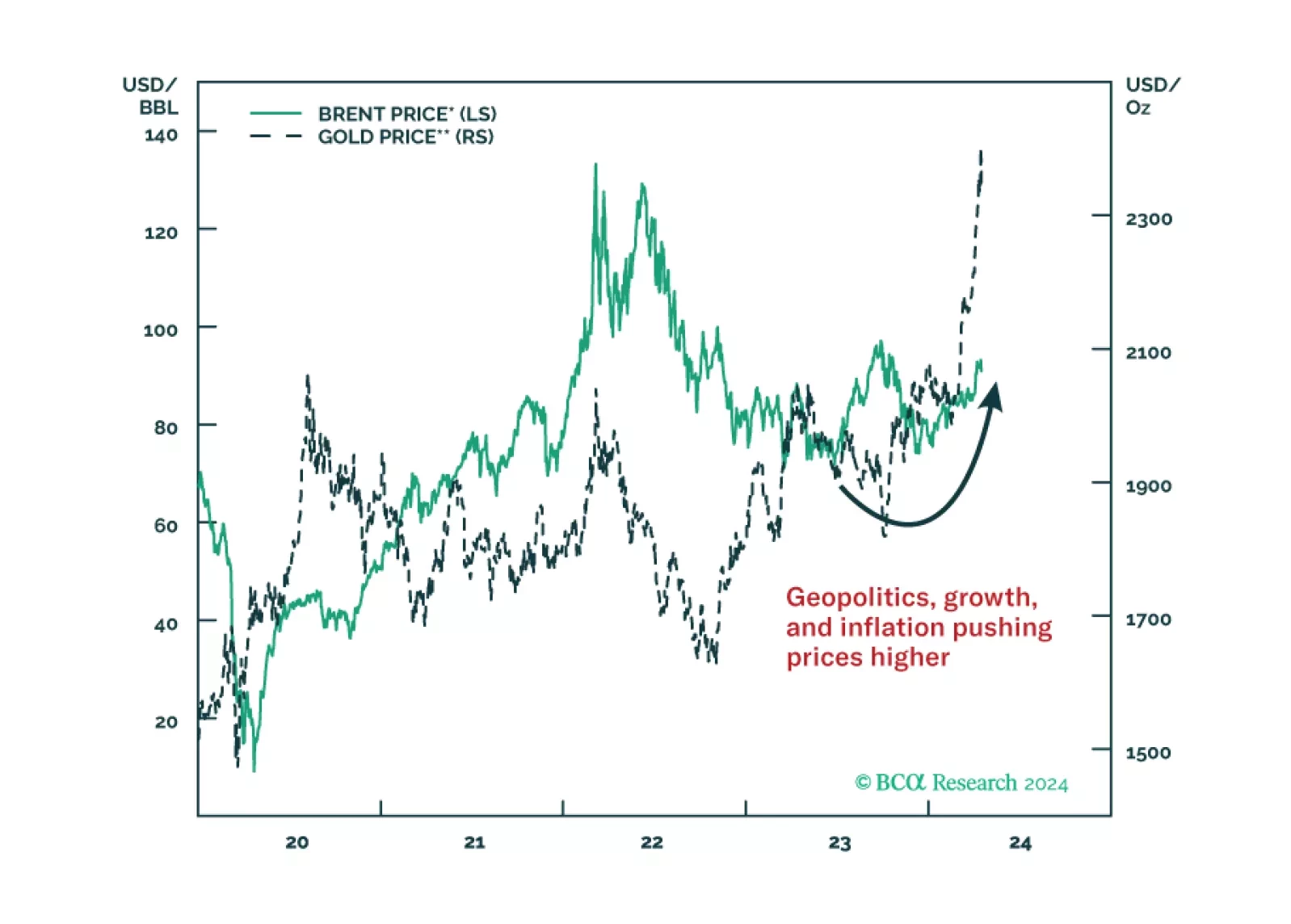

Middle East

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

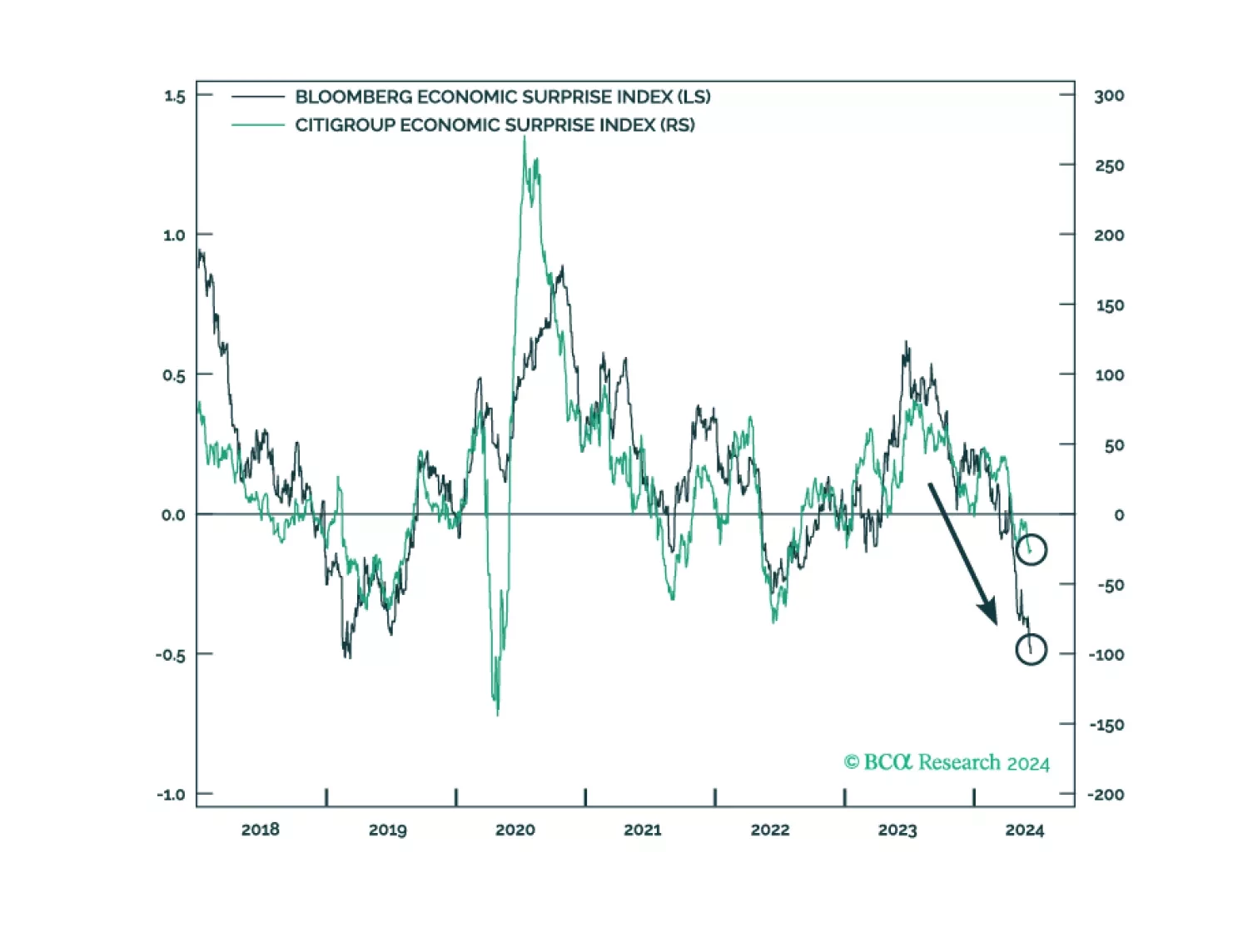

In Section I, we examine some concerning signs of US economic weakness that emerged in June. We also discuss portfolio positioning in the face of falling interest rates and cross-check our recommended US equity overweight in the face of extremely optimistic expectations about AI’s impact on growth. We conclude that defensive positioning continues to be warranted. In Section II, we dig into those optimistic expectations for AI. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. We doubt that AI will end up truly boosting economic activity by this magnitude.

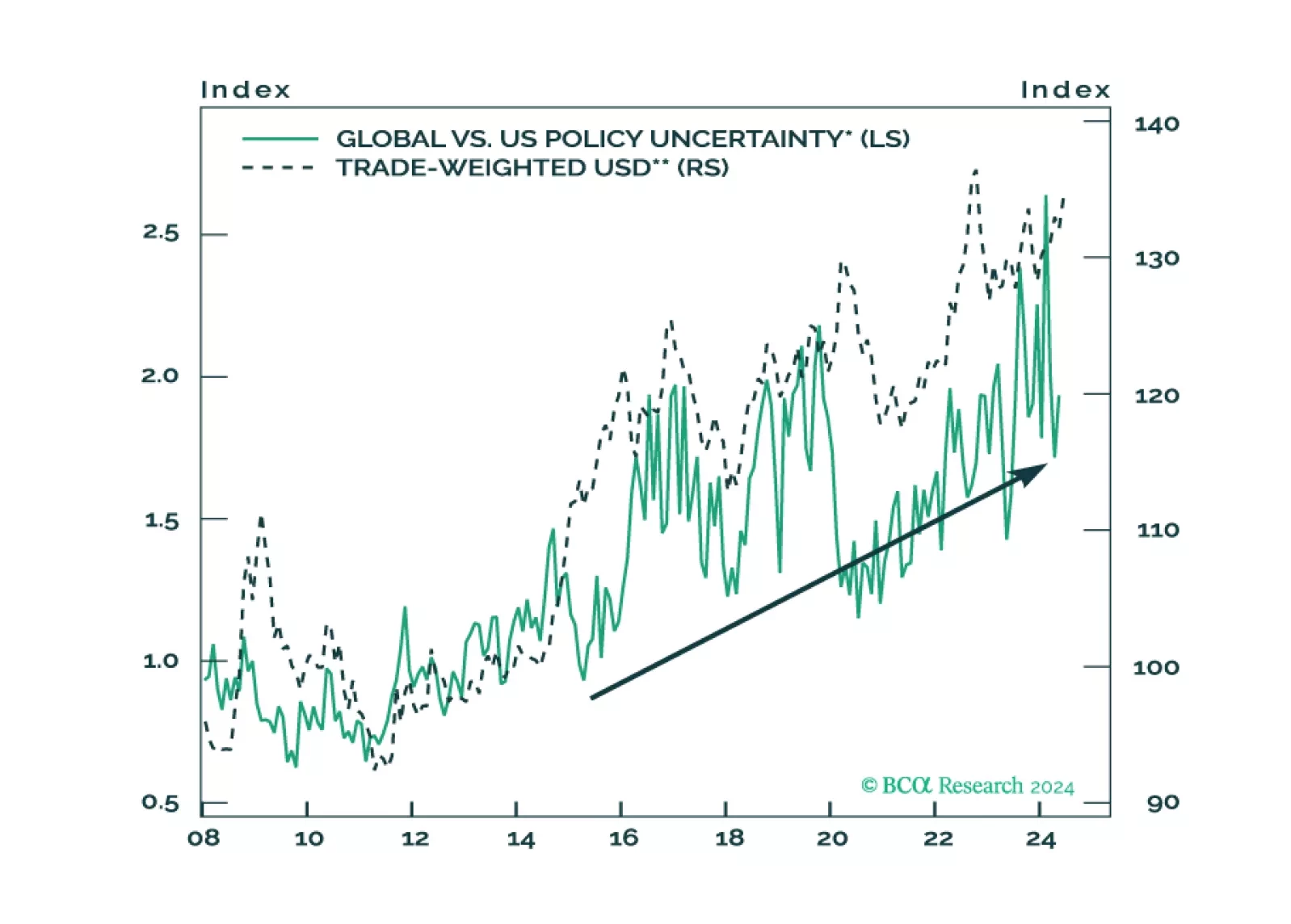

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.

The implication is that Israel chose not to escalate the risk of direct war with Iran. Hence we remain in our base-case “Minor War, Minor Oil Shock” scenario.

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.

In the near term, favor oil and oil producers outside the Gulf Arab states. Over a 12-month horizon, favor US and North American equities, defensive sectors over cyclicals, and safe-assets. Within cyclicals, stick to energy and defense.