Monetary

Deflationary pressures and weak core Europe growth support CE3 bond longs as rate cuts loom. The Czech and Hungarian central banks held rates steady at 3.5% and 6.5% this week, following Poland’s earlier decision to keep rates unchanged at 5.25%. While citing…

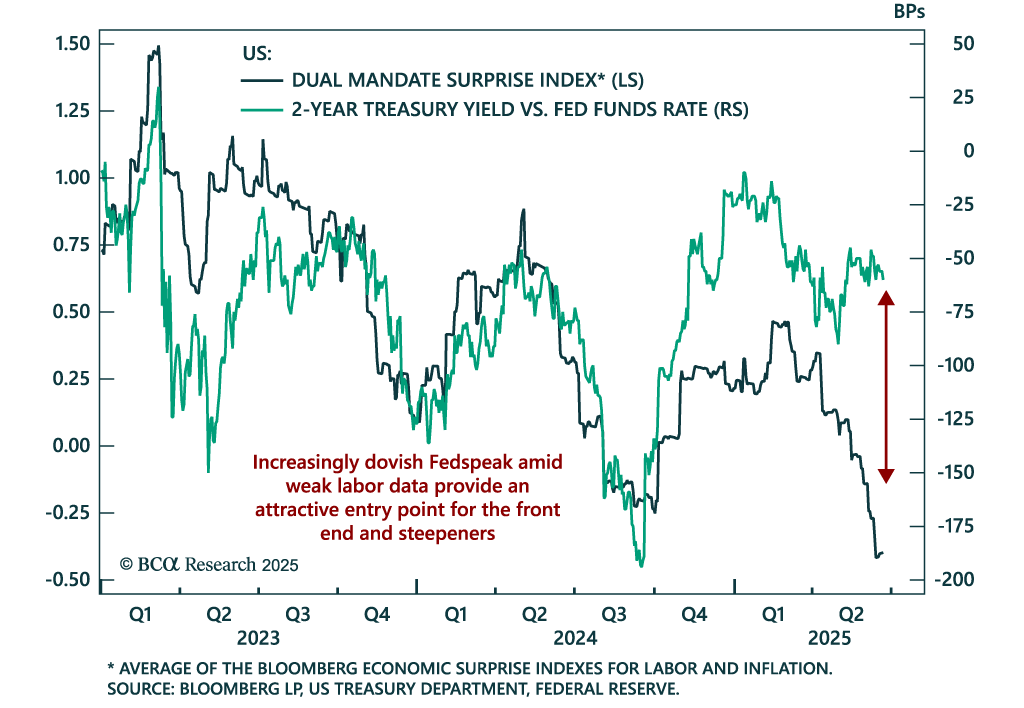

Dovish signals from Fed Governors Waller and Bowman increase the likelihood of a rate cut as early as July, supporting long front-end positions and steepeners. Last week’s FOMC meeting revealed a split between hawkish participants focused on the inflationary…

In this Insight, we highlight our strong conviction trades based on the central bank meetings held by the Bank of England, the Norges Bank, the Swiss National Bank and the Riksbank.

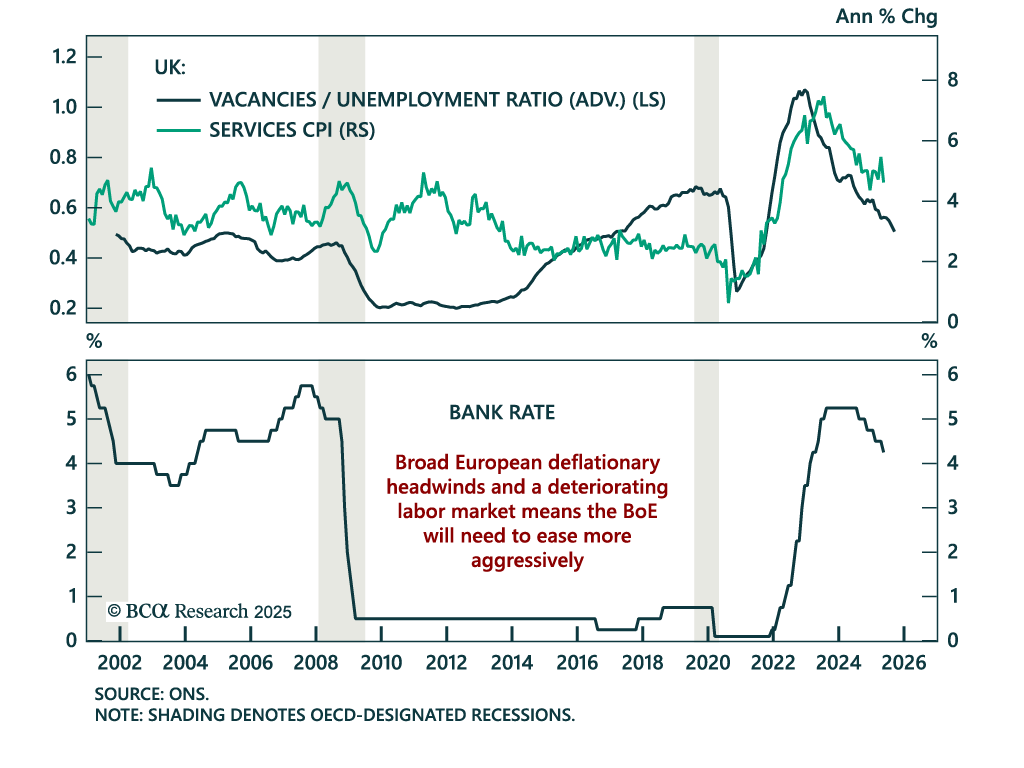

European central banks are pivoting quickly amid deflationary pressure, reinforcing our long UK Gilts and short GBP trades. The Norges Bank surprised with a 25 bps cut to 4.25%, abandoning its hawkish stance. The Swiss National Bank cut by 25 bps to 0%, in…

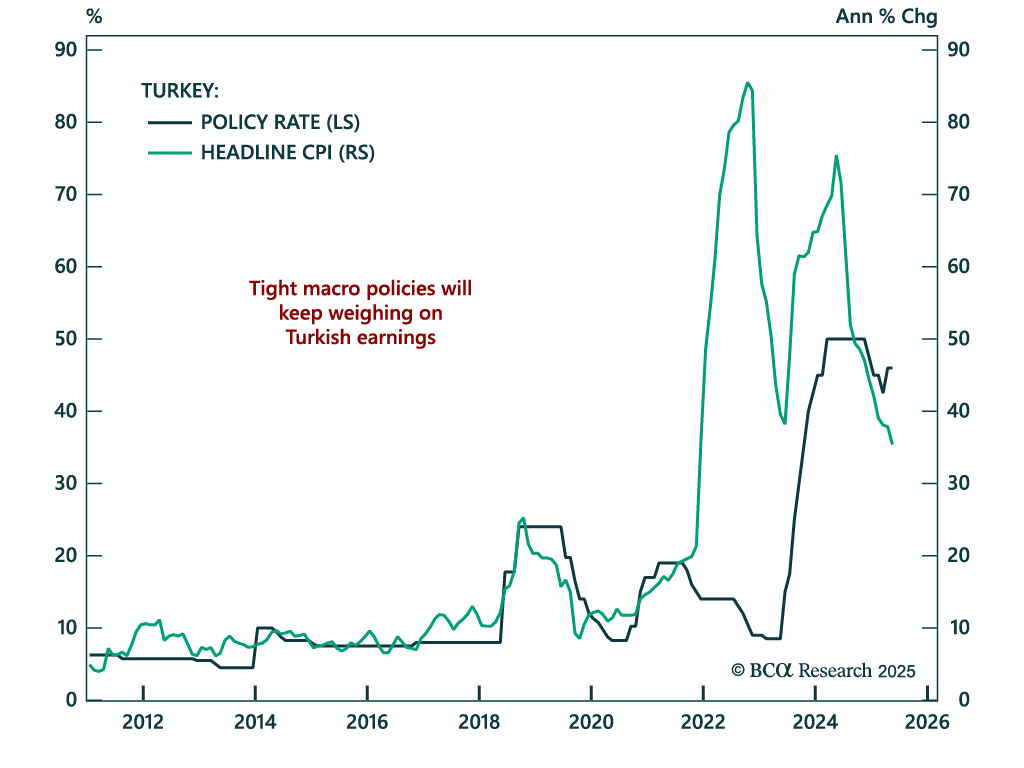

Turkey’s tight policy stance will weigh on growth and earnings, reinforcing our bearish view on Turkish equities. The central bank held rates at 46% and maintained a hawkish bias, consistent with efforts to bring inflation down from 35% to single digits.…

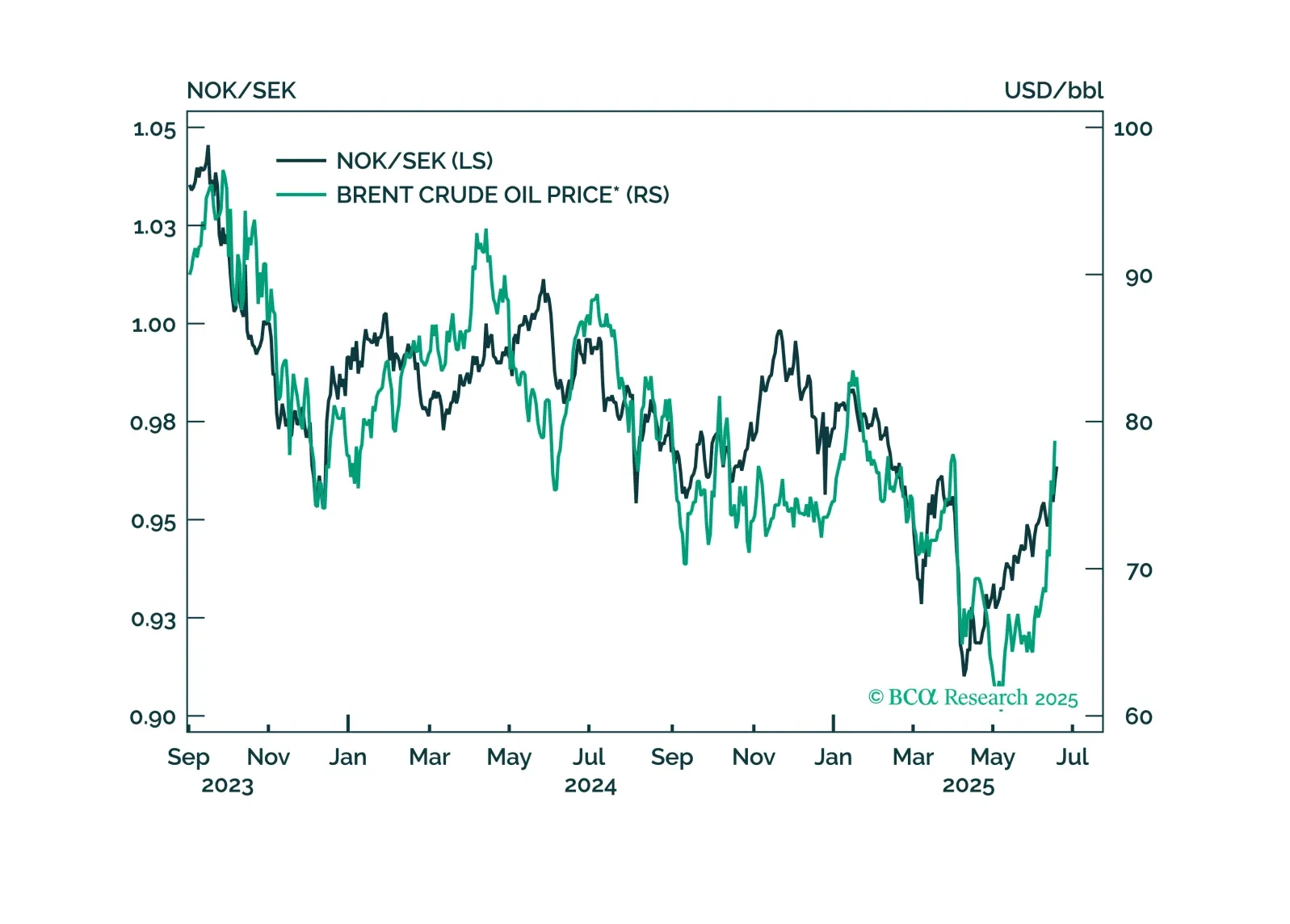

In this Insight, we look at the best trade idea from the recent rate cut by the Riksbank.

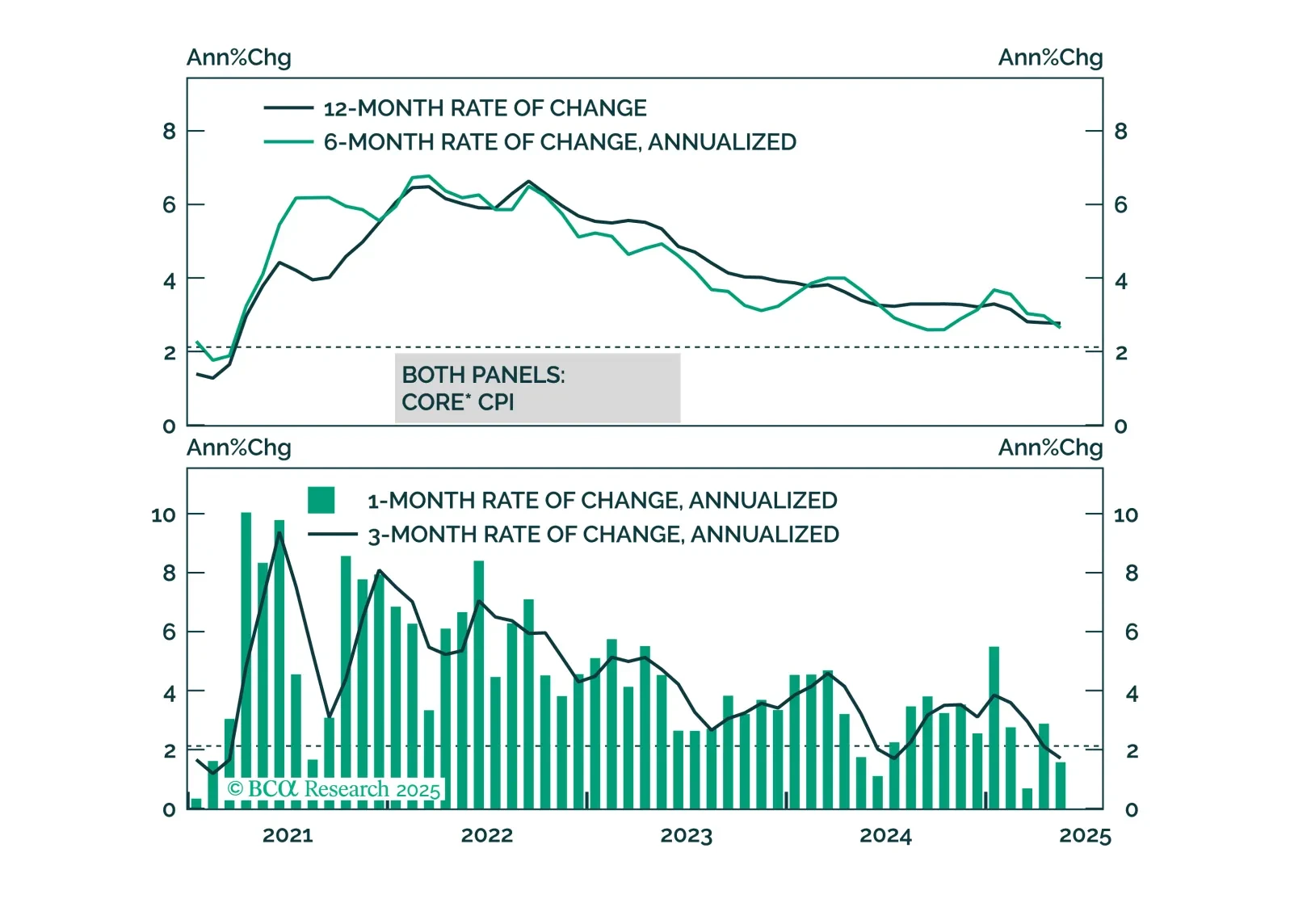

While we anticipate higher inflation in June, it looks increasingly likely that the price impact from tariffs will be less aggressive and long-lasting than many feared.

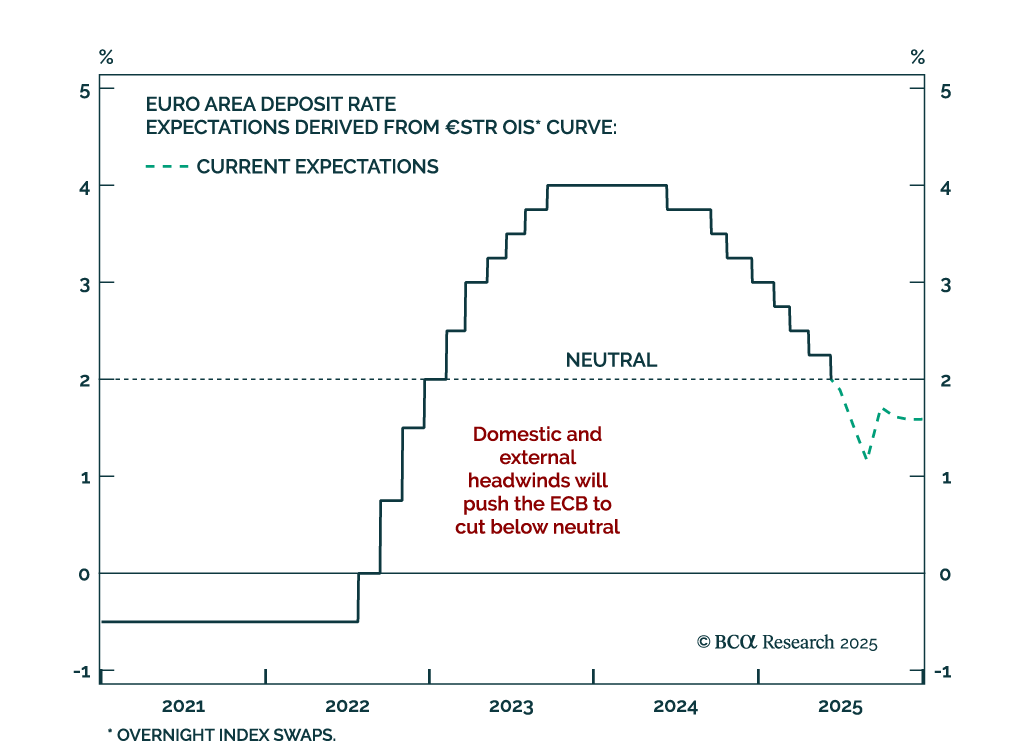

The ECB’s expected rate cut to 2% marks a slower easing phase, capping Bund yields. The shift to a quarterly pace of cuts, barring surprises, confirms a more gradual approach despite ongoing disinflation and weak growth. Staff projections downgraded inflation…

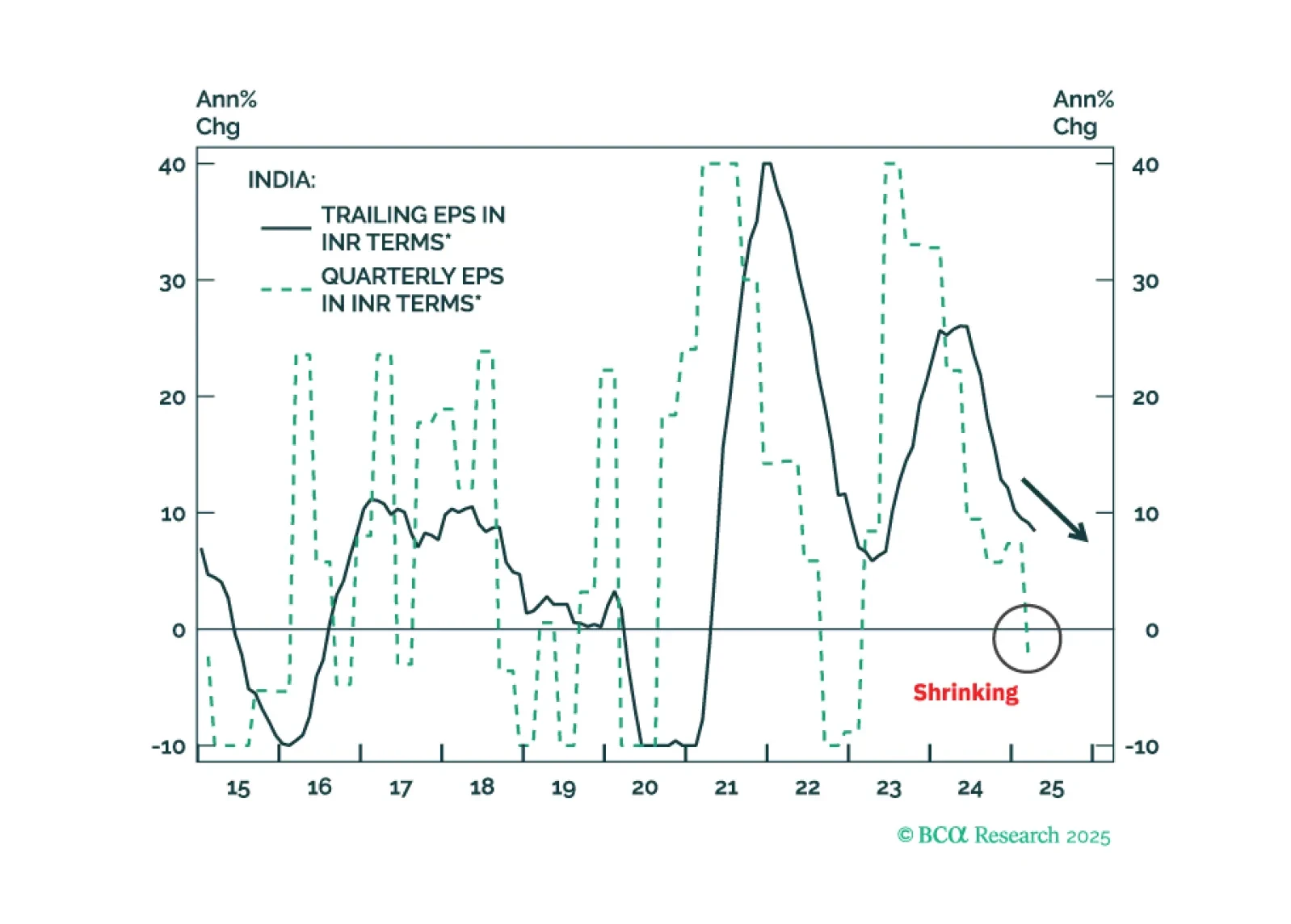

India's IT service exports have been booming and will continue to do so despite wider AI usage. Indian IT stocks, however, will not benefit from it as the expanding Global Capability Centers (GCCs) in India compete with the nation’s IT companies, driving the latter's profitability down.

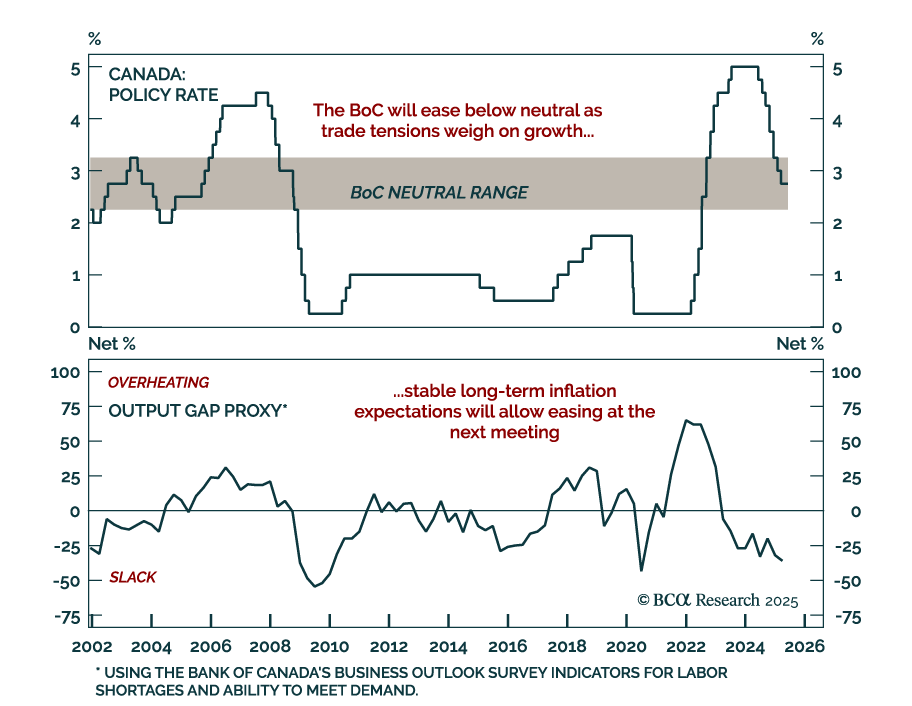

The Bank of Canada held rates at 2.75% but signaled a dovish shift, pushing us to overweight Canadian government bonds and go long CORRA futures. The policy rate remains within the BoC’s neutral range, allowing the Bank to wait for more clarity on trade…