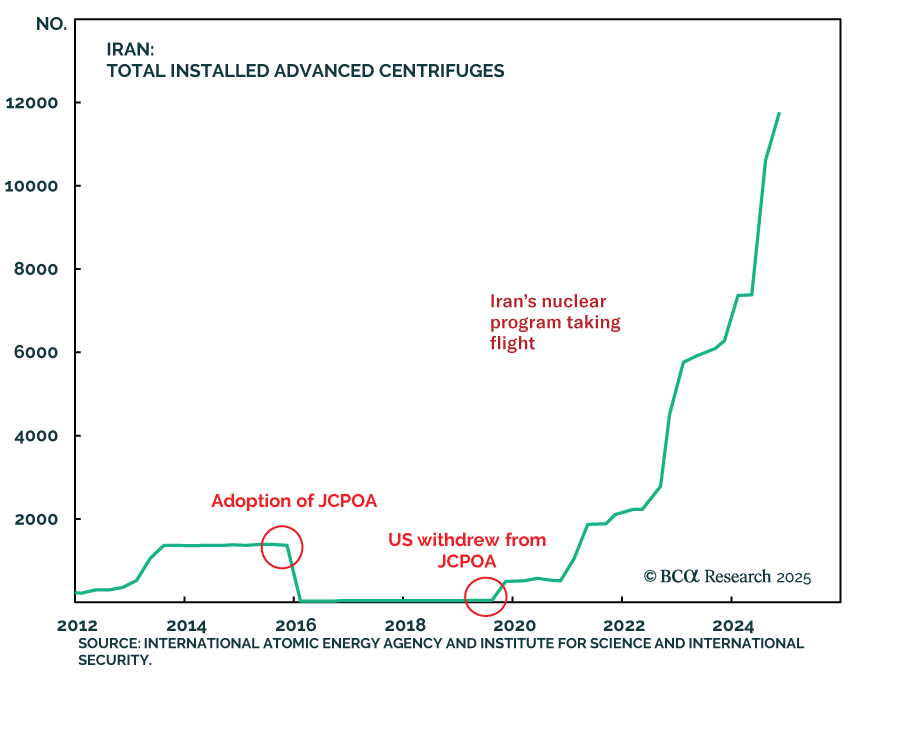

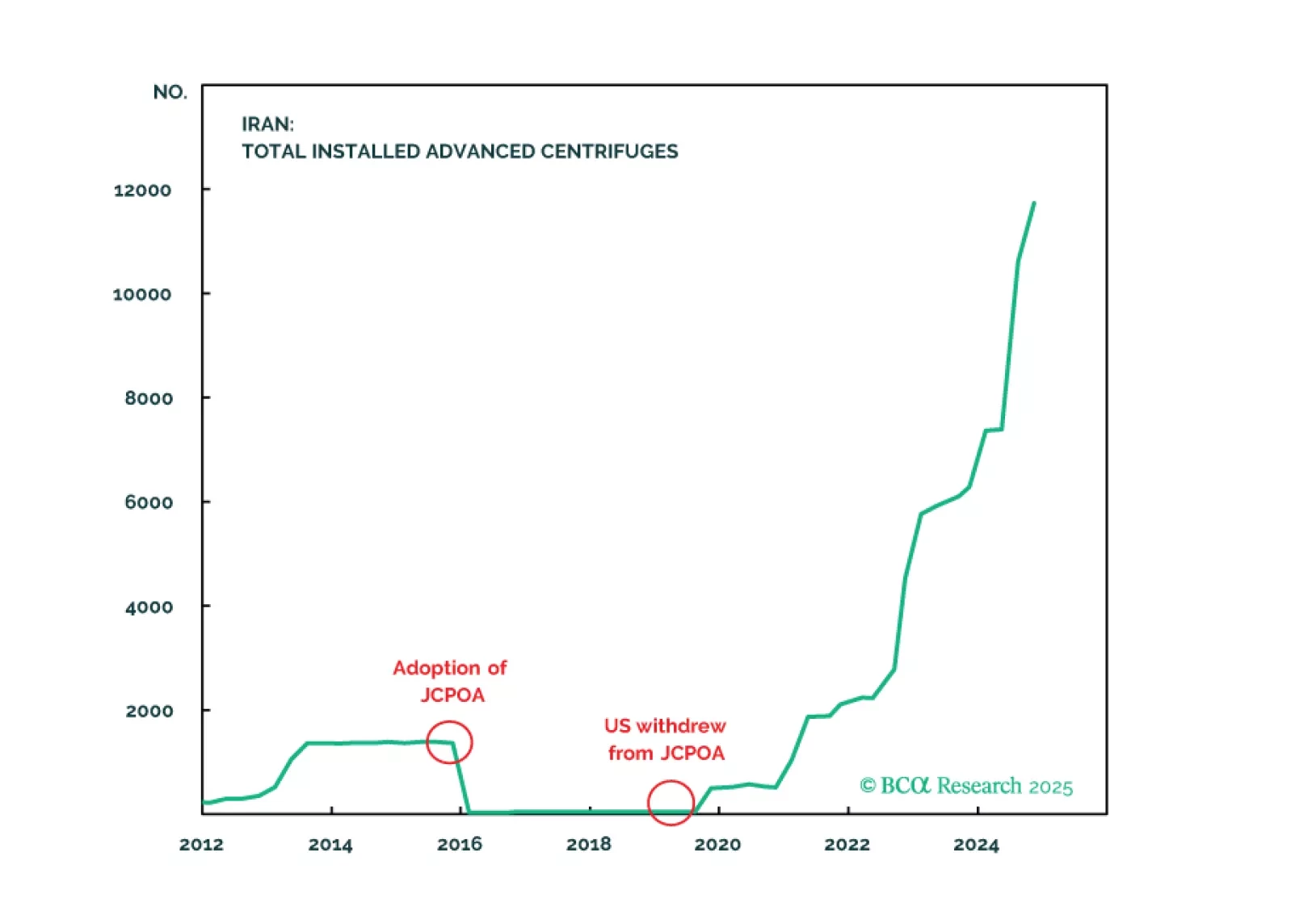

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.

We maintain 37% odds of a major recessionary oil shock, 51% odds of minor shocks, and 12% odds of no shocks.

October seasonality tends to be negative for stocks in an election year. That is the only thing that has stayed our hand from shifting out of our tactical underweight on US equities, initiated – poorly – in July.

But the big macro news from September has not been bearish. The Fed has signaled jumbo cuts. Within seven weeks, the US central bank intends to cut by 100bps! Meanwhile, China appears to have reached a “policy bottom,” with its September 26 Politburo meeting signaling an extraordinary rhetorical shift towards fiscal policy. As such, we are starting to sniff out global reflation, akin to the 2015-2016 mid-cycle slowdown.

The labor market data still worries us. It is clearly deteriorating, on paper. Is it because of an imminent recession or “normalization?” It is difficult to say. We are open minded.

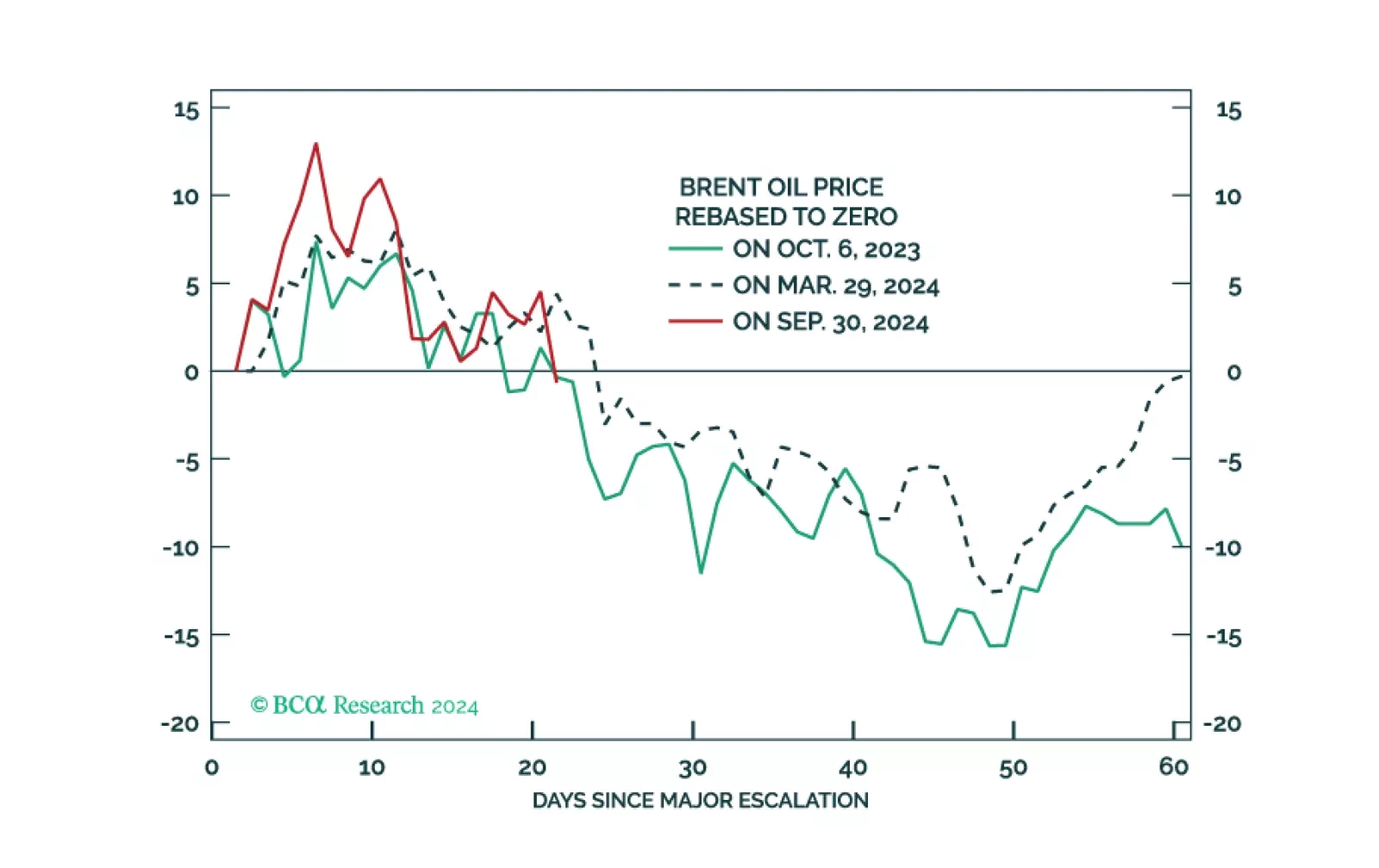

Finally, the Middle East tensions are again on the horizon. If Iran stays its hand against Saudi energy facilities – which we expect it to continue to do – the Iran-Israel conflict is a sideshow. Nonetheless, with global reflation afoot, we went long oil last week, on September 26. As such, geopolitics is a neat tailwind to that call.