Monetary

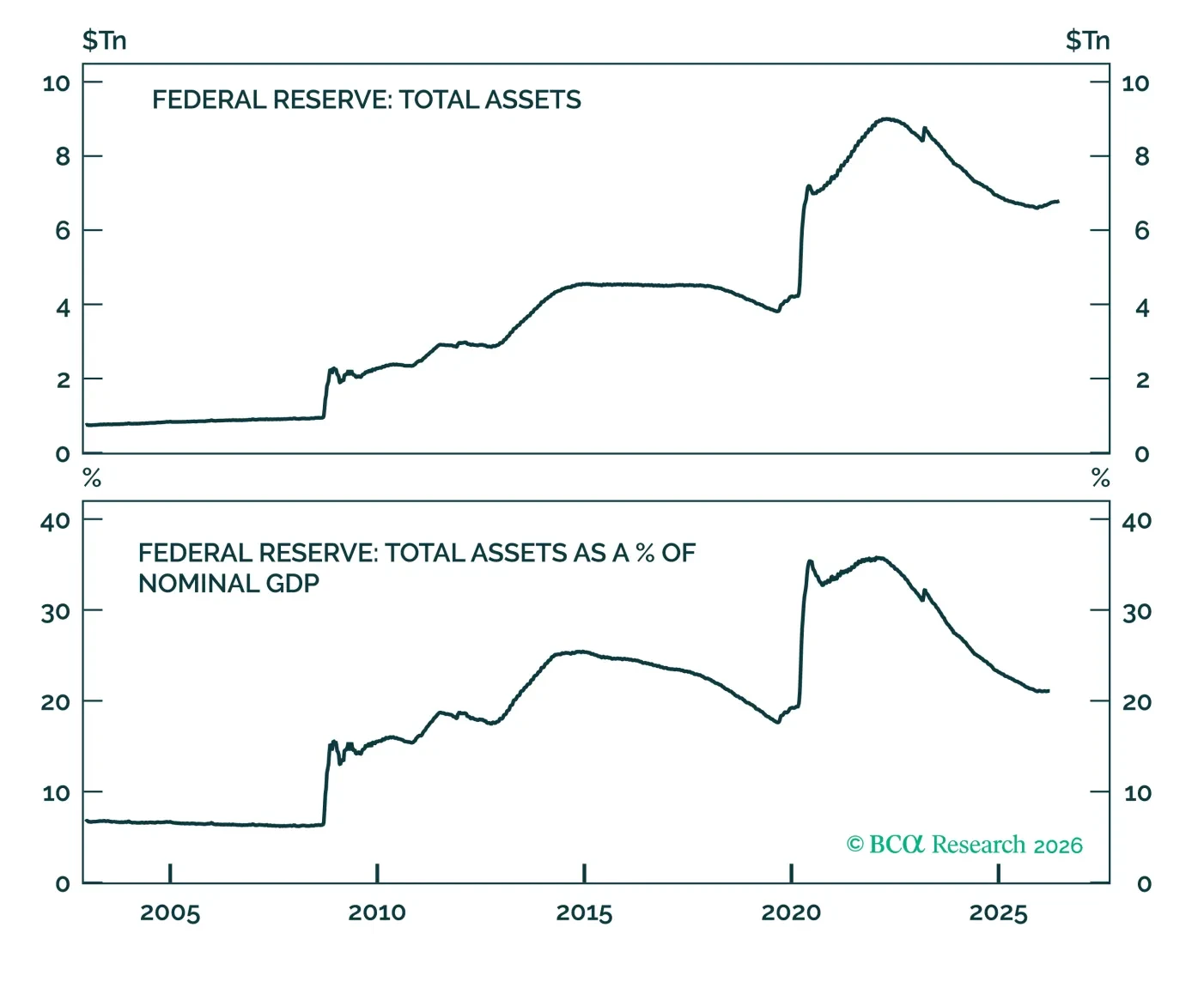

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.

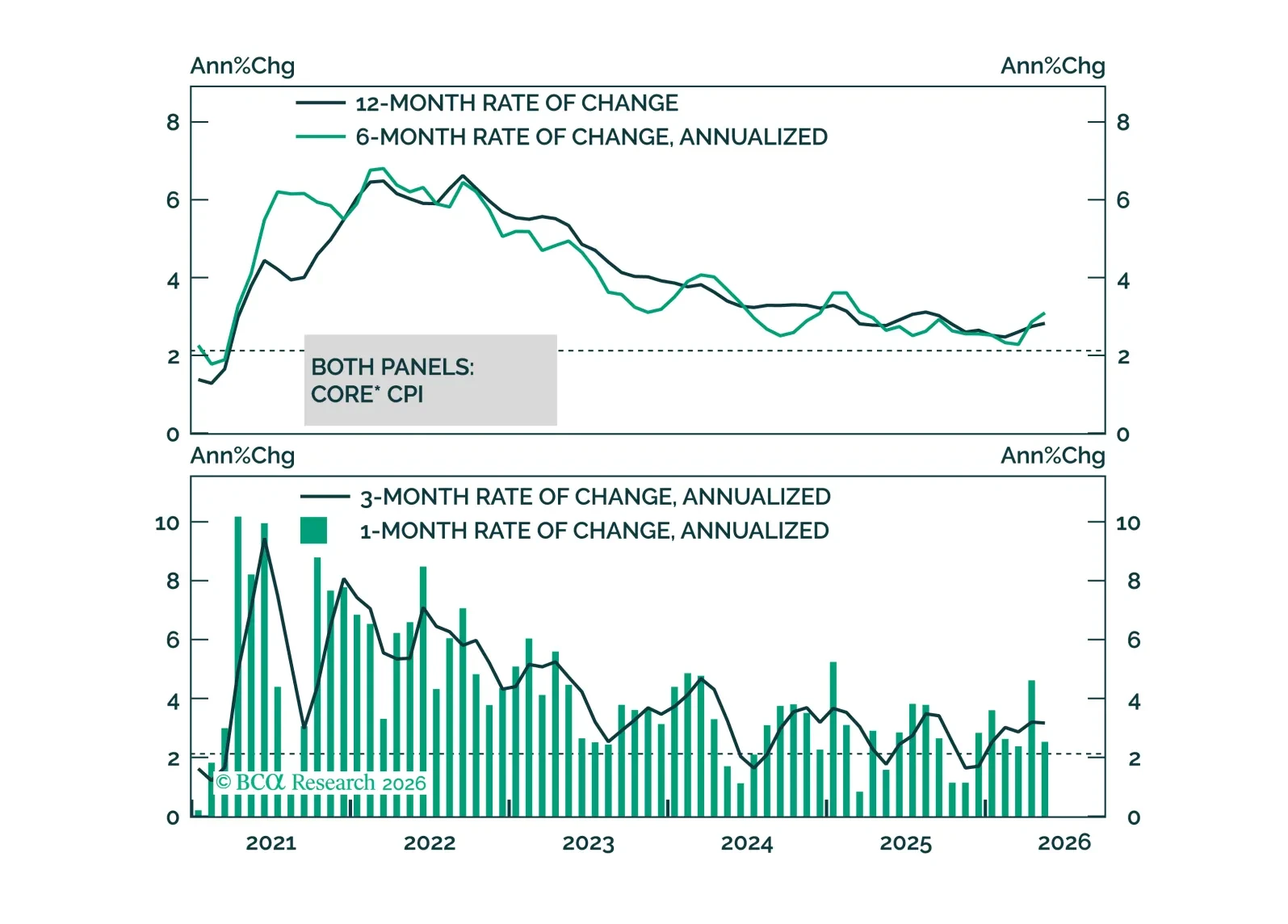

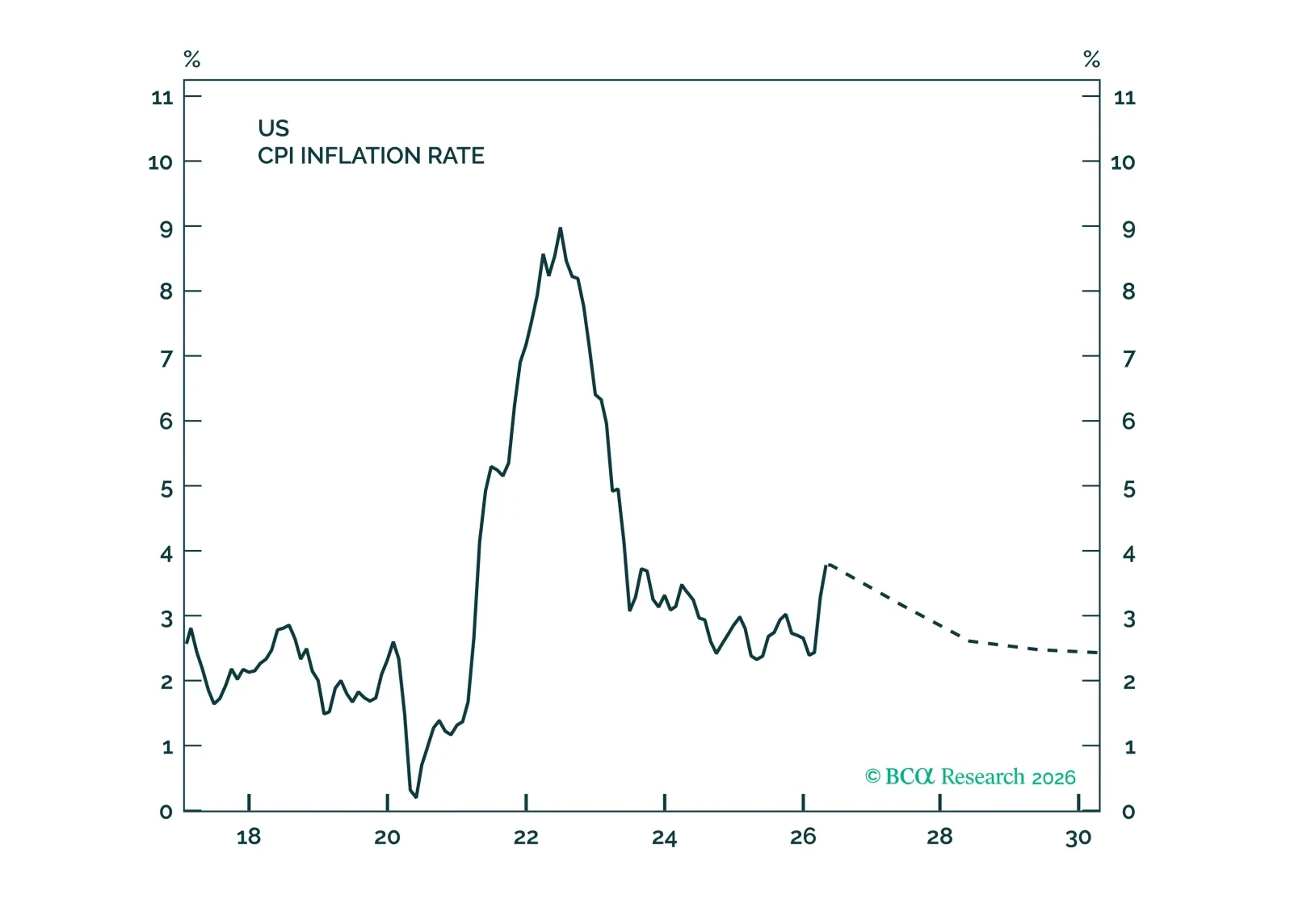

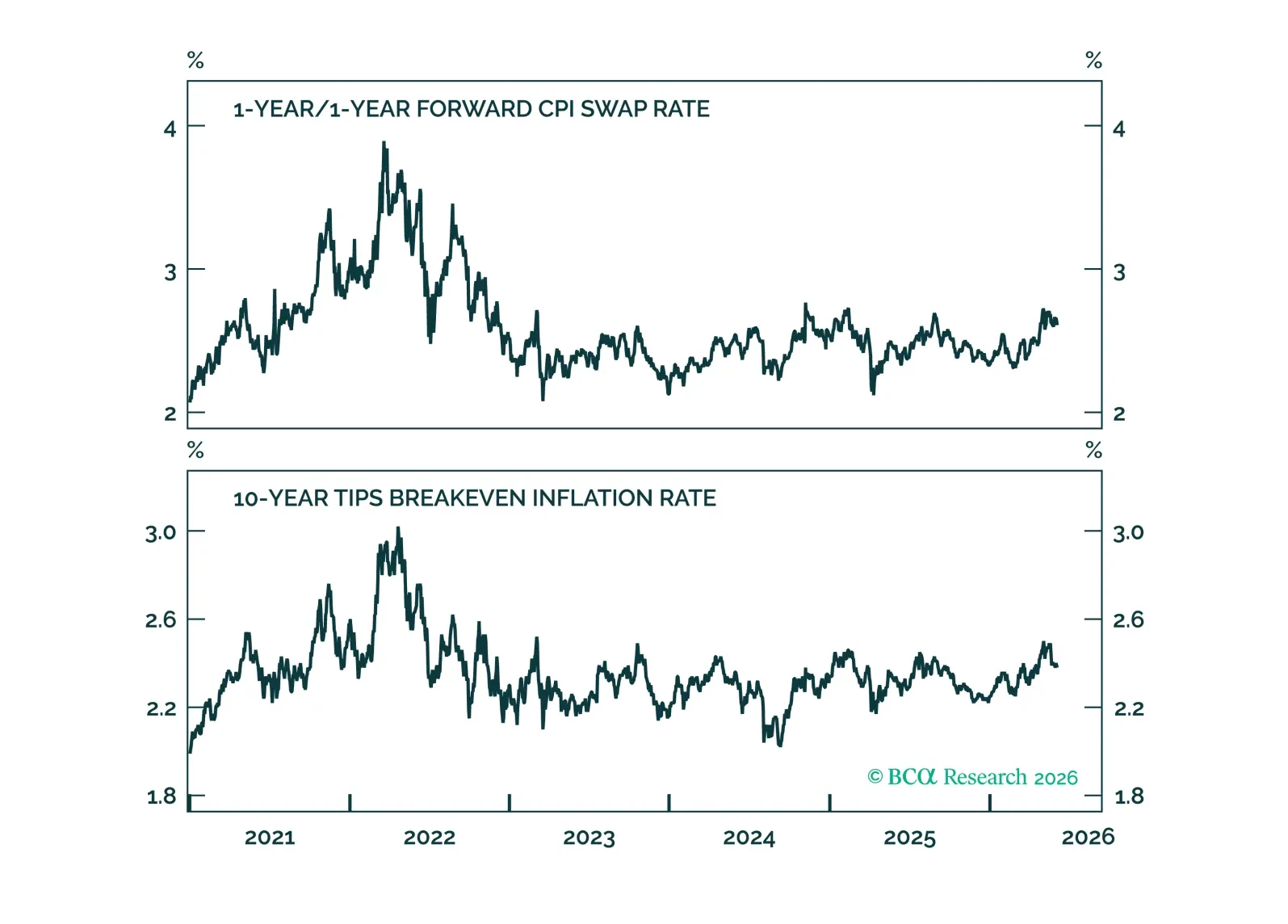

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

Our Portfolio Allocation Summary for June 2026.

Our Portfolio Allocation Summary for May 2026.

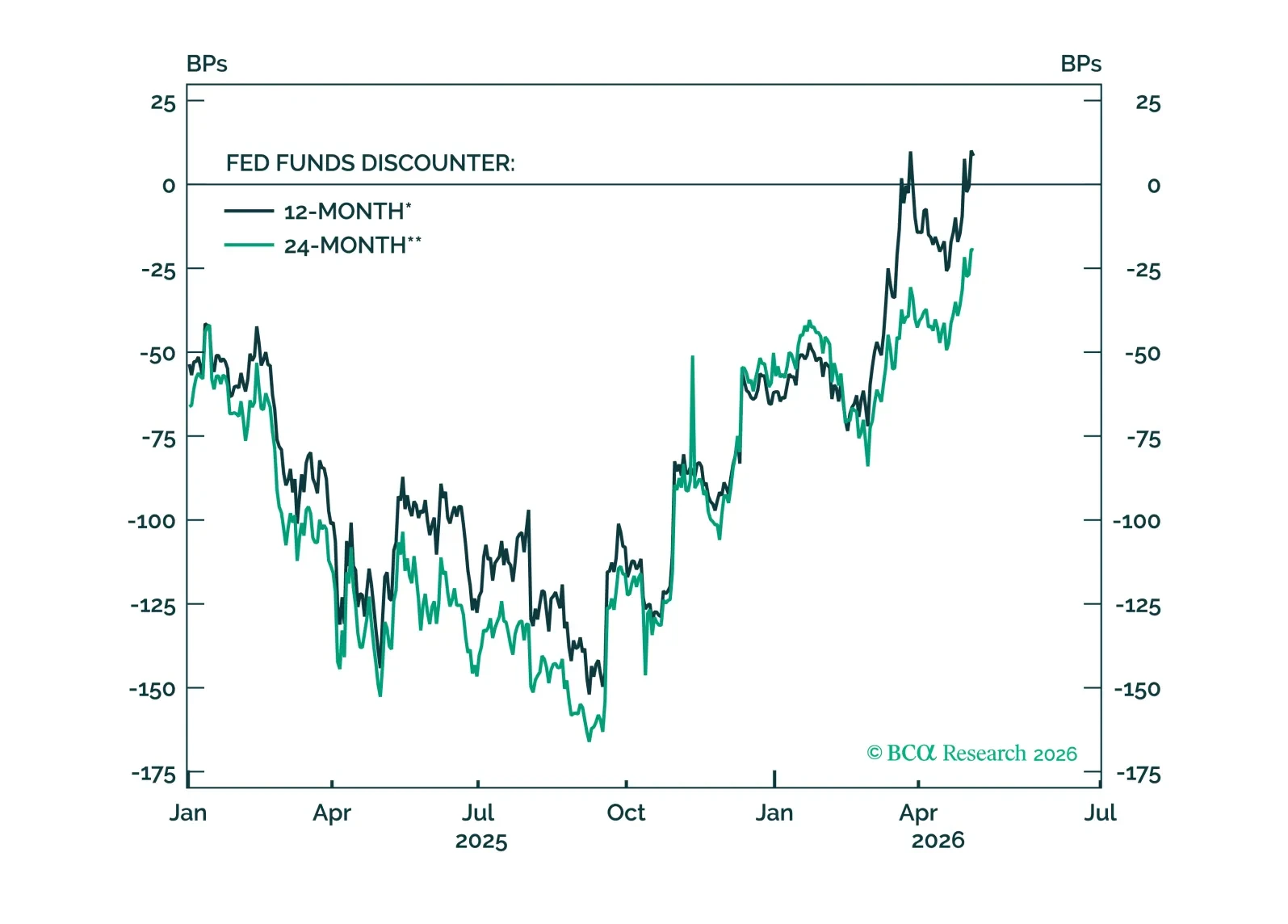

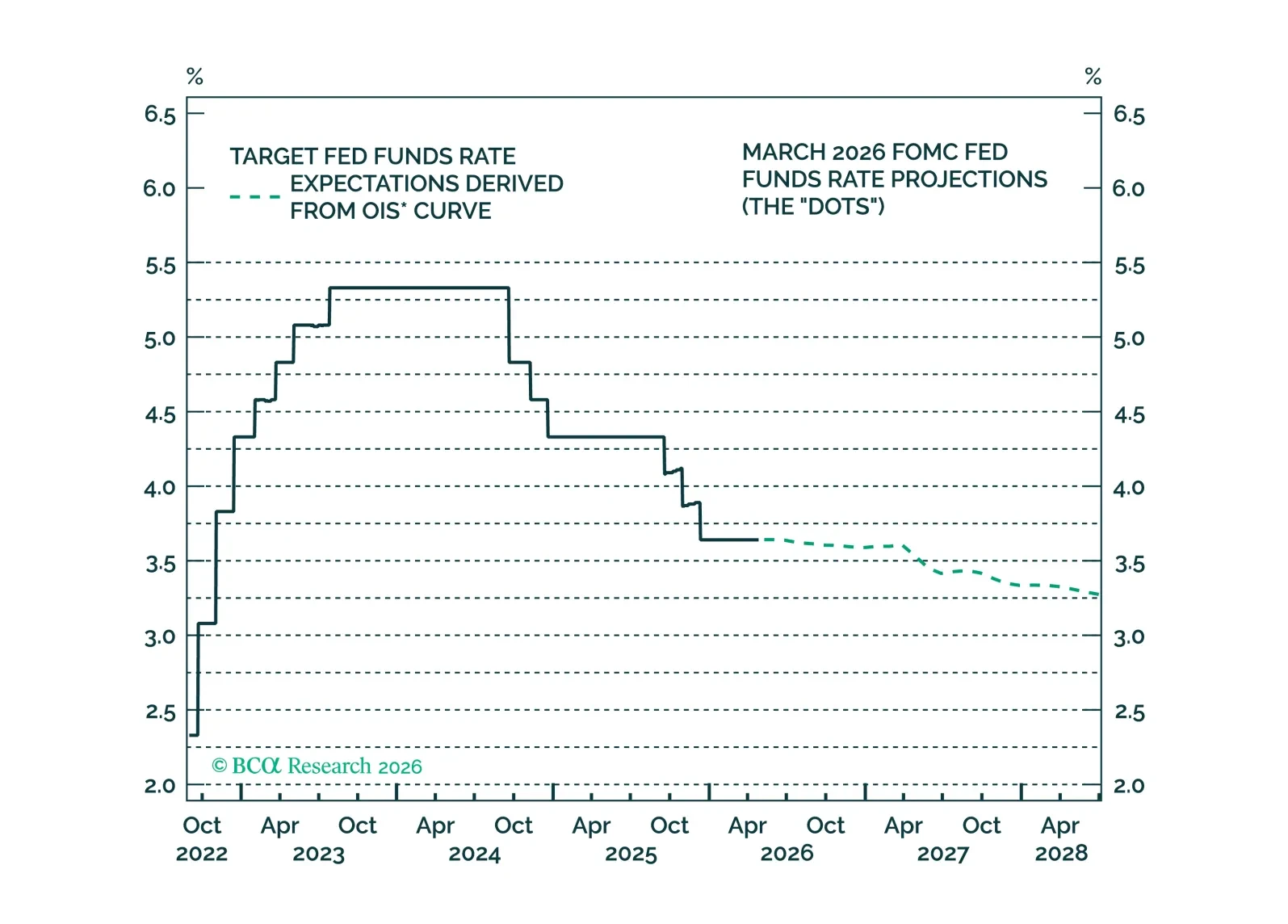

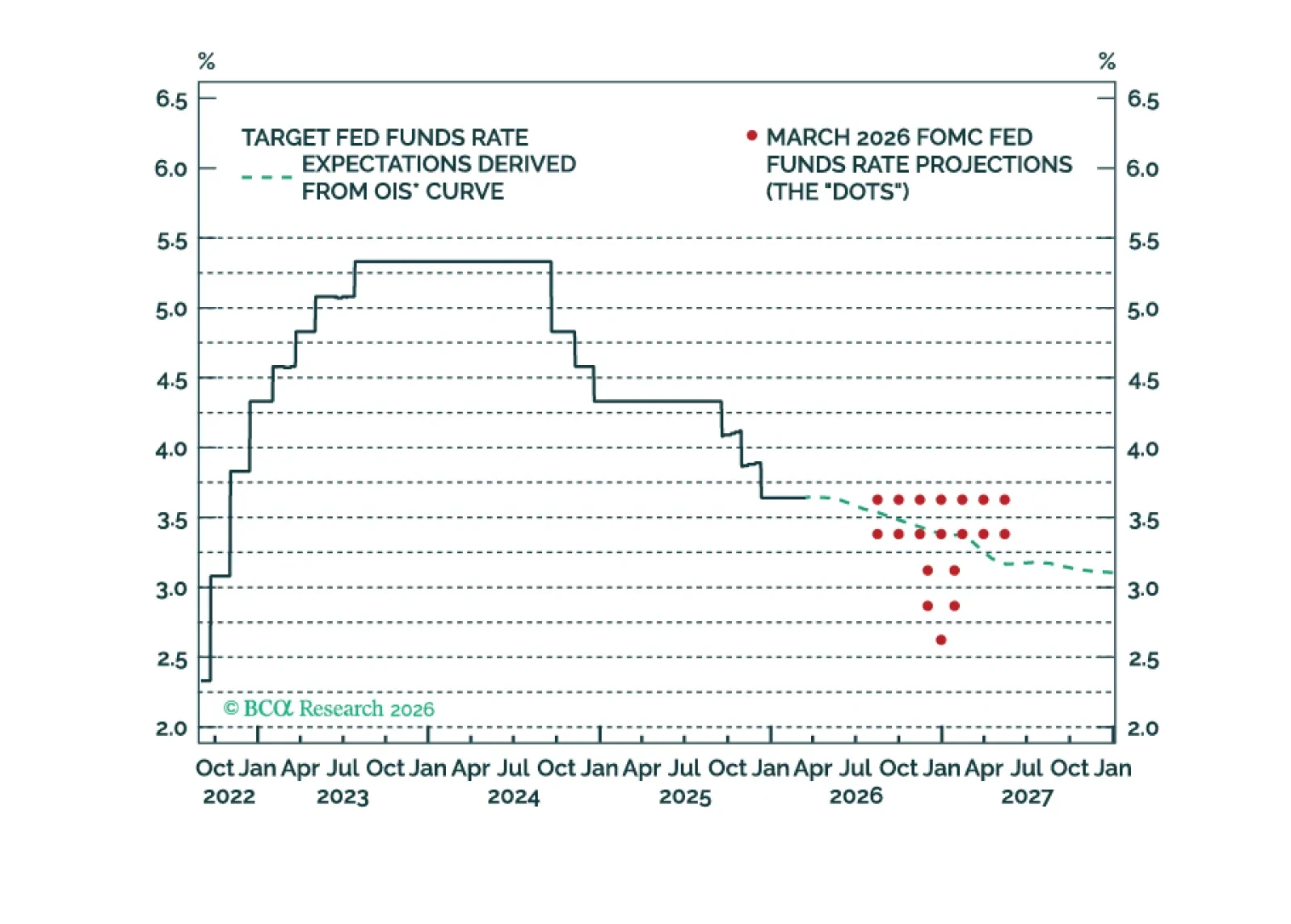

FOMC participants are coalescing around the idea that the funds rate will stay on hold for some time, an outcome that is now well priced in the bond market and that will not materially change under a new Fed Chair.

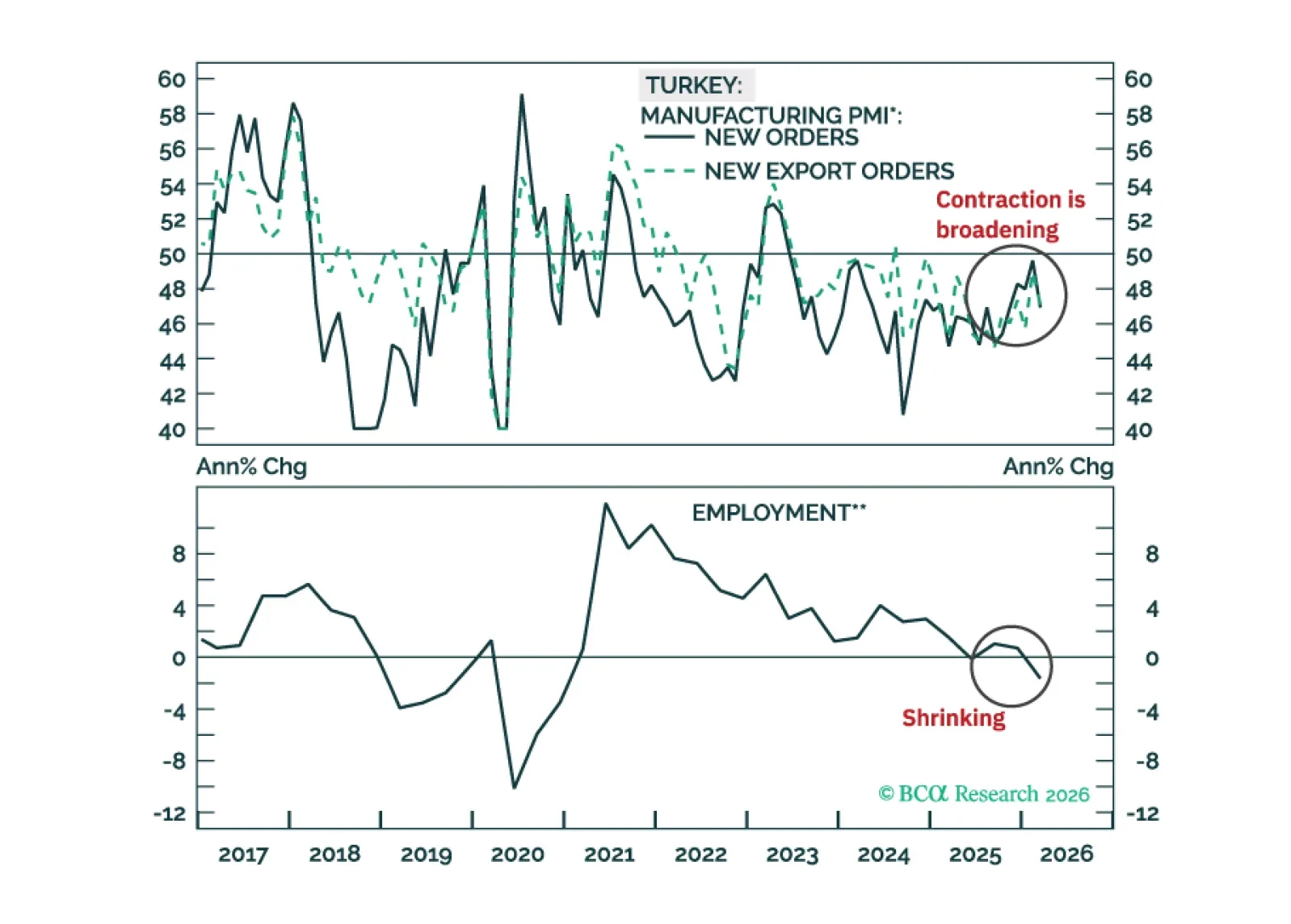

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

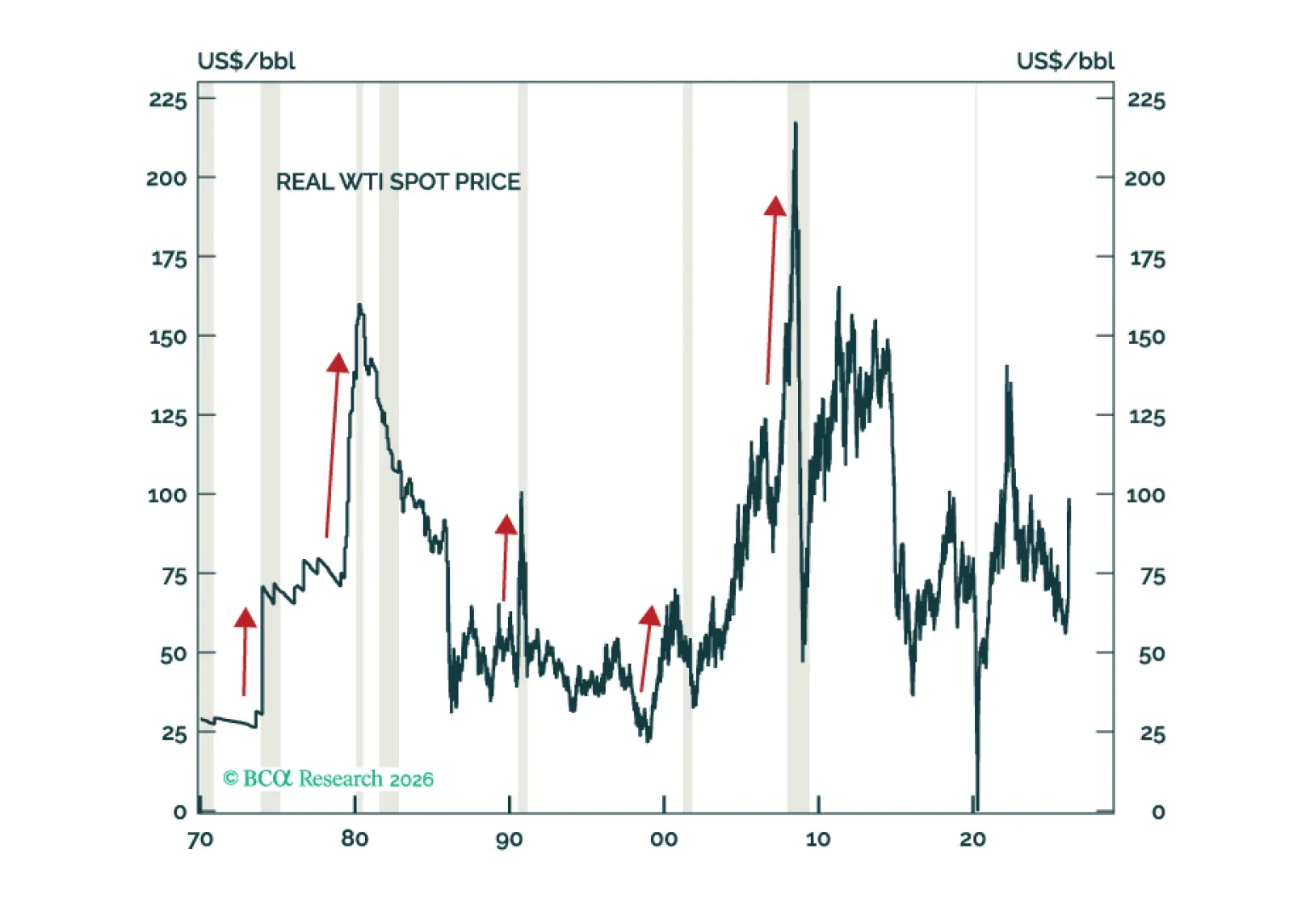

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

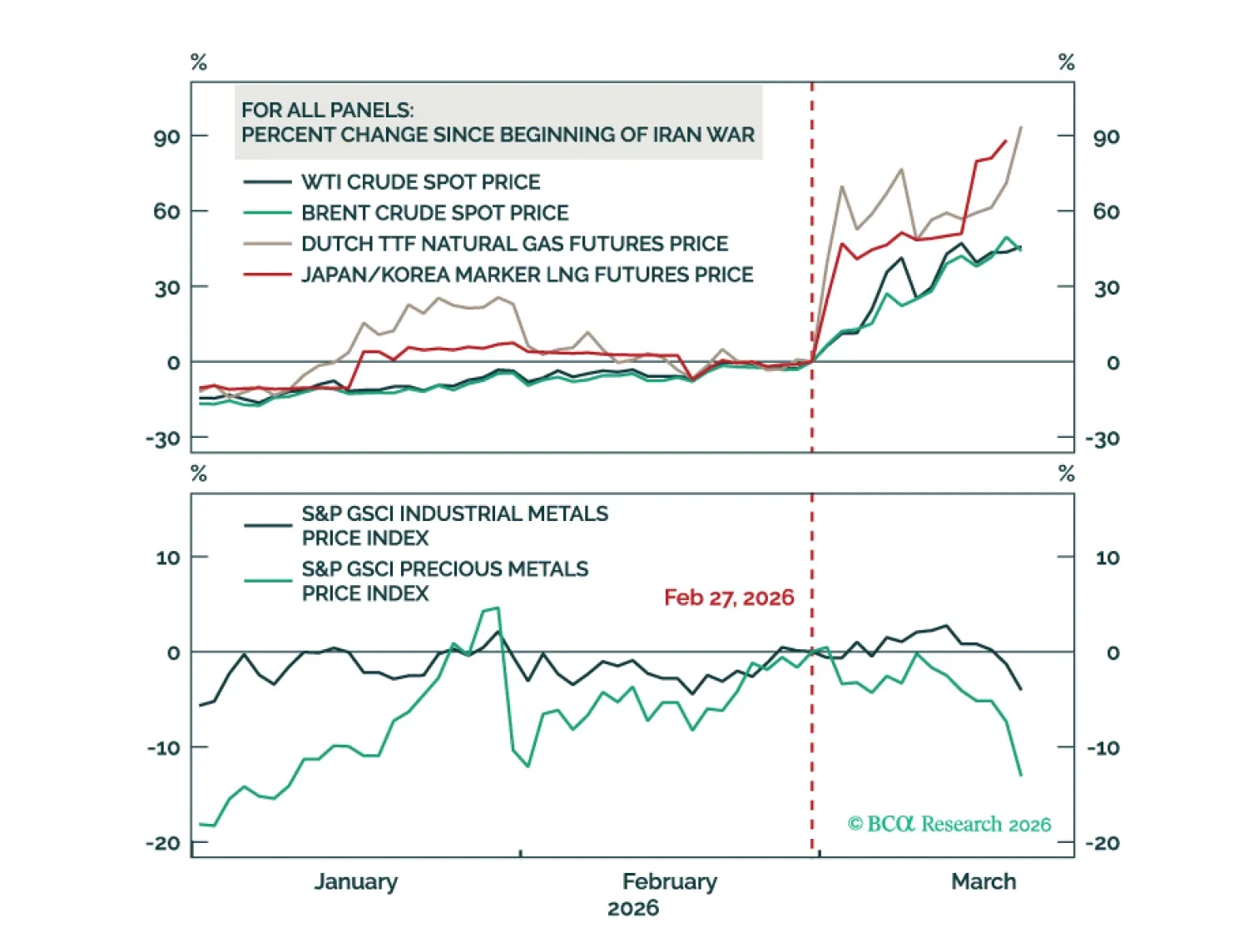

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.