Monetary

Highlights Geopolitical conflicts point to energy price spikes and could add to inflation surprises in the near term. However, US fiscal drag and China’s economic slowdown are both disinflationary risks to be aware of. Specifically, energy-producers like Russia and Iran gain greater leverage amid energy shortages. Europe’s natural gas prices could spike again. Conflict in the Middle East could disrupt oil flows. President Biden’s $1.75 trillion social spending bill is a litmus test for fiscal fatigue in developed markets. It could fail, and even assuming it passes it will not prevent overall fiscal drag in 2022-23. However, it is inflationary over the long run. China’s slowdown poses the chief disinflationary risk. But we still think policy will ease to avoid an economic crash ahead of the fall 2022 national party congress. We are closing this year’s long value / short growth trade for a loss of 3.75%. Cyclical sectors ended up being a better way to play the reopening trade. Feature Equity markets rallied in recent weeks despite sharp upward moves in core inflation across the world (Chart 1). Inflation is fast becoming a popular concern and we see geopolitical risks that could drive headline inflation still higher in the short run. We also see underrated disinflationary factors, namely China’s property sector distress and economic slowdown. Several major developments have occurred in recent weeks that we will cover in this report. Our conclusions: Biden’s domestic agenda will pass but risks are high and macro impact is limited. Congress passed Biden’s infrastructure deal and will probably still pass his signature social spending bill, although inflation is creating pushback. Together these bills have little impact on the budget deficit outlook but they will add to inflationary pressures. Energy shortages embolden Russia and Iran. Winter weather is unpredictable, the energy crisis may not be over. But investors are underrating Russia’s aggressive posture toward the West. Any conflict with Iran could also cause oil disruptions in the near future. US-China relations may improve but not for long. A bilateral summit between Presidents Joe Biden and Xi Jinping will not reduce tensions for very long, if at all. Climate change cooperation is an insufficient basis to reverse the cold war-style confrontation over the long run. Chart 1Inflation Rattles Policymakers

Inflation Rattles Policymakers

Inflation Rattles Policymakers

The investment takeaway is that geopolitical tensions could push energy prices still higher in the short term. Iran and Russia need to be monitored. However, China’s economic slowdown will weigh on growth. China poses an underrated disinflationary risk to our views. US Congress: Bellwether For Fiscal Fatigue While inflation is starting to trouble households and voters, investors should bear in mind that the current set of politicians have long aimed to generate an inflation overshoot. They spent the previous decade in fear of deflation, since it generated anti-establishment or populist parties that threatened to disrupt the political system. They quietly built up an institutional consensus around more robust fiscal policy and monetary-fiscal coordination. Now they are seeing that agenda succeed but are facing the first major hurdle in the form of higher prices. They will not simply cut and run. Inflation is accompanied by rising wages, which today’s leaders want to see – almost all of them have promised households a greater share of the fruits of their labor, in keeping with the new, pro-worker, populist zeitgeist. Real wages are growing at 1.1% in the US and 0.9% across the G7 (Chart 2). Even more than central bankers, political leaders are focused on jobs and employment, i.e. voters. Yet the labor market still has considerable slack (Chart 3). Almost all of the major western governments have been politically recapitalized since the pandemic, either through elections or new coalitions. Almost all of them were elected on promises of robust public investment programs to “build back better,” i.e. create jobs, build infrastructure, revitalize industry, and decarbonize the energy economy. Thus while they are concerned about inflation, they will leave that to central banks, as they will be loathe to abandon their grand investment plans. Chart 2Higher Wages: Real Or Nominal?

Higher Wages: Real Or Nominal?

Higher Wages: Real Or Nominal?

Still, there will be a breaking point at which inflation forces governments to put their spending plans on hold. The US Congress is the immediate test of whether today’s inflation will trigger fiscal fatigue and force a course correction. Chart 3Policymakers Fear Populism, Focus On Employment

Policymakers Fear Populism, Focus On Employment

Policymakers Fear Populism, Focus On Employment

President Biden’s $550 billion infrastructure bill passed Congress last week and will be signed into law around November 15. Now he is worried that his signature $1.75 trillion social spending bill will falter due to inflation fears. He cannot spare a single vote in the Senate (and only three votes in the House of Representatives). Odds that the bill fails are about 35%. Democratic Party leaders will not abandon the cause due to recent inflation prints. They see a once-in-a-generation opportunity to expand the role of government, the social safety net, and the interests of their constituents. If they miss this chance due to inflation that ends up being transitory then they will lose the enthusiastic left wing of the party and suffer a devastating loss in next year’s midterm elections, in which they are already at a disadvantage. Biden’s social bill is also likely to pass because the budget reconciliation process necessary to pass the bill is the same process needed to raise the national debt limit by December 3. A linkage of the two by party leaders would ensure that both pass … and otherwise Democrats risk self-inflicting a national debt default. The reconciliation bill is more about long-term than short-term inflation risk. The bill does not look to have a substantial impact on the budget outlook: the new spending is partially offset by new taxes and spread out over ten years. The various legislative scenarios look virtually the same in our back-of-the-envelope budget projections (Chart 4).

Chart 4

However, given that the output gap is virtually closed, this bill combined with the infrastructure bill will add to inflationary pressures. The fiscal drag will diminish by 2024, not coincidentally the presidential election year 2024, not coincidentally the presidential election year. The deficit is not expected to increase or decrease substantially between 2023 and 2024. From then onward the budget deficit will expand. The increased government demand for goods and services and the increased disposable income for low-earning families will add to inflationary pressures. Other developed markets face a similar situation: inflation is picking up, but big spending has been promised and normalizing budgets will marginally weigh on growth in the next few years (Chart 5). True, growth should hold up since the private economy is rebounding in the wake of the pandemic. But politicians will not be inclined to renege on campaign promises of liberal spending in the face of fiscal drag. The current crop of leaders is primed to make major public investments. This is true of Germany, Japan, Canada, and Italy as well as the United States. It is partly true in France, where fiscal retrenchment has been put on hold given the presidential election in the spring. The effect will be inflationary, especially for the US where populist spending is more extravagant than elsewhere.

Chart 5

The long run will depend on structural factors and how much the new investments improve productivity. Bottom Line: A single vote in the US Senate could derail the president’s social spending bill, so the US is now the bellwether for fiscal fatigue in the developed world. Biden is likely to pass the bill, as global fiscal drag is disinflationary over the next 12 months. Yet inflation could stay elevated for other reasons. And this fiscal drag will dissipate later in the business cycle. Russia And Iran Gain Leverage Amid Energy Crunch The global energy price spike arose from a combination of structural factors – namely the pandemic and stimulus. It has abated in recent weeks but will remain a latent problem through the winter season, especially if La Niña makes temperatures unusually cold as expected. Rising energy prices feed into general producer prices, which are being passed onto consumers (Chart 6). They look to be moderating but the weather is unpredictable. There is another reason that near-term energy prices could spike or stay elevated: geopolitics. Tight global energy supply-demand balances mean that there is little margin of safety if unexpected supply disruptions occur. This gives greater leverage to energy producers, two of which are especially relevant at the moment: Russia and Iran. Russia’s long-running conflict with the West is heating up on several fronts, as expected. Russia may not have caused the European energy crisis but it is exacerbating shortages by restricting flows of natural gas for political reasons, as it is wont to do (Chart 7). Moscow always maintains plausible deniability but it is currently flexing its energy muscles in several areas: Chart 6Energy Price Depends On Winter ... And Russia/Iran!

Energy Price Depends On Winter ... And Russia/Iran!

Energy Price Depends On Winter ... And Russia/Iran!

Ukraine: Russia has avoided filling up and fully utilizing pipelines and storage facilities in Ukraine, where the US is now warning that Russia could stage a large military action in retaliation for Ukrainian drone strikes in the still-simmering Russia-Ukraine war. Belarus: Russia says it will not increase the gas flow through the major Yamal-Europe natural gas pipeline in 2022 even as Belarus threatens to halt the pipeline’s operation entirely. Belarus, backed by Russia, is locked in a conflict with Poland and the EU over Belarus’s funneling of migrants into their territory (Chart 8). The conflict could lead not only to energy supply disruptions but also to a broader closure of trade and a military standoff.1 Russia has flown two Tu-160 nuclear-armed bombers over Belarus and the border area in a sign of support. Moldova: Russia is withholding natural gas to pressure the new, pro-EU Moldovan government.

Chart 7

Chart 8

Russia’s main motive is obvious: it wants Germany and the EU to approve and certify the new Nord Stream II pipeline. Nord Stream II enables Germany and Russia to bypass Ukraine, where pipeline politics raise the risk of shortages and wars. Lame duck German Chancellor Angela Merkel worked with Russia to complete this pipeline before the end of her term, convincing the Biden administration to issue a waiver on congressional sanctions that could have halted its construction. However, two of the parties in the incoming German government, the Greens and the Free Democrats, oppose the pipeline. While these parties may not have been able to stop the pipeline from operating, Russia does not want to take any chances and is trying to force Germany’s and the EU’s hand. The energy crisis makes it more likely that the pipeline will be approved, since the European Commission will have to make its decision during a period when cold weather and shortages will make it politically acceptable to certify the pipeline.2 The decision will further drive a wedge between Germany and eastern EU members, which is what Russia wants. EU natural gas prices will likely subside sometime next year and will probably not derail the economic recovery, according to both our commodity and Europe strategists. A bigger and longer-lasting Russian energy squeeze would emerge if the Nord Stream II pipeline is not certified. This is a low risk at this point but the next six months could bring surprises. More broadly, the West’s conflict with Russia can easily escalate from here. First, President Vladimir Putin faces economic challenges and weak political support. He frequently diverts popular attention by staging aggressive moves abroad. There is no reason to believe his post-2004 strategy of restoring Russia’s sphere of influence in the former Soviet space has changed. High energy prices give him greater leverage even aside from pipeline coercion – so it is not surprising that Russia is moving troops to the Ukraine border again. Growing military support for Belarus, or an expanded conflict in Ukraine, are likely to create a crisis now or later. Second, the US-Germany agreement to allow Nord Stream II explicitly states that Russia must not weaponize natural gas supply. This statement has had zero effect so far. But when the energy shortage subsides, the EU could pursue retaliatory measures along with the United States. Of course, Russia has been able to weather sanctions. But tensions are already escalating significantly. After Russia, Iran also gains leverage during times of tight energy supplies. With global oil inventories drawing down, Iran is in the position to inflict “maximum pressure” on the US and its allies, a role reversal from the 2017-20 period in which large inventories enabled the US to impose crippling sanctions on Iran after pulling out of the 2015 nuclear deal (Chart 9). Iran is rapidly advancing on its nuclear program and a new round of diplomatic negotiations may only serve to buy time before it crosses the “breakout” threshold of uranium enrichment capability as early as this month or next. In a recent special report we argued that there is a 40% chance of a crisis over Iran in the Middle East. Such a crisis could ultimately lead to an oil shock in the Persian Gulf or Strait of Hormuz. Chart 9Now Iran Can Use 'Maximum Pressure'

Now Iran Can Use 'Maximum Pressure'

Now Iran Can Use 'Maximum Pressure'

Bottom Line: Russia’s natural gas coercion of Europe could keep European energy prices high through March or May. More broadly Russia’s renewed tensions with the West confirm our view that oil producers gain geopolitical leverage amid the current supply shortages. Iran also gains leverage and its conflict with the US could lead to global oil supply disruptions anytime over the next 12 months. Until Nord Stream II is certified and a new Iranian nuclear agreement is signed, there are two clear sources of potential energy shocks. Moreover in today’s inflationary context there is limited margin of safety for unexpected supply disruptions regardless of source. Xi’s Historical Rewrite China continues to be a major source of risk for the global economy and financial markets in the lead-up to the twentieth national party congress in fall 2022. While Chinese assets have sold off this year, global risk assets are still vulnerable to negative surprises from China. The five-year political reshuffle in 2022 is more important than usual since President Xi Jinping was originally supposed to step down but will instead stick around as leader for life, like China’s previous strongmen Mao Zedong and Deng Xiaoping.3 Xi’s rejection of term limits became clear in 2017 and is not really news. But Xi will fortify himself and his faction in 2022 against any opposition whatsoever. He is extremely vigilant about any threats that could disrupt this process, whether at home or abroad. The Communist Party’s sixth plenary session this week highlights both Xi’s success within the Communist Party and the sensitivity of the period. Xi produced a new “historical resolution,” or interpretation of the party’s history, which is only the third such resolution. A few remarks on this historical resolution are pertinent: Mao’s resolution: Chairman Mao wrote the first such resolution in 1945 to lay down his version of the party’s history and solidify his personal control. It is naturally a revolutionary leftist document. Deng’s revision of Mao: General Deng Xiaoping then produced a major revision in 1981, shortly after initiating China’s economic opening and reform. Deng’s interpretation aimed to hold Mao accountable for “gross mistakes” during the Cultural Revolution and yet to recognize the Communist Party’s positive achievements in founding the People’s Republic. His version gave credit to the party and collective leadership rather than Mao’s personal rule. Two 30-year periods: The implication was that the party’s history should be divided into two thirty-year periods: the period of foundations and conflict with Mao as the party’s core and the period of improvement and prosperity with Deng as the core. Jiang’s support of Deng: Deng’s telling came under scrutiny from new leftists in the wake of Tiananmen Square incident in 1989. But General Secretary Jiang Zemin largely held to Deng’s version of the story that the days of reform and opening were a far better example of the party’s leadership because they were so much more stable and prosperous.4 Xi’s reaction to Jiang and Deng: Since coming to power in 2012, Xi Jinping has shown an interest in revising the party’s official interpretation of its own history. The central claim of the revisionists is that China could never have achieved its economic success if not for Mao’s strongman rule. Mao’s rule and the Communist Party’s central control thus regain their centrality to modern China’s story. China’s prosperity owes its existence to these primary political conditions. The two periods cannot be separated. Xi’s synthesis of Deng and Mao: Now Xi has written himself into that history above all other figures – indeed the communique from the Sixth Plenum mentions Xi more often than Marx, Mao, or Deng (Chart 10). The implication is that Xi is the synthesis of Mao and Deng, as we argued back in 2017 at the end of the nineteenth national party congress. The synthesis consists of a strongman who nevertheless maintains a vibrant economy for strategic ends.

Chart 10

What are the practical policy implications of this history lesson? Higher Country Risk: China’s revival of personal rule, as opposed to consensus rule, marks a permanent increase in “country risk” and political risk for investors. Autocratic governments lack institutional guardrails (checks and balances) that prevent drastic policy mistakes. When Xi tries to step down there will probably be a succession crisis. Higher Macroeconomic Risk: China is more likely to get stuck in the “middle-income trap.” Liberal or pro-market economic reform is de-emphasized both in the new historical resolution and in the Xi administration’s broader program. Centralization is already suppressing animal spirits, entrepreneurship, and the private sector. Higher Geopolitical Risk: The return to autocracy and the withdrawal from economic liberalism also entail a conflict with the United States, which is still the world’s largest economy and most powerful military. The US is not what it once was but it will put pressure on China’s economy and build alliances aimed at strategic containment. Bottom Line: China is trying to escape the middle-income trap, like Taiwan, Japan, and South Korea, but it is trying to do so by means of autocracy, import substitution, and conflict with the United States. These other Asian economies improved productivity by democratizing, embracing globalization, and maintaining a special relationship with the United States. China’s odds of succeeding are low. China will focus on power consolidation through fall 2022 and this will lead to negative surprises for financial markets. China Slowdown: The Disinflationary Risk While it is very unlikely that Xi will face serious challenges to his rule, strange things can happen at critical junctures. Therefore the regime will be extremely alert for any threats, foreign or domestic, and will ultimately prioritize politics above all other things, which means investors will suffer negative surprises. The lingering pandemic still poses an inflationary risk for the rest of the world while the other main risk is disinflationary: Inflationary Risk – Zero COVID: The “Covid Zero” policy of attempting to stamp out any trace of the virus will still be relevant at least over the next 12 months (Chart 11). Clampdowns serve a dual purpose since the Xi administration wants to minimize foreign interference and domestic dissent before the party congress. Hence the global economy can suffer more negative supply shocks if ports or factories are closed. Inflationary Risk – Energy Closures: The government is rationing electricity amid energy shortages to prioritize household heating and essential services. This could hurt factory output over the winter if the weather is bad. Disinflationary Risk – Property Bust: The country is still flirting with overtightening monetary, fiscal, and regulatory policies. Throughout the year we have argued that authorities would avoid overtightening. But China is still very much in a danger zone in which policy mistakes could be made. Recent rumors suggest the government is trying to “correct the overcorrection” of regulatory policy. The government is reportedly mulling measures to relax the curbs on the property sector. We are inclined to agree but there is no sign yet that markets are responding, judging by corporate defaults and the crunch in financial conditions (Chart 12).

Chart 11

Chart 12China Has Not Contained Property Turmoil

China Has Not Contained Property Turmoil

China Has Not Contained Property Turmoil

Evergrande, the world’s most indebted property developer, is still hobbling along, but its troubles are not over. There are signs of contagion among other developers, including state-owned enterprises, that cannot meet the government’s “three red lines.” 5 Credit growth has now broken beneath the government’s target range of 12%, though money growth has bounced off the lower 8% limit set for this year (Chart 13). China is dangerously close to overtightening. China’s economic slowdown has not yet been fully felt in the global economy based on China’s import volumes, which are tightly linked to the combined credit-and-fiscal-spending impulse (Chart 14). The implication is that recent pullbacks in industrial metal prices and commodity indexes will continue. Chart 13China Tries To Avoid Over-Tightening

China Tries To Avoid Over-Tightening

China Tries To Avoid Over-Tightening

Chart 14China Slowdown Not Yet Fully Felt

China Slowdown Not Yet Fully Felt

China Slowdown Not Yet Fully Felt

Until China eases policy more substantially, it poses a disinflationary risk and a strong point in favor of the transitory view of global inflation. It is difficult for China to ease policy – let alone stimulate – when producer prices are so high (see Chart 6 above). The result is a dangerous quandary in which the government’s regulatory crackdowns are triggering a property bust yet the government is prevented from providing the usual policy support as the going gets tough. Asset prices and broader risk sentiment could go into free fall. However, the party has a powerful incentive to prevent a generalized crisis ahead of the party congress. So we are inclined to accept signs that property curbs and other policies will be eased. Bottom Line: The full disinflationary impact of China’s financial turmoil and economic slowdown has yet to be felt globally. Biden-Xi Summit Not A Game Changer As long as inflation prevents robust monetary and fiscal easing, Beijing is incentivized to improve sentiment in other ways. One way is to back away from the regulatory crackdown in other sectors, such as Big Tech. The other is to improve relations with the United States. A stabilization of US ties would be useful before the party congress since President Xi would prefer not to have the US interfering in China’s internal affairs during such a critical hour. No surprise that China is showing signs of trying to stabilize the relationship. The US is apparently reciprocating. Presidents Biden and Xi also agreed to hold a virtual bilateral summit next week, which could lead to a new series of talks. The US Trade Representative also plans to restart trade negotiations. The plan is to enforce the Phase One trade deal, issue waivers for tariffs that hurt US companies, and pursue new talks over outstanding structural disputes. The Phase One trade deal has fallen far short of its goals in general but on the energy front it is doing well. China will continue importing US commodities amid global shortages (Chart 15).

Chart 15

Chart 15

The summit alone will have a limited impact. Biden had a summit with Putin earlier this year but relations could deteriorate tomorrow over cyber-attacks, Ukraine, or Belarus. However, there is some basis for the US and China to cooperate next year: Iran. Xi is consolidating power at home in 2022 and probably wants to use negotiations to keep the Americans at bay. Biden is pivoting to foreign policy in 2022, since Congress will not get anything done, and will primarily focus on halting Iran’s nuclear program. If China assists the US with Iran, then there is a basis for a reduction in tensions. The problem is not only Iran itself but also that China will not jump to enforce sanctions on Iran amid energy shortages. And China is not about to make sweeping structural economic concessions to the US as the Xi administration doubles down on state-guided industrial policy. Meanwhile the US is pursuing a long-term policy of strategic containment and Biden will not want to be seen as appeasing China ahead of midterm elections, especially given Xi’s reversion to autocracy. What about cooperation on climate change? The US and China also delivered a surprise joint statement at the United Nations climate change conference in Scotland (COP26), confirming the widely held expectation that climate policy is an area of engagement. These powers and Europe have a strategic interest in reducing dependency on Middle Eastern oil (Chart 16). Climate talks will begin in the first half of next year. However, climate cooperation is not significant enough alone to outweigh the deeper conflicts between the US and China. Moreover climate policy itself is somewhat antagonistic, as the EU and US are looking at applying “carbon adjustment fees” to carbon-intensive imports, e.g. iron and steel exports from China and other high-polluting producers (Chart 17). While the EU and US are not on the same page yet, and these carbon tariffs are far from implementation, the emergence of green protectionism does not bode well for US-China relations even aside from their fundamental political and military disputes.

Chart 16

Bottom Line: Some short-term stabilization of US-China relations is possible but not guaranteed. Markets will cheer if it happens but the effect will be fleeting. Chinese assets are still extremely vulnerable to political and geopolitical risks.

Chart 17

Investment Takeaways Gold can still go higher. Financial markets are pricing higher inflation and weak real rates. Gold has been our chief trade to prepare both for higher inflation and geopolitical risk. We are closing our long value / growth equity trade for a loss of 3.75%. We are maintaining our long DM Europe / short EM Europe trade. This trade has performed poorly due to the rally in energy prices and hence Russian equities. But while energy prices may overshoot in the near term, investors will flee Russian equities as geopolitical risks materialize. We are maintaining our long Korea / short Taiwan trade despite its being deeply in the red. This trade is valid over a strategic or long-term time horizon, in which a major geopolitical crisis and/or war is likely. Our expectation that China will ease policy to stabilize the economy ahead of fall 2022 should support Korean equities. Matt Gertken Vice President Geopolitical Strategy mattg@bcaresearch.com Footnotes 1 Over the past year President Alexander Lukashenko’s repression of domestic unrest prompted the EU to impose sanctions. Lukashenko responded by organizing an immigration scheme in which Middle Eastern migrants are flown into Belarus and funneled into the EU via Poland. The EU is threatening to expand sanctions while Belarus is threatening to cut off the Yamal-Europe pipeline amid Europe’s energy crisis. See Pavel Felgenhauer, “Belarus as Latest Front in Acute East-West Standoff,” Jamestown Foundation, November 11, 2021, Jamestown.org. 2 Both Germany and the EU must approve of Nord Stream II for it to enter into operation. The German Federal Network Agency has until January 8, 2022 to certify the project. The Economy Ministry has already given the green light. Then the European Commission has two-to-four months to respond. The EU is supposed to consider whether the pipeline meets the EU’s requirement that gas transport be “unbundled” or separated from gas production and sales. This is a higher hurdle but Germany’s clout will be felt. Hence final approval could come by March 8 or May 8, 2022. The energy crisis will put pressure for an early certification but the EU Commission may take the full time to pretend that it is not being blackmailed. See Joseph Nasr and Christoph Steitz, “Certifying Nord Stream 2 poses no threat to gas supply to EU – Germany,” Reuters, October 26, 2021, reuters.com. 3 Xi is not serving for an “unprecedented third term,” as the mainstream media keeps reporting. China’s top office is not constant nor were term limits ever firmly established. Each leader’s reign should be measured by their effective control rather than technical terms in office. Mao reigned for 27 years (1949-76), Deng for 14 years or more (1978-92), Jiang Zemin for 10 years (1992-2002), and Hu Jintao for 10 years (2002-2012). 4 See Joseph Fewsmith, “Mao’s Shadow” Hoover Institution, China Leadership Monitor 43 (2014), and “The 19th Party Congress: Ringing In Xi Jinping’s New Age,” Hoover Institution, China Leadership Monitor 55 (2018), hoover.org. 5 Liability-to-asset ratios less than 70%, debt-to-equity less than 100%, and cash-to-short-term-debt ratios of more than 1.0x. Strategic View Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months) Open Trades & Positions

Image

Dear client, This week, we are introducing our new “Currency Month-In-Review” report. The new format should dovetail nicely with the historical back sections you have become accustomed to, but with a more holistic approach to interpreting data releases, along with actionable investment advice. We would appreciate any comments, criticisms, and feedback to help us better serve you. Kind regards, The Foreign Exchange Strategy team Highlights The DXY index has broken above our 95-threshold level. As a momentum currency, the prospect for further gains in the near term are high. That said, we are sticking with our longer-term (12-18 month) bearish view. Most of the catalysts propping the dollar in the near-term should reverse. The Fed will continue to lag the inflation curve, and economic growth will rotate from the US to other economies that are getting their populations vaccinated. Both are dollar bearish. Speculative positioning in the dollar is now approaching extremes. This warns against establishing fresh long positions. Amidst the volatility in currency markets, trading opportunities are emerging. This week, we are initiating a limit-buy on EUR/CHF trade at 1.05. Feature The latest CPI report from the US was strong, taking markets much by surprise. In the currency world, the spread between the 3-month Eurodollar and Euribor interest rate shot up, pushing up the dollar (Chart 1). December 2022 Eurodollar futures are now pricing in a much faster pace of rate hikes than they did earlier this year. This helped cement the dollar as king this year (Chart 2). Chart 1The Dollar And Interest Rates

The Dollar And Interest Rates

The Dollar And Interest Rates

Chart 2AThe Strength In The DXY Is Not Fully Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

Chart 2BThe Strength In The DXY Is Not Fully Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

Chart 2CThe Strength In The DXY Is Not Fully Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

Chart 2DThe Strength In The DXY Is Not Fully Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

The Strength In The DXY Is Justified By The Economic Picture

Economic data has also been moving in favor of the US of late. The economic surprise index in the US is at 19, while in the eurozone and Japan, it is at -50 and -73.9, respectively. From a broader perspective, the recovery in the services PMI in the US had been more robust than most other developed economies. That said, there are also signs that US economic momentum is giving way to other countries. The US is likely to be the first country to close its output gap, and commensurately, inflation is surprising to the upside (Chart 3). Wage growth has also inflected higher. This is raising the prospect that inflation might be more of a genuine concern. For many other countries, surging house prices are threatening financial stability. In New Zealand, the central bank now has a mandate to consider house prices when calibrating policy. Chart 3AThe US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

Chart 3BThe US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

Chart 3CThe US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

Chart 3DThe US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

The US Is Generating Genuine Inflation. This Is Depressing Real Rates

The key point is that many central banks have already withdrawn accommodation ahead of the Fed, which puts the recent dollar rally into question. QE has ended in Canada and New Zealand. Norway and New Zealand have hiked interest rates. Forward curves suggest that most central banks should continue to withdraw accommodation. The key question is whether the Fed turns more hawkish that what is already priced in, or disappoints market expectations. We side with the latter. In the meantime, real rates continue to remain deeply negative in the US. With negative real rates and a deteriorating trade balance, the US will need to significantly raise interest rates to attract portfolio investment. For the US, portfolio investment has mostly been in the form of equity purchases rather than bond flows (Chart 4) and Chart 5). But even an increase in the US 10-year yield to 2.25% will keep real interest rates low. In the following sections, we look at the latest economic releases and provide our assessment of the impact going forward on various currencies. Chart 4AThe Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

Chart 4BThe Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

Chart 4CThe Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

The Fed Could Disappoint Market Expectations

Chart 4

Chart 5AThe US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

Chart 5BThe US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

Chart 5CThe US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

Chart 5DThe US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

The US Trade Deficit Needs To Be Financed Externally

US Dollar The last month has seen US economic data outperform that of its peers. Within the G10, the Citigroup economic surprise index is much higher in the US (+19), than say, the euro area (-50) or Japan (-74). This has supported the DXY, which is up almost 1% over the last month. For risk-management purposes, we are turning neutral on the DXY in the near term, even though our longer-term view remains bearish. The two most important releases in the US over the last month were the jobs report and this week’s CPI report. Nonfarm payrolls increased by 531,000 jobs and unemployment fell to 4.6% in October. This is inching closer to NAIRU. Meanwhile, headline CPI came in at 6.2% year-on-year in September while core inflation came in at 4.9%, the highest for several decades. This is occurring within the context of accelerating wage growth (unit labor costs in the nonfarm business sector surged 8.3% in Q3), higher house prices, and an ebullient stock market, reinforcing the wealth effect. That said, strong domestic demand in the US will have to trigger a much more hawkish Fed for the dollar to reach escape velocity. This is because it will push real interest rates lower as it inflates the US current account deficit. The trade deficit grew 11.2% in September, the sharpest monthly increase since July of 2020. Equity portfolio flows, which have been sustaining the trade deficit, are softening of late. Bond portfolio flows will need a much weaker dollar, or higher Treasury yields, to accelerate. Against such a backdrop, the Fed recently announced a “dovish taper” by reducing the monthly pace of its asset purchases by $15 billion, with the tapering expected to be completed by mid-2022. No imminent rate hike was signaled. The market is likely to continue to challenge such a dovish stance, which will put near-term upward pressure on the dollar, until inflation eventually rolls over. From a relative standpoint, the Fed is lagging many other major developed market central banks in normalizing monetary policy. We are sticking to our long-term bearish view on the dollar index, but a more proactive Fed is a risk to this view. We are upgrading our near-term outlook on the dollar to neutral. Chart 6AUS Dollar

US Dollar

US Dollar

Chart 6BUS Dollar

US Dollar

US Dollar

Euro The euro has been breaking down in recent sessions and is the main cause of the surge in the DXY index. The euro is down 0.7% over the last month and is currently at 1.145. The key catalyst for the weakness in the euro is the perception that the ECB will severely lag the Fed in normalizing policy settings. This is occurring within the context of surging inflation in the euro area. Headline CPI came in at 4.1% in October, above expectations of 3.7% and well above September’s 3.4% print. The is dampening real rates in the entire eurozone. On the flip side, there is credence to the ECB’s dovish stance given that unemployment is still above NAIRU and eurozone wage growth remains very tepid. On the economy, the recent improvement in both the Sentix and ZEW expectations bode well for euro area activity. Lower real rates have been the proximate driver of a soft euro in recent trading sessions. That said, real rates could improve if inflation proves transitory. The energy component of the CPI was up 23% year-on-year, by far the biggest contributor to the headline print. Any sign that the ECB is tilting towards a more hawkish direction will initially materialize in the form of reduced asset purchases. This would curtail the significant portfolio outflows from the eurozone this year. From a positioning standpoint, speculative long positions in the euro have also been liquidated, which provides some footing for the currency. We are maintaining a neutral stance on the euro in the very near term, with a bias to buy on weakness. Chart 7AEuro

Euro

Euro

Chart 7BEuro

Euro

Euro

Japanese Yen JPY is the worst-performing currency this year and it is also one of the most shorted. Over the last month, the yen is down 0.4%. Japan is just now emerging from the pandemic, having vaccinated most of its population. Ergo, the economic surprise index, which currently sits at -74, could stage a powerful rebound. While both the inflation print and employment data were in line with expectations (the unemployment rate came in at 2.8% in September), there were other encouraging signs. In October, the Eco Watcher’s Survey rose from 42.1 to 55.5, the manufacturing PMI rose from 51.5 to 53.2, and machine tool orders accelerated 81.5% year-on-year. The Bank of Japan kept monetary policy unchanged at its latest meeting. The policy stance of the BoJ remains dovish, with little prospect of any interest rate increase until 2025. Therefore, in an environment where interest rates rise, that will hurt the yen at the margin. That said, the underperformance of Japanese assets is attracting portfolio inflows, especially from equity investors. As we wrote last week, the underperformance of certain Japanese equity sectors has not been fully justified by the improving earnings picture. From a valuation standpoint, the yen is the cheapest G10 currency according to our PPP models, and it is also quite cheap according to our intermediate-term timing model. Therefore, even given the breakout in the DXY index, we are maintaining our near-term positive for the yen. Chart 8AJapanese Yen

Japanese Yen

Japanese Yen

Chart 8BJapanese Yen

Japanese Yen

Japanese Yen

British Pound As a high-beta currency, sterling has been one of the victims of dollar strength. GBP is down 1.6% over the last month. The biggest driver was the volte-face from the BoE. The BoE kept rates on hold despite their seemingly hawkish messaging weeks ahead of the MPC meeting. Gilt yields fell along with the pound. Following the expiry of the furlough scheme in September, the central bank is waiting to the see the potential impact on the labor market before curtailing accommodation. Hence, a hike in December is still on the table. Incoming data continues to strengthen the case for the BoE to tighten policy. CPI is at 3.5%, with the transport and housing sectors continuing to see surging prices. At 4.5%, the unemployment rate is at NAIRU. Wages are also inflecting higher. The latest GDP report (Q3 GDP rose 6.6% year-on-year) continues to suggest the UK economy maintains upward momentum. The October manufacturing PMI rose from 57.1 to 57.8. Near term, the pound could continue to face weakness as speculators liquidate positions and capital inflows soften. This is especially the case as the post-Brexit environment remains quite volatile. As a play on this trend, we are tactically long EUR/GBP. However, we remain bullish sterling on a cyclical horizon as real rates should continue to normalize. Chart 9ABritish Pound

British Pound

British Pound

Chart 9BBritish Pound

British Pound

British Pound

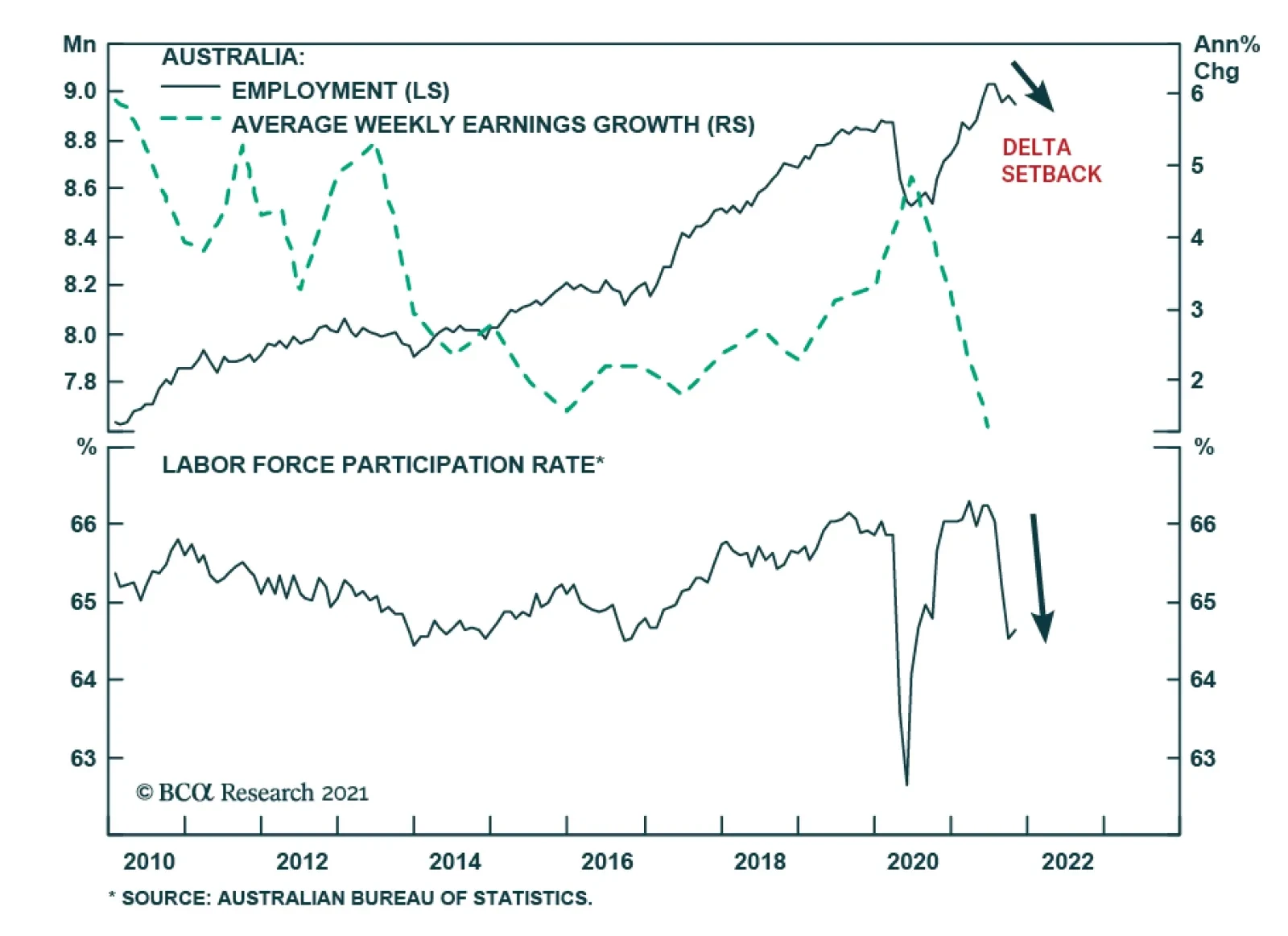

Australian Dollar The Australian dollar is down 0.8% over the last month, as both a stronger dollar and lower iron ore prices exert downward pressure on the exchange rate. The biggest developments over the last few weeks in Australia were the CPI report and the RBA policy meeting. The Q3 print for CPI was 3%, the upper bound of the central bank’s target range, with the trimmed-mean and weighted-median figure coming in at 2.1%. This helped justify the RBA’s decision to abandon the 0.1% yield target on the April 2024 bond. That said, the central bank maintained its cash rate target of 0.1% until earliest 2023 and left the pace of asset purchases unchanged. The RBA trimmed its forecast for GDP for this year to 3% from 4% and said more than 50% of jobs were currently experiencing little to no wage growth. Wages grew just 1.7% in the year to June, far below the 3%-plus levels the RBA believes is necessary to keep inflation sustainably within the 2%-3% band and trigger a rate hike. Hence, the release of the Q3 wage price index, on November 17, will be closely watched. Any upward surprise can challenge the RBA’s measured projections. The bearish case for the Aussie is well known, with speculative positioning near a record short. That said, real yields in Australia have been improving and portfolio flows are accelerating, especially into the mining and energy sectors, which are benefiting from a terms-of-trade tailwind. This sets the stage for a coil-spring rebound in the Aussie. Meanwhile, the AUD is cheap, especially on a terms-of-trade basis. At the crosses, we are long AUD/NZD as a play on these trends. From a tactical standpoint, we are neutral the Aussie, but will buy outright at 70 cents. Chart 10AAustralian Dollar

Australian Dollar

Australian Dollar

Chart 10BAustralian Dollar

Australia Dollar

Australia Dollar

New Zealand Dollar The New Zealand dollar is up 1.3% over the last month. New Zealand’s economy is firing on all cylinders. CPI accelerated sharply from 3.3% to 4.9% in Q3, well above the RBNZ’s target band of 1%-3%, and behind only that of the US. The unemployment rate fell to 3.4% in Q3, far lower than the 3.9% forecasted by economists polled by Reuters. Wage growth was strong in the quarter with the private sector labor cost index registering a 0.7% lift. The seasonally adjusted employment number jumped 2.0% on the quarter, beating expectations of a 0.4% increase. The participation rate also rose to 71.2%, higher than the 70.6% forecast. Meanwhile, house prices continue to move higher, especially in Wellington. As a result, the RBNZ has been one of the most hawkish G10 central banks, hiking rates last month for the first time in seven years to 0.5%. Another 0.25% hike is likely at the November 24 meeting. Meanwhile, at 2.6%, New Zealand currently has the highest G10 10-year bond yield. This is bullish for the kiwi. The one caveat is that the Covid-19 situation in New Zealand continues to deteriorate, which could be a catalyst for a pause. Portfolio flows into New Zealand have turned negative in recent quarters. The equity market, which is quite expensive, has underperformed and the currency is overvalued according to our models, which has dampened the appeal of higher yields. We continue to believe the NZD will fare well cyclically, but hawkish expectations from the RBNZ are already priced in. This provides room for disappointment. Chart 11ANew Zealand Dollar

New Zealand Dollar

New Zealand Dollar

Chart 11BNew Zealand Dollar

New Zealand Dollar

New Zealand Dollar

Canadian Dollar The CAD is the best-performing currency this year, even though it is down 1% over the last month. The key driver of the CAD in recent weeks remains the outlook for monetary policy, and the path of energy prices. CPI inflation came in at 4.4% year-on-year for September, beating market expectations and among the highest across the G10. The CPI-trim hit 3.4% year-on-year. With all eight major components of the CPI rising year-over-year, upward price pressures are broad-based. The housing market also appears bubbly, all providing fertile ground for tighter monetary settings. At first blush, the October employment report was disappointing, with only 31,000 jobs added. However, employment in Canada is already above pre-pandemic levels and is likely to now settle towards trend growth of around 2%. This suggests a print of 30,000 - 40,000 jobs, in line with October’s release. The unemployment rate continues to drop, hitting 6.7%. Incoming data justified the Bank of Canada’s policy response. It delivered a hawkish surprise announcing an end to its quantitative easing program and shifting to the reinvestment phase whereby its holdings of Canadian government bonds will be held constant. It also brought forward the first rate hike to Q2 2022. The BoC will marginally diverge from the US Fed, which is expected to keep rates unchanged through most of next year. This will continue to boost real rates in Canada. Meanwhile, net purchases of Canadian securities continue to inflect higher, as the commodity sector benefits from a terms-of-trade boom. That said, from a tactical standpoint, speculators are marginally long the CAD. As such, our near-term view is cautious. We however doubt the CAD will significantly break below 78 cents, given burgeoning tailwinds. Chart 12ACanadian Dollar

Canadian Dollar

Canadian Dollar

Chart 12BCanadian Dollar

Canadian Dollar

Canadian Dollar

Swiss Franc The Swiss franc is up 1% against the dollar over the last month. EUR/CHF has also been very weak in recent trading sessions, constantly testing the 1.054 level. In our view, this has been much more due to euro weakness (see euro section above) than franc strength. The Swiss franc is trading near 11-month highs versus the euro. On the economic front, the labor market is improving and inflation in Switzerland is picking up. House prices have also risen quite robustly. This is lessening the need for the central back to maintain ultra-accommodative settings. That said, the Swiss National Bank is likely to lag the rest of the G10 in lifting rates from -0.75%, currently the lowest benchmark interest rate in the world. This suggests that market pricing of a 25 basis-point rate rise by the SNB by the end of 2022 is misplaced. Inflation would have to rise substantially more - above the SNB's target range of less than 2% - before any hike is possible. The SNB has also said it remained ready to intervene to weaken a highly valued Swiss franc. The ECB’s dovish stance is one reason why the SNB will be loath to let the currency appreciate. Our guess is that the 1.05 level provides a near-term line in the sand, which will prompt the SNB to intervene. We would be buyers of EUR/CHF below 1.05. Chart 13ASwiss Franc

Swiss Franc

Swiss Franc

Chart 13BSwiss Franc

Swiss Franc

Swiss Franc

Norwegian Krone The Norwegian krone has violently sold off in recent weeks, prompting our long Scandinavian basket to be stopped out. This has been mostly due to low liquidity and the high-beta nature of the krone. Norway’s central bank kept interest rates on hold at its latest meeting but reiterated it will likely hike its key rate by 25 basis points to 0.5% in December. The central bank noted that the economic recovery pushed activity back to pre-pandemic levels, while unemployment receded further. That said, underlying inflation still runs below the bank’s target. The recent surge in oil prices has provided strong support for Norway’s trade balance and terms of trade. Oil and gas make up around 18% of Norway’s GDP. This is encouraging portfolio flows and has provided underlying support for the NOK. That said, given that much of the Norges Bank’s hawkishness has likely been priced into the NOK, the rewards of going long the currency should start shifting to its carry. Chart 14ANorwegian Krone

Norwegian Krone

Norwegian Krone

Chart 14BNorwegian Krone

Norwegian Krone

Norwegian Krone

Swedish Krona The SEK was up 0.9% over the last month. Sweden never closed its economy, yet Covid-19 still had an impact. The good news is that this is mostly behind them. GDP expanded by 1.8% on the quarter in Q3, beating forecasts and the country recently ended all pandemic curbs. The labor market is recovering, and inflation is rising. CPIF inflation, on which the Riksbank sets its 2% target, is at 2.8%. Surging energy prices should turn out to be less of a problem for Sweden than the more coal-dependent countries in Europe, suggesting any increase in prices will be more genuine. The Riksbank will complete its planned balance-sheet expansion later this year and has committed to maintaining the size of its bond holdings through 2022. The central bank, one of the most dovish amongst the G10, is slated to keep its policy rate flat at least until 2024. This could change if inflationary pressures remain persistent. The big risk for Sweden is a slowdown in Europe and China. Supply chain bottlenecks are another issue. Several Swedish car and truck makers were forced to halt production in August due to semiconductor shortages. With the recent surge in the dollar, we were stopped out of our short EUR/SEK and USD/SEK positions for a profit. We will be looking to reinstate these trades from higher levels. Chart 15ASwedish Krona

Swedish Krona

Swedish Krona

Chart 15BSwedish Krona

Swedish Krona

Swedish Krona

Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Kate Sun Research Analyst kate.sun@bcaresearch.com Trades & Forecasts Strategic View Cyclical Holdings (6-18 months) Tactical Holdings (0-6 months) Limit Orders Forecast Summary

Rising inflationary pressures are seeping into Aussie inflation expectations which according to the Melbourne Institute reached 4.6% in November. Nevertheless, the RBA pushed back against market rate hike expectations at last week’s meeting. Instead, it…

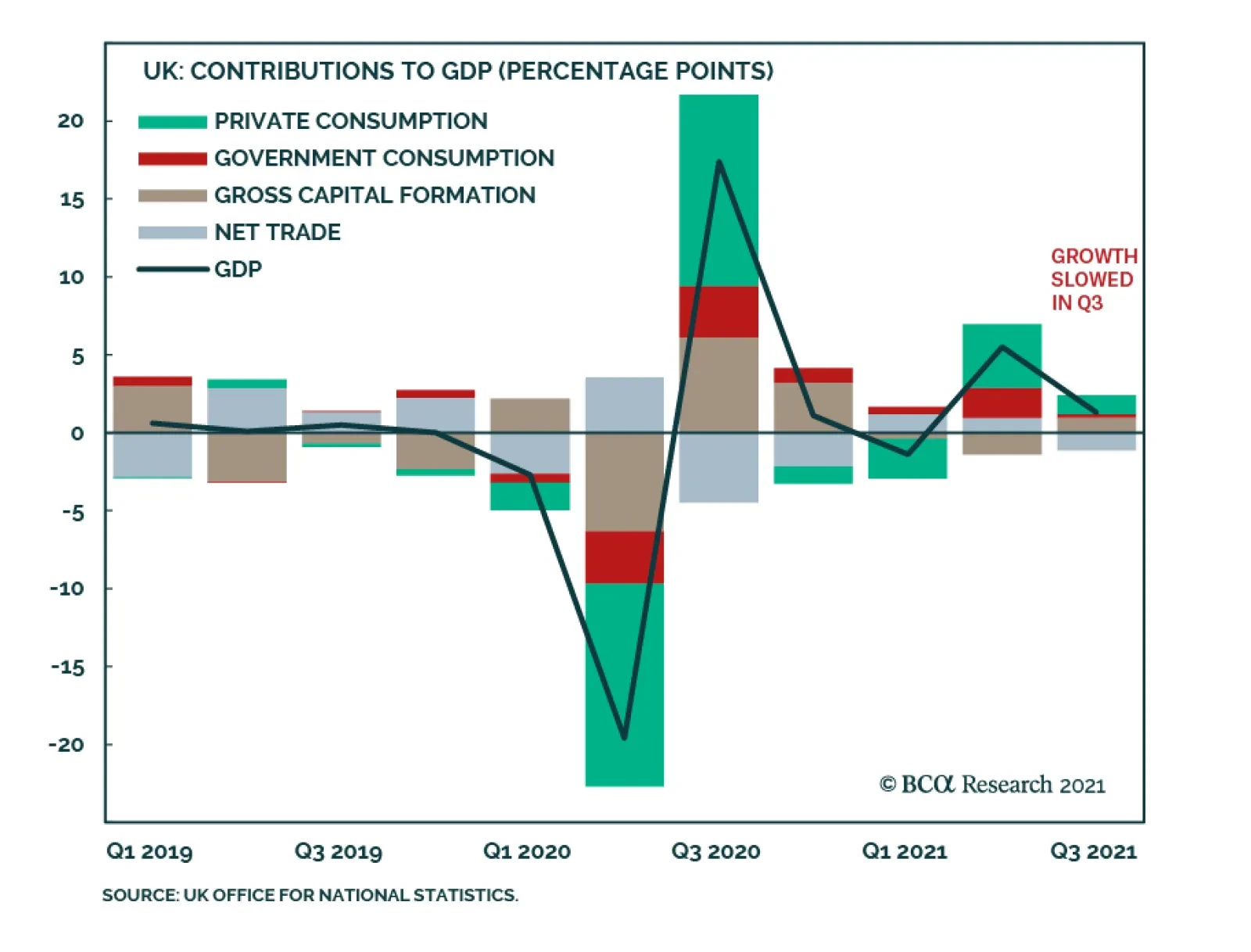

The UK economy decelerated in Q3 with the GDP print falling below expectations. Economic growth slowed from 5.5% to 1.3% q/q versus an anticipated 1.5% rate. Similarly, year-over-year growth moderated to 6.6% from 23.6%. However, the month-on-month momentum…

Highlights Fed/BoE: Both the Fed and the Bank of England found ways to talk down 2022 rate hike expectations discounted in US and UK bond markets. This is only a temporary reprieve, however, as the near-term uncertainties over the persistence of cost-push inflation will eventually be overwhelmed by medium-term certainties of demand-pull inflation confirmed by tightening labor markets. Stay underweight US Treasuries and UK Gilts in global bond portfolios. US Treasury Curve: Longer-term US Treasury yields are priced too low relative to the likely peak in the fed funds rate in the next cycle. Position for a steeper US Treasury curve until Fed rate hikes are imminent, which will likely not be until Q4/2022. Feature Chart of the WeekShifting Rate Expectations Driving Bond Yields As QE Fades

Shifting Rate Expectations Driving Bond Yields As QE Fades

Shifting Rate Expectations Driving Bond Yields As QE Fades

Bond market uncertainty about future monetary policy moves is on the rise. Bond volatility has picked up, most notably at the front end of yield curves that are most sensitive to rate hike expectations which have been intensifying. Yet last week, the Federal Reserve and Bank of England (BoE) were able to talk bond investors off the ledge – at least, temporarily - by pushing back against expectations of multiple rate hikes in the US and UK in 2022. Central bankers in those countries are stuck in a difficult spot. Inflation is high enough to warrant some tightening of monetary policy. Yet there are lingering concerns over how long the current upturn in global inflation will last. Meanwhile, there are just enough questions on the underlying pace of economic momentum to require policymakers to see more data, especially in labor markets, before feeling comfortable enough to pull the trigger on actual rate hikes. We now see that happening first in the UK early next year, and in the US in late 2022. One thing that is certain is that the ups and downs of interest rate expectations – and the central bank forward guidance that influences them – will increasingly become the more dominant driver of bond yields and yield curve shape as global pandemic bond-buying programs get wound down (Chart of the Week). On that front, we see more potential for bond-bearish steepening in the UK and US over the next several months. The BoE: Another Bad Date With The Unreliable Boyfriend The UK financial press infamously dubbed the BoE “the unreliable boyfriend”, under the leadership of former Governor Mark Carney, for hinting at interest rate increases that never materialized. At last week’s Monetary Policy Committee (MPC) meeting, rates were kept unchanged in a 7-2 vote despite some intense signaling in recent weeks that a rate hike was imminent. Under current BoE Governor Andrew Bailey, this edition of the MPC is more like an indecisive spouse than unreliable boyfriend. On the one hand, there is a clear overshoot of UK inflation (and inflation expectations) that would justify a rate hike as soon as possible (Chart 2). The BoE’s new economic forecasts presented in the November Monetary Policy Report (MPR) called for headline CPI inflation to reach a peak of 5% in April 2022 – significantly higher than the 4% late-2021 forecast from the August MPR. On the other hand, high current inflation is already having a dampening effect on economic sentiment. The GfK index of UK consumer confidence is down -10% from the peak seen in July, despite diminishing concerns over COVID seen in public opinion polls (Chart 3, middle panel). A similar divergence is evident in the BoE’s Decision Maker Panel survey of UK Chief Financial Officers, which showed that uncertainty over future sales was somewhat elevated compared to diminished concerns about COVID and Brexit (bottom panel). Chart 2Fed/BoE Cannot Stay Dovish For Much Longer

Fed/BoE Cannot Stay Dovish For Much Longer

Fed/BoE Cannot Stay Dovish For Much Longer

Chart 3High UK Inflation Raises Growth Uncertainty

High UK Inflation Raises Growth Uncertainty

High UK Inflation Raises Growth Uncertainty

The BoE highlighted these divergences in economic sentiment series in the November MPR as examples of how high inflation, fueled by global supply chain disruptions and soaring energy prices, introduced uncertainty into the central bank’s forecasts. Even more uncertainty exists in the BoE’s ability to assess the amount of spare capacity, and underlying inflationary pressure, in the UK economy. The BoE dedicated a 9-page section of the November MPR to a discussion about estimating the growth of the supply-side of the UK economy, evidence of how difficult that process has become during the COVID era. The BoE concluded that the pandemic would end up reducing the level of UK potential supply by -2% from pre-COVID levels, even though the growth rate would return to a pre-pandemic pace of around 1.5% by 2023-24. This is a combination that makes setting monetary policy tricky. Reduced supply indicates that the UK economy has a smaller output gap with more inflationary pressure that would require higher interest rates. Yet sluggish growth in potential supply implies that the UK equilibrium interest rate is likely still very low, thus the BoE would not have to raise rates much to get policy back to neutral. This uncertainty over the size of the output gap in the UK economy will force to BoE to focus more on the labor market as the best “real-time” measure of spare capacity. On that front, the evidence is also difficult to interpret. The UK unemployment rate fell to 4.5% over the three months to August, the last available data before the UK government’s COVID furlough schemes, which protected worker incomes hit by COVID job losses, ended on September 30. The UK Office of National Statistics estimates that there were between 900,000 and 1.4 million UK workers furloughed in late September, representing a significant source of labor supply to be absorbed when the government income assistance ends. Thus, the BoE would need to see at least a month or two of post-furlough employment reports – not just job growth, but labor force participation - to assess how quickly those workers were being reabsorbed into the UK labor market. By the BoE’s own estimates, the impact of the furlough schemes, combined with the compositional issues arising from pandemic job losses being borne more by lower-wage workers, boosted UK wage growth by 2.2% (Chart 4, bottom panel). “Underlying” wage growth, net of those effects, is 0.6%, above the pre-COVID peak, suggesting a tightening labor market before the return of furloughed workers to the labor force. In the end, we see the BoE’s November non-hike as nothing more than a delay of the inevitable. While a December hike is possible, this would represent a “double tightening” of monetary policy with the current BoE quantitative easing program set to expire at year-end. The more likely date for a rate hike is now February. This would give the MPC a few months of post-furlough labor data to assess the amount of spare capacity in UK labor markets. We expect the data to show enough underlying health in labor demand relative to supply for the BoE to conclude that accelerating wage growth represents a more sustainable form of UK inflation in 2022 than energy prices or supply-chain disruptions were in 2021, justifying a move to begin hiking rates. We continue to recommend positioning for a steeper UK Gilt curve, focused on longer-maturities where yields were too low relative to even a moderate future BoE rate hike cycle (Chart 5). We entered a new tactical butterfly spread trade last week, going long the 10-year Gilt bullet versus a duration-neutral 7-year/30-year barbell – we continue to like that trade as a way to play for eventual BoE rate hikes in the first half of 2022. Chart 4BoE Needs More Employment Data To Confirm Wage Uptrend

BoE Needs More Employment Data To Confirm Wage Uptrend

BoE Needs More Employment Data To Confirm Wage Uptrend

Chart 5Stay In UK Long-End Gilt Curve Steepeners

Stay In UK Long-End Gilt Curve Steepeners

Stay In UK Long-End Gilt Curve Steepeners

Bottom Line: The Bank of England is still on a path to begin rate hikes, either in December or, more likely, February of next year. Stay underweight UK Gilts. Position For A Steeper US Treasury Curve The Fed announced last week that tapering would begin right away in November, in a move that has been hinted at since the summer. The monthly pace of purchases of Treasuries and Agency MBS will decline by $10 billion and $5 billion, respectively in November and also December. The Fed declined to commit to any specific tapering amounts beyond that, although it seems likely that the same monthly pace of reduction will continue in 2022. This would take the buying of Treasuries and MBS, net of maturing debt, to zero by June of next year, clearing the first necessary hurdle before the FOMC could contemplate a hike in the funds rate. A completion of the taper by June has been hinted at in the speeches of several Fed officials in recent weeks. This is a bit faster than the expected pace of tapering seen in the most recent New York Fed Primary Dealer and Market Participant Surveys from September (Chart 6), but should not be categorized as a hawkish surprise. There were also few bond-bearish signals on future policy moves hinted at by Fed Chair Jay Powell in post post-FOMC meeting press conference.

Chart 6

Chart 7Upside Risk To UST Yields From A Tightening Labor Market

Upside Risk To UST Yields From A Tightening Labor Market

Upside Risk To UST Yields From A Tightening Labor Market

Powell did note that it was still not clear how long the current supply chain/commodity price driven surge in inflation would persist into next year. The expectation, however, was that these forces would eventually subside and allow US inflation to return back to levels much closer to the Fed’s 2% target. Given the uncertainties in the timing of that peak and decline in US inflation, the Fed has limited ability to calibrate any post-taper rate hikes by focusing solely on inflation - especially with longer-term inflation expectations still at levels consistent with the Fed’s target. The Fed will continue to look at US labor market developments to determine the timing and pace of future rate hikes. The last set of FOMC economic projections compiled for the September meeting have the US unemployment rate falling to 3.8% next year, below the median FOMC estimate of full employment at 4%, with one 25bp rate hike penciled in for 2022. We can use that as a baseline assumption on what the Fed considers to be the level of “maximum employment” that would need to be reached before rate hikes could begin. The US unemployment rate fell to 4.6% in October, thus there is still some more to go before hitting that 3.8% rate hike threshold. Yet among the FOMC members, the estimates of full employment range from 3.5%-4.5%, so the October print did knock on the door of that range (Chart 7, middle panel). With US wage growth already showing signs of breaking out – the Atlanta Fed Wage Tracker hit a 14-year high of 14% in September (bottom panel), while the Employment Cost Index rose by a record quarterly pace of 1.3% in Q3 – the Fed will likely be under a lot of pressure to begin hiking rates soon after the taper is expected to end next June. Chart 8UST Curve Forwards Too Flat Vs. Likely Fed Rate Hikes

UST Curve Forwards Too Flat Vs. Likely Fed Rate Hikes

UST Curve Forwards Too Flat Vs. Likely Fed Rate Hikes

We still see December 2022 as the most likely liftoff date, although a faster decline in unemployment could move that timetable forward. The bigger issue for the US Treasury market, however, is not the timing of liftoff but how fast the pace of hikes will be afterward. On that note, future rate expectations are still far too low. For example, according to the New York Fed’s Primary Dealer Survey, the fed funds rate is expected to average only 1.7% over the next ten years (top panel), a level that has proved to be a ceiling for the 10-year Treasury yield so far in 2021. Our colleagues at BCA Research US Bond Strategy recently made the case for expecting the US Treasury curve to bearishly steepen in the coming months. In their view, longer-maturity Treasury yield forward rates were too low compared to a fair value determined by the likely path for the funds rate that assumes rate hikes start in December of next year and rise by 100bps per year to a terminal rate of 2.08% (Chart 8). Interestingly, 2-year Treasury forward rates were in line with the projections of our US Bond Strategy team’s fair value framework. We fully agree with our US Bond colleagues on the likelihood of future Treasury curve steepening. This fits with our views on many developed market countries, not just the US, where longer-maturity bond yields were pricing in too few future rate hikes relative to what was likely to occur over the next few years. Even when taking a much longer perspective, the US Treasury curve looks too flat right now. Going back to the mid-1980s, the current 2-year/10-year US Treasury curve slope of just over 100bps has never been reached (in a flattening move) in the absence of actual Fed rate hikes (Chart 9). Chart 9UST Curve Has Never Been This Flat Without Some Actual Fed Rate Hikes

UST Curve Has Never Been This Flat Without Some Actual Fed Rate Hikes

UST Curve Has Never Been This Flat Without Some Actual Fed Rate Hikes

This week, we are adding a new trade to our Tactical Overlay table to benefit from this expected move in the US yield curve, a US Treasury 2-year/10-year curve steepener (combined with a position in cash, or US 3-month treasury bills, to make the entire trade duration-neutral). We are also taking profits on our previous Tactical US curve flattening trade, which has returned 0.84% since initiation back in June. The exact securities and weightings for our new trade can be found in the Tactical Overlay Trades table below. Bottom Line: Longer-term US Treasury yields are priced too low relative to the likely peak in the fed funds rate in the next cycle. Position for a steeper US Treasury curve until Fed rate hikes are imminent, which will likely not be until Q4/2022. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Recommendations Duration Regional Allocation Spread Product Tactical Overlay Trades GFIS Model Bond Portfolio Recommended Positioning Active Duration Contribution: GFIS Recommended Portfolio Vs. Custom Performance Benchmark

Image

The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Highlights Fed: Chair Powell’s remarks after the November FOMC meeting suggest that the Fed will not panic and move quickly toward tightening in the face of high inflation. Rather, the Fed will stay the course and will only lift rates once its “maximum employment” liftoff trigger is met. We continue to expect Fed liftoff in December 2022. Nominal Treasuries: We project that Treasury securities will still deliver negative total returns, even if Fed liftoff is delayed until December 2022. Investors can protect returns by favoring the 2-year note (long 2yr over cash/10yr barbell) and 20-year bond (long 20yr over 10yr/30yr barbell). TIPS: Investors should short 2-year TIPS outright in anticipation of falling short-dated inflation expectations during the next 12 months. The Taper Is Done, Now Onto Liftoff The Fed announced a tapering of its asset purchases last week and the details of the tapering plan were consistent with what had already been signaled to the public. The Fed will purchase $70 billion of Treasuries this month (compared to $80 billion in October) and $35 billion of agency MBS (down from $40 billion in October). It will then reduce monthly Treasury and MBS purchases by $10 billion and $5 billion each month, respectively, until it reaches net zero asset purchases by June of next year (Chart 2). The Fed didn’t give specific guidance on what will happen with the balance sheet after June, but it’s highly likely that it will follow the pattern of the last tightening cycle and keep the balance sheet flat for a long time, until the fed funds rate is well above the zero bound. The Fed also gave itself the option to increase or decrease the pace of purchases if such changes are warranted by the economic outlook, but it would take a major shock to knock the Fed off its pre-set course. Chart 1The Market's Liftoff Expectations

The Market's Liftoff Expectations

The Market's Liftoff Expectations

Chart 2Net Purchases Will Reach Zero By June

Net Purchases Will Reach Zero By June

Net Purchases Will Reach Zero By June

With the tapering announcement out of the way, the Fed can now turn to the more important question of when to start lifting interest rates. Jay Powell made it clear at last week’s press conference that the committee hasn’t yet formally taken up the issue, but that didn’t stop reporters from pressing the Chairman to provide more details about when the Fed will hike. None of that should be too surprising. There’s intense market interest and a great deal of uncertainty about the timing of Fed liftoff. Two months ago, markets were pricing-in no rate hikes at all in 2022. Now, markets are looking for Fed liftoff at the September 2022 FOMC meeting and are discounting a 90% chance of 2 rate hikes by the end of next year (Chart 1). The Fed’s Thinking On Liftoff So, what did we learn from last week’s FOMC Statement and press conference about how the Fed is thinking about the liftoff date? First, we know from previous comments that the Fed would prefer to reduce net asset purchases to zero before it starts lifting rates. This means that the July 2022 FOMC meeting is the first “live meeting” where a rate hike could possibly occur, and the fed funds futures market is already pricing-in a 74% chance that liftoff will occur at that meeting (Chart 1). We aren’t so sure. In fact, we don’t see the Fed lifting rates until December 2022, and Chair Powell’s comments about inflation at last week’s press conference only increased our confidence in that view. On inflation, Powell echoed comments by Fed Governor Randal Quarles that we flagged in a recent report.1 Both Powell and Quarles put less emphasis on the length of time that inflation remains above the Fed’s target and more emphasis on the causes of that inflation and whether it’s appropriate for the Fed to lean against it. Here’s Powell from last week (emphasis added): Supply constraints have been larger and longer lasting than anticipated. Nonetheless, it remains the case that the drivers of higher inflation have been predominantly connected to dislocations caused by the pandemic, specifically the effects on supply and demand from the shutdown, the uneven reopening, and the ongoing effects of the virus itself. Our tools cannot ease supply constraints. Like most forecasters, we continue to believe that our dynamic economy will adjust to the supply and demand imbalances, and that as it does, inflation will decline to levels much closer to our 2 percent longer-run goal. Of course, it is very difficult to predict the persistence of supply constraints or their effects on inflation. Global supply chains are complex; they will return to normal function, but the timing of that is highly uncertain.2 Essentially, Powell is pointing out that it would be a mistake for the Fed to tighten policy to bring down inflation only to find out that the economy’s natural supply side response was about to do so anyways. The Fed would have dragged down aggregate demand for no reason. So what would cause the Fed to lift rates? We see two potential triggers. The first liftoff trigger would be an assessment by the FOMC that the labor market has reached “maximum employment”. This is the liftoff condition that the Fed has officially set for itself. The second liftoff trigger would be an uncomfortable increase in long-dated inflation expectations. A spike in long-dated inflation expectations would be worrying enough that the Fed would abandon its “maximum employment” goal and tighten earlier. The “Maximum Employment” Trigger Chart 3How Far From "Maximum Employment"?

How Far From "Maximum Employment"?

How Far From "Maximum Employment"?

The concept of “maximum employment” brings a whole host of other issues along with it. How will the Fed know if the labor market is at “maximum employment”? We’ve discussed this topic at length ourselves and have come to a few helpful conclusions.3 First, we can infer from the most recent Summary of Economic Projections that the Fed views an unemployment rate of 3.8% as roughly consistent with “maximum employment”. It is therefore highly unlikely that the Fed will even consider declaring victory on its employment goal until the unemployment rate is in the vicinity of 3.8%, down from its current 4.6% (Chart 3). Second, there are good reasons to believe that the aging of the US population and the recent sharp increase in retirements will prevent the labor force participation rate from re-gaining its pre-pandemic level. However, FOMC participants seem to agree that the prime-age (25-54) labor force participation rate should be close to its February 2020 level for the “maximum employment” condition to be satisfied (Chart 3, bottom panel). Chair Powell even specifically referenced the prime-age participation rate at last week’s press conference.

Chart 4

We think a declaration of “maximum employment” will only occur once the unemployment rate is near 3.8% and the prime-age (25-54) labor force participation rate is near its February 2020 level of 82.9%, up from its current 81.7%. It’s unlikely that these conditions will be met in time for a July 2022 rate hike. The Appendix to this report updates our scenarios for the average monthly nonfarm payroll growth that is required to reach different combinations of the unemployment and participation rates by specific future dates. Our scenarios use the overall participation rate (not the prime-age one), but we think the scenarios derived from the New York Fed’s Surveys of Market Participants and Primary Dealers come close to capturing reasonable conditions for “maximum employment”. Based on those scenarios, we calculate that average monthly nonfarm payroll growth of 602k to 733k is required to reach “maximum employment” by June 2022. Conversely, average monthly payroll growth of only 379k to 455k is required to reach “maximum employment” by December 2022. We see the latter as easily achievable and the former as more of a stretch. On the topic of employment growth, it’s worth noting that both monthly nonfarm payroll growth and the prime-age labor force participation rate were dragged down by the spread of the Delta variant during the past few months (Chart 4). With new COVID cases falling, we should see stronger payroll growth and a higher prime-age part rate in the months ahead. Relatedly, falling COVID cases will also help alleviate some the constraints on labor supply as workers grow less fearful of the virus and more confident about re-entering the labor force. This will not only push prime-age participation higher, but it will also take some of the sting out of wage growth. Wage growth has been extremely high recently as the number of job openings has far outpaced the number of new hires (Chart 5). Fading COVID fears should increase the pace of hiring and slow wage growth. This will give the Fed even more confidence that it should stay the course. Chart 5Peak Wage Growth?

Peak Wage Growth?

Peak Wage Growth?

The Inflation Expectations Trigger Chart 6Inflation Expectations Are Well-Anchored

Inflation Expectations Are Well-Anchored

Inflation Expectations Are Well-Anchored