Monetary

As tensions from the US-China trade war abate, investors are starting to refocus on economic fundamentals. This year, Chinese policymakers will maintain their tight grip on local government spending and bank lending, and will continue to fine-tune policies…

Highlights The recently signed Phase One deal is positive for China and global equity markets as it brings a temporary truce to the trade war. However, China is unlikely to change its current policy trajectory to create additional domestic demand to consume $200 billion in new imports from the US. China is likely to meet the commitment only half way in the next two years, and meet the 2020 import target from the US by a redistribution of its purchases overseas. The RMB will modestly appreciate in the next three to six months. On the monetary policy front, there is no sign of further monetary easing from the PBoC. We continue to recommend an overweight stance towards Chinese stocks in the next six months, relative to the global benchmark. Feature Economic data released last week, including Q4 GDP growth, December industrial production, fixed-asset investment and trade data, all suggest that the Chinese economy bottomed before the end of 2019. The Phase One trade deal between China and the US marks a significant de-escalation in a two-year trade war. The RMB appreciated by 1.4% against the greenback since the beginning of the year, pushing USD-CNY firmly below the key psychological 7 mark. The performance of equities in China’s onshore and offshore markets confirms that the economy has bottomed. Since December 11, 2019, Chinese cyclical sectors have outperformed defensives and both the investable and domestic markets have broken above their respective 200-day moving averages versus global stocks (Chart 1A and 1B). Chart 1ABoth Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Both Onshore And Offshore Equities Signal A Bottoming In China's Economy

Chart 1BCyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

Cyclicals Have Significantly Outperformed Defensives Lately

We continue to recommend a cyclical long stance on Chinese stocks. We expect pro-growth policy support to accelerate in the first quarter, economic recovery to further solidify, and the Phase One trade deal to reduce economic and financial market volatility until the November 2020 US presidential election. All of these factors should support an outperformance in Chinese stocks relative to their global peers. Some Inconvenient Truth To The Truce China’s commitment to purchase an additional $200 billion in goods from the US was more than market participants anticipated. We do not think China will honor this commitment to its full extent. Moreover, we also do not think this will change China’s domestic economic policy trajectory for 2020. Details in Chapter 6 of the Phase One trade agreement titled “Expanding Trade”1 include: In the next 2 years, China is committed to purchase an additional $200 billion worth of goods and services from the US, from the 2017 baseline. The additional $200 billion amount is split over the next two years: China will need to add no less than $77 billion of imports from the US in 2020, and $123 billion in 2021. This amounts to a 41% increase in 2020 and a 66% increase in 2021, from the 2017 baseline of $186 billion (Chart 2). The text from Chapter 6 of the Phase One deal also specifies that, between January 2020 and December 2021, China will add a total of $77.7 billion in purchases of manufactured goods (including aircraft components), $32 billion in agricultural products, $52.4 billion in energy and $37.9 billion in services from the US (Chart 3). Chart 2Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Phase One Trade Deal Sets An Ambitious Import Target For The Next Two Years

Chart 3Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

Chinese Imports Of Agro And Energy Goods From The US Likely To See The Biggest Increase In 2020 From 2019

China’s annual import growth from the US in 2017 was the highest one in the past ten years. If we assume that China will simply add $200 billion of new imports in the next two years from the US to this high starting point, it will need to boost domestic demand to accommodate at least a 4-6% increase in total imports in the next two years from 2019.2 In contrast, growth in China’s total imports in 2019 contracted by 3% from 2018, and averaged at only 2% in the last five years. In other words, in 2020 and 2021, even if China does not increase imports from other countries, just the commitment from purchases of US goods alone would require a sizable boost in China’s domestic demand. However, the assumption above is overly simplified and optimistic. Even though Chinese leadership may have shifted their policy priority from financial deleveraging to supporting economic growth this year, we do not think they will fully abandon the battle against systemic risks in the financial sector. Therefore, China is unlikely to significantly deviate from its current policy trajectory and stimulate aggressively to create additional domestic demand to consume the agreed $200 billion in new imports from the US. It is equally unlikely that China will absorb the $200 billion additional imports from the US, at the expense of its domestic production. A more plausible approach, which is our base case scenario, is that China will meet a large portion of the 2020 import target before November, to show good faith. After the US presidential election, China will face the challenge of either a re-escalation from the Phase Two trade talk with a re-elected President Trump, or a new US president with his/her own political agenda. In either case, at this point China is unlikely to have the intention to meet the import target for 2021. Chart 4China Likely To Shift Agro And Energy Import Suppliers To The US

Managing Expectations

Managing Expectations

In 2020, to absorb a $77 billion additional imports from the US, China will likely shift some of its imports, such as agriculture and energy products, from other countries to suppliers in the US. China currently imports $150 billion of agriculture goods and $298 billion of energy related products on an annual basis, so the pie is large enough to absorb some of increased import commitments by shifting the sources of imports (Chart 4). The same logic goes for the manufactured goods category in the trade agreement, which includes cars, airplanes, steel, industrial machinery, and so on.3 China is likely to choose to shift its import suppliers of these goods to the US, while increasing its own share of intermediate goods supplies to the US manufacturers. Almost all of the eight subcategories under the manufactured goods category in the Phase One trade agreement are deeply integrated in the global supply chain. For example, foreign value-added share accounts for 23% of the total output value of the US automobile industry.4 In other words, if a “Made in America” car is worth $20,000, $4,600 is produced by foreign suppliers of intermediate goods. Since China has been the leading source of this foreign value-added in the US automobile industry, a sizeable slice of these additional imports will likely benefit Chinese manufacturers. In this scenario, we expect an increase in bilateral trade between China and the US in 2020, at the expense of other players in the global supply chain. Lastly, while this is not our base case scenario, it is possible the Phase One trade agreement was set up for failure, if China is simply hoping to delay the imposition of additional tariffs as part of a gamble that President Trump will not be re-elected. In this scenario, China might not make any meaningful additional purchases from the US even in 2020 (while claiming that they will be made closer to the election), implying that bilateral trade between China and the US will only revert to its historical average this year, at best. Bottom Line: Chinese policymakers are unlikely willing to alter their existing policy trajectory when accommodating more imports of US goods. China will, at best, reshuffle its supply chain to absorb a portion of the commitment before November 2020. The RMB And Monetary Policy: A Refocus On The Economic Fundamentals As tensions from the US-China trade war abate, investors are starting to refocus on economic fundamentals. The RMB has appreciated by 1.4% against the USD since the beginning of this year (Chart 5). The recent appreciation in the currency is a reversal to its fair value, which reflects an ongoing economic recovery (Chart 6). In the next three to six months, the improvement in China’s economic fundamentals and market sentiment should support a continuation in the RMB’s reversal to its structural trend. Chart 5USD/CNY Has Durably Fallen Below 7

USD/CNY Has Durably Fallen Below 7

USD/CNY Has Durably Fallen Below 7

Chart 6The Recent Appreciation In RMB Is A Reversal To Its Fair Value

The Recent Appreciation In RMB Is A Reversal To Its Fair Value

The Recent Appreciation In RMB Is A Reversal To Its Fair Value

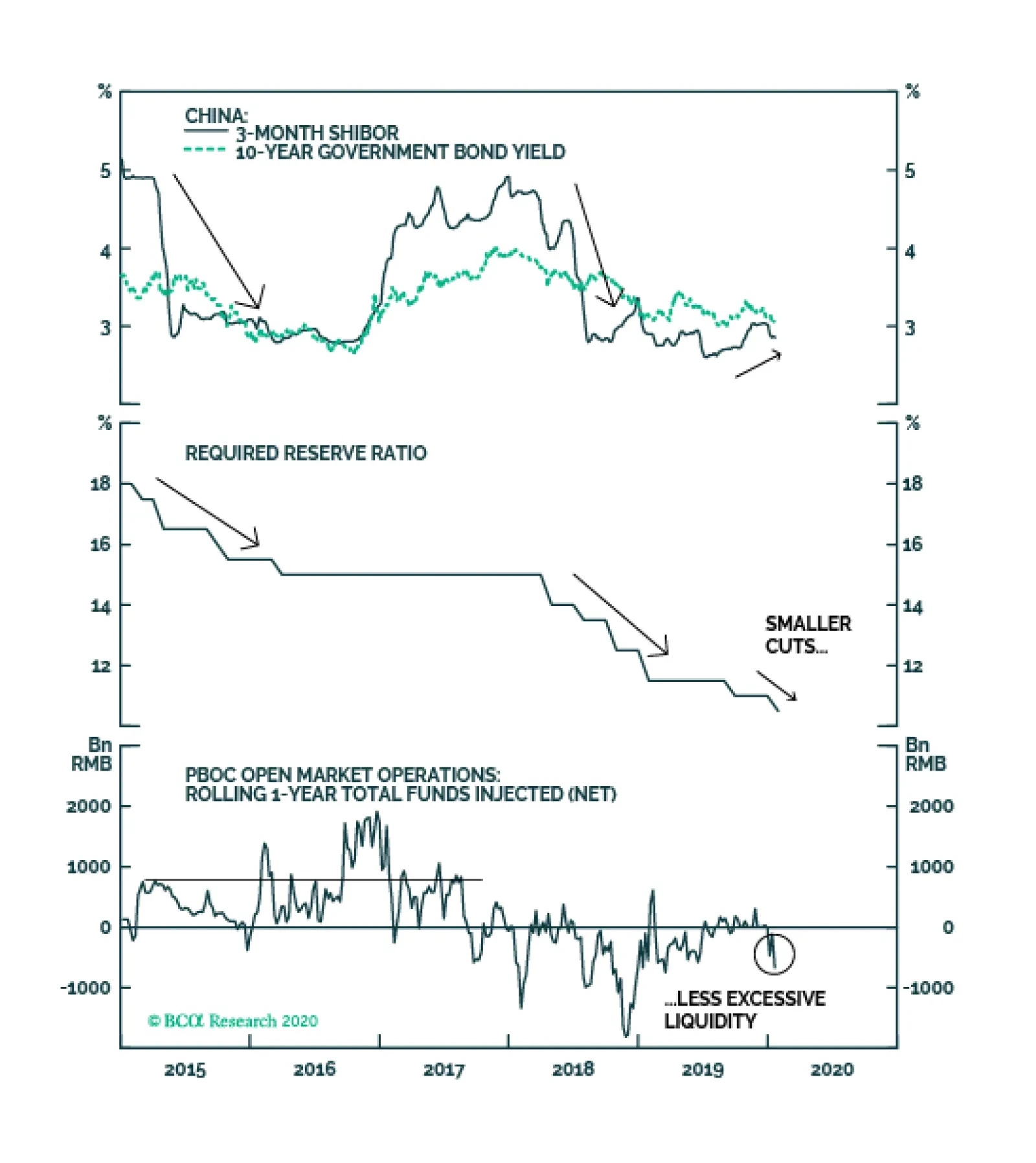

But Chinese leadership’s cautious approach to boosting domestic demand will also cap the upside potential in the RMB appreciation. We think Chinese policymakers will maintain their tight grip this year on local government spending and bank lending, and will continue to fine-tune policies based on economic conditions. This will limit the magnitude in both the stimulus and economic recovery. Baring a major re-escalation in the trade war, the RMB should oscillate within a relatively narrow band through the third quarter of this year. For that reason, the PBoC is unlikely to intervene in the RMB exchange rate by significantly altering its monetary stance (Chart 7). The 3-month interbank lending rate, China’s de facto policy rate, remains low compared with the 2015-16 easing cycle. There is no sign that the PBoC will allow the rate to fall much more. The recent bank reserve requirement ratio (RRR) rate cut provides additional liquidity to the interbank system, but on a net basis liquidity does not seem excessive (Chart 8). Chart 7PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

PBoC Unlikely To Alter Monetary Policy To Intervene RMB Exchange Rate This Year

Chart 8No Sign Of Meaningful Monetary Easing From PBoC

No Sign Of Meaningful Monetary Easing From PBoC

No Sign Of Meaningful Monetary Easing From PBoC

Historically, the 3-month interbank lending rate only falls significantly and durably when the PBoC places consecutive RRR rate cuts (in both 2015 and mid-2018) and/or keeps net fund injections positive through the open market for a prolonged period (such as in the 2015/16 easing cycle). Chart 8 suggests the current monetary environment does not indicate that such an extremely easy stance is in place, as PBoC net fund injections through the open market remain negative. Furthermore, neither the 3-month interbank lending rate nor the 10-year government bond yield has fallen below its most recent lows in the third quarter of last year. Bottom Line: While the current environment supports a stronger RMB, the upside potential in RMB appreciation is capped by a modest scale of economic recovery. There is no sign that the PBoC is easing its monetary stance by lowering the policy rate. Investment Conclusions We have been cyclically overweight Chinese stocks on the basis of a bottoming in the economy in the first quarter of 2020, and the likelihood of an eventual trade deal. These two factors were confirmed in the past two weeks. Last week’s small selloffs in both onshore and offshore Chinese equity markets were likely technical corrections and pre-Chinese New Year profit taking, rather than a fundamental shift in investors’ sentiment towards Chinese stocks (Chart 9). We expect Chinese stocks to resume an upward trajectory after the Chinese New Year. Chart 9Small Corrections Following A 14% Gain Since Dec 2019

Small Corrections Following A 14% Gain Since Dec 2019

Small Corrections Following A 14% Gain Since Dec 2019

Chart 10Offshore Stocks Still Showing More Upside Potential Than Onshore

Offshore Stocks Still Showing More Upside Potential Than Onshore

Offshore Stocks Still Showing More Upside Potential Than Onshore

China’s economic conditions and corporate earnings should continue to improve, with investable stocks showing more upside potential than their domestic counterparts (Chart 10). As growth supporting measures continue to work their way through the economy and solidify an economic recovery, China’s leadership may pull back the scale of the stimulus in the second half of the year. Therefore, the relative outperformance in both markets may be front loaded and subsequently subside in the second half of 2020. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 https://assets.bwbx.io/documents/users/iqjWHBFdfxIU/rVaHxDBUtdew/v0 2 China’s total imports of goods and services in 2019 was $2604 billion, including $168 billion imports from the US. If China was to fully meet the $200 billion target of additional imports from the US, assuming no change to imports from other countries in 2020 from 2019, China’s total imports would jump to $2699 billion in 2020 and $2745 billion in 2021. 3 The eight subcategories of Manufacturing Goods listed in the Annex 6.1 of the Phase One Trade agreement include: Industrial Machinery, Electrical Equipment and Machinery, Pharmaceutical Products, Aircraft, Vehicles, Optical and Medical Instruments, Iron and Steel, Other Manufactured Goods including solar-grade polysilicon and other organic and inorganic chemicals, hardwood lumber, integrated circuits (manufactured in US), and chemical products. 4 WIOD Data, 2016 release and OECD Input-Output Tables (IOTs), 2015 release. Cyclical Investment Stance Equity Sector Recommendations

Highlights We continue to have a positive view on global equities over the next 12 months, but see heightened risks of a near-term correction. Despite dwindling spare capacity, government bond yields are still lower today than they were shortly after the financial crisis. Many investors argue that bond yields cannot rise much because asset values would plunge if yields rose sharply, while debt burdens would quickly become unsustainable. We disagree. We think there is greater scope for yields to rise than is widely believed. Investors should maintain below-benchmark duration in fixed-income portfolios, favoring inflation-linked over nominal bonds and positioning for steeper yield curves. Gold should also do well next year. As long as bond yields are rising in response to stronger growth, as will be the case for the next two years, equities will fare well. The stock market will buckle, however, once stagflation sets in around 2022. Stocks Need To Work Off Overbought Conditions Before Moving Higher Again In last week’s report, entitled “Time For A Breather,” we downgraded our tactical three-month view on global equities from overweight to neutral on the grounds that stocks had run up too hard, too fast. Net long positions in equity futures among asset managers and levered funds are now at levels that have historically preceded corrections (Chart 1). Chart 1Stocks Are At A Heightened Risk Of A Correction

Stocks Are At A Heightened Risk Of A Correction

Stocks Are At A Heightened Risk Of A Correction

Chart 2Breadth Is Quite Narrow

Breadth Is Quite Narrow

Breadth Is Quite Narrow

Chart 3The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The rally has been lopsided, characterized by very narrow breadth. The top five stocks in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, and Facebook) now comprise 18% of market cap, a higher share than in the late 1999/early 2000s (Chart 2). As my colleague, Anastasios Avgeriou, has pointed out, Apple’s $30 billion one day market cap gain on January 9th was greater than the market cap of the median stock in the S&P 500 index. Despite our near-term concerns, we continue to maintain a positive 12-month view on global equities. Easier financial conditions, a turn in the global inventory cycle, modestly looser fiscal policy in the UK and euro area, and re-upped fiscal/credit stimulus in China should all support global growth this year. Faster growth, in turn, will lift corporate earnings. The equity risk premium also remains quite high, particularly outside the US (Chart 3). A Fragile Trade Truce A de-escalation in the trade war should provide a further tailwind to equities. The “phase one” agreement signed on Wednesday features a commitment by China to purchase an additional $200 billion in US goods and services over the next two years relative to 2017 levels. In return, the US will halve tariffs, to 7.5%, on the $120 billion tranche in Chinese imports and suspend any further tariff hikes. No firm schedule exists to begin “phase two” talks, and at this point, it is quite likely that no negotiations will take place until after the US presidential election. Nevertheless, the tail risk of an out-of-control trade war has receded for the time being, which is positive for stocks. Better Chinese Trade Data Adding to growing optimism over the global economy and diminished trade tensions, Chinese trade data surprised on the upside this week. Exports rose 7.6% in December, well above the consensus estimate of 2.9%. Imports surged 16.3%, easily surpassing the consensus estimate of 9.6%. While base effects explain some of the improvement, the overall tone of the trade data is consistent with the strengthening Chinese PMIs and improvement in industrial production and retail sales (Chart 4). Chart 4Chinese Trade Data Is Improving

Chinese Trade Data Is Improving

Chinese Trade Data Is Improving

Chart 5Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better News Out Of China Has Propelled The Yuan Higher Versus The US Dollar

Better news out of China has pushed the yuan to the strongest level against the US dollar since last summer (Chart 5). The Chinese currency is the most important driver of other EM currencies. If the yuan continues to strengthen, as we expect, EM assets – particularly EM stocks and local-currency bonds – should do well this year. How High Can Bond Yields (Realistically) Go? Despite rising over the past few months, global government bond yields are lower today than they were shortly after the financial crisis ended (Chart 6). The decline in yields has occurred alongside dwindling spare capacity. In most countries, the unemployment rate today is below 2007/08 lows (Chart 7). Many investors argue that bond yields cannot rise much from current levels because asset values would plunge if yields rose sharply, while debt burdens would quickly become unsustainable. If such an unfortunate turn of events were to occur, central bankers would have to shelve any tightening plans, just as Jay Powell had to do in late 2018. Chart 6Bond Yields Are Lower Today Than They Were After The Great Recession

Bond Yields Are Lower Today Than They Were After The Great Recession

Bond Yields Are Lower Today Than They Were After The Great Recession

Chart 7Unemployment Rates Are Below Their Pre-Recession Lows In Most Economies

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Convexity Fears One argument often heard these days is that asset prices have become hypersensitive to changes in interest rates. There is some basis for thinking this. As Box 1 explains, the relationship between asset returns and interest rates tends to be “convex,” meaning that any given change in interest rates will have a bigger effect on returns if rates are low to begin with, as they are today. The effect is particularly pronounced for long duration assets such as long-term bonds, equities, or real estate. Nevertheless, while the theoretical presence of convexity in asset returns is crystal clear, many commentators overstate its practical importance. As Chart 8 shows, the average maturity of government debt stands at seven years. At that level of maturity, the effects of convexity tend to be quite small.1 Chart 8Average Debt Maturity Is Below 10 Years In Most Countries

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Granted, the overall stock of debt has increased in relation to GDP. However, much of that additional debt has been absorbed by central banks, reducing the amount of government debt available for the private sector. What about equities? The ratio of stock market capitalization-to-GDP has risen to 59%, up from a low of 24% in 2009, and close to its 2000 highs (Chart 9). Does that mean that stocks will sink if yields rise from current levels? Not necessarily. Remember that the discount rate is not the only thing that affects the present value of a stream of income. The expected growth rate of that income also matters. In fact, in the standard dividend discount model, it is simply the difference between the discount rate and the growth rate of dividends that determines how much a stock is worth. If higher bond yields coincide with rising growth expectations, stock prices do not need to fall at all. Chart 9Equity Market Cap Is Approaching Previous Highs

Equity Market Cap Is Approaching Previous Highs

Equity Market Cap Is Approaching Previous Highs

Chart 10 shows that the monthly correlation between equity returns and bond yields remains as high as ever. This suggests that favorable economic news, to the extent that it leads investors to revise up the expected growth rate for earnings, usually more than compensates for a rising discount rate (Chart 11). Chart 10Correlation Between Equity Returns And Bond Yields Remains High

Correlation Between Equity Returns And Bond Yields Remains High

Correlation Between Equity Returns And Bond Yields Remains High

Chart 11Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

Earnings Estimates Tend To Move In Sync With Swings In Bond Yields

So why are so many investors worried that higher bond yields will undercut stocks? The answer has less to do with convexity and more to do with the fear that bond yields will reach a level that chokes off growth. The combination of a rising discount rate and a falling growth rate would be toxic for equities and other risk assets. Debt Worries Likewise, it is not so much that corporate bond investors are worried that rising yields will cause interest payments to swell. After all, interest costs are still quite low as a share of cash flows for most firms (Chart 12). Rather, the fear is that higher yields will imperil growth, causing those cash flows to evaporate. Government debt is also much less of a problem than often assumed, at least in countries that issue bonds in their own currencies. The standard rule for debt sustainability says that the debt-to-GDP ratio will always converge to a stable level if the interest rate is below the growth rate of the economy.2 This is easily the case in almost all economies today (Chart 13). Chart 12US Corporate Sector: Interest Payments Are Not A Worry

US Corporate Sector: Interest Payments Are Not A Worry

US Corporate Sector: Interest Payments Are Not A Worry

Chart 13Bond Yield Minus GDP Growth: Please Mind The Gap

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

The only places where central banks are severely constrained in raising rates are in economies such as Canada, Sweden, and Australia where debt-financed housing bubbles have formed (Chart 14). However, even in these countries, the quality of mortgage underwriting has generally been strong, implying that a banking crisis would likely be avoided. Chart 14Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

Canada, Sweden, And Australia Stand Out As Having Very Frothy Housing Markets

It’s Really About The Neutral Rate The discussion above suggests that the main constraint to higher bond yields is the economy itself. If bond yields rise enough, the interest rate-sensitive sectors of the economy will weaken, and a recession will ensue. As long as bond yields are rising in response to stronger growth, as will be the case for the next two years, equities will be fine. Unfortunately, no one knows where the neutral rate – the interest rate demarcating the boundary between expansionary and contractionary monetary policy – really lies. Chart 15Rising Labor Share Of Income Occurring Alongside Labor Market Tightening

Rising Labor Share Of Income Occurring Alongside Labor Market Tightening

Rising Labor Share Of Income Occurring Alongside Labor Market Tightening

Slower trend growth has probably reduced the neutral rate, as has the shift to a more “capital-lite” economy. On the flipside, other forces have probably raised the neutral rate over the past few years. A tighter labor market has increased workers’ share of national income (Chart 15). Since workers spend more of every dollar of income than companies, this has raised aggregate demand. Fiscal policy has also been loosened, while elevated asset prices have likely incentivized some spending that would otherwise not have taken place. Even though we do not know the exact value of the neutral rate, we do know that the unemployment rate has been falling in most countries for the past 10 years, a period during which bond yields were generally higher than today. This suggests that monetary policy remains in expansionary territory. True, global growth did slow in 2018, just as the Fed was raising rates. However, this probably had more to do with the natural ebb and flow of the global manufacturing cycle, exacerbated by the Chinese deleveraging campaign and the brewing trade war. If global growth recovers this year, as we expect, estimates of the neutral rate will rise. This will allow equity prices to increase even in an environment of modestly higher bond yields. Inflation Is Coming… Eventually While stronger economic growth will lift bond yields this year, the big move in yields will only come when inflation breaks out. Core inflation tends to track unit labor costs (Chart 16). Unit labor cost inflation has remained range-bound for most of the recovery in the United States, which explains the failure of inflation to take flight. Unit labor cost inflation has been even more moribund elsewhere. Chart 16Core Inflation Tends To Track Unit Labor Costs

Core Inflation Tends To Track Unit Labor Costs

Core Inflation Tends To Track Unit Labor Costs

Chart 17Correlation Between Labor Market Slack And Wage Growth Remains Intact

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Looking out, barring a major surge in productivity, rising wage growth should lead to accelerating unit labor cost inflation, first in the US and then in the rest of the world, which will translate into higher price inflation. We doubt that such a price-wage spiral will erupt this year. If anything, US wage growth has leveled off recently, with the year-over-year change in average hourly earnings falling back below the 3% mark. Nevertheless, the long-term correlation between labor market slack and wage growth remains intact (Chart 17). As wage growth reaccelerates, unit labor cost inflation will drift higher, setting the stage for a period of rising price inflation. Investors should maintain below-benchmark duration in global fixed-income portfolios, favoring inflation-linked over nominal bonds and positioning for steeper yield curves. Gold should also do well next year. As long as bond yields are rising in response to stronger growth, as will be the case for the next two years, equities will be fine. The stock market will buckle, however, once stagflation sets in around 2022. Box 1 Asset Prices And Interest Rates: The Role Of Convexity

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1Assuming semi-annual compounding, the price of a 10-year bond with a 5% coupon rate falls by 7.9% if the yield increases from 1% to 2%, which is only slightly higher than the 7.6% decline that would be incurred if the yield increases from 4% to 5%. 2One might add that if the interest rate is below the growth rate of the economy, a higher starting point for the debt stock will allow for more debt issuance without leading to a higher debt-to-GDP ratio. As we have shown before, the steady-state debt-to-GDP ratio can be expressed as p/(r-g), where r is the interest rate, g is trend GDP growth, and p is the primary (i.e., non-interest) budget balance. Thus, for example, if the government wanted to achieve a stable debt-to-GDP ratio of 50% and r-g is -2%, it would need to run a primary budget deficit of 0.5*0.02=1% of GDP. However, if the government targeted a stable debt-to-GDP ratio of 200%, it could run a primary budget deficit of 2*0.02=4% of GDP. Global Investment Strategy View Matrix

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

MacroQuant Model And Current Subjective Scores

Bond Yields: How High Is Too High?

Bond Yields: How High Is Too High?

Strategic Recommendations Closed Trades

Highlights Global Investment Strategy View Matrix

Time For A Breather

Time For A Breather

Receding trade tensions; diminished risks of a hard Brexit; reduced odds of a victory for Elizabeth Warren in the US presidential elections; liquidity injections by most major central banks; and improved sentiment about the state of the global economy all helped push stocks higher late last year. Some clouds have formed over the outlook since the start of the year, however. The December US ISM manufacturing index fell to the lowest level since 2009, while the PMIs in the euro area, UK, and Japan gave up some of their November gains. The conflict between the US and Iran also flared up. Although tensions have abated in recent days, BCA’s geopolitical strategists worry that the détente may not last. The US is seeking to shift its military focus towards East Asia in order to counter China’s ascendency. They argue that this could create a dangerous power vacuum in the Middle East. Stock market sentiment is quite bullish at the moment, which makes equities more vulnerable to any disappointing news. While we are maintaining our positive 12-month view on global equities and high-yield credit in anticipation that global growth will rebound convincingly later this year, we are downgrading our tactical 3-month view to neutral. Ho Ho Ho After handing investors a sack of coal last Christmas, Santa was back to his true self this past holiday season. Global equities rose 3.4% in December, finishing the year off with a stellar fourth quarter which saw the MSCI All-Country World index surge by 8.6%. Five forces helped push stocks higher: 1) Receding trade tensions; 2) Diminished risks of a hard Brexit; 3) Reduced odds of a victory for Elizabeth Warren in the US presidential elections; 4) Liquidity injections by the Fed, ECB, and the People’s Bank of China; and arguably most importantly 5) Improved sentiment about the state of the global economy. Tarrified No More Trade tensions subsided sharply after China and the US reached a “Phase One” agreement. The deal prevented tariffs from rising on December 15th on $160 billion of Chinese imports. It also rolls back the tariff rate from 15% to 7.5% on about $120 billion in imports that have been subject to levies since September (Chart 1). Chart 1The Evolution Of The US-China Trade War

The Evolution Of The US-China Trade War

The Evolution Of The US-China Trade War

In addition, the Trump Administration allowed the November 13th deadline on European auto tariffs to lapse. This suggests that the US is unlikely to impose tariffs under the Section 232 investigation of auto imports. The auto sector has been at the forefront of the global manufacturing slowdown, so any good news for that industry is welcome. To top it all off, the US House of Representatives ratified the USMCA, the successor to NAFTA, on December 19th. We expect it to be signed into law in the first quarter of this year. Brexit Risks Fading... Chart 2The Majority Of British Voters Aren't Keen On Brexit

The Majority Of British Voters Aren't Keen On Brexit

The Majority Of British Voters Aren't Keen On Brexit

Boris Johnson’s commanding victory in the UK elections has given him the votes necessary to push a withdrawal bill through parliament by the end of the month. The British government will then seek to negotiate a free trade agreement by the end of the year. A “no-deal” Brexit is unacceptable to the majority of British voters (Chart 2). As such, the Johnson government will have no choice but to strike a deal with the EU. ... While Trump Gains On the other side of the Atlantic, President Trump’s re-election prospects improved late last year despite (and perhaps because of) the ongoing impeachment process. There is an uncanny correlation between the probability that betting markets assign to a Trump victory and the value of the S&P 500 (Chart 3). Chart 3An Uncanny Correlation

An Uncanny Correlation

An Uncanny Correlation

Chart 4Who Will Win The 2020 Democratic Nomination?

Time For A Breather

Time For A Breather

It certainly has not hurt market sentiment that Elizabeth Warren’s poll numbers have been dropping recently (Chart 4). Warren’s best hope was to squeeze out Bernie Sanders as soon as possible, thereby leaving the far-left populist lane all to herself. That dream appears to have been dashed, which suggests that even if Trump loses, a centrist like Joe Biden could emerge as president. An Uneasy Truce It remains to be seen how President Trump’s decision to assassinate General Qassem Soleimani, a top Iranian commander, will affect the election outcome. A YouGov/HuffPost poll taken over the weekend revealed that 43% of Americans approved of the airstrike against Soleimani compared to 38% that disapproved.1 History suggests that the public’s patience for war will quickly wear thin if it results in American casualties or significantly higher gasoline prices. Neither side has an incentive to allow the conflict to spiral out of control. Foreign minister Mohammad Javad Zarif tweeted on Tuesday shortly after Iran lobbed missiles at two US military bases that Iran had “concluded” its retaliatory strike, adding that “We do not seek escalation or war.” Despite claims on Iranian public television that 80 “American terrorists” were killed in the attacks, no US troops were harmed. This suggests that the Iranians may be putting on a show for domestic consumption. The US economy is less vulnerable to spikes in oil prices than in the past. Nevertheless, plenty of things could still go wrong. BCA’s geopolitical team, led by Matt Gertken, has argued that the US is seeking to shift its military focus towards East Asia in order to counter China’s ascendency. This could create a dangerous power vacuum in the Middle East. There is also a risk that President Trump overplays his hand. Contrary to the President’s claims, Soleimani was quite popular in Iran (Chart 5). If Trump begins to mock the Iranian leadership’s feeble response, Iran will have no choice but to take more aggressive action. Chart 5Soleimani Was More Popular In Iran Than Trump Claims

Time For A Breather

Time For A Breather

Chart 6US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

One thing that could embolden Trump is that the US economy is less vulnerable to spikes in oil prices than in the past. US oil output reached as high as 12.9 mm b/d in 2019, allowing the country to become a net exporter of oil for the first time in history (Chart 6). Any increase in oil prices would incentivize further domestic production, which would help bring prices back down. The US economy has also become less energy intensive – it takes less than half as much oil to produce a unit of GDP today than it did in the early 1980s. Finally, unlike in the past, the Fed will not need to raise rates in response to higher oil prices due to the fact that inflation expectations are currently well anchored. In fact, as we discuss below, we expect the Fed and other central banks to continue to provide a tailwind for growth over the course of 2020. The Fed’s “It’s Not QE” QE Program The jump in overnight lending rates in mid-September torpedoed the Federal Reserve’s efforts to shrink its balance sheet. Thanks to a steady stream of Treasury bill purchases since then, the Fed’s asset holdings have swelled by over $400 billion, reversing more than half of the decline observed since early 2018 (Chart 7). Chart 7Fed's Asset Holdings Are Growing Anew

Fed's Asset Holdings Are Growing Anew

Fed's Asset Holdings Are Growing Anew

Chart 8The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed has insisted that its latest intervention does not amount to a new QE program, stressing that it is buying short-term securities rather than long-dated bonds. In so doing, it is simply creating bank reserves, rather than seeking to suppress the term premium by altering the maturity structure of the private sector’s holdings of government debt. Nevertheless, even such straightforward interventions have proven to be powerful signaling tools. By growing its balance sheet, a central bank is implicitly promising to keep monetary policy very accommodative. It is worth remembering that the run-up in the NASDAQ in 1999 coincided with a significant balance-sheet expansion by the Fed in response to Y2K fears, which came on the heels of three “insurance cuts” in 1998 (Chart 8). Gentle Jay Paves The Way Chart 9Inflation Expectations Remain Muted

Inflation Expectations Remain Muted

Inflation Expectations Remain Muted

In 2000, the Fed moved quickly to reverse the liquidity injection it had orchestrated the prior year. We do not expect such a reversal anytime soon. Moreover, unlike in 2000, when the Federal Reserve kept raising rates – ultimately bringing the Fed funds rate up to 6.5% in May 2000 – the Fed is likely to stay on hold this year. The Fed’s ongoing strategic policy review is poised to move the central bank even closer towards explicitly adopting an average inflation target of 2% over the course of a business cycle. Since inflation tends to fall during recessions, this implies that the Fed will seek to target an inflation rate somewhat higher than 2% during expansions. Realized core PCE inflation has averaged only 1.6% since the recession ended. Both market-based and survey-based measures of long-term inflation expectations remain downbeat (Chart 9). This suggests that the bar for raising rates this year is quite high. More Monetary Easing In The Euro Area And China Chart 10Chinese Monetary Easing Should Help Global Growth Bottom Out

Chinese Monetary Easing Should Help Global Growth Bottom Out

Chinese Monetary Easing Should Help Global Growth Bottom Out

The ECB resumed its QE program in November after a 10-month hiatus. While the current pace of €20 billion in monthly asset purchases is well below the prior pace of €80 billion, the central bank did say it would continue buying assets for “as long as necessary” to bring inflation up to its target. The language harkens back to Mario Draghi’s 2012 “whatever it takes” pledge, this time applied to the ECB’s inflation mandate. Not to be outdone, the People’s Bank of China cut the reserve requirement ratio by 50 basis points last week, a move that will release RMB 800 billion ($US 115 billion) of fresh liquidity into the banking system. Historically, cuts in reserve requirements have led to faster credit growth and ultimately, to stronger economic growth both in China and abroad (Chart 10). The PBOC has also instructed lenders to adopt the Loan Prime Rate (LPR) as the new benchmark lending rate. The LPR currently sits 20bps below the old benchmark rate (Chart 11). Hence, the PBOC’s order amounts to a stealth rate cut. Our China strategists expect further reductions in the LPR over the next six months. In addition, the crackdown on shadow bank lending seems to be subsiding, which bodes well for overall credit growth later this year (Chart 12). Chart 11China: Stealth Monetary Easing

China: Stealth Monetary Easing

China: Stealth Monetary Easing

Chart 12Crackdown On Shadow Banking In China Is Easing

Crackdown On Shadow Banking In China Is Easing

Crackdown On Shadow Banking In China Is Easing

Rising Economic Confidence Chart 13Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Chart 14The Wider Public Was Also Worried About A Downturn

The Wider Public Was Also Worried About A Downturn

The Wider Public Was Also Worried About A Downturn

At the start of 2019, nearly half of US CFOs thought the economy would be in a recession by the end of the year. Similarly, two-thirds of European CFOs and four-fifths of Canadian CFOs expected their respective economies to succumb to recession. Professional economists were equally dire (Chart 13). Households also became increasingly worried about a downturn. Google searches for “recession” spiked to near 2009-highs last summer (Chart 14). The mood has certainly improved since then. According to the latest Duke CFO survey, optimism about the economic outlook has increased. More importantly, CFO optimism about the prospects for their own firms has risen to the highest level in the 18-year history of the survey (Chart 15). Chart 15CFOs Have Become More Optimistic Of Late

CFOs Have Become More Optimistic Of Late

CFOs Have Become More Optimistic Of Late

Show Me The Money Going forward, global growth needs to accelerate in order to validate the improved confidence of CFOs and investors alike. We think that it will, thanks to the lagged effects from the easing in financial conditions in 2019, a turn in the global inventory cycle, a de-escalation in the trade war, easier fiscal policy in the UK and euro area, and re-upped fiscal/credit stimulus in China. For now, however, the economic data remains mixed. On the positive side, household spending is still robust across most of the world, a fact that has been reflected in the resilience of service-sector PMIs (Chart 16). Chart 16AThe Service Sector Has Remained Resilient (I)

The Service Sector Has Remained Resilient (I)

The Service Sector Has Remained Resilient (I)

Chart 16BThe Service Sector Has Remained Resilient (II)

The Service Sector Has Remained Resilient (II)

The Service Sector Has Remained Resilient (II)

Chart 17US Wage Growth Has Picked Up, Especially At The Bottom Of The Income Distribution

Time For A Breather

Time For A Breather

Chart 18US Housing Backdrop Is Solid

US Housing Backdrop Is Solid

US Housing Backdrop Is Solid

The US consumer, in particular, is showing little signs of fatigue. The Atlanta Fed GDPNow estimates that real personal consumption grew by 2.4% in the fourth quarter, having increased at an average annualized pace of 3% in the first three quarters of 2019. Both a strong labor market and housing market have buoyed US consumption. Payrolls have risen by an average of 200K per month for the past six months, double what is necessary to keep up with labor force growth. This week’s strong ADP release – which featured a 29K jump in jobs in goods-producing industries in December, the best since April – suggests that today’s jobs report will remain healthy. In addition, wage growth has picked up, particularly at the bottom of the income distribution (Chart 17). Residential construction has also been strong. Homebuilder sentiment reached the best level since June 1999 (Chart 18). Global Manufacturing: Too Early To Call The All-Clear The outlook for manufacturing remains the biggest question mark in the global economy. The US ISM manufacturing index dropped to 47.2 in December, its lowest level since June 2009. The composition of the report was poor, with the new orders-to-inventory ratio dropping close to recent lows. Chart 19Other US Manufacturing Gauges Are Not As Weak As The ISM

Other US Manufacturing Gauges Are Not As Weak As The ISM

Other US Manufacturing Gauges Are Not As Weak As The ISM

We would discount the ISM report to some extent. The regional Fed manufacturing indices have not been nearly as disappointing as the ISM (Chart 19). The Markit PMI, which tracks US manufacturing activity better than the ISM, clocked in at a respectable 52.4 in December, down only slightly from November’s reading of 52.6. Nevertheless, it is hard to be excited about the near-term outlook for US manufacturing, especially in light of Boeing’s decision to suspend production of the 737 Max temporarily. Most estimates suggest that the production halt will reduce real US GDP growth by 0.3%-to-0.5% in the first quarter. The euro area manufacturing PMI gave up some of its November gains, falling to 46.3 in December. While the index is still above its September low of 45.7, it has been under 50 for 11 straight months now. The UK and Japanese PMI also retreated. Chinese manufacturing has shown clearer signs of bottoming out. Despite dipping in December, the private sector Caixin manufacturing PMI remains near its 2017 highs. The official PMI published by the National Bureau of Statistics is less upbeat, but still managed to come in slightly above 50 in December. The production subcomponent reached the highest level since August 2018. Reflecting the positive trend in the Chinese economy, Korean exports to China rose by 3.3% in December, the first positive growth rate in 14 months (Chart 20). Taiwan’s exports have also rebounded. The manufacturing PMI rose above 50 in both economies in December. In Taiwan’s case, this was the first time the PMI moved into expansionary territory since September 2018. On balance, we continue to expect global manufacturing to recover in 2020. This is in line with our observation that global manufacturing cycles typically last three years, with 18 months of weaker growth followed by 18 months of stronger growth (Chart 21). That said, the weakness in European and US manufacturing (at least judged by the ISM) is likely to give investors pause. Chart 20Some Positive Signs Emerging From Korea And Taiwan

Time For A Breather

Time For A Breather

Chart 21A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

Investment Conclusions We turned bullish on stocks in late 2018, having temporarily moved to the sidelines during the summer of that year. Global equities have gained 25% since our upgrade. We see another 10% of upside for 2020, led by European and EM bourses. Despite its recent gains, the real value of the MSCI All-Country World Index is only 3% above its prior peak in January 2018. The 12-month forward PE ratio of 16.3 is still somewhat lower than it was back then. The valuation picture is even more enticing if we compare equity earnings yields with bond yields, which is tantamount to computing a rough equity risk premium (ERP). The global ERP remains quite high by historic standards, especially outside the US where earnings yields are higher and bond yields are generally lower (Chart 22). Chart 22The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

Chart 23Stock Market Sentiment Is Quite Bullish

Stock Market Sentiment Is Quite Bullish

Stock Market Sentiment Is Quite Bullish

Nevertheless, sentiment is quite positive towards stocks at the moment (Chart 23). Elevated bullish sentiment, against the backdrop of ongoing uncertainty about the outlook for global manufacturing and an uneasy truce between the US and Iran, poses a near-term headwind to risk assets. As such, while we are maintaining our positive 12-month view on global equities and high-yield credit, we are downgrading our tactical 3-month view to neutral for the time being. We do not regard this as a major realignment of our views; we will turn tactically bullish again if stocks dip about 5% from current levels. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Ariel Edwards-Levy, “Here's What Americans Think About Trump's Iran Policy,” TheHuffingtonPost.com (January 6, 2020). MacroQuant Model And Current Subjective Scores

Time For A Breather

Time For A Breather

Strategic Recommendations Closed Trades

Highlights The consensus view seems to be that equities have to cool off in 2020, even if the danger has passed: Recession fears have dissipated as the yield curve has returned to its normal upward-sloping orientation and US-China trade tensions have abated, but equity return expectations are modest following last year’s bonanza. We agree that a bear market is unlikely, but expect a better year than the consensus, … : Bull markets tend to sprint to the finish line, and if the next recession won’t start before the middle of 2021, 2020 should be another strong year for the S&P 500. … even if earnings growth is uninspiring: Multiples almost always expand when the Fed eases from an already accommodative position, and they expand a lot provided the Fed isn’t easing in response to a market bust or financial crisis. We expect that an inflation revival will take the consensus by surprise, but not this year: We think rising inflation will induce the Fed to bring the curtain down on the expansion and the equity bull market, but not until 2021 at the earliest. Feature We spent the last full week before the holidays meeting with clients and prospects on the west coast. As they look ahead to 2020, investors don’t see any major storm clouds on the horizon, but they sense that stocks have run about as far as they can. We agree with the view that neither a recession nor a bear market awaits, but we expect equities will comfortably outdistance bonds and cash. Forced to take a stand on whether the S&P 500 will beat or fall short of the typical consensus expectation for mid-to-high-single-digit gains,1 we would happily bet the over. As we detailed in our last two publications in December, our optimistic take stems from the deliberately reflationary policy being pursued by the Fed and other major central banks. Restoring inflation expectations to its desired range is job number one for the Fed, and its open commitment to doing so ensures that risk assets will have the monetary policy wind at their back for an extended period. The European Central Bank and the Bank of Japan want to rekindle inflation as well, and can be counted upon to maintain easy policy settings. The rest of the world’s central banks will continue to take their cue from their more influential peers, as no one wants the export headwind of a strong currency in a low-growth environment. Earnings growth has been the primary driver of the 11-year-old equity bull market, not multiple expansion. In our base-case scenario, easy monetary policy will encourage multiple expansion, while a less threatening trade climate, and a modest revival in Chinese aggregate demand, will boost economic activity, especially outside of the US. The modest global acceleration provoked by a pickup in Chinese imports will support earnings growth, so that both equity drivers, earnings and multiples, will be moving in the right direction. We anticipate that at least half of the current bull market’s remaining upside will come from multiple expansion, however. Dismaying as it might be for investors with a value bent, our bull thesis is built on the view that today’s fully-to-somewhat-richly-valued stocks will become overvalued before this market cycle is complete. A Stealth Earnings Boom Skeptics of the efficacy of extraordinarily accommodative monetary policy have decried the current bull market as “manipulated,” fed by monetary steroid injections that have inflated asset prices at the cost of undermining the real economy’s future prospects. The data flatly contradict the skeptics’ claims: since the end of February 2009, consensus forward four-quarter S&P 500 earnings expectations have grown at an annualized rate of 9.6% (Chart 1, middle panel), while the forward multiple has expanded at a 4.6% pace (Chart 1, bottom panel). Growth in forward earnings estimates has accounted for two-thirds of the 14.6% annualized appreciation in the S&P 500 (Chart 1, top panel); multiple expansion has only contributed a third. Chart 1A Great Decade For Earnings

A Great Decade For Earnings

A Great Decade For Earnings

Chart 2DM Growth Has Been Weak

DM Growth Has Been Weak

DM Growth Has Been Weak

Positioning for a valuation overshoot does not inspire as much confidence as positioning for robust earnings growth. US economic growth has been lackluster since the crisis (Chart 2, top panel), and it’s been downright anemic in Europe (Chart 2, middle panel) and Japan (Chart 2, bottom panel). Few investors foresaw potent earnings growth against that macro backdrop, as aggregate corporate revenue growth ought to converge with nominal GDP growth over time. Only margin expansion could deliver S&P 500 earnings growth above and beyond a meager 4% revenue growth base. As early as 2011, US corporate profit margins looked quite stretched (Chart 3), making further expansion seem improbable. After adjusting for the secular decline in effective corporate income tax rates, corporations’ growing share of national income, the expansion of the high-margin financial sector and the secular decline in debt service costs,2 however, history suggested that profit margins still had room to grow. It would be 2018 before they would peak, thanks in part to the 40% cut in the top marginal corporate income tax rate, and the plunge in debt service costs (Chart 4). Compensation is corporations’ single largest expense, though, and the inexorable decline in labor's share of profits was the key driver (Chart 5). Since China’s entry into the WTO, real wages have failed to keep up with productivity gains (Chart 6), dramatizing the shift of profit share from labor to capital. Chart 3Never Say Die Margin Growth, Nourished On...

Never Say Die Margin Growth, Nourished On...

Never Say Die Margin Growth, Nourished On...

Chart 4... Rock-Bottom Rates ...

... Rock-Bottom Rates ...

... Rock-Bottom Rates ...

Chart 5... And Labor's Woes

... And Labor's Woes

... And Labor's Woes

Chart 6Globalization Has Helped Corporate Profits

Globalization Has Helped Corporate Profits

Globalization Has Helped Corporate Profits

Profit margins contracted across the first three quarters of 2019, with per-share revenue growth topping per-share earnings growth by an average of three percentage points. We expect that real unit labor costs will rise as the pendulum swings back in labor’s direction in line with an extremely tight job market and a slowdown in outsourcing as globalization loses momentum. Revived activity in the rest of the world can offset some margin pressure from a rising wage bill, however, especially if it helps push the dollar lower. And rising wages aren’t all bad for profits, as rising household income leads to rising consumption, and rising consumption boosts corporate revenue growth. In our base-case 2020 scenario, S&P 500 earnings will grow despite accelerating wage growth. Multiples And The Monetary Policy Cycle Although the S&P 500’s forward multiple is already elevated (Chart 7), the historical relationship between monetary policy and equity multiples argues that re-rating is more likely than de-rating going forward. We divide the fed funds rate cycle (Chart 8) into four phases based on the direction of the fed funds rate (higher or lower) and the state of monetary policy (easy or tight). We are currently in Phase IV, when the Fed has most recently eased policy while policy settings were already accommodative. If margins have finally peaked, multiple expansion will have to assume a bigger role in supporting the bull market. Chart 7Elevated But Not Worrisome

Elevated But Not Worrisome

Elevated But Not Worrisome

Chart 8The Fed Funds Rate Cycle

The Conventional Wisdom

The Conventional Wisdom

Since consensus earnings estimates began to be compiled in 1979, forward multiples have shrunk when the Fed hikes rates and expanded when it cuts them (Table 1). The empirical results align with intuition and arithmetic: investors should become stingier when the rate used to discount future earnings rises, and more generous when that rate falls. While we believe that the mid-cycle rate cuts are finished and that the fed funds rate will fall no further over the rest of this bull market, continued multiple expansion does not require continued rate cuts. Phase IV usually ends with an extended stretch when the Fed holds the funds rate at its trough level, but forward multiples do not peak until the final stages of the phase. Making the intuition-and-arithmetic statement more exact, investors become more generous when rates fall, and remain that way until a rate hike is a sure bet. Table 1A Consistent Inverse Relationship

The Conventional Wisdom

The Conventional Wisdom

Away from the last two Phase IVs, when the Fed cut rates in response to the duress issuing from the end of the dot-com mania and the financial crisis, re-rating gains have been significantly larger. Table 2 details the changes in multiples in each Phase IV episode over the last 40 years. Away from the grinding de-rating following the dot-com bust, and the slow re-rating accompanying the tepid post-crisis recovery, multiples have expanded at better than a 17% annualized rate. Voluntary cuts like last summer’s, made when policy is already easy, independent of the imperative to nurse a post-crisis economy back to health, have been awfully good for investors. Table 2Voluntary Cuts Turbocharge Multiples

The Conventional Wisdom

The Conventional Wisdom

There have been only two instances when the starting multiple has been as high as it was at the start of the latest run of rate cuts. As noted above, conditions in the spring of 2001, when the NASDAQ was a year into its eventual two-and-a-half-year slide, and a recession had just begun, bear little resemblance to conditions today. The fall of 1998, when the Fed delivered a rapid-fire 75 basis points of easing to protect the economy from the potential ramifications of Long Term Capital Management’s failure, looks a lot more like last summer. It is not our base case that the latest round of insurance cuts will push forward multiples to dot-com levels, but they do have scope to expand. The Inflation Timetable It remains our high-conviction view that inflation expectations will not return to the Fed’s target levels quickly. Their path has seemed to provide a nearly perfect real-life case study supporting the adaptive expectations framework, which posits that the recent past exerts a powerful influence on near-term expectations about the future. Inflation is way down the list of investors’ concerns because it has been dormant ever since the crisis, just as it was in the mid-‘60s once memories of high postwar inflation had faded. It conversely remained an acute fear for more than a decade after the Volcker Fed turned the tide in the early ‘80s (Chart 9). Multiples have really surged when the Fed has provided discretionary accommodation outside of periods of distress. The slow but meaningful rise in the trimmed mean PCE (Chart 10, top panel) and CPI series3 (Chart 10, bottom panel) should pull core PCE and core CPI higher over time. In the near term, however, the absence of upward momentum in several leading inflation indicators will likely stretch “over time” beyond the first half of the year, if not the whole year. As tight as the labor market is, unit labor costs have not been able to break out of the range that’s contained them for the last five years (Chart 11, top panel); the New York Fed’s Underlying Inflation Gauge has pulled a disappearing act after a seemingly decisive breakout in mid-2018 (Chart 11, middle panel); and the share of small businesses planning price increases has come off the late 2018 boil (Chart 11, bottom panel). Chart 9Recency Bias In Action

Recency Bias In Action

Recency Bias In Action

Chart 10Inflation's Not Dead, ...

Inflation's Not Dead, ...

Inflation's Not Dead, ...

Chart 11... But It's Still Hibernating

... But It's Still Hibernating

... But It's Still Hibernating

Investment Implications We spent the holidays reading up on the history of strikes in the United States and believe a shift in the balance of negotiating power from management to labor may be stirring, as a two-part Special Report will soon explore. Such a shift would render wages much more sensitive to a lack of labor market slack. Upward wage pressure could then filter into consumer prices either via a cost-push or demand-pull framework, as corporations either seek to defend margins from higher input costs or try to implement opportunistic price hikes. Cost-push or demand-pull, many investors seem to be dismissing the potential for an inflation revival, especially the ones we met in northern California, where the deeply held consensus view asserts that looming job destruction from artificial intelligence makes broad wage growth all but impossible. Inflation is not an immediate concern, but we expect it will ultimately spell the end of the bull market and the expansion. Allocating a generous share of long-maturity Treasury exposures to TIPS is an excellent way to protect a portfolio against its eventual re-emergence. We advise investors to maintain at least an equal weight allocation to equities to profit from our view that ongoing multiple expansion will surprise to the upside. Risk-friendly positioning remains appropriate, as long as intensifying US-Iran tensions or other geopolitical conflicts don’t negate the positive impact of reflationary monetary policy. Doug Peta, CFA Chief US Investment Strategist dougp@bcaresearch.com Footnotes 1 The ten buy- and sell-side strategists surveyed in Barron’s 2020 Outlook, published December 16th, called for an average gain of 4%. 2 Please see the October 2012 BCA Special Report, “Are US Corporate Profit Margins Really All That High?” available at www.bcaresearch.com. 3 Trimmed-mean inflation series operate like figure skating judging in the Olympics – the top and bottom readings are thrown out, and the mean is calculated from the remaining scores.

Feature Recommended Allocation

Monthly Portfolio Update: Counting The Milestones

Monthly Portfolio Update: Counting The Milestones

Since BCA published its 2020 Outlook,1 and the December GAA Monthly Portfolio Update,2 nothing has happened to make us fundamentally change our views. We see the global manufacturing cycle rebounding over the coming quarters, but major central banks remaining dovish. This combination of accelerating growth and easy monetary policy should be positive for risk assets. We accordingly continue to recommend an overweight on equities versus bonds, prefer the more cyclical euro zone and EM equity markets over the US, and selectively like credit (particularly the riskier end of the US junk bond universe). In the 2020 Outlook, we laid out a series of milestones that would indicate how our scenario is playing out: whether we need to reconsider it, or whether we should be adding further to risk (Table 1). Here is how those milestones are progressing. Table 1Milestones For The 2020 Outlook

Monthly Portfolio Update: Counting The Milestones

Monthly Portfolio Update: Counting The Milestones

Chinese growth. Total Social Financing picked up in November (CNY1.75 trillion versus CNY619 billion the previous month) and the most recent hard data (notably retail sales and industrial production) showed improvement. But the momentum of credit creation and activity generally remain weak (Chart 1). We expect that Chinese growth will begin to accelerate in early 2020, due to the lagged effect of monetary stimulus in the first half of last year, and easier fiscal policy. Moreover, December’s annual Central Economic Work Conference pointed to greater government emphasis on growth stability.3 The clampdown on shadow banking also seems to be easing (Chart 2). However, we need to see further signs of Chinese growth accelerating before, for example, we become more bullish on Emerging Markets and commodities. Chart 1Chinese Credit And Activity Remain Weak

Chinese Credit And Activity Remain Weak

Chinese Credit And Activity Remain Weak

Chart 2Clampdown On Shadow Banking Easing?

Clampdown On Shadow Banking Easing?

Clampdown On Shadow Banking Easing?

Trade war. The last-minute agreement to cancel the December 15 rise in US tariffs on Chinese imports represents the “ceasefire” we expected, rather than “phase one” of a more profound agreement. It is still unclear whether previous tariffs will be rolled back (Chart 3). China’s supposed promise to increase imports of US agricultural products from $10 billion a year to $40 billion-$50 billion seems unrealistic. Progress on more fundamental topics such as China’s subsidies for state-owned companies seems far off. For now, President Trump has done enough to minimize the negative impact on the US economy in an election year. But there remains a possibility that trade war reemerges as a risk during 2020. Chart 3How Far The Rollback?

How Far The Rollback?

How Far The Rollback?

Progress against these milestones suggests that our current asset allocation recommendation structure – moderately risk-on, but with hedges against downside risk – is appropriate for now. Global growth. Data confirming the rebound in the manufacturing cycle remain mixed. Economic surprises have generally been positive in the euro zone, but have slipped in the US and Japan, and remain soft in the Emerging Markets (Chart 4). In Germany, the manufacturing PMI slipped back to 43.7 in December, but the Ifo and ZEW surveys both rebounded (Chart 5). There is, however, still little sign that the weakness in manufacturing is spilling over into consumption and services. In Germany, unemployment remains at a record low and wages are strong. In the US, wage growth continues to trend up, and there is no indication in the weekly initial claims data that companies are starting to lay off workers at more than the seasonally normal pace (Chart 6). Market indicators of the cycle are also showing some positive signs. Among commodities, the price of copper – the most cyclical metal – has begun to rise. Chinese cyclical stocks are outperforming defensives. But the US dollar has not yet showed any significant depreciation (Chart 7). Chart 4Economic Surprises Mixed

Economic Surprises Mixed

Economic Surprises Mixed

Chart 5Germany Showing Signs Of Bottoming

Germany Showing Signs Of Bottoming

Germany Showing Signs Of Bottoming

Chart 6No Problems In The Labor Market

No Signs Of Weakening Labor Market No Problems In The Labor Market

No Signs Of Weakening Labor Market No Problems In The Labor Market

Chart 7Some Positive Signs From The Markets

Some Positive Signs From The Markets

Some Positive Signs From The Markets

US politics. President Trump’s approval rating has picked up slightly – we warned that its slipping might cause him to get aggressive on trade or foreign policy (Chart 8). Markets might worry at the possibility of “President Warren” given her focus on increased regulation of industries such as finance, energy, and technology. But she has fallen a little in the polls. Even in liberal California (where the primary will be unusually early next year – March 3), she is only level with Biden and Sanders in opinion polls. Our geopolitical strategists see US politics as one of the key geopolitical risks this year,4 but the risk seems subdued for now. Chart 8Trump’s Approval Rating Stable To Rising

Monthly Portfolio Update: Counting The Milestones

Monthly Portfolio Update: Counting The Milestones

Fed tightening. Expansions usually end when inflation rises, either causing the Fed to raise rates to choke it off, or with the Fed ignoring the inflation and allowing debt and asset bubbles to form. Any signs, therefore, that inflation, or inflation expectations, are rising would signal that we are truly in the “end game”. For now, there are no such signs. US inflation is likely to soften over the next six months, as a result of the economic slowdown and strong dollar. And TIPS breakevens imply the market believes the Fed will miss its inflation target by an average of 80-90 BPs a year over the next decade (Chart 9). The Fed is likely to sound very dovish over the coming year. The review of its monetary policy framework, probably to be announced in July, may result in some sort of “catch-up” policy: under this, if inflation undershoots the Fed’s target, the target automatically rises the following year.5 Its efforts to support the repo market, including short-term Treasury securities purchases of $60 billion a month, will increase the Fed’s balance-sheet, and represent a “mini-QE” (Chart 10). The Fed is likely to be reluctant to turn more hawkish ahead of the presidential election. These dovish moves – and continued accommodative policies from the ECB and Bank of Japan – mean that monetary policy will be supportive for risk assets throughout 2020. Chart 9Inflation Remains Subdued

Inflation Expectations Driven By Oil Inflation Remains Subdued

Inflation Expectations Driven By Oil Inflation Remains Subdued

These milestones suggest, therefore, that our current asset allocation recommendation structure – moderately risk-on, but with hedges (long cash and gold) against downside risk – is appropriate for now. Chart 10A "Mini-QE"?

A Mini-"QE"?

A Mini-"QE"?

Equities: We shifted last month to an underweight on US equities, with an overweight on the euro zone, and neutral on Emerging Markets. The US tends to underperform during upswings in the global manufacturing cycle (Chart 11). Europe looks attractive because of its heavy weighting in sectors we like such as Financials, Autos and Capital Goods. Europe’s returns will also be boosted by the appreciation in the euro and pound that we expect (our equity recommendations assume no currency hedging). For EM, we would turn more positive if we saw a clear pickup in Chinese credit and economic growth. Chart 11US Underperforms When Growth Picks Up

US Underperforms When Growth Picks

US Underperforms When Growth Picks

Chart 12Fed Won't Cut As The Market Expects

Fed Won't Cut As The Market Expects

Fed Won't Cut As The Market Expects

Fixed Income: Our positive view on global growth implies that long-term rates will rise. We see the US Treasury 10-year yield reaching 2.5% by mid-2020. The market still expects the Fed to cut rates once over the next 12 months. If it stays on hold, as we expect, that slight hawkish surprise would be compatible with a moderate rise in rates (Chart 12). Core euro zone rates might rise by a little less, perhaps by 30-40 BPs, and Japanese government bond yields by 10-15 BPs. We, therefore, continue to recommend a small underweight on duration and an overweight on TIPS which look particularly cheaply valued. Within credit, our preferences are for European investment grade (not as expensive as in the US, and with the ECB buying corporate debt again) and the lower end of the US junk-bond universe (since CCC-rated bonds missed out on 2019’s rally). In a rebounding global economy, the US dollar should depreciate, particularly since it looks somewhat over-valued, and with speculative positions long the dollar. Currencies: In a rebounding global economy, the US dollar should depreciate, particularly since it looks somewhat over-valued (Chart 13), and with speculative positions long the dollar (Chart 14). But its performance is likely to vary depending on the currency pair. Our FX strategists expect the dollar to weaken to 1.18 against the euro and 1.40 against the pound over the next 12 months, and even more against currencies such as the NOK, SEK, and AUD.6 But the dollar is likely to strengthen against the yen (an even more counter-cyclical currency) and against currencies in EM, where central banks will continue to cut rates and inject liquidity aggressively to support their economies. Chart 13Dollar Looks Expensive...

Dollar Looks Expensive...

Dollar Looks Expensive...

Chart 14...And Speculators Are Long

Monthly Portfolio Update: Counting The Milestones

Monthly Portfolio Update: Counting The Milestones

Commodities: Supply in the oil market remains tight, with OPEC deepening its production cuts to 1.7 million barrels/day. The crude oil price was held down in 2019 by weakening demand, which should recover along with the cycle in 2020 (Chart 15). Our energy strategists expect Brent to average $67 a barrel in 2020 (compared to $66 now), with WTI $4 lower. Metal prices could rise in 2020 as Chinese growth recovers and the US dollar depreciates – the two most important factors that drive them (Chart 16). Given the uncertainty over both, we remain neutral for now, but would turn more positive (including on commodity-related assets, such as Australian or EM equities) if we see clear signs of their moving in the right direction. We see gold as a good downside hedge in a world of ultra-low interest rates, especially since central banks may allow inflation to overshoot over the coming years. Chart 15Supply/Demand Balance Points To Higher Oil Price

Markets Will Tighten In 2020 Supply/Demand Balance Points To Higher Oil Price

Markets Will Tighten In 2020 Supply/Demand Balance Points To Higher Oil Price

Chart 16Metals Are Driven By The Dollar And China

Metals Are Driven By The Dollar And China

Metals Are Driven By The Dollar And China

Garry Evans, Senior Vice President Chief Global Asset Allocation Strategist garry@bcaresearch.com Footnotes 1 Please see "Outlook 2020: Heading Into The End Game," dated 22 November 2019, available at bca.bcaresearch.com. 2 Please see "GAA Monthly Portfolio Update: How To Position For The End Game," dated 2 December 2019, available at gaa.bcaresearch.com. 3 Please see China Investment Strategy Weekly Report, "A Year-End Tactical Upgrade," dated 18 December 2019, available at cis.bcaresearch.com 4 Please see Geopolitical Strategy "Strategic Outlook: 2020 Key Views: The Anarchic Society," dated 6 December 2019, available at gps.bcaresearch.com 5 For example, if the Fed's inflation target is 2% but inflation is only 1.7% one year, the target would automatically rise to 2.3% the following year. 6 Please see Foreign Exchange Strategy, "2020 Key Views: Top Trade Ideas," dated December 13, 2019, available at fes.bcaresearch.com GAA Asset Allocation

As 2019 draws to a close, we thank you for your ongoing readership and support. We wish you and your loved ones a happy holiday season and all the best for a healthy and prosperous 2020. Highlights We explore the principal risks to our optimistic 2020 outlook. Trade and the 2020 US Presidential election remain potential landmines. A stronger dollar would tighten global financial conditions and be deflationary. Credit market tremors would end buybacks. Stronger-than-expected inflation would force a cycle-ending Federal Reserve tightening. Weaker-than-expected inflation would first allow for larger bubbles to form at the expense of a more painful recession and deeper a bear market down the road. Hedging against those risks warrants overweighting cash, TIPs and gold. Feature Chart I-1Timing is Ripe For A Recovery

Timing is Ripe For A Recovery

Timing is Ripe For A Recovery

As always, this year’s visit from Ms. and Mr. X was thought-provoking and generated diverse investment ideas.1 While we did not share Mr. X’s fears, his caution may be justified because an aging business cycle, elevated equity multiples and extremely expensive government bonds do not mesh with pro-risk portfolio positioning. With this in mind, we will explore the greatest risks to our positive market outlook, which include politics, the US dollar, problems in the credit market, a quicker resumption of inflation and lower inflation. The Central Scenario To understand how these five risks affect our central thesis, let’s review the key views and themes that underpin our bullish outlook. BCA expects global economic activity to recover in 2020. First, the global inventory contraction is advanced, which increases the chance that the manufacturing cycle will track its usual pattern of an 18-month decline followed by an 18-month acceleration (Chart I-1). Secondly, Chinese policymakers are putting a floor under domestic economic activity and the stabilization in credit growth and the climbing fiscal impulse already augur well for global growth (Chart I-2). Thirdly, global liquidity is in a major upswing, thanks to easing by central banks around the world (Chart I-3). Finally, the trade détente between the US and China agreed last week reduces the odds of a destructive trade war. Chart I-2China's Policy Turnaround

China's Policy Turnaround

China's Policy Turnaround

Chart I-3Easing Abound!

Easing Abound!

Easing Abound!