Monetary

Highlights The currency market is bifurcated in terms of shorter-term expectations versus longer-term factors. The Swedish krona, Norwegian krone, and British pound are solid long-term buys, but could remain very volatile in the short term. We continue to focus on the crosses rather than outright dollar bets. Remain long SEK/NZD, GBP/JPY, and NOK/SEK. Tighten stops on long GBP/JPY to protect profits. EUR/SEK should top out once global growth improves. Sell the gold/silver ratio at 90, as recommended in last week’s report.1 Feature Chart I-1One Way Street Since 2018

One Way Street Since 2018

One Way Street Since 2018

Of all the G10 currencies we follow, the Swedish krona is probably the one that is the most perplexing. The Riksbank is one of the few central banks to have raised rates this year, but the krona remains the weakest G10 currency. Admittedly, the performance of the Swedish manufacturing sector has been dismal, and was especially so in September, but this has not been a story specific to Sweden alone. The euro area, which is also experiencing a deep manufacturing recession, has seen better currency performance despite a more dovish European Central Bank (ECB). The underperformance of the krona begs the question of whether it signals a much prolonged global manufacturing recession, or is indicative of something more endogenous to Sweden. Put another way, has the driver of USD/SEK (and even USD/NOK) strength been an appreciating dollar, or more domestic factors (Chart I-1)? And if it is the latter, what are the important signposts to look out for should a turnaround be around the corner? The Soft Versus Hard Data Debate The big question for Sweden is whether the manufacturing sector is just in a volatile bottoming process, or about to contract much further. Industrial production is currently growing at 4% year-over-year, but the signal from the soft data is that it should be contracting in the double digits (Chart I-2, top panel). As such there is either a big disconnect between the perception of investors and reality, or we are on the verge of a much deeper manufacturing slump. Exchange rates tend to be extremely fluid in discounting a wide swath of economic data, and in the case of Sweden, in discounting the outcome for global growth. However, with EUR/SEK at 10.8 and USD/SEK at 9.7 – the latter well above its 2008 highs – it is fair to assume that anything other than a deep recession will justify a stronger SEK. One of the more consistent ratios in calling a bottom in the Swedish manufacturing sector in particular (and that of the Eurozone in general) is the manufacturing new orders-to-inventories ratio (Chart I-2, bottom panel). The tick down in September was disconcerting. However, unlike the manufacturing PMI, this ratio is not hitting new lows, tentative evidence that we might be in a volatile bottoming process rather than a protracted slump. The last time we encountered such a divergence was in 2011/2012, at the height of the European debt crisis; in that instance, Swedish hard data ended up sending the right signal for the overall economy. The deterioration in the manufacturing sector has yet to hit domestic consumption in general or the labor market in particular. The deterioration in the manufacturing sector has yet to hit domestic consumption in general or the labor market in particular. The import component of the PMI index remains well above that of exports. Meanwhile, the employment component of the PMI index began to stabilize around the middle of this year, meaning employment growth should bottom at around 1% or so (Chart I-3). Swedish exports are higher up the manufacturing food chain than in most other developed economies, and autos are quite important. But so far, the Swedish economy has weathered the auto slowdown quite well, with production still clocking in at 7% per year. Chart I-2Soft Data Is Much Worse

Soft Data Is Much Worse

Soft Data Is Much Worse

Chart I-3Domestic Demand Is Holding Up Well

Domestic Demand Is Holding Up Well

Domestic Demand Is Holding Up Well

The tick up in the Swedish unemployment rate is problematic, but we do not believe it constitutes a major change in labor market dynamics. Sweden has a long history of higher openness toward asylum seekers and refugees than many other European countries. The Syrian crisis a couple of years ago led to an exceptional surge, where the number of asylum seekers skyrocketed to over 150,000 or almost 1.5% of the total population (Chart I-4). Historically, immigration has provided a big labor dividend to Sweden, allowing growth to outpace both the U.S. and the euro area. But this has also been a source of frictional unemployment, as new migrants integrate into the labor force. Chart I-4A New Pool Of Labor That Has To Be Integrated

A New Pool Of Labor That Has To Be Integrated

A New Pool Of Labor That Has To Be Integrated

Foreign-born workers now constitute about 20% of the total population, a big portion of which need to learn a new language and adopt new skills (Chart I-5A). This growth dividend will be reaped for many years to come. Integration is a politically contentious issue, and so the highly restrictive asylum and reunification law adopted in mid-2016 probably means the immigration boom is behind us. The rise of the anti-immigration Sweden Democrats in the September 2018 elections is a case in point. However, the pivot of the democratic population towards the right has been a global phenomenon, and so is not as negative for Sweden on a relative basis. All that to say, compared to most developed nations, Sweden still enjoys a relatively positive demographic outlook (Chart I-5B). Chart I-5AA Huge Labor Dividend

A Huge Labor Dividend

A Huge Labor Dividend

Chart I-5BNo Apparent Demographic Cliff

No Apparent Demographic Cliff

No Apparent Demographic Cliff

The inflow of migrants has a mixed impact on inflation. While there is downward pressure on wages, due to an increase in the share of employment that pays lower wages, there is still upward pressure on housing and consumption in response to the increased number of workers. This comes on top of a fiscal boost as the government spends more on social services. Meanwhile, the unemployment rate among foreign-born people is around 15%. This means that the Phillips curve is flat for the first few years, before it starts to steepen. But as the new labor force is finally absorbed into the economy, it should start to generate meaningful wage pressures. The Riksbank clearly understands these dynamics, which is why over the prior years, its stance has been dovish even when the Swedish economy has been holding up well. Interest rates were cut to negative territory in 2015 and held at -0.5% (lower than the ECB policy rate) all through the global recovery in 2016 and 2017. Quantitative easing has also been extended up until 2020, well ahead of the ECB’s renewed asset purchase program announcement. Both have tremendously eased monetary conditions in Sweden, including via a weaker currency. Going forward, there are a few key reasons to believe the path of least resistance for the krona is now up: A weak krona has typically helped the manufacturing sector with a lag of twelve months. A weak krona has typically helped the manufacturing sector with a lag of twelve months. Negative divergences only tend to happen ahead of deep recessions. Unless we are in that particular situation now, better demand for relatively cheaper Swedish goods (think Volvo versus BMW) should lead to a stronger krona (Chart I-6). Yes, the Riskbank has been conducting QE, but the pace of expansion in its balance sheet has been slowing in recent quarters. USD/SEK has tended to track relative balance sheet trends between the Riksbank and the Fed, but a gaping wedge has opened up in favor of the krona (Chart I-7). Meanwhile, with the Fed about to re-expand its balance sheet, this should also favor a stronger SEK versus the USD. Chart I-6Swedish Krona And Manufacturing

Swedish Krona And Manufacturing

Swedish Krona And Manufacturing

Chart I-7USD/SEK And Relative Balance Sheets

USD/SEK And Relative Balance Sheets

USD/SEK And Relative Balance Sheets

The Swedish housing market is becoming a thorn in the Riksbank’s side. When negative rates were introduced in 2015, growth in house prices exploded to the tune of 15% year-on-year (Chart I-8). More recently, a curb on migration has allowed a cooling of sorts, but Swedish household leverage remains very elevated. With the memory of the 1990s housing crisis still fresh in their minds, this is making the Riksbank quite uncomfortable with its current policy stance. The carry cost is lower from being short NZD compared to being short the U.S. dollar. Our bias is that though Governor Stefan Ingves prefers to renormalize policy as quickly as possible, given that he is managing a small-open economy with trade a whopping 45% of GDP, but is held hostage to external conditions. The SEK is the cheapest currency in the G10 universe, and could bounce sharply on even the softest evidence indicating global growth has bottomed. Furthermore, rising global growth will tighten resource utilization, which should begin to boost underlying inflationary pressures in Sweden (Chart I-9) Chart I-8House Prices In Sweden##br## Are Bubbly

House Prices In Sweden Are Bubbly

House Prices In Sweden Are Bubbly

Chart I-9Resource Utilization And Inflation In Sweden

Resource Utilization And Inflation In Sweden

Resource Utilization And Inflation In Sweden

In terms of SEK trading strategy, USD/SEK and NZD/SEK tend to be highly correlated; since the SEK has a higher beta to global growth than the kiwi (Sweden exports 45% of its GDP versus 27% for New Zealand). On a relative basis, the Swedish economy appears to have bottomed relative to that of the U.S., making the SEK/NZD an attractive way to play USD/SEK downside. Meanwhile, the carry cost is lower from being short NZD compared to being short the U.S. dollar (Chart I-10). As for EUR/SEK, the cross could consolidate at current levels before heading lower but will ultimately peak once global growth reaccelerates. Chart I-10Remain Long SEK/NZD

Remain Long SEK/NZD

Remain Long SEK/NZD

Bottom Line: We remain long the SEK/NZD as a relative value play, but the true upside lies in the SEK/USD cross. Our bias is that SEK weakness has been driven by the market’s focus on disappointing soft data, while hard data remains relatively resilient. Once it becomes clearer that the global growth environment is not as precarious as the surveys suggest, the krona could bounce sharply. Housekeeping Our long GBP/JPY position hit 5% this week. We are tightening stops to 138 in order to protect profits. We were also stopped out of short EUR/NOK for a 2% loss. We are standing aside for now. EUR/NOK is now trading above 2008 recession levels, which is only justifiable by a prolonged growth recession, but risk management warrants patience for now. Stay tuned. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, titled “On Money Velocity, EUR/USD And Silver,” dated October 11, 2019, available at fes.bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been soft: Retail sales contracted by 0.3% month-on-month in September. Industrial production fell by 0.4% month-on-month. Both export and import prices fell by 1.6% year-on-year in September. Michigan Consumer Sentiment Index grew to 96 in October, up from 93.2 in the previous month. NY Empire State Manufacturing Index increased to 4 in October, up from 2 in September. Building permits and housing starts both fell by 2.7% and 9.4% month-on-month in September, but the housing recovery remains intact. Initial jobless claims increased to 214K for the week ended Oct 11th. The DXY index depreciated by 0.7% this week. The latest Beige Book summarized that the U.S. economy expanded at a slight-to-modest pace. The slowdown in the manufacturing sector remains the biggest risk to the economy, while trade tensions continue to weigh on business sentiment and capex intensions. The most recent “entente” in trade discussions might represent a pivotal shift from heightened uncertainty that has prevailed throughout the summer. Report Links: On Money Velocity, EUR/USD And Silver - October 11, 2019 Preserving Capital During Riot Points - September 6, 2019 Has The Currency Landscape Shifted? - August 16, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area remain subdued: Headline inflation fell to 0.8% year-on-year in September, the slowest in nearly three years. Core inflation however, increased to 1% year-on-year. Industrial production in the euro area continued to contract, by 2.8% year-on-year in August. The ZEW sentiment in the euro area fell further to -23.5 in October, however this is well above expectations of -33. The ZEW sentiment for Germany also fell to -22.8 in October. It is worth noting that expectations continue to improve relative to the current situation. The trade balance in the euro area improved to €20.3 billion in August, up from the downward-revised €17.5 billion in July. However, this is mostly due to a contraction in imports. EUR/USD rose by 0.9% this week, in part helped by broad dollar weakness. The trade dynamics in the euro area remain worrisome: exports fell by 2.2% year-on-year in August, while imports plunged by 4.1% year-on-year. Notably, year-to-date, the EU’s trade surplus with U.S. grew to €103 billion, up from €91 billion a year earlier, while the trade deficit with China widened further to €127 billion from €116 billion. Report Links: On Money Velocity, EUR/USD And Silver - October 11, 2019 A Few Trade Ideas - Sept. 27, 2019 Battle Of The Central Banks - June 21, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan continue to disappoint: Industrial production fell by 4.7% year-on-year in August. Capacity utilization decreased by 2.9% month-on-month in August. The Japanese yen fell by 0.8% against the U.S. dollar this week. Kuroda has again emphasized that the BoJ will not hesitate to act if economic developments continue to deteriorate. On the other hand, while the Fed and the ECB are both on course to expand their balance sheets through asset purchases, it is an open question as to how much more the BoJ can do, beyond yield curve control. We remain long the yen in anticipation that it will require a “Lehman moment” for the BoJ to act aggressively. Report Links: A Few Trade Ideas - Sept. 27, 2019 Has The Currency Landscape Shifted? - August 16, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been mostly negative: The ILO unemployment rate slightly increased to 3.9% in August. Average earnings quarterly growth slowed to 3.8%, however this was above expectations of 3.7%. The Retail price index grew by 2.4% year-on-year in September, a slowdown from 2.6% in the previous month. Headline inflation was unchanged at 1.7% year-on-year in September, while core inflation jumped to 1.7% from 1.5%. Retail sales grew by 3.1% year-on-year in September, up from 2.6% in the previous month. GBP/USD surged by 3.3% this week on optimism towards the European Council Summit on Brexit. From a valuation perspective, the pound is trading at a large discount to its fair value. Should positive Brexit news continue to hit the headlines, the pound could continue to soar. We are long GBP/JPY, which is above 5% in the money. Tighten stop to 138. Report Links: A Few Trade Ideas - Sept. 27, 2019 United Kingdon: Cyclical Slowdown Or Structural Malaise? - Sept. 20, 2019 Battle Of The Central Banks - June 21, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been modest: NAB business confidence fell further to -2, while conditions improved to 1 in Q3. On the labor market front, the unemployment rate fell further to 5.2% in September. 14.7K jobs were created, consisting of 26.2K full-time jobs and a loss of 11.4K part-time jobs. AUD/USD increased by 0.4% this week. RBA minutes were released earlier this week. Interestingly, it presents a sharp debate about the effects of low rates. On the one hand, lower rates have been theoretically justified to achieve full employment and the inflation target. On the other hand, some RBA members fear that low rates could fuel already inflated house prices. The probability for another rate cut has thus decreased post RBA minutes. Report Links: A Contrarian View On The Australian Dollar - May 24, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been negative: Visitor arrivals increased by 1.8% year-on-year in August, slightly down from 2% in the previous month. Headline inflation slowed to 1.5% year-on-year in Q3. NZD/USD has been more or less flat this week. Closely tied to global growth, the New Zealand dollar has been fluctuating with the ebb and flow of the U.S.-China trade headlines. The two countries have agreed on a partial deal last week, however the details remain vague. While the kiwi is a high beta currency, it should unerperform at the crosses. We continue to play the kiwi weakness through the Aussie dollar and the Swedish Krona. Report Links: USD/CNY And Market Turbulence - August 9, 2019 Where To Next For The U.S. Dollar? - June 7, 2019 Not Out Of The Woods Yet - April 5, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been relatively strong: The unemployment rate decreased further to 5.5% in September. Moreover, average hourly wages continued to grow by 4.3% year-on-year, up from 3.8% in the previous month. Lastly, 53.7K jobs were created in September, well above expectations of 10K. Both headline and core inflation were unchanged at 1.9% year-on-year in September. The Canadian dollar has appreciated by 1% against the U.S. dollar, on the back of the positive employment data last Friday. All eyes are on the federal election this month, which could be crucial for the future of the Canadian energy sector and environment policies. Report Links: Preserving Capital During Riot Points - September 6, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been positive: The trade surplus (excluding precious metals) widened sharply to CHF 2.88 billion in September. Notably, Swiss exports grew by 8.2% month-on-month to CHF 20.3 billion, led by higher sales of chemical and pharmaceutical products. Swiss imports slightly dropped by 1.4% month-on-month to CHF 17.4 billion. Producer and import prices continued to fall by 2% year-on-year in September. USD/CHF fell by 1% this week. The Swiss franc will continue to fight a tug-of-war between being a defensive currency, but a tool of manipulation by the SNB. Our guestimate is that EUR/CHF 1.06 is an ultimate stress point. Global portfolios should hold the Swiss franc as insurance, for the simple reason that the currency is a structural outperformer. Report Links: Notes On The SNB - October 4, 2019 What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been depressed: The trade balance shifted to a deficit of NOK 1.2 billion in September. That’s a decrease of NOK 24 billion year-on-year. The Norwegian krone has depreciated by nearly 1% against the U.S. dollar this week. Energy prices remain subdued over the past few weeks. Moreover, the Norwegian trade balance has shifted to a deficit for the first time since November 2017. Exports plunged by 19.5% year-on-year, due to lower sales of energy products, while imports jumped by 12.9% year-on-year. The message is clear – Norway continues to hold up well domestically, but dependence on petroleum exports is introducing volatility into any growth forecasts. BCA has lowered its oil price projections for 2019, which has dampened the appeal of the Norwegian Krone. Stay tuned. Report Links: A Few Trade Ideas - Sept. 27, 2019 Portfolio Tweaks Into Thin Summer Trading - July 5, 2019 On Gold, Oil And Cryptocurrencies - June 28, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been neutral: The unemployment rate was unchanged at 7.1% in September. USD/SEK fell by 1.1% this week. As the worst performing G-10 currency this year, the Swedish krona is now trading at a large discount to its fair value. Please refer to our front section this week which presents an in-depth analysis on the Swedish economy and the krona. Report Links: Where To Next For The U.S. Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 201 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights The interim “phase 1” trade agreement reached last week represents a significant step forward towards reaching a détente in the China-U.S. trade war. Regardless of what happens next in the Brexit negotiations, a hard exit will be avoided. Stay long the pound. U.S. earnings growth is likely to be flat in the third quarter, in contrast to bottom-up expectations of a year-over-year decline. Earnings growth should pick up as global growth reaccelerates by year end. Stronger global growth will put downward pressure on the U.S. dollar. Remain overweight global equities relative to bonds over a 12-month horizon. Cyclical stocks should start to outperform defensives. Financials will finally have their day in the sun. Favorable Tradewinds In our Fourth Quarter Strategy Outlook published two weeks ago, we argued that global equities had entered a “show me” phase, meaning that tangible evidence of a de-escalation in the trade war and a recovery in global growth would be necessary for stock indices to move higher.1 We received some positive news on the trade front last Friday. In exchange for suspending the planned October 15th hike in tariffs from 25% to 30% on $250 billion of Chinese imports, China agreed to purchase $40-$50 billion of U.S. agricultural products per year, improve market access for U.S. financial services companies, and enhance the transparency of currency management. Admittedly, there is still much to be done. The text of the agreement has yet to be finalized. Both sides are aiming to conclude the deal by the time of the APEC summit in Santiago, Chile on November 16-17. Considering that a number of key issues remain unresolved, including what sort of enforcement and resolution mechanisms will be included in the deal, further delays or even a breakdown in the talks are possible. The interim deal agreed upon last week also punts the thorny issue of how to handle intellectual property protections to a “phase 2” of the negotiations slated to begin soon after “phase 1” is wrapped up. According to the independent and bipartisan U.S. Commission on the Theft of American Intellectual Property, U.S. producers lose between $225 and $600 billion annually from IP theft.2 China has often been considered among the worst offenders. Given the importance of the IP issue, meaningful progress will be necessary to ensure that tariffs of 15% on about $160 billion of Chinese imports are not introduced on December 15th. Trump Wants A Deal Despite the many hurdles that remain, last week’s developments significantly raise the prospects of a détente in the 18 month-long trade war. As a self-professed “master negotiator,” President Trump has put his credibility on the line by describing the negotiations as a “love fest,” calling the trade pact “the greatest and biggest deal ever made for our Great Patriot Farmers,” and saying that he has “little doubt” that a final agreement will be reached. Just as he did with NAFTA’s successor USMCA – a deal that is substantively similar to the one it replaced – Trump is likely to shift into marketing mode, trumpeting the “tremendous” new deal that he has negotiated on behalf of the American people. From a political point of view, this makes perfect sense. Rightly or wrongly, President Trump gets better marks from voters on his handling of the economy than anything else (Chart 1). A protracted trade war would undermine the U.S. economy, thereby hurting Trump’s re-election prospects. Chart 1Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

Kumbaya

Kumbaya

Chart 2Chinese Business Are Not Paying The Bulk Of The Tariffs

Kumbaya

Kumbaya

Notwithstanding his claims to the contrary, the evidence firmly suggests that U.S. consumers, rather than Chinese businesses, are paying the bulk of the tariffs. Chart 2 shows that U.S. import prices from China have barely declined, even as tariff rates on Chinese imports have risen. To the extent that the latest rounds of tariffs are focused on Chinese goods for which there is little U.S. or third-country competition, the ability of Chinese producers to pass on the cost of the tariffs will only increase. If all the tariff hikes that have been announced were implemented, the effective tariff rate on Chinese imports would rise from around 15% as of late August to as high as 25% in December (Chart 3). Such a tariff rate would reduce U.S. household disposable incomes by over $100 billion, wiping out most of the gains from the 2017 tax cuts. Trump can’t let the trade war reach this point. Chart 3Successive Rounds Of Tariffs Have Started To Add Up

Successive Rounds Of Tariffs Have Started To Add Up

Successive Rounds Of Tariffs Have Started To Add Up

Will China Play Hardball? One risk to a favorable resolution to the trade war is that China will increasingly see Trump as desperate to make a deal. This could lead the Chinese to take a hardline stance in the negotiations. While this risk cannot be dismissed, we would downplay it for three reasons: First, even though China’s exporters have been able to maintain some degree of pricing power during the trade war, trade volumes have still suffered, with exports to the U.S. down nearly 22% year-over-year in September. Second, as the crippling sanctions against ZTE have demonstrated, China remains highly dependent on U.S. technologies. This gives Trump a lot of leverage in the trade negotiations. Chart 4Who Will Win The 2020 Democratic Nomination?

Kumbaya

Kumbaya

Third, as Trump himself likes to say, China will find it easier to negotiate with him in his first term in office than in his second. Hoping that Trump would lose his re-election bid might have made sense for China a few months ago when Joe Biden was riding high in the polls; but now that Elizabeth Warren has emerged as the favorite to secure the Democratic nomination, that hope has been dashed (Chart 4). As we noted several weeks ago, China is likely to find Warren no less vexing on trade matters than Trump.3 All this suggests that China, just like Trump, will look for ways to cool trade tensions over the coming weeks. Brexit Breakthrough? As we go to press, the prospects for a Brexit deal have brightened. Although the details have yet to be released, the proposed deal would effectively put Northern Ireland in a veritable quantum superposition where it is both in the European common market and in the U.K. at the same time. This feat will be achieved by keeping Northern Ireland within the U.K. political jurisdiction but still aligned with EU regulatory standards. Negotiations could still go awry. Despite Prime Minister Boris Johnson’s assurance that he secured “a great new deal,” the Conservative’s coalition partner, the Northern Irish Democratic Unionist Party, is still withholding its support for the accord. Labour leader Jeremy Corbyn has also rejected the deal, saying that it is even worse than Theresa May’s originally proposed pact. Regardless of what transpires over the coming days, we continue to think that a hard Brexit will be avoided. Throughout the entire Brexit ordeal, we have argued that there was insufficient political support within the British ruling class for a no-deal Brexit. That conviction has only grown as polling data has revealed that an increased share of voters would choose to stay in the EU if another referendum were held (Chart 5). We have been long the pound versus the euro since August 3, 2017. The trade has gained 6.6% over this period. Investors should stick with this position. Based on real interest rate differentials, GBP/EUR should be trading near 1.30 rather than the current level of 1.16 (Chart 6). We expect the cross to move towards its fair value as hard Brexit risks diminish further. Chart 5Brexit Angst: A Case Of Bremorse

Brexit Angst: A Case Of Bremorse

Brexit Angst: A Case Of Bremorse

Chart 6Substantial Upside In The Pound

Substantial Upside In The Pound

Substantial Upside In The Pound

Global Growth Prospects Improving Chart 7Growth Slowdown Has Been More Pronounced In The Soft Data

Growth Slowdown Has Been More Pronounced In The Soft Data

Growth Slowdown Has Been More Pronounced In The Soft Data

Chart 8Manufacturing Output Rebounds Amid The ISM Slump

Manufacturing Output Rebounds Amid The ISM Slump

Manufacturing Output Rebounds Amid The ISM Slump

A détente in the trade war and a resolution to the Brexit saga should help support global growth. The weakness in the economic data has been much more pronounced in so-called “soft” measures such as business surveys than in “hard” measures such as industrial production (Chart 7). Notably, U.S. manufacturing output has stabilized over the past three months, even as the ISM manufacturing index has swooned (Chart 8). As sentiment rebounds, the soft data should improve. Global financial conditions have eased significantly over the past five months, thanks in large part to the dovish pivot by most central banks (Chart 9). The net number of central banks cutting rates generally leads the global manufacturing PMI by 6-to-9 months (Chart 10). In addition, the Fed’s decision to start buying Treasurys again will increase dollar liquidity, thus further contributing to looser financial conditions. Chart 9Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Chart 10The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

The Effects Of Easing Monetary Policy Should Soon Trickle Down To The Economy

Stepped-up Chinese stimulus should also help jumpstart global growth. Chinese money and credit growth both came in above expectations in September. The PBoC has been cutting reserve requirements, which has helped bring down interbank rates. Further cuts to the medium-term lending facility are likely over the remainder of this year. Changes in Chinese credit growth lead global growth by about nine months (Chart 11). Chart 11Chinese Credit Should Support The Recovery In Global Growth

Chinese Credit Should Support The Recovery In Global Growth

Chinese Credit Should Support The Recovery In Global Growth

Stay Overweight Global Equities While the road to finalizing a “phase 1” trade deal in time for the APEC summit is likely to be a bumpy one, we continue to reiterate our recommendation that investors overweight global stocks relative to bonds over a 12-month horizon. We expect to upgrade EM and European equities over the coming weeks once we see a bit more evidence that global growth is bottoming out. Ultimately, the trajectory of stocks will hinge on what happens to earnings. The U.S. earnings season began this week. As of last week, analysts expected S&P 500 EPS to decline by 4.6% in Q3 relative to the same quarter last year according to data compiled by FactSet. Keep in mind, however, that EPS growth has beaten estimates by around four percentage points since 2015 (Chart 12). Thus, a reasonable bet is that U.S. earnings will be flat this quarter, clearing a low bar of expectations. Chart 12Actual EPS Has Generally Beaten Estimates

Kumbaya

Kumbaya

Chart 13Earnings And Nominal GDP Growth Tend To Move In Lock-Step

Earnings And Nominal GDP Growth Tend To Move In Lock-Step

Earnings And Nominal GDP Growth Tend To Move In Lock-Step

The fact that 83% of the 63 S&P 500 companies that have reported earnings thus far have beaten estimates – better than the historic average of 64% – supports the view that current Q3 estimates are too dour. Looking out, earning growth should pick up as nominal GDP growth accelerates (Chart 13). European and EM equities generally outperform the global benchmark when global growth is speeding up (Chart 14). This is due to the more cyclical nature of their stock markets. In addition, as a countercyclical currency, the dollar tends to weaken in a faster growth environment. A weaker dollar disproportionately benefits cyclical stocks (Chart 15). Chart 14EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

Chart 15Cyclical Stocks Will Outperform If The Dollar Weakens

Cyclical Stocks Will Outperform If The Dollar Weakens

Cyclical Stocks Will Outperform If The Dollar Weakens

We would include financials in our definition of cyclical sectors. As global growth improves, long-term bond yields will increase at the margin. Since central banks are in no hurry to raise rates, yield curves will steepen. This will boost bank profits and share prices (Chart 16). Cyclical stocks are currently quite cheap compared to defensives (Chart 17). Likewise, non-U.S. equities are quite inexpensive compared to their U.S. peers, even if one adjusts for differences in sector composition across regions. While U.S. stocks trade at 17.5-times forward earnings, international stocks trade at a more attractive forward PE ratio of 13.7. The combination of higher earnings yields and lower interest rates abroad implies that the equity risk premium is roughly two percentage points higher outside the United States (Chart 18). Chart 16Steeper Yield Curves Will Benefit Financials

Steeper Yield Curves Will Benefit Financials

Steeper Yield Curves Will Benefit Financials

Chart 17Cyclical Stocks Are More Attractive Than Defensives

Cyclical Stocks Are More Attractive Than Defensives

Cyclical Stocks Are More Attractive Than Defensives

Chart 18The Equity Risk Premium Is Quite High, Especially Outside The U.S.

The Equity Risk Premium Is Quite High, Especially Outside The U.S.

The Equity Risk Premium Is Quite High, Especially Outside The U.S.

We expect to upgrade EM and European equities over the coming weeks once we see a bit more evidence that global growth is bottoming out. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1Please see Global Investment Strategy, “Fourth Quarter 2019 Strategy Outlook: A ‘Show Me’ Market,” dated October 4, 2019. 2 “Update to IP Commission Report: The Report of the Commission on the Theft of American Intellectual Property,” The National Bureau of Asian Research, 2017. 3Please see Global Investment Strategy Weekly Report, “Elizabeth Warren And The Markets,” dated September 13, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Kumbaya

Kumbaya

Strategic Recommendations Closed Trades

Highlights Duration & Fed: Our late-1990s & 2015/16 roadmap for the economy still holds, but risks are mounting. Despite the risks, we expect that trade tensions will calm enough for the economic data to improve during the next few months. The result will be one more Fed rate cut this month, followed by an extended on-hold period. Investors should keep portfolio duration low in that environment. Junk Quality Spreads: This year’s divergence between the Caa/Ba quality spread and the high-yield index spread is highly unusual, but has more to do with movements in Treasury yields and changing index duration than with broader concerns about corporate credit quality. Investment Grade Risk & Reward: We present a novel approach for assessing the risk/reward trade-off among investment grade corporate bond sectors. We note that Saudi Arabian and Mexican Sovereign bonds, Foreign Agency bonds and Conventional 30-year Agency MBS look particularly attractive in risk-adjusted terms. Feature Contagion? This publication has repeatedly pointed to the late-1990s and the 2015/16 periods as appropriate comparables for today’s global growth slowdown. That is, we expect that the current spate of weakness will stay confined within the manufacturing sector and will not spread into the broader economy, leading the U.S. into recession. This call is important from an investment perspective because it implies that the Fed is not currently engaged in an easing cycle that will bring the funds rate back to zero. Rather, we anticipate only three rate cuts this year (we’ve already seen two), followed by the eventual resumption of hikes. Bond yields will not make new lows in that environment. Chart 1Manufacturing Weakness Spreading?

Manufacturing Weakness Spreading?

Manufacturing Weakness Spreading?

Chart 2"Hard" Data Still Firm

"Hard" Data Still Firm

"Hard" Data Still Firm

But some data received this month challenge our economic narrative. Specifically, September’s drop in the ISM Non-Manufacturing PMI from 56.4 to 52.6 and the year-over-year decline in the Conference Board’s survey of consumer confidence (Chart 1). Both are sending tentative signals that economic weakness might be spreading from the manufacturing sector into the broader U.S. economy. The Fed is worried about the same thing, as evidenced by this passage from the September FOMC minutes: One risk that the economy faced was that the softness recorded of late in firms’ capital formation, manufacturing, and exporting activities might spread to their hiring decisions, with adverse implications for household income and spending. Participants observed that such an eventuality was not embedded in their baseline outlook; however, a couple of them indicated that this was partly because they assumed that an appropriate adjustment to the policy rate path would help forestall that eventuality. This passage makes two important points. First, it stresses the risk of contagion from manufacturing into services and consumer spending as a precondition for recession. This risk has clearly increased, but we are not yet ready to abandon our base case outlook. For one thing, Chart 1 shows that the ISM Non-Manufacturing survey printed at 51.8 for one month in 2016, before rebounding sharply. Second, the “hard” economic data paint a much rosier picture that the “soft” survey data (Chart 2). Industrial production has already bounced off its lows and, unlike the ISM Manufacturing PMI, has not yet approached 2015/16 levels. Similarly, new orders for capital goods are much stronger than during the 2015/16 period. As for consumer spending, it continues to grow at a rapid pace despite the drop in confidence. Chart 3Expect One Rate Cut In October

Expect One Rate Cut In October

Expect One Rate Cut In October

The most logical explanation for the divergence between “hard” and “soft” data is that business and consumer sentiment are being pulled down by concerns about the ongoing trade war. Our sense is that some positive news on that front is now required to bring the survey data back into line with the “hard” numbers. On that note, we anticipate that the looming 2020 election will provide enough incentive for President Trump to reach some sort of détente with China. In fact, as we go to press, optimism about a potential trade deal has pushed the 10-year Treasury yield up above 1.70%. If this optimism is not vindicated, then weak survey data will eventually drag the “hard” data lower. The economy is at a critical and highly uncertain juncture. Amidst so much uncertainty, and with so much hinging on near-term political decisions, how should we expect the Fed to respond? The above passage from the September FOMC minutes gives us a strong clue. It illustrates that the Fed believes that sufficiently accommodative monetary policy will help mitigate the risk of contagion from manufacturing into services and consumer spending. In other words, the Fed must help weather the current storm by ensuring that financial conditions remain supportive. This means refraining from delivering hawkish surprises to market expectations.1 The Fed believes that sufficiently accommodative monetary policy will help mitigate the risk of contagion from manufacturing into services and consumer spending. With that in mind, we note that the market has mostly priced-in an October rate cut (Chart 3), and we expect the Fed to deliver on that expectation. Assuming an October cut, the market is only pricing-in a 28% chance of another cut in December. Overall, the market is priced for 59 basis points of rate cuts during the next 12 months. We anticipate a 25 bps cut this month, followed by an improvement in the economic data that will make further cuts unnecessary. Bottom Line: Our late-1990s & 2015/16 roadmap for the economy still holds, but risks are mounting. Despite the risks, we expect that trade tensions will calm enough for the economic data to improve during the next few months. The result will be one more Fed rate cut this month, followed by an extended on-hold period. Investors should keep portfolio duration low in that environment. High-Yield Quality Spreads: Less Than Meets The Eye Corporate bonds have generally performed quite well this year, but oddly, the lowest tier of junk has not kept pace (Chart 4). Investment grade excess returns have followed a typical risk-on pattern. That is, the lowest rated / riskiest credit tiers have performed best in a bull market. However, in the high-yield space, Caa-rated debt has bucked the trend and actually underperformed the duration-matched Treasury index by 33 bps. Chart 4Caa-Rated Junk Is Not Keeping Pace

Caa-Rated Junk Is Not Keeping Pace

Caa-Rated Junk Is Not Keeping Pace

Is this a potentially worrying sign for corporate spreads more generally? To consider the question, we looked at the historical relationships between quality spreads – the spread differential between low-rated and high-rated credit tiers – and the overall index spreads for both investment grade and high-yield. We found a strong positive correlation in both cases, but no leading or lagging properties. That is, quality spreads tend to follow the same trend as the overall index spread, but do not flag signs of trouble before the overall index. Nonetheless, the current divergence between the Caa/Ba quality spread and the high-yield index spread is highly unusual (Chart 5). Our sense, however, is that the divergence has less to do with concerns about credit quality and more to do with this year’s large moves in Treasury yields and changes to bond index duration. Chart 5De-Coupling In Quality Spreads...

De-Coupling In Quality Spreads...

De-Coupling In Quality Spreads...

Chart 6...Is Due To Duration

...Is Due To Duration

...Is Due To Duration

Specifically, we note that this year’s large decline in Treasury yields has caused junk index duration to plunge, but the drop has been greater for the Ba credit tier than the Caa credit tier (Chart 6). Ba index duration has fallen by 0.8 this year (from 4.4 to 3.5), while Caa index duration has fallen by 0.6 (3.4 to 2.8). The result is that if we control for changes in duration by looking at a 12-month breakeven spread instead of the average index option-adjusted spread (OAS), we see that the quality spread widening is roughly consistent with the overall index (Chart 6, panel 3).2 In other words, the steep drop in Treasury yields has not led to the same reduction in risk in the Caa credit tier as it has in the other junk credit tiers. Caa spreads have widened on a relative basis, as a result. This year’s large decline in Treasury yields has caused junk index duration to plunge. It’s also interesting to note that the opposite dynamic is afoot within the investment grade corporate space. The Baa/Aa quality spread is more or less consistent with the overall index spread in OAS terms (Chart 5, top panel), but the quality spread widening is exacerbated when the impact of changing duration is considered (Chart 6, panels 1 & 2). That is, index duration has lengthened by more for the upper credit tiers than it has for the Baa credit tier. This makes Baa corporates look particularly attractive in risk-adjusted terms, as we have noted in prior research.3 From a big picture perspective, it is unusual for Treasury yields to fall so much without a concurrent widening in credit risk premiums. Eventually, this anomaly will be resolved by either: Higher Treasury yields in the event that recession is avoided, or Wider credit spreads in the event of a contraction in U.S. economic activity But in the meantime, negatively convex sectors such as high-yield corporates and Agency MBS look particularly attractive on a risk-adjusted basis. These sectors have benefited from the drop in Treasury yields by seeing their durations fall. They should perform well as long as the current environment of low Treasury yields and stable credit spreads persists. We take a more detailed look at the prospects for risk-adjusted performance within the different investment grade bond sectors in the next section. Risk And Reward In Investment Grade Bond Sectors As mentioned above, in this week’s report we present a novel approach for considering the risk/reward trade-off between different investment grade sectors of the U.S. bond market. We consider 23 sectors in total: 4 corporate credit tiers Conventional 30-year Agency MBS and Agency CMBS Aaa-rated non-Agency CMBS, credit card ABS and auto loan ABS Domestic and Foreign Agency bonds Supranationals Local Authority bonds (mostly taxable munis and USD-denominated Canadian provincial debt) USD-denominated Sovereign bonds for 10 different emerging markets Reward First, we consider the reward side of the equation. We do not impose any macro view, but instead, use the average index OAS as the best estimate for each sector’s 12-month expected excess returns relative to a duration-matched position in Treasuries. Chart 7 shows the expected excess returns for each sector. Right away, the attractiveness of Mexican sovereign debt is apparent. Mexico carries an A rating, but offers a greater spread than the Baa corporate index. Chart 7Expected Returns

A Perspective On Risk And Reward

A Perspective On Risk And Reward

Risk We decided to assess risk using a breakeven spread framework. We calculate a 12-month breakeven spread for each sector. This spread represents the basis point spread widening required for each sector to break even with a duration-matched position in Treasury securities on a 12-month horizon. We calculate the breakeven spread using the following equation: 0 = OAS – D(B) + 0.5*CVXs*(dYs)2 - 0.5*CVXT*(dYT)2 Where: OAS = the sector’s option-adjusted spread D = the sector’s duration B = the breakeven spread CVXs = the sector’s convexity CVXT = the convexity of a duration-matched Treasury security dYs = trailing 1-year volatility of the sector’s yield dYT = trailing 1-year volatility of the duration-matched Treasury yield Chart 8 shows each sector’s 12-month breakeven spread, and it illustrates that the breakeven spread is a sub-optimal measure of risk. In theory, the highest breakeven spreads should be the least likely to see losses, but this is obviously not the case. Baa-rated South African Sovereign debt carries the largest breakeven spread, but it should be among the riskiest of the sectors. Chart 812-Month Breakeven Spreads

A Perspective On Risk And Reward

A Perspective On Risk And Reward

The missing piece of the puzzle is spread volatility. South African sovereign spreads need to widen by 39 bps before losses are incurred, while Aaa-rated credit card ABS spreads only need to widen by 13 bps. However, if spread volatility is much higher for South African sovereigns than for credit card ABS, then the sovereign sector still might be more likely to see losses. To control for this difference we calculate the standard deviation of annual spread changes for each sector, starting from May 2014 when all sectors have available data. We then divide each sector’s breakeven spread by the result. This calculation gives us a volatility-adjusted 12-month breakeven spread. In other words, it is the number of standard deviations of spread widening required for each sector to see losses on a 12-month horizon (Chart 9). Chart 912-Month Volatility-Adjusted Breakeven Spreads

A Perspective On Risk And Reward

A Perspective On Risk And Reward

Risk & Reward We bring risk and reward together in Charts 10-12. Chart 10 shows expected returns on the y-axis and the vol-adjusted 12-month breakeven spread on the x-axis. Sectors plotting near the top-right of the chart give the best returns and lowest risk of losses, while sectors plotting near the bottom-left provide low expected returns and high risk of losses. Immediately, Saudi Arabian sovereigns and Foreign Agency debt stand out as offering high expected returns for their risk levels. Note that South African sovereigns plot off the charts, toward the top-left of Charts 10-12, as indicated by the arrows. Chart 10Expected Returns Vs. Risk Of Negative Excess Returns

A Perspective On Risk And Reward

A Perspective On Risk And Reward

Chart 11Expected Returns Vs. Risk Of Losing 100 BPs

A Perspective On Risk And Reward

A Perspective On Risk And Reward

Chart 12Expected Returns Vs. Risk Of Losing 200 BPs

A Perspective On Risk And Reward

A Perspective On Risk And Reward

In Charts 11 and 12 we make one further refinement to our risk measure. In these charts, instead of calculating 12-month breakeven spreads, we calculate the spread change necessary for each sector to underperform Treasuries by 100 bps and 200 bps, respectively. Saudi Arabian sovereigns and Foreign Agency debt stand out as offering high expected returns for their risk levels. This adjustment arguably gives a more useful perspective on risk. For example, because spreads are quite narrow in the Supranational and Domestic Agency sectors, the risk of negative returns versus Treasuries is quite elevated. However, these sectors also carry high credit ratings and low spread volatility, making it exceedingly unlikely that they would deliver losses of 100 bps or more. Considering Charts 11 and 12, we look for sectors that clearly dominate other ones, i.e. plotting both higher and further to the right. Once again, Foreign Agencies and Saudi Arabian sovereigns both look very appealing. Mexican sovereign debt also offers very high expected return, and less risk that the Baa corporate sector. We would also like to point out the attractiveness of Agency MBS. As we noted in a recent report, Agency MBS offer considerably less risk than high-rated corporate debt, and similar expected returns. Note that this analysis doesn’t impose any macroeconomic view, and our sense is that the macro back-drop is more favorable for MBS spreads than for corporates.4 All in all, we reiterate our recommendation to favor Agency MBS over Aaa-, Aa- and A-rated corporate bonds. We will continue to refine this approach to measuring the risk/reward trade-off in the coming weeks, including incorporating high-yield debt into our analysis. Stay tuned. Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 For further discussion on this topic please see U.S. Bond Strategy Weekly Report, “Act As Appropriate”, dated August 27, 2019, available at usbs.bcaresearch.com 2 The 12-month breakeven spread is the spread widening required on a 12-month horizon to break even with a duration-matched position in Treasury securities. It can be approximated by dividing the option-adjusted spread by duration, as is done in Chart 6. 3 Please see U.S. Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy Weekly Report, “Two Themes And Two Trades”, dated October 1, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights In this Weekly Report, we present our semi-annual chartbook of the BCA Central Bank Monitors. All of the Monitors are now below the zero line, indicating a growing need to ease global monetary policy (Chart of the Week). Central bankers have already gone down that path in several countries over the past few months (the U.S., the euro area, Australia and New Zealand), helping sustain the powerful 2019 rally in global bond markets. Feature With the global manufacturing & trade downturn now threatening to spill over into domestic demand in the major developed markets, policymakers will need to stay dovish to stave off recession. This will keep global bond yields at depressed levels in the near term, at least until widely-followed data like manufacturing PMIs stabilize and/or there is positive news on U.S.-China trade negotiations. Chart of the WeekStrong Pressures To Ease Global Monetary Policy

Strong Pressures To Ease Global Monetary Policy

Strong Pressures To Ease Global Monetary Policy

Yields already discount a lot of bad economic news, however, and there is a ray of hope visible in the bottoming out of our global leading economic indicator. A sustainable bottom in global bond yields, though, will require some change in the current downward growth or inflation momentum highlighted in our Central Bank Monitors. Yields already discount a lot of bad economic news, however, and there is a ray of hope visible in the bottoming out of our global leading economic indicator. A sustainable bottom in global bond yields, though, will require some change in the current downward growth or inflation momentum highlighted in our Central Bank Monitors. An Overview Of The BCA Central Bank Monitors* Chart 2Low Bond Yields Are Consistent With Our CB Monitors

Low Bond Yields Are Consistent With Our CB Monitors

Low Bond Yields Are Consistent With Our CB Monitors

The BCA Central Bank Monitors are composite indicators designed to measure the cyclical growth and inflation pressures that can influence future monetary policy decisions. The economic data series used to construct the Monitors are not the same for every country, but the list of indicators generally measure the same things (i.e. manufacturing cycles, domestic demand strength, commodity prices, labor market conditions, exchange rates, etc). The data series are standardized and combined to form the Monitors. Readings above the zero line for each Monitor indicate pressures for central banks to raise interest rates, and vice versa. Through the nexus between growth, inflation, and market expectations of future interest rate changes, the Monitors do exhibit broad correlations to government bond yields in the Developed Markets (Chart 2). All of the Monitors are currently pointing in a bond-bullish direction, making them less useful as a country allocation tool within global bond portfolios. With easing pressures most intense in the euro area, given that the ECB Monitor has the lowest reading, our recommended overweight stance on core euro area government bonds (hedged into U.S. dollars) remains well supported. In each BCA Central Bank Monitor Chartbook, we include a new chart for each country that we have not shown previously. In this edition, we show the components of the Monitors, grouped into those focusing on economic growth and inflation, plotted against our central bank discounters that indicate the amount of rate cuts/hikes priced into global Overnight Index Swap (OIS) curves. Fed Monitor: Signaling A Need For More Cuts Our Fed Monitor has fallen below the zero line (Chart 3A), indicating that the Fed’s summer rate cuts were justified with more easing still required. The Monitor, however, has not yet fallen to levels seen during U.S. recessions and is more consistent with the below-trend growth periods in 2016 and the late-1990s. The views of the FOMC on U.S. monetary policy are more deeply divided now than has been seen in many years. The doves can point to slumping global growth, persistent trade uncertainty, contracting capital spending and falling inflation expectations as reasons to continue cutting rates. The hawks can look at continued labor market tightness, elevated asset prices and realized inflation rates holding near the Fed’s 2% inflation target (Chart 3B) as reasons to keep monetary policy steady. That mixed picture can be seen in the components of our Fed Monitor, with the growth components showing the biggest pressure for more rate cuts compared to more stable readings from the inflation and financial components (Chart 3C). Chart 3AU.S.: Fed Monitor

U.S.: Fed Monitor

U.S.: Fed Monitor

Chart 3BU.S. Realized Inflation Holding Firm

U.S. Realized Inflation Holding Firm

U.S. Realized Inflation Holding Firm

Chart 3CGreatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

Greatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

Greatest Pressure For Fed Rate Cuts From Growth Components Of Our Fed Monitor

The U.S. Treasury market may have gotten ahead of itself after the latest decline in yields, which looks stretched versus the Fed Monitor. The U.S. Treasury market may have gotten ahead of itself after the latest decline in yields, which looks stretched versus the Fed Monitor (Chart 3D). We still expect the Fed to deliver just one more rate cut at the FOMC meeting at the end of October, as the “hard” U.S. data is outpeforming the “soft” data like the weak ISM surveys. That leaves Treasury yields vulnerable to some rebound if global growth stabilizes, although that is conditional on no new breakdown of the U.S.-China trade negotiations – a factor that continues to weigh on U.S. business confidence. Chart 3DTreasury Yields More Than Fully Discount Fed Easing Pressures

Treasury Yields More Than Fully Discount Fed Easing Pressures

Treasury Yields More Than Fully Discount Fed Easing Pressures

BoE Monitor: Easier Policy Needed Our Bank of England (BoE) Monitor, which was in the “tighter money required” zone from 2016-18, has been below the zero line since April of this year (Chart 4A). The market agrees with the message from the Monitor and is now pricing in -12bps of rate cuts over the next twelve months. The relentless uncertainty surrounding Brexit has triggered sharp downgrades of growth expectations and weakened business confidence, which the BoE is now factoring into its own projections. In the August Inflation Report, the BoE lowered its 2020 inflation forecast to below 2% - no surprise given the sharp fall in realized inflation that has already occurred even as economic growth has still not yet fallen substantially below trend (Chart 4B). Chart 4AU.K.: BoE Monitor

U.K.: BoE Monitor

U.K.: BoE Monitor

Chart 4BFalling U.K. Inflation Opens The Door To A BoE Ease

Falling U.K. Inflation Opens The Door To A BoE Ease

Falling U.K. Inflation Opens The Door To A BoE Ease

Still, weakening growth components have been the main driver of the BoE Monitor into rate cut territory (Chart 4C). While a strong jobs market is helping support consumer spending, the Brexit turmoil is having a lasting impact on future growth. Since the 2016 Brexit referendum, business confidence and real business investment have collapsed which, in turn, has hurt productivity growth, as we discussed in a Special Report last month.1 Chart 4CBrexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

Brexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

Brexit Uncertainty + Slumping Growth = Pressure For BoE Rate Cuts

The uncertainty around Brexit dominates the economic outlook and any future BoE decisions. Our Geopolitical Strategy service anticipates that Brexit will be delayed beyond October 31st. As a result, uncertainty will continue to weigh on Gilt yields, even though yields have already fallen in line with our BoE Monitor (Chart 4D). We continue to recommend an overweight stance on U.K. Gilts. Chart 4DGilt Yields Have Fallen In Line With Our BoE Monitor

Gilt Yields Have Fallen In Line With Our BoE Monitor

Gilt Yields Have Fallen In Line With Our BoE Monitor

ECB Monitor: Intense Pressure For Easier Monetary Policy Our European Central Bank (ECB) Monitor is now well below the zero line, signaling a strong need for easier monetary policy (Chart 5A). The global manufacturing downturn has hit the export-dependent economies of the euro area hard, with Germany now likely in a technical recession. Our European Central Bank (ECB) Monitor is now well below the zero line, signaling a strong need for easier monetary policy. Despite the weaker growth momentum, there remains far less spare capacity in the euro area economy than at any time since before the 2009 global recession (Chart 5B). This is keeping realized inflation in positive territory, in contrast to what was seen during the previous downturn in 2015-16. Chart 5AEuro Area: ECB Monitor

Euro Area: ECB Monitor

Euro Area: ECB Monitor

Chart 5BEuro Area Inflation Is Subdued, Despite Tight Labor Markets

Euro Area Inflation Is Subdued, Despite Tight Labor Markets

Euro Area Inflation Is Subdued, Despite Tight Labor Markets

The ECB has already responded to the weakening growth & inflation pressures, introducing a new TLTRO program back in March and then cutting the overnight deposit rate and restarting its Asset Purchase Program in September. The latest policy moves were reported to be more contentious, with the “hard money” northern euro area countries opposed to restarting bond purchases. The new incoming ECB President, Christine Lagarde, will likely have her hands full trying to gain consensus on any further easing measures from here, even as both the growth and inflation components of our ECB Monitor indicate that more stimulus is needed (Chart 5C). Chart 5CA Consistent Message On The Need For Future ECB Easing From Growth & Inflation

A Consistent Message On The Need For Future ECB Easing From Growth & Inflation

A Consistent Message On The Need For Future ECB Easing From Growth & Inflation

The big decline in euro area bond yields, which has pushed large swaths of sovereign yields into negative territory, does not look particularly stretched relative to the plunge in the ECB Monitor (Chart 5D). Without signs that the global manufacturing downturn is ending, however, euro area yields will stay mired at current deeply depressed levels. We recommend a moderate overweight on core European government bonds, on a currency-hedged basis into U.S. dollars. Chart 5DBund Rally Looks In Line With The ECB Monitor

Bund Rally Looks In Line With The ECB Monitor

Bund Rally Looks In Line With The ECB Monitor

BoJ Monitor: A Rate Cut On The Horizon? Our Bank of Japan (BoJ) Monitor has drifted slightly below the zero line into “rate cut required” territory (Chart 6A). Over the past few years, the BoJ’s monetary policy has remained unchanged for the most part and its messaging has grown less dovish, citing an expanding economy. However, recent Japanese economic data shows widespread deterioration in growth momentum, as the nation has been hit hard by the global manufacturing and trade recession. Yet even with weaker growth, Japan’s unemployment rate keeps hitting all-time lows. This has not helped boost inflation much, though, with Japan’s CPI inflation still struggling to reach even the 1% level (Chart 6B). Still, the latest leg lower in our BoJ Monitor has been driven by the growth, rather than inflation, components (Chart 6C). Chart 6AJapan: BoJ Monitor

Japan: BoJ Monitor

Japan: BoJ Monitor

Chart 6BNo Spare Capacity In Japan, But Still No Inflation

No Spare Capacity In Japan, But Still No Inflation

No Spare Capacity In Japan, But Still No Inflation

Weakening confidence has resulted in significant declines in both consumer spending and business investment. Due to the struggling domestic economy, it was expected that the Abe government would postpone the scheduled consumption tax hike, but it was finally initiated on October 1st. The timing could not be worse given the ongoing contraction in global manufacturing and trade activity that has clearly spilled over into Japan’s export and industrially-focused economy. Chart 6CThe Slumping Japanese Economy Could Use Some More BoJ Assistance

The Slumping Japanese Economy Could Use Some More BoJ Assistance

The Slumping Japanese Economy Could Use Some More BoJ Assistance

The BoJ will likely try and deliver some sort of easing in the next few months, but its options are limited after years of already hyper-easy policy. A modest rate cut is likely all that will be delivered, on top of a continuation of the Yield Curve Control policy. That will be enough to keep JGB yields at depressed levels (Chart 6D), even if global yields were to begin climbing. Chart 6DJGB Yields Look Fairly Valued Vs The BoJ Monitor

JGB Yields Look Fairly Valued Vs The BoJ Monitor

JGB Yields Look Fairly Valued Vs The BoJ Monitor

BoC Monitor: Rate Cuts Needed, But Will The BoC Deliver? The Bank of Canada (BoC) Monitor has been below zero since April of this year, indicating a need for easier monetary policy (Chart 7A). Although the BoC has maintained its policy rate at 1.75%, dovish Fed policy and softening domestic economic growth are making it harder for the BoC to continue sitting on its hands Although the Canadian labor market remains solid, household consumption has continued to weaken alongside falling consumer confidence. However, the inflation rate for both headline and core CPI measures is still hovering near the mid-point of BoC 1-3% target range (Chart 7B). Chart 7ACanada: BoC Monitor

Canada: BoC Monitor

Canada: BoC Monitor

Chart 7BRising Inflation Making The BoC’s Job Harder

Rising Inflation Making The BoC's Job Harder

Rising Inflation Making The BoC's Job Harder

At the moment, our BoC Monitor is more influenced by weaker growth components than stabilizing inflation components (Chart 7C). Similar mixed messages are also evident in other data. According to the latest BoC Business Outlook Survey, the overall outlook has edged up to the historical average,2 but real capex growth remains in negative territory and manufacturing new orders are still falling. In contrast, the Canadian labor market remains tight and both wage and price inflation are holding firm. Chart 7CBoC Growth & Inflation Components Signaling Moderate Pressure To Ease

BoC Growth & Inflation Components Signaling Moderate Pressure To Rise

BoC Growth & Inflation Components Signaling Moderate Pressure To Rise

Canadian government bonds have rallied strongly this year, but the yield momentum has appeared to overshoot the decline in our BoC Monitor (Chart 7D). The Canadian OIS curve is discounting -27bps of rate cuts over the next twelve months, but the BoC is not signaling that they will ease. We upgraded our recommended stance on Canadian government bonds to neutral back in May, and we see no need to alter that view without further evidence of more deterioration in Canadian growth or inflation data.3 Chart 7DCanadian Bond Rally Looks A Bit Stretched

Canadian Bond Rally Looks A Bit Stretched

Canadian Bond Rally Looks A Bit Stretched

RBA Monitor: Expect Another Cut The Reserve Bank of Australia (RBA) Monitor has been below the zero line since September 2018, indicating a need for easier monetary policy (Chart 8A). The RBA has already delivered on that signal this year, cutting the Cash Rate twice to an all-time low of 0.75%. Markets are still expecting more, with the Australian OIS curve discounting another -29bps of cuts over the next year, although most of those cuts are expected to occur within the next six months. The signal from our RBA Monitor suggests that Australian bond yields should remain under downward pressure, although the yield momentum has been excessive relative to the fall in the Monitor. Both headline and core CPI inflation remain below the RBA’s 2-3% target range (Chart 8B), and the central bank continues to lower its inflation forecasts, suggesting an entrenched dovish bias. Chart 8AAustralia: RBA Monitor

Australia: RBA Monitor

Australia: RBA Monitor

Chart 8BNo Inflation For The RBA To Worry About

No Inflation For The RBA To Worry About

No Inflation For The RBA To Worry About

The latest downturn in our RBA Monitor is related to declines in both the inflation and growth components (Chart 8C). The weakness in the growth components is led by falling exports to Asia, in addition to the sharp drop in house prices in the major cities. The fall in the inflation components reflects both weak inflation expectations and spare capacity in labor markets. Chart 8CA Loud & Clear Message On The Need For RBA Easing

A Loud & Clear Message On The Need For RBA Easing

A Loud & Clear Message On The Need For RBA Easing

The signal from our RBA Monitor suggests that Australian bond yields should remain under downward pressure, although the yield momentum has been excessive relative to the fall in the Monitor (Chart 8D). Australia’s economy will not begin to outperform again, however, until China’s current growth slump starts to bottom out, which is unlikely to occur until the first quarter of 2020 at the earliest. Thus, we expect the RBA to deliver another rate cut before the end of the year, justifying a continued overweight stance on Australian government bonds. Chart 8DA Lot Of Bad News Discounted In Australian Bond Yields

A Lot Of Bad News Discounted In Australian Bond Yields

A Lot Of Bad News Discounted In Australian Bond Yields

RBNZ Monitor: More Easing To Come Our Reserve Bank of New Zealand (RBNZ) monitor remains well below zero, indicating that easier monetary policy is still required (Chart 9A). The central bank has already delivered two rate cuts this year: a -25bps cut in May and, more importantly, a shock rate cut of -50bps in August. Forward guidance remains dovish, with RBNZ Governor Adrian Orr signaling more easing is likely and even hinting at negative rates in the future. This rhetoric is reflected in the NZ OIS curve, which is pricing in a further -42bps of easing over the next twelve months. High inflation is not a constraint for the RBNZ. Both headline and core measures of inflation are currently at 1.7% (Chart 9B). As the RBNZ targets a 1-3% range over the medium term, the prospect of overshooting the 2% longer-term target will not restrict policymakers from acting as appropriate to boost growth. Chart 9ANew Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

New Zealand: RBNZ Monitor

Chart 9BNZ Inflation Creeping Higher

NZ Inflation Creeping Higher

NZ Inflation Creeping Higher

Most of the pressure to ease has come from the continued deterioration in the growth component of our RBNZ Monitor (Chart 9C), reflecting weakness in manufacturing and consumption. The manufacturing PMI is currently in contractionary territory at 48.4, having fallen almost five points since February of this year. Annual growth in retail sales has been slowing for the past two years while consumer confidence is at 7-year lows. Chart 9CWeak Growth Is The Reason RBNZ Rate Cuts Are Needed

Weak Growth Is The Reason RBNZ Rate Cuts Are Needed

Weak Growth Is The Reason RBNZ Rate Cuts Are Needed

We feel confident in reiterating our bullish recommendation on NZ government bonds versus U.S. and German sovereign debt. The RBNZ Monitor suggests that policy will stay dovish for some time, while NZ yields still offer a relatively attractive yield, unlike deeply overbought Treasuries and Bunds (Chart 9D). Chart 9DStill A Bullish Case For New Zealand Government Bonds

Still A Bullish Case For New Zealand Government Bonds

Still A Bullish Case For New Zealand Government Bonds

Riksbank Monitor: Watching And Waiting Our Riksbank Monitor remains very slightly below zero and the market is currently priced for -4bps of rate cuts over the next year (Chart 10A). The Riksbank has decided to hold the Repo Rate constant at -0.25% while forecasting a hike towards the end of this year or the beginning of 2020. Given the policy environment, rate cuts remain unlikely. At most, the Riksbank can further delay rate hikes if the data continues to disappoint. The Riksbank noted in its September Monetary Policy Report that the unexpectedly weak development of the labor market indicates that resource utilization will normalize sooner than expected. This is reflected in Chart 10B, where the unemployment gap is now negative. Meanwhile, inflation readings are giving a mixed signal for the central bank. While the headline CPI measure has declined precipitously year-to-date, owing to the dramatic fall in oil prices, core inflation has continued to climb steadily. Chart 10ASweden: Riksbank Monitor

Sweden: Riksbank Monitor

Sweden: Riksbank Monitor

Chart 10BMixed Messages From Swedish Inflation

Mixed Messages From Swedish Inflation

Mixed Messages From Swedish Inflation

As a result, the inflation components of our Riksbank monitor - driven by a spike in the Citigroup Inflation Surprise Index, wage growth hooking upward and inflation expectations holding firm around 2% - are signaling the need for tighter monetary policy (Chart 10C). However, the growth components – led by weak exports, employment, and manufacturing data - are exerting pressure in the opposite direction. This is evident in the Swedish Manufacturing PMI, which tumbled from 51.8 to 46.3 in September, deep into contractionary territory. Chart 10CThere Is A Reason Why The Riksbank Has Been On Hold

There Is A Reason Why The Riksbank Has Been On Hold

There Is A Reason Why The Riksbank Has Been On Hold

Keeping in mind the inflation constraint, it remains unlikely that the Riksbank will cut rates unless the economic data disappoints more significantly to the downside. This should help put a floor under Swedish bond yields in the near term (Chart 10D). Chart 10DSwedish Yields Have Fallen Too Far, Too Fast

Swedish Yields Have Fallen Too Far, Too Fast

Swedish Yields Have Fallen Too Far, Too Fast

Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Ray Park, CFA Research Analyst ray@bcaresearch.com Shakti Sharma Research Associate shaktis@bcaresearch.com Footnotes * NOTE: All information in this report reflects our knowledge of global events as of Thursday, October 10. 1 Please see BCA Global Fixed Income Strategy Special Report “United Kingdom: Cyclical Slowdown Or Structural Malaise?” dated September 20, 2019, available at gfis.bcaresearch.com. 2https://www.bankofcanada.ca/2019/06/business-outlook-survey-summer-2019/ 3 Please see BCA Global Fixed Income Weekly Report, “Reconcilable Differences” dated May 8, 2019, available at gfis.bcaresearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

BCA Central Bank Monitor Chartbook: Intensifying Pressure To Ease

BCA Central Bank Monitor Chartbook: Intensifying Pressure To Ease

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

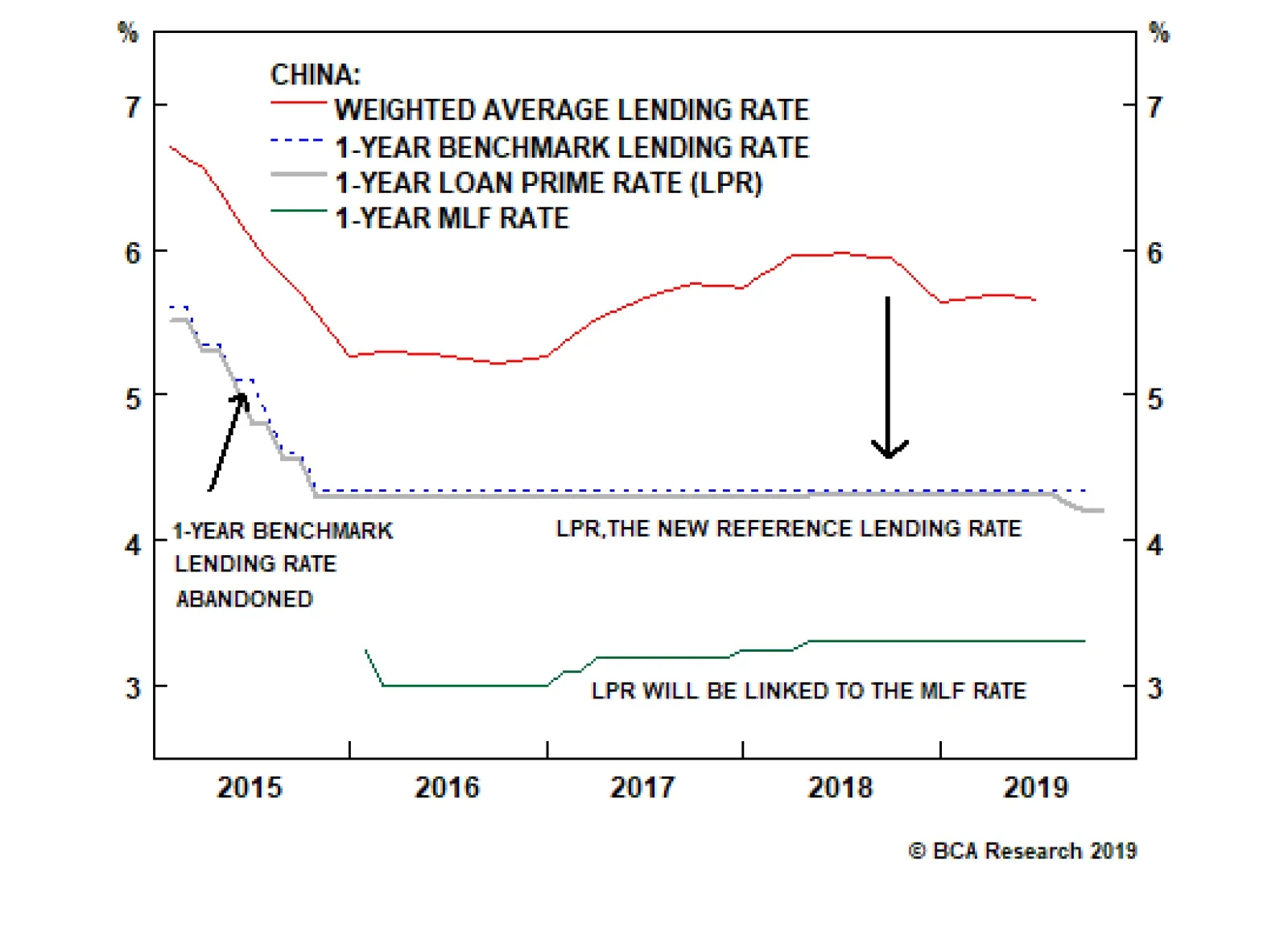

The LPR rate is essentially the MLF rate plus bank profit margins. The market will guide the top line lending rate, while the PBoC will have control over the floor rate (MLF) through open market operations. The fact that the PBoC is keeping the MLF rate…

On August 20th, the PBoC launched a new loan prime rate (LPR) system, a revamped reference regime for setting bank loan interest rates. In September, the new LPR rate for one-year bank loans was lowered by five basis points. The new LPR reform is designed…

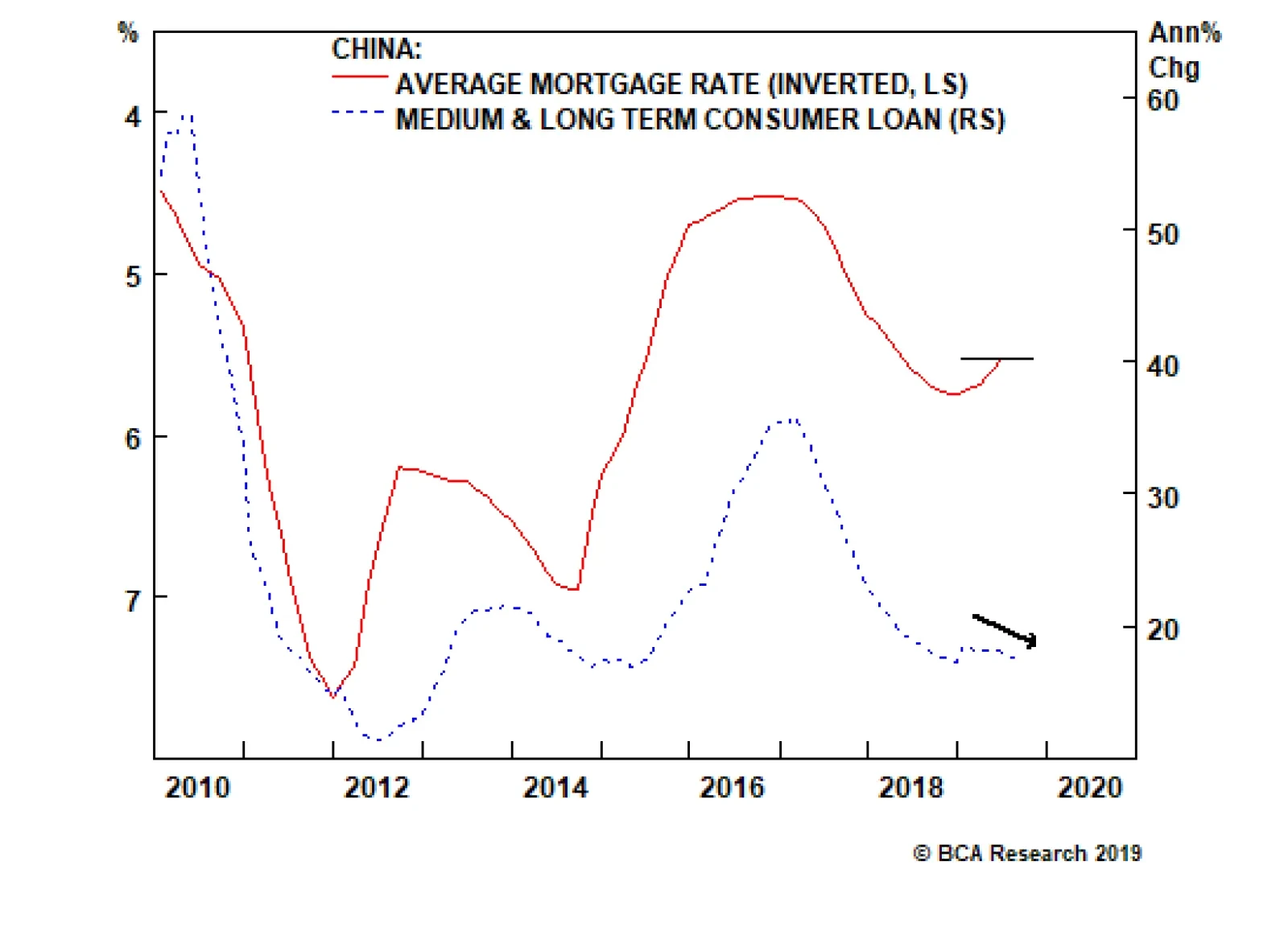

Highlights The Chinese economy is still slowing, and there is not yet enough evidence from forward-looking economic data to suggest a turnaround is imminent. Deflation has returned to China’s industrial sector. Even though overall price deceleration has been relatively mild, it is further squeezing already deteriorating industrial profit growth. We do not expect deflation to spiral into a 2015/2016-style episode, which removes at least one risk to our growth outlook. At the same time, a mild deceleration in prices will not provide enough incentive for Chinese policymakers to hit the stimulus button. The People’s Bank of China’s new interest rate-setting regime, the LPR, will not provide much in the way of stimulus over the next few months. But it has the potential to improve China’s monetary policy transmission mechanism over the coming year, increasing the odds that policymakers will succeed in stabilizing economic activity. Short-term downside risks to growth have not abated, and we remain tactically bearish on Chinese stocks. Cyclically, we continue to recommend an overweight stance, on the basis of an eventual reacceleration in economic activity. Feature Chart 1The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing

The Chinese Economy Is Still Slowing