Monetary

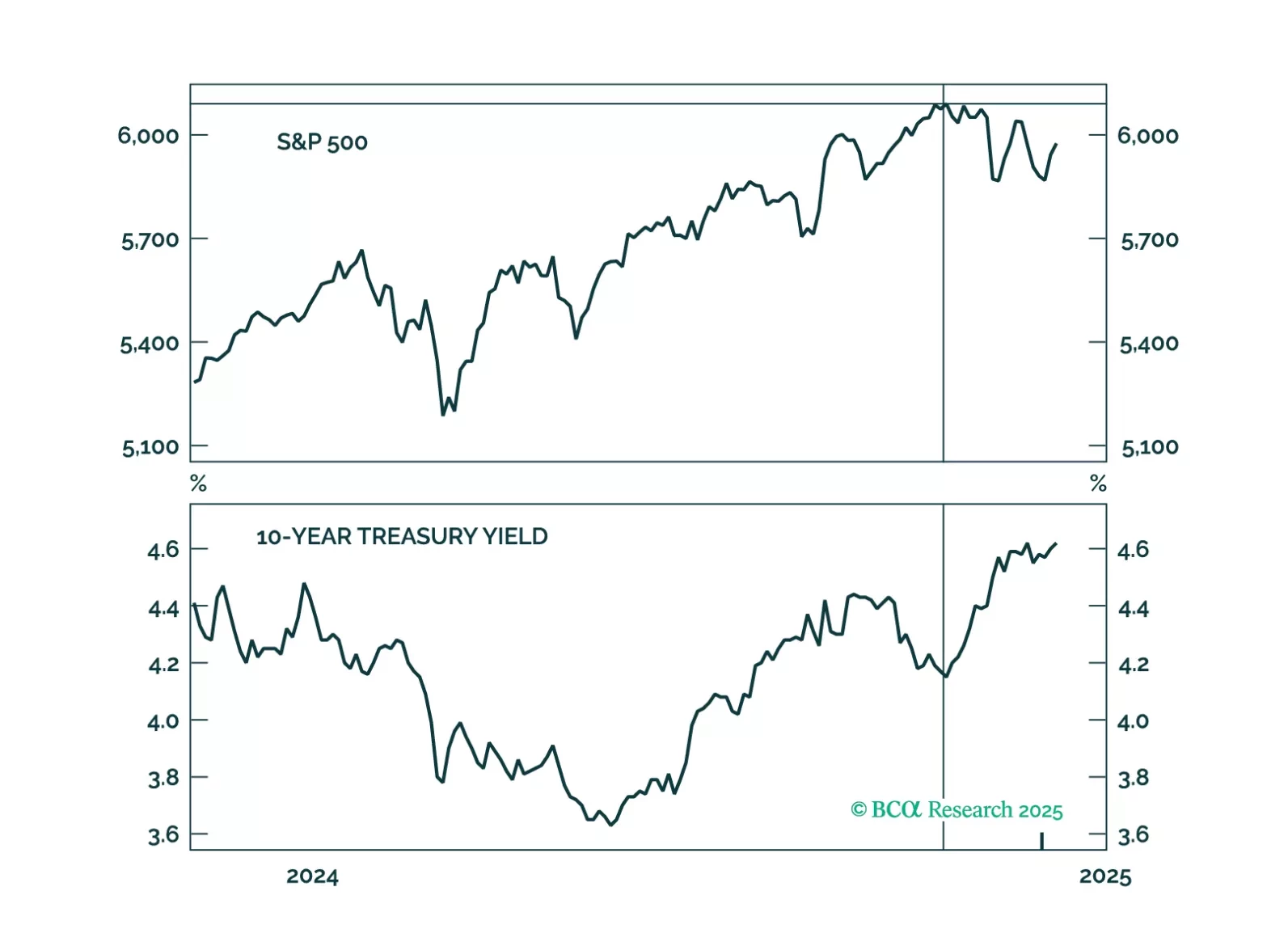

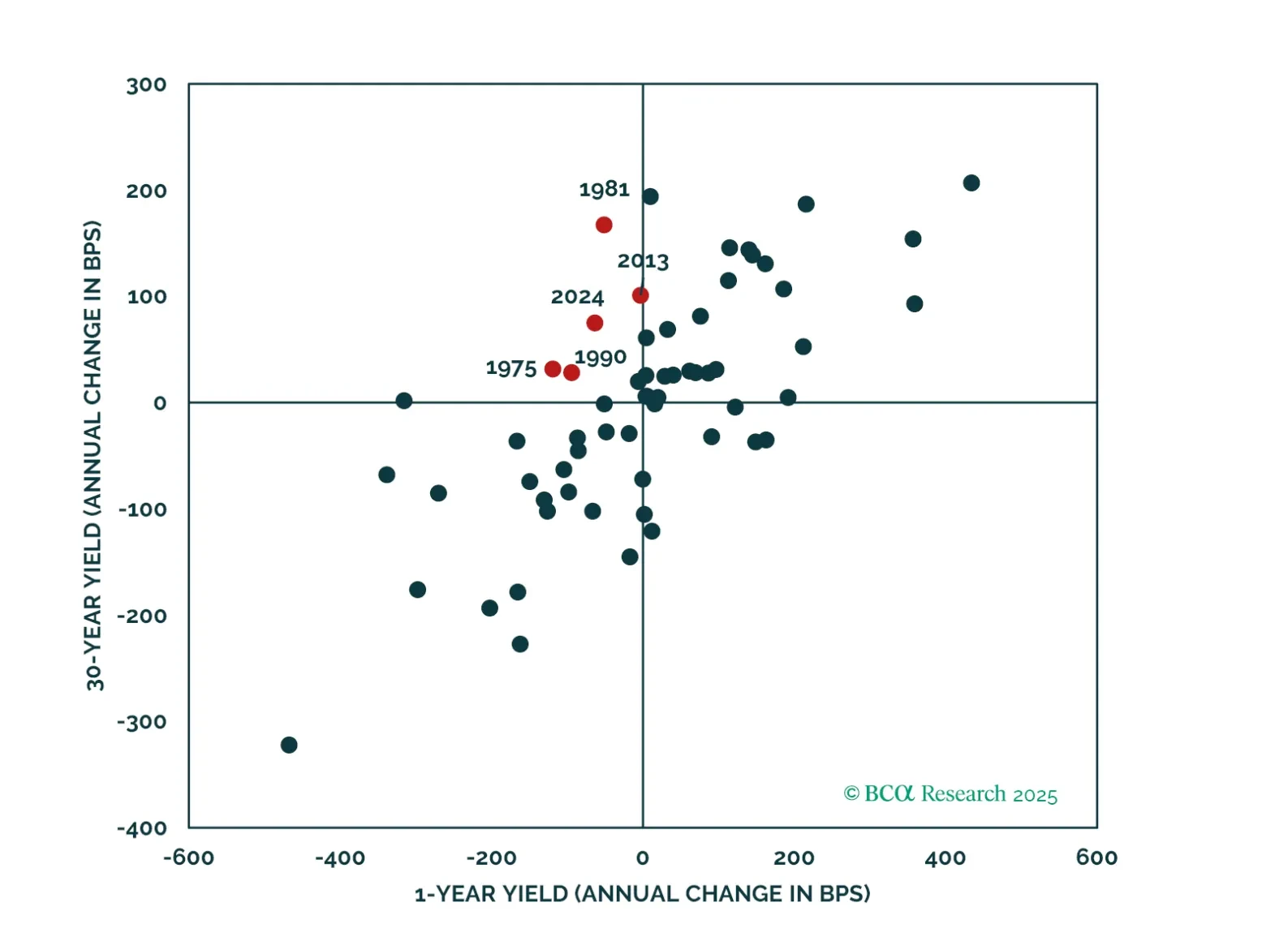

We examine Treasury market valuation and look for indicators that could help us time the next peak in yields. We also update the forecasts from our Treasury yield model.

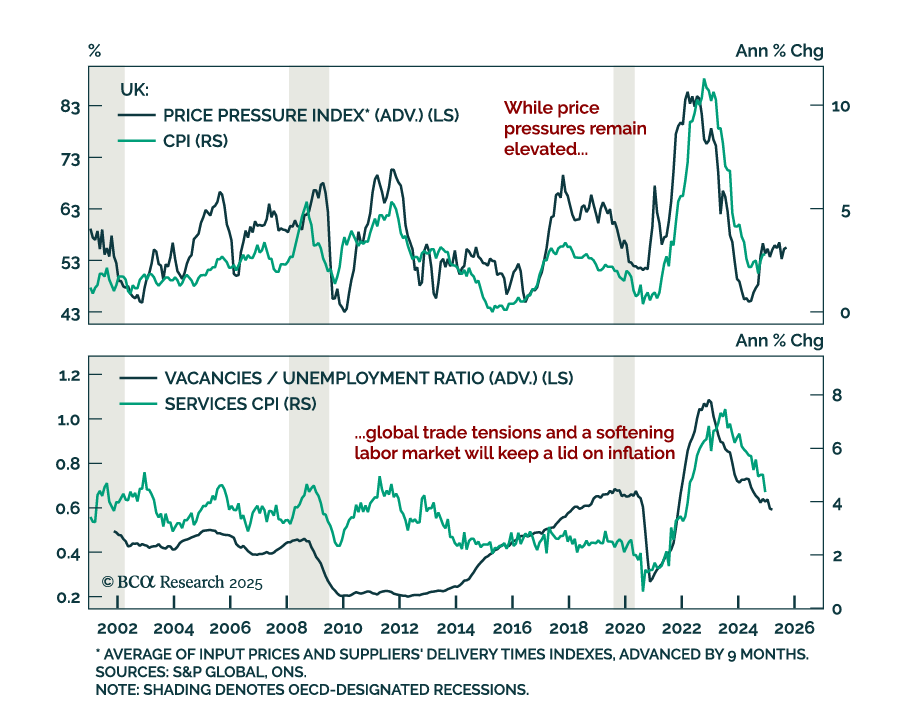

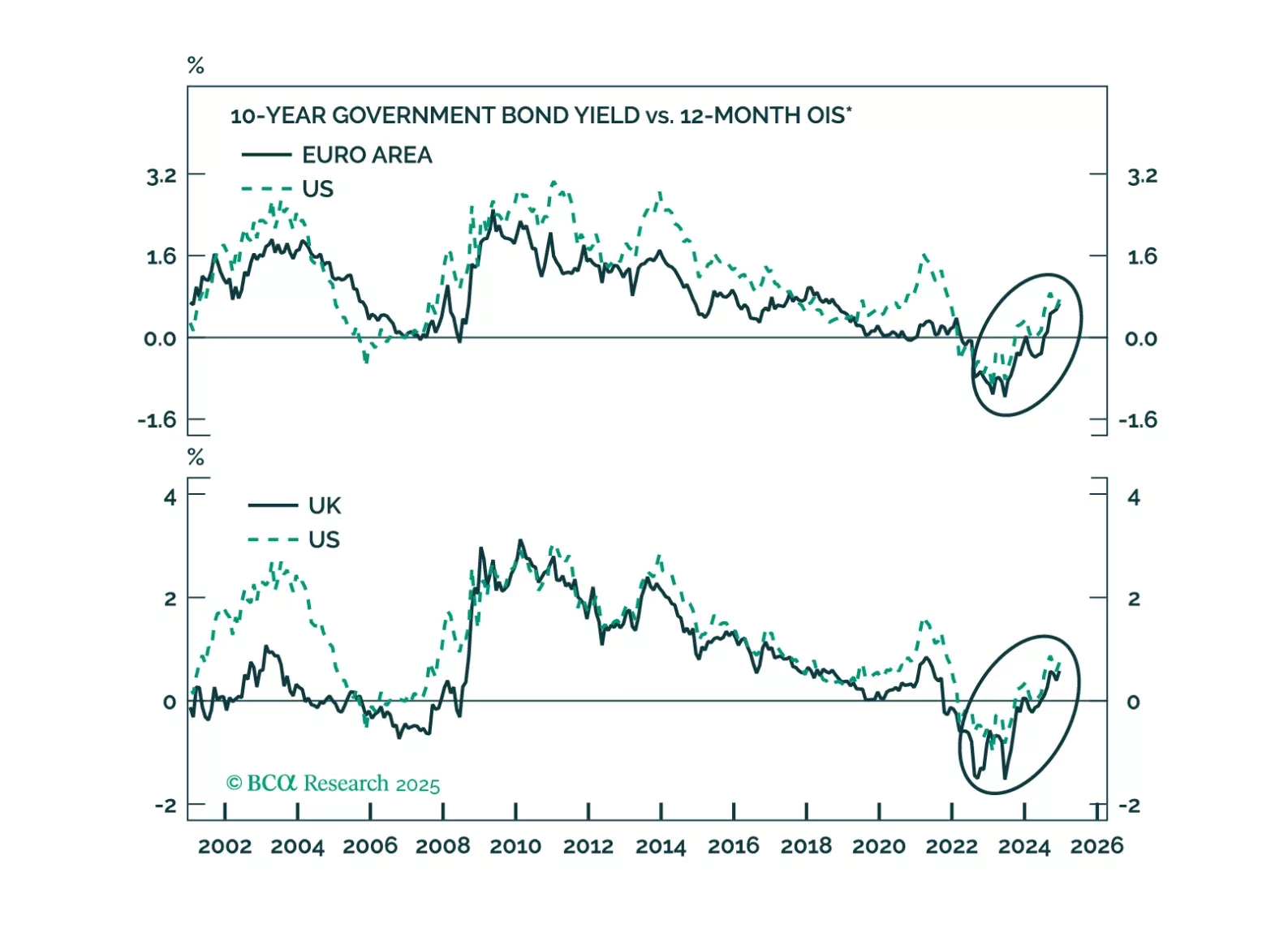

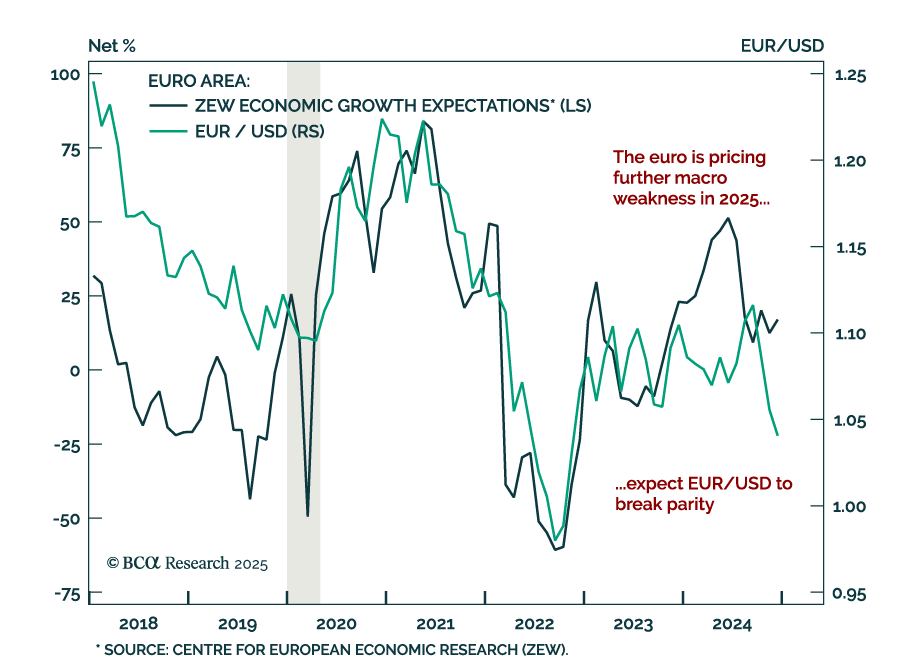

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?

Our Portfolio Allocation Summary for January 2025.

Paradoxically, raging optimism on the US economy is making a reacceleration in growth less likely in 2025. The reaction of the bond market has made the Fed rethink its cutting campaign. Markets are also constraining Trump’s agenda. US manufacturing will not recover with a surging dollar. Fears of inflation and debt sustainability have made moderate House Republicans push back against the President Elect’s wishes. Given the sky-high optimism embedded in asset prices, we believe a defensive portfolio stance is warranted on a 12-month horizon. Overweight gold to hedge the risk of a fiscal crisis.

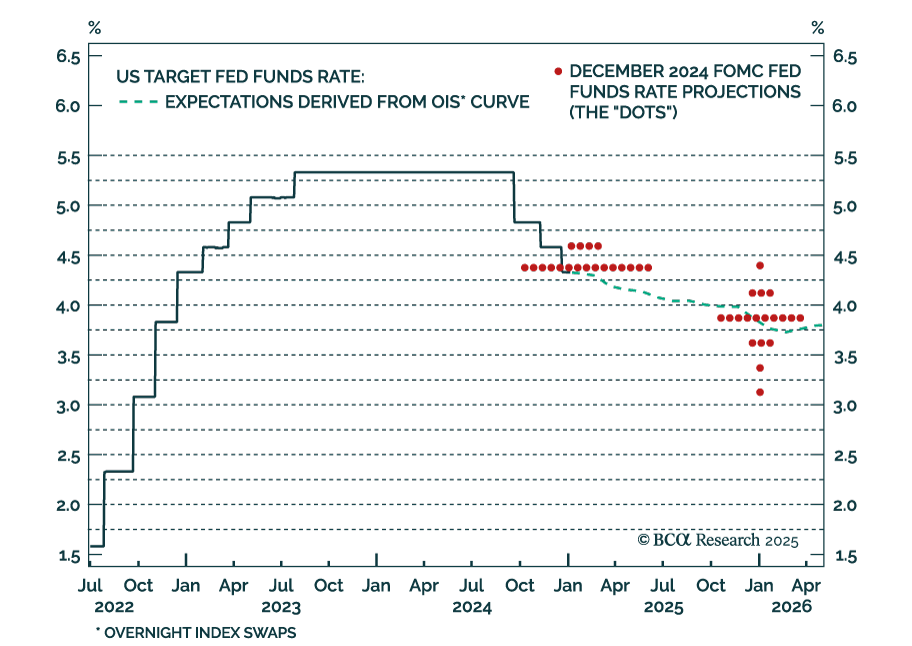

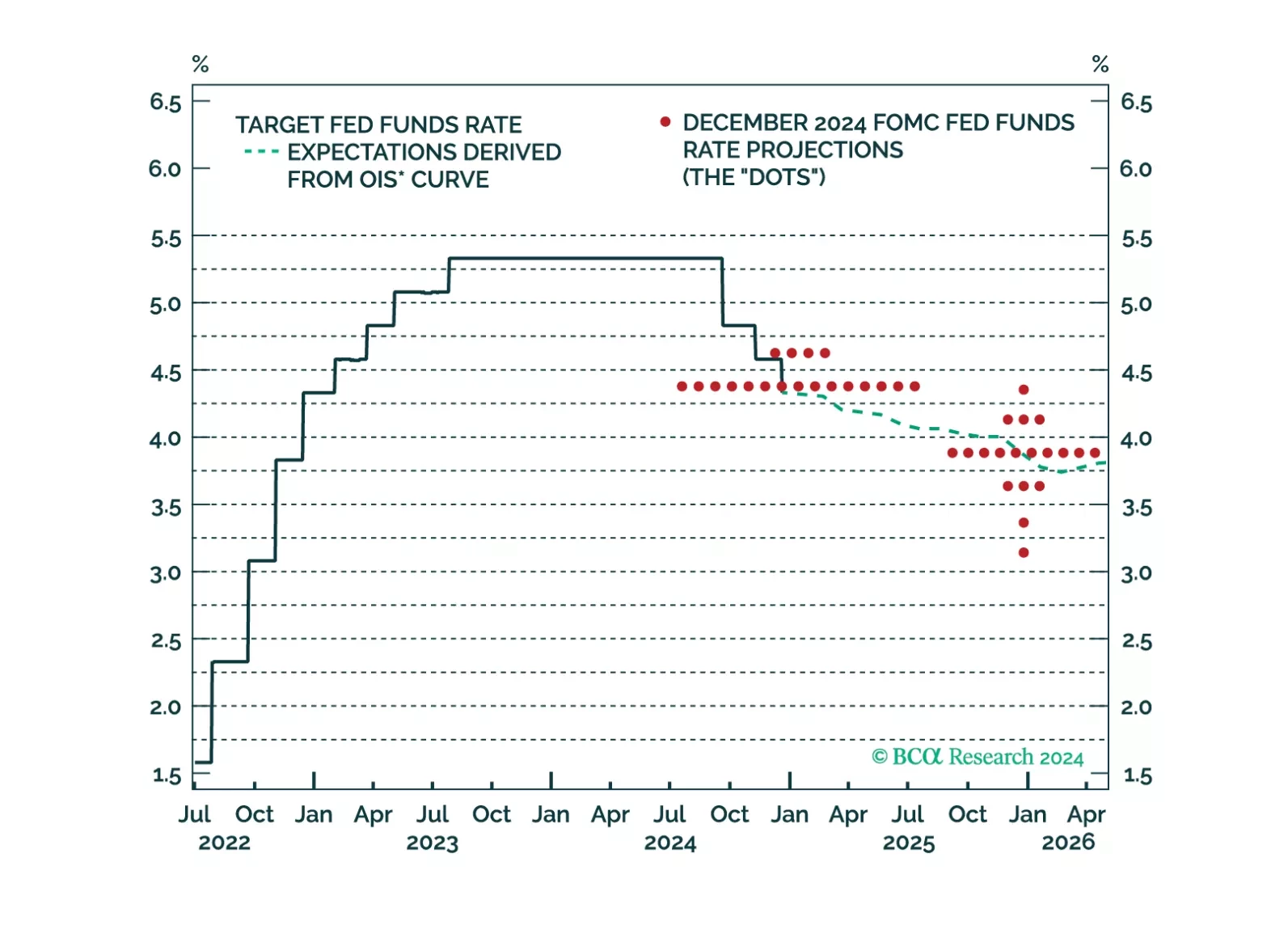

Our outlook for Fed policy in 2025 discusses our expectations for interest rates, the Fed’s balance sheet and the 2025 strategic review.