Monetary

Incredibly, the tone shifted again in February, when Premier Li Keqiang and the PBoC publicly disputed whether the January credit spike represented “flood irrigation-style” stimulus, something Premier Li made clear was to be avoided. These shifts impacted…

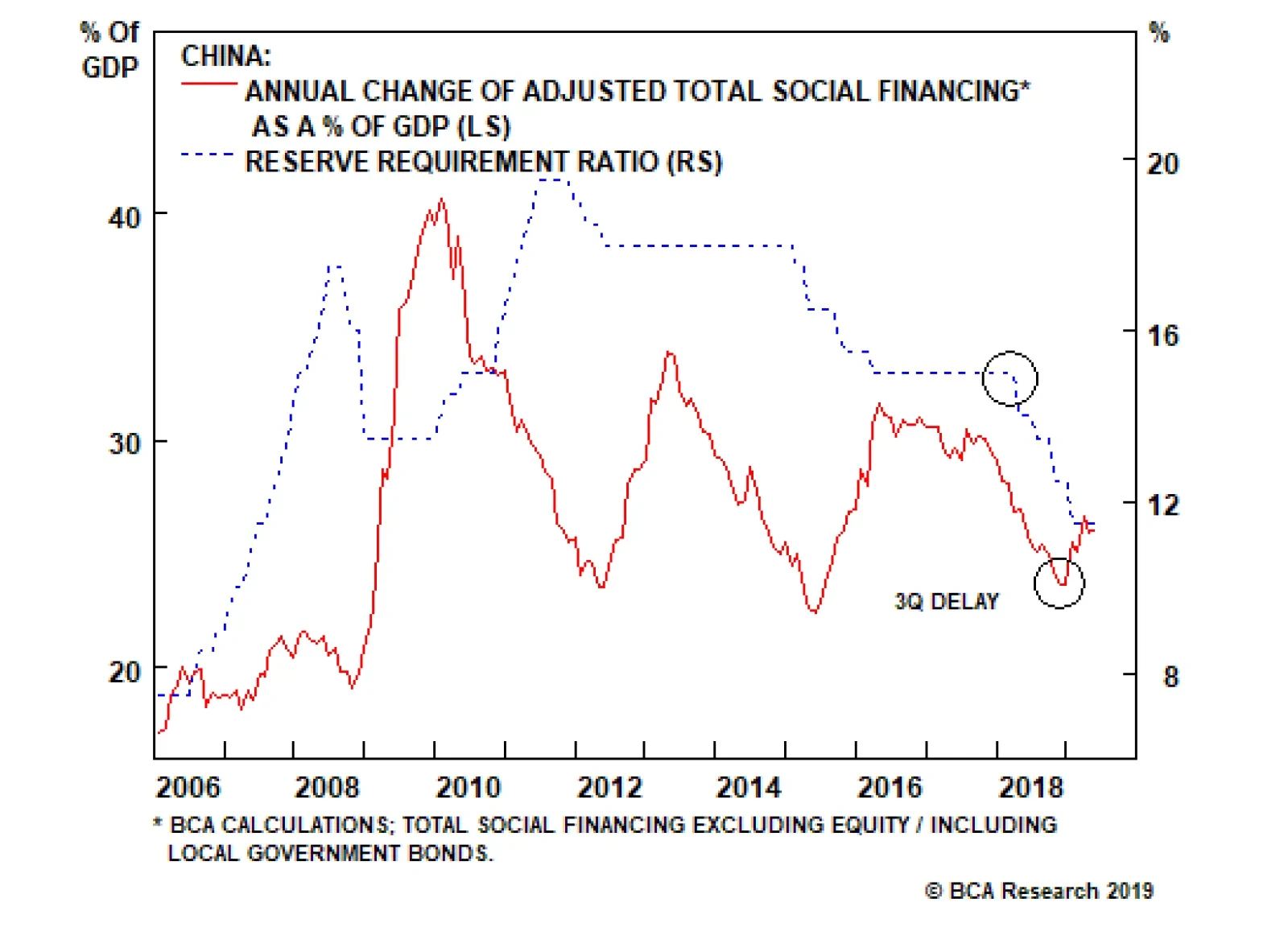

The events of the past year have also demonstrated that the effectiveness of Chinese monetary policy has declined relative to past economic cycles. This, in conjunction with the reluctant/reactive nature of the monetary authorities, has clear implications for…

NOTE: There will be no report on Wednesday, July 17 due to our regular summer break. Highlights Chinese policymakers as well as the People’s Bank of China (PBoC) have historically been reactive, meaning they have typically waited for economic pain to become entrenched before accelerating reflationary measures. The agreement reached at the June G20 Summit to renew trade negotiations with the U.S., while temporary, takes the pressure off the immediate need to further stimulate the economy. While China has the ability to juice the economy, the pain threshold has been raised higher during this cycle, and the country’s leadership has been reluctant to let go of its financial deleveraging campaign. This approach has resulted in a “half measure” stimulus over the past 12 months. The outlook for Chinese stocks is negative over the next three months, as a flip-flop policy approach will increase market volatility. However, over a cyclical (i.e. six- to 12-month) time horizon, we are maintaining a bullish stance toward Chinese stocks in hedged currency terms. Feature Last week marked the first anniversary of the imposition of tariffs on imports from China by the U.S. – an event that has clearly had a lasting and meaningful impact on global economic activity. Last week was also the first anniversary of a significant monetary easing measure: China’s 3-month interbank repo rate fell 90 basis points on July 3, 2018, 3 days before the first tranche of import tariffs took effect. This decline was just under half of what would ultimately occur (the 3-month repo rate fell from 4.5% in early July to 2.4% in early August), and was taken as a sign by many investors that the PBoC had shifted to a maximum reflationary stance (Chart 1). Chart 1Indecisively Falling Interbank Rate

Indecisively Falling Interbank Rate

Indecisively Falling Interbank Rate

However, several facts underscore that either the PBoC did not, in retrospect, move completely toward a pro-growth stance, or that China’s monetary transmission mechanism is seriously impaired. In our view, it is a combination of both: Despite evidence suggesting it should, the PBoC did not cut its benchmark lending rate. The repo rate declined in the third quarter last year on the back of increased liquidity supply in the interbank market. The weighted average lending rate also fell, but not massively, and not by as much as our model had predicted (Chart 2). A pickup in credit expansion has significantly lagged easing. Excluding local government bonds, the general pickup in credit has been modest. Based on this measure of Total Social Financing, new credit to GDP still remains lower today than at any point during the 2015-2016 downturn (Chart 3). Chart 2Lending Rate: Not Much Easing

Lending Rate: Not Much Easing

Lending Rate: Not Much Easing

Chart 3No Strong Re-Leveraging

No Strong Re-leveraging

No Strong Re-leveraging

With the conclusion of the G20 Summit temporarily halting the trade war escalation and implementation of additional tariffs, these observations raise important questions: Will the PBoC be proactive in easing policy? What does this mean for investors over the coming year? The PBoC Will Be Reactive Rather Than Proactive Chart 4Shadow-Banking Crackdown Continues

Shadow-Banking Crackdown Continues

Shadow-Banking Crackdown Continues

In our view, the PBoC’s policy actions last year can at best be described as half-measures, despite the fact that the central bank was quick to reduce interbank interest rates in last July by cutting the reserve requirement ratio (RRR). The reason is that the PBoC clearly maintained macro-prudential/administrative restrictions on shadow banking activity, despite significantly easing liquidity in the interbank market. Chart 4 shows that shadow-banking credit as a share of total adjusted social financing continued to decelerate rapidly throughout 2018. It now accounts for a mere 12% of the stock of total adjusted social financing, by far the lowest point since 2009. This underscores that the PBoC and policymakers more generally have a deep-seated desire to avoid (further) inflating China’s substantial money and credit excesses – a dynamic that we have discussed in previous reports.1 Looking forward, there are three reasons why the PBoC’s reactive nature is unlikely to change in the near term, in addition to policymakers’ concerns about financial system’s excesses. First, the PBoC has historically been a reactive central bank, in a way that goes beyond the now-typical “data dependent” approach of its developed-market peers. Chart 5 provides a close look at China’s previous economic growth cycles and their corresponding credit expansions. The chart highlights that Chinese policymakers tend to stay behind the curve when it comes to monetary easing: In the previous three growth cycles, the first sign of monetary easing (defined as an RRR and/or benchmark lending rate cut) lagged the peak of nominal GDP growth by an average of four quarters. Rate cuts took place not when economic growth peaked, but once economic activity had already weakened considerably (Chart 6). Chart 5Chinese Policymakers Tend To Stay 'Behind The Curve'

Chinese Policymakers Tend To Stay 'Behind The Curve'

Chinese Policymakers Tend To Stay 'Behind The Curve'

Chart 6More 'Pain' Needed For Massive Easing

More 'Pain' Needed for Massive Easing

More 'Pain' Needed for Massive Easing

The same pattern has applied to other monetary easing tools that the PBoC has deployed in the past, including the Medium Lending Facility (MLF), the Targeted Medium-term Lending Facility (TMLF), the standing Lending Facility (SLF), and the Pledged Supplementary Lending program (PSL) – all of which only took shape after the economy had already shown across-the-board weakness. It will take more widespread and entrenched economic weakness for the PBoC to meaningfully ease further. The local government debt-to-bond swap program was also launched well into the 2015 growth downturn. When widespread and sustained weakness in activity emerged, Chinese policymakers responded by “throwing the kitchen sink” at the economy – by moving forward with multiple rate cuts and often creating new forms of easing in an attempt to catalyze a quick rebound. Since the PBoC has already implemented a series of easing measures, we believe it will take more widespread and entrenched weakness in the real economy for the PBoC to meaningfully ease further. Chart 7Chinese Currency Is Under Pressure

Chinese Currency Is Under Pressure

Chinese Currency Is Under Pressure

Second, the PBoC is likely to be reactive because of the potentially negative effects that proactive rate cuts could cause on sentiment towards the RMB. Chart 7 highlights the close historical correlation between the RRR, interest rate differentials and the USD/CNY. USD/CNY was trading at 7.8 the last time the weighted average RRR was at 11%, which was back in 2007. At the current juncture, interest rate differentials already point to a weaker currency. The PBoC has signaled that USD/CNY at 7 is no longer a line in the sand that must be defended, meaning this level is not a hard constraint that would prevent the central bank from cutting either the RRR or the benchmark lending rates if warranted. In fact, a measured depreciation in the RMB would help mitigate some of the blow from increased tariffs. Nevertheless, in an environment where the currency has already weakened significantly, cutting the RRR or the benchmark lending rates quickly or by a large amount could create self-reinforcing expectations of further depreciation. China has implemented a better counter-cyclical mechanism to defend the RMB than it had in 2015-‘16,2 but the potential for capital outflows remains a serious concern.3 Third, the Trump-Xi meeting at the June G20 Summit in Osaka temporarily averted a further escalation of the trade war and additional tariffs. The agreement to continue trade negotiations lacks tangible progress from either side, and thus the “truce” is likely to be short-lived. Chart 8Markets So Far Unimpressed By Stimulus

Markets So Far Unimpressed By Stimulus

Markets So Far Unimpressed By Stimulus

However, as we pointed out in last week’s report,4 the existence of talks is likely to take some pressure off Chinese policymakers’ immediate need to floor the reflation accelerator. Readouts from recent PBoC leadership meetings indicate that speculative excesses in the financial system remain a top concern for Chinese policymakers. China’s onshore market, after rallying by 2% following the good news from the G20 meeting, has given back all its gain (Chart 8). Given that the onshore equity market is extremely sensitive to China’s credit growth, the short-lived rally since the G20 meeting suggests markets have been unimpressed by the authorities’ reflationary efforts so far. Bottom Line: Chinese policymakers have not fully abandoned their financial deleveraging campaign, which President Xi Jinping initiated two years ago. This implies China’s central bank is likely to maintain its reactive approach in further easing monetary policy, and will likely try to avoid going “all-in” on stimulus for as long as possible. The Reduced Effectiveness Of Monetary Policy The events of the past year have also demonstrated that the effectiveness of Chinese monetary policy has declined relative to past economic cycles. This, in conjunction with the reluctant/reactive nature of the monetary authorities, has clear implications for investors over the coming year. When there is lack of clarity in policy interpretation, Chinese banks tend to stay on the sidelines. Chart 9A Long Delayed Credit Response To Monetary Easing

A Long Delayed Credit Response To Monetary Easing

A Long Delayed Credit Response To Monetary Easing

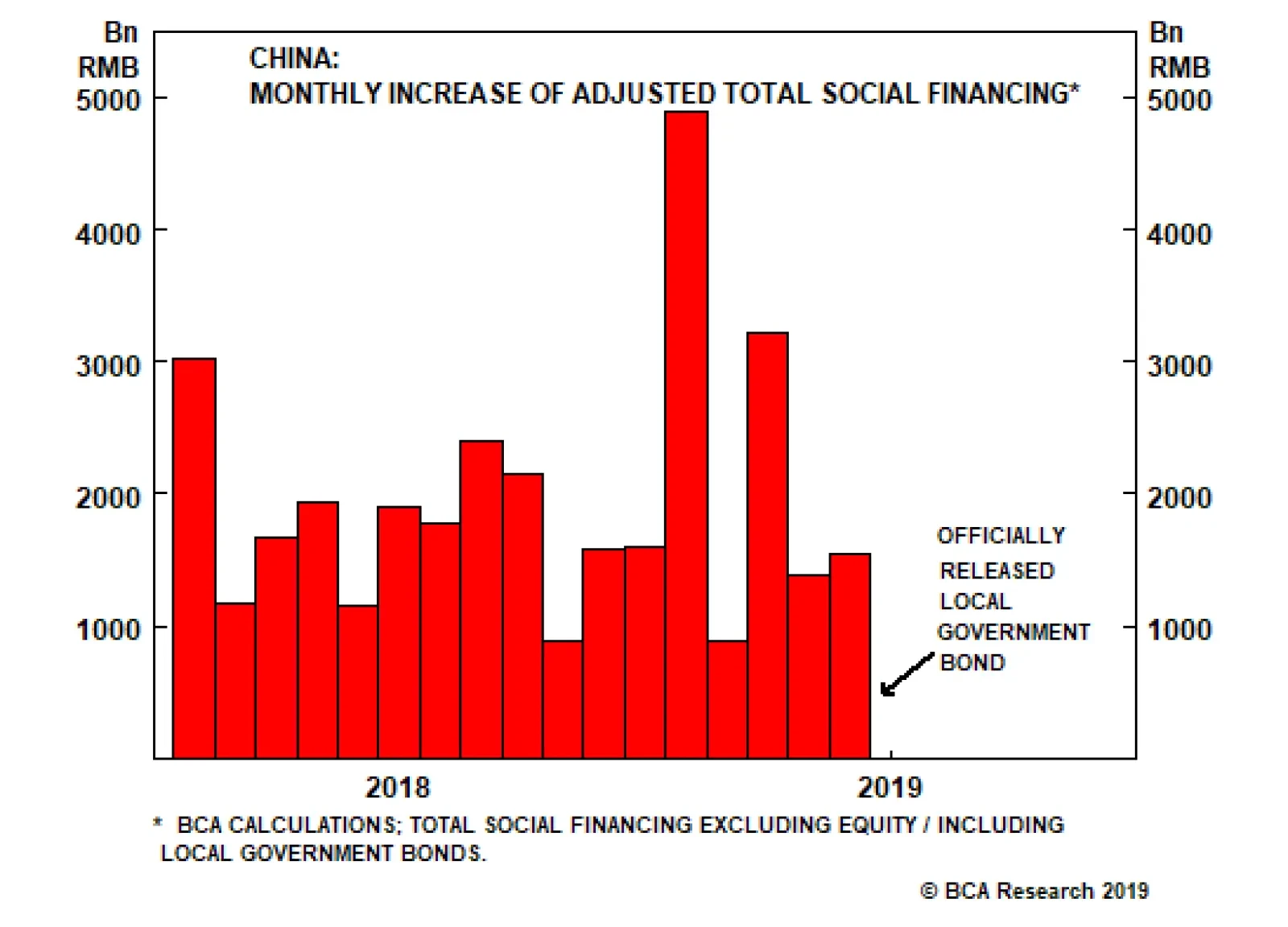

The PBoC has cut the RRR five times since the second quarter of last year, which has freed up a total of 3.35 trillion yuan of liquidity for the banking system5 and has helped spur significant easing in overall monetary conditions. Yet, as we noted earlier, overall credit growth did not pick up until January of this year, lagging the first rate cut by three quarters (Chart 9). Prior to the economic slowdown in 2015-2016, credit growth used to respond to cuts in the RRR almost immediately. In other words, when banking system liquidity was ample, banks historically lent without hesitation. Post-2015, however, this relationship has changed. The PBoC has increasingly been having trouble channeling new liquidity into actual financing for the real economy. A sharp deterioration in reported bank asset quality that began in 2014 is likely part of the explanation,6 but we suspect that more recent extreme policy contradiction – in particular, repeated flip-flopping among authorities between their desire to support growth and their focus on financial stability – has caused economic agents to wait on the sidelines. While monetary conditions eased and the government urged banks to lend (particularly to the private sector) in the second half of 2018, the “prudent” stance coming from Chinese top leaders was little changed, and tight regulations on financial institutions remained in place. This combination did not give banks the confidence to lend. This changed in the first quarter of this year, when new credit creation-to-GDP surged from 23.6% to 25.6%. The surge occurred shortly after the late-December Central Economic Work Conference (CEWC), which sent a clear message that the central government’s policy focus had shifted to “stabilizing aggregate demand.” Incredibly, the tone shifted again in February, when Premier Li Keqiang and the PBoC publicly disputed whether the January credit spike represented “flood irrigation-style” stimulus, something Premier Li made clear was to be avoided.7 Charts 10 and 11 highlight how these shifts impacted credit growth: The first quarter was clearly on track for a 2015-2016-magnitude outcome, whereas April and May saw the path of credit growth return back to a moderate re-leveraging scenario.

Chart 10

Chart 11

To get back on track for a 2015-2016 magnitude reflation, we will need to see June’s credit creation at or above 5 trillion yuan – equivalent to January’s credit numbers (Chart 12). Chart 12'Credit Binge' In June Unlikely

Credit Binge' in June Unlikely

Credit Binge' in June Unlikely

As we go to press, the number for June’s total social financing has not been officially released yet. But the official reading from the total local government bond issuance in June (including both general bond and special-purpose bond issuance), a key component of our adjusted total social financing series, came in at 900 billion yuan. This is three times more than local government bonds issued in May and twice the size of January’s. Nevertheless, January’s bank lending, particularly short-term lending, was unusually large; an episode highly criticized by Chinese leadership as we mentioned above. As PBoC stated in its defense to this criticism, January is “traditionally the biggest month of the year for bank loans due to seasonal factors”. Therefore, without a clear shift in policy signal from China’s top leadership, we do not expect June’s bank lending number to be a repeat of January’s. Instead, June’s total credit impulse will likely put the cumulative progress in credit growth closer to our 27% of nominal GDP assumption (assuming an 8% nominal GDP growth for the remainder of 2019). This would fall into our “half-strength” credit cycle scenario relative to past reflationary episodes. Bottom Line: Ultimately, we do not doubt that Chinese policymakers will be able to engineer a significant re-acceleration in economic activity should they choose to do so. But in order for policymakers to achieve this goal, policy ambiguity and inconsistency will have to be meaningfully reduced. Investment Implications Over a cyclical time horizon, we recommend staying long/overweight Chinese stocks in hedged currency terms. From our perspective, neither policymakers’ bias towards reluctance nor the reduced effectiveness of monetary policy convincingly argue against our bullish stance towards Chinese stocks over a cyclical (i.e. six- to twelve-month) time horizon, but the tactical implications are clearly negative. Over a cyclical horizon, one of two scenarios is likely to unfold: Either downside risk brought on by current tariffs and weakness in domestic demand is contained enough such that Chinese economic activity does not materially decelerate, or the trade dispute escalates into a full-tariff scenario of 25% on all U.S. imports from China that dramatically impacts Chinese growth. In the first scenario, policymakers will likely to continue providing half-measured responses, and unconstrained “across-the-board” easing will not occur. But Chart 13 highlights that Chinese stocks, particularly the investable market, are priced for a much worse economic outcome, suggesting Chinese relative equity performance would trend higher in these circumstances. Chart 13Chinese Stocks Priced In For A Worse Economic Outlook

Chinese Stocks Priced In For A Worse Economic Outlook

Chinese Stocks Priced In For A Worse Economic Outlook

Chart 14Bullish On A Cyclical Horizon, Bearish In The Near Term

Bullish On A Cyclical Horizon, Bearish In The Near Term

Bullish On A Cyclical Horizon, Bearish In The Near Term

In the second scenario, Chinese business and consumer sentiment is likely to collapse and policymakers will be facing high odds of a substantial slowdown in economic activity. This will create the political will necessary for unconstrained “across-the-board” easing, similar to what occurred in 2015-2016. The sharp re-acceleration in economic activity that would result from broad-based stimulus would clearly be positive for listed Chinese earnings per share (Chart 14), meaning the cyclical outlook for Chinese stocks would likely be even more positive than in the first scenario. However, the near-term equity market outlook of the second scenario would be extremely negative, as a financial market meltdown in of itself would likely be required to build the political will necessary to ultimately ease. Bottom Line: For investors with a time horizon of less than three months, we would not recommend a long position in Chinese stocks, neither in absolute terms nor relative to the global benchmark. However, over a strictly cyclical (i.e. six- to 12-month) time horizon, we recommend staying long/overweight Chinese stocks in hedged currency terms. Jing Sima China Strategist JingS@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Special Report, “China: How Stimulating is The Stimulus?”, dated August 8, 2018, available at cis.bcaresearch.com 2 A series of countercyclical measures China implemented in 2016-2017 includes: tightening controls on capital outflows, reducing offshore RMB liquidity supply, raising offshore RMB borrowing costs, and setting a firmer daily reference point for the RMB’s trading band. 3 Please see China Investment Strategy Special Report, “Monitoring Chinese Capital Outflows”, dated March 20, 2019, available at cis.bcaresearch.com 4 Please see China Investment Strategy Weekly Report, “China Macro and Market Review”, dated July 4, 2019, available at cis.bcaresearch.com 5 According to PBoC announcements. 6 Please see China Investment Strategy Weekly Report, “Trade Is Not China’s Only Problem”, dated November 21, 2018, available at cis.bcaresearch.com 7 Please see “Chinese Premier In Rare Spat With Central Bank”, Financial Times. Cyclical Investment Stance Equity Sector Recommendations

Oil prices will remain volatile as markets work through the lingering effects of tighter financial conditions prevailing last year, which, along with extended angst over Sino-U.S. trade tensions, slowed commodity demand growth (Chart of the Week). In 2H19, globally accommodative monetary policy and fiscal stimulus will revive demand for industrial commodities, particularly in EM economies. This will be most apparent in oil markets, where we continue to expect demand growth to strengthen going into 2020, aided in part by a weaker USD. On the supply side, this week’s extension of OPEC 2.0’s production cuts into 1Q20 means growth will remain constrained. Prices will rise, and forward curves, particularly for Brent, will steepen as refiners are forced to draw inventories to meet product demand.1 We continue to expect Brent to average $73/bbl this year and $75/bbl next, respectively. We expect WTI to trade $7/bbl and $5/bbl below that this year and next. Chart of the WeekEasing Financial Conditions Will Spur Oil Demand

Easing Financial Conditions Will Spur Oil Demand

Easing Financial Conditions Will Spur Oil Demand

Highlights Energy: Overweight. Venezuela’s oil production reportedly recovered to 1.1mm b/d in June. Most of the increased production found its way to China, which accounted for just under 60% of crude and product exports.2 Given its modus operandi, we believe OPEC 2.0 likely will accommodate higher production in Venezuela by reducing production in other member states, keeping overall output relatively constant. Base Metals: Neutral. Copper treatment and refining charges fell to new lows at the end of last week, with Fastmarkets MB’s Asia – Pacific TC/RC index recording its lowest level on record at $52.40/MT ($0.0524/lb).3 TC/RC levels fall when supplies are low, as refiners have to discount their services to attract concentrate supplies. Elsewhere, workers at Codelco’s Chuquicamata copper mine agreed to a new contract last week, ending a brief strike. Precious Metals: Neutral. Gold’s rally resumed this week, reflecting investors’ expectations for expanded central-bank accommodation globally, which, all else equal, will keep interest rates lower for longer. The Fed's dovish turn, in particular, will weaken the USD later this year, which will be positive for EM commodity demand, the engine for commodity demand growth globally. Ags/Softs: Underweight. The USDA reported 56% of corn in the ground was in good to excellent condition last week, vs. 76% of the crop last year. For soybeans, 54% of the U.S. crop was in good or excellent condition, vs. 71% last year. The USDA’s Crop Progress reports cover 92% and 95% of total acreage planted in the U.S., respectively. Feature Oil prices will remain volatile over the short term, as markets transition from tighter monetary conditions to a more accommodative global backdrop (Chart 2). Based on our research into the drivers of oil-price volatility, this should translate into a less stressful pricing environment for industrial commodities generally, base metals and oil in particular (Chart 3).4 Chart 2Volatility Indicators Are Moderating

Volatility Indicators Are Moderating

Volatility Indicators Are Moderating

Chart 3Signaling Oil Price Volatility Will Fall

Signaling Oil Price Volatility Will Fall

Signaling Oil Price Volatility Will Fall

Much of the current oil-price volatility is being driven by worries over damage to aggregate global demand and growth expectations in the wake of the Sino-U.S. trade war, and by what now appears to be a too-aggressive posture by central banks implementing rates-normalization policies last year. Both of these can affect consumption and investment locally and globally.5 Fear That Real Demand Will Weaken At present, any indication real demand is faltering – e.g., weaker manufacturing PMIs – gives industrial commodities an excuse to sell off (Chart 4). In the case of the Sino-U.S. trade war, presidents Xi and Trump appear to have agreed to re-start trade negotiations. Markets are not going to be terribly concerned with the specifics of a trade deal between the U.S. and China, but it does appear some rollback in U.S. tariffs will be necessary for a trade deal – perhaps in exchange for greater access to Chinese markets. However, our geopolitical strategists make the odds of a trade deal by the time U.S. elections roll around 1:3. Our colleagues in BCA Research’s Global Investment Strategy note, “The specifics of the deal are less important than there being a deal – any deal – that avoids a major escalation. Ultimately, the distinction between a ‘small’ trade war and a ‘moderate’ trade war is a function of how high tariffs end up being. Tariffs are taxes, and while no one likes to pay taxes, they are a familiar part of the global capitalist system.”6 As for monetary policy, major central banks are embarked on a coordinated effort to reverse falling inflation expectations, and will be vigorously stimulating their money supply and credit growth over the balance of the year. In addition, fiscal stimulus globally – in the U.S. and China most prominently – will boost real demand for industrial commodities, particularly oil and base metals.7 Monetary and fiscal stimulus operates with a lag, which is why we continue to expect its more visible for commodity demand to become apparent in commodity prices later in 2H19 and next year. This lagged effect can be seen in our expectation for the evolution of EM import volumes to year end, which we estimate using data compiled the CPB World Trade Monitor (Chart 5). EM import volumes are closely tied to the evolution of EM income, which drives global commodity demand.8 Chart 4Globally, The Real Economy Has Slowed

Globally, The Real Economy Has Slowed

Globally, The Real Economy Has Slowed

Chart 5EM Imports and Income Will Rebound

EM Imports and Income Will Rebound

EM Imports and Income Will Rebound

In our modeling of supply-demand balances and prices, we accounted for the reduced EM GDP growth brought about by more restrictive monetary policy last year and the slowdown in global trade in our most recent forecast. In our base case, we took our expected global oil-demand growth this year down to 1.35mm b/d from 1.5mm b/d earlier, and to 1.55mm b/d next year from 1.6mm b/d previously. These adjustments reduced our price expectation for Brent crude oil slightly to $73/bbl this year and $75/bbl next year, with WTI trading $7/bbl and $5/bbl below those respective levels (Chart 6). Chart 6Our Forecasts Reflect Lower Demand, Tighter Supply

Our Forecasts Reflect Lower Demand, Tighter Supply

Our Forecasts Reflect Lower Demand, Tighter Supply

Oil Markets Will Get Tighter For all of the concern over real demand, prompt demand remains stout relative to available supply, as can be seen in the backwardations for global benchmark crude oil prices (Chart 7). This week’s extension of OPEC 2.0’s production cuts into 1Q20 means supply growth will remain constrained, which, given our demand expectation, will tighten balances globally (Chart 8).9 Chart 7Global Oil Benchmarks Remain Backwardated

Global Oil Benchmarks Remain Backwardated

Global Oil Benchmarks Remain Backwardated

Chart 8Oil Supply Demand Balances Will Tighten

Oil Supply Demand Balances Will Tighten

Oil Supply Demand Balances Will Tighten

Chart 9Oil Inventories Will Fall, As Supply Is Constrained

Oil Inventories Will Fall, As Supply Is Constrained

Oil Inventories Will Fall, As Supply Is Constrained

As balances tighten in the wake of global fiscal and monetary stimulus, oil prices will rise, and forward curves, particularly for Brent, will steepen as refiners are forced to draw inventories to meet product demand (Chart 9). For this reason we remain long September – December 2019 Brent vs. short September – December 2020 Brent, expecting backwardation to increase.10 Bottom Line: We remain constructive toward oil markets, as they transition to a more accommodative monetary backdrop globally. Combined with fiscal stimulus in the U.S. and China in particular, demand will remain supported in 2H19 and 2020. The extension of OPEC 2.0’s production-cutting deal will tighten markets, forcing refiners to draw down inventories. Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Footnotes 1 OPEC 2.0 is a name we coined for the OPEC/non-OPEC oil-producing coalition led by the Kingdom of Saudi Arabia (KSA) and Russia. Their agreement to extend production cuts of 1.2mm b/d into 1Q19 was announced this week in Vienna. Please see OPEC/non-OPEC rolls over oil output cuts for 9 months published by S&P Global Platts on July 2, 2019. Compliance with these cuts has been higher by ~ 400k b/d in 1H19 by our reckoning. 2 Please see Venezuela's June oil exports recover to over 1 million bpd: data published July 2, 2019, by reuters.com. 3 Please see Copper concs TCs drop marginally on traders purchase; Cobre Panama’s fresh supply hits market published by Fastmarkets MB June 28, 2019. 4 We are using “volatility” in the technical sense here – i.e., the standard deviation of per-annum returns. We have shown this can be explained by different variables, including EM volatility; U.S. financial conditions – as seen in the St. Louis Fed’s financial-stress index; and by speculative positioning, which tends to follow the evolution of prices as news flows change. For discussions of our volatility modeling, including the construction of Working’s T index, please see Specs Back Up The Truck For Oil, published April 26, 2018, and Feedback Loop: Spec Positioning & Oil Price Volatility, published May 10, 2018, by BCA Research’s Commodity & Energy Strategy. Both are available at ces.bcaresearch.com. 5 Please see The economic implications of rising protectionism: a euro area and global perspective published by European Central Bank April 24, 2019. 6 Please see Third Quarter 2019 Strategy Outlook: The Long Hurrah, BCA Research’s global macro outlook for 3Q19, published June 28, 2019, by our Global Investment Strategy. It is available at gis.bcaresearch.com. The larger issues that will have to be addressed at some point in the future are non-tariff barriers to trade, exemplified by Huawei’s exclusion from access to U.S. technology on national security grounds. An expansion of such non-tariff barriers would strand huge amounts of capital globally, which likely would lead to a global recession. 7 Our chief global strategist, Peter Berezin, notes in the above-cited BCA Research third-quarter outlook that Fed policy is expected to remain ultra-accommodative into late 2021, which will push the USD lower later this year, and will support commodity demand generally. 8 We use an FX-based model to estimate EM import volumes to year end off the CPB data. 9 We will be updating our Venezuela and OPEC 2.0 production estimates to reflect this development in our July global oil market balance publication later this month. 10 We have been long 2H19 Brent vs. short 2H20 Brent since February 28, 2019. The July and August pieces of this position returned 222.7% and 273% since inception. We remain long the September – December exposure. Investment Views and Themes Recommendations Strategic Recommendations TRADE RECOMMENDATION PERFORMANCE IN 2019 Q2

Image

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Image

Highlights The EM equity and currency rebounds should be faded. When corporate profits are contracting, lower interest rates typically do not preclude equity prices from dropping. This is the case in EM and China. Our leading indicators for the Chinese business cycle continue to point to intensifying profit contraction in both China and EM. The ratio of global broad money supply to the current value of securities worldwide is at an all-time low. This casts doubt on the “too much money chasing too few assets” hypothesis. Feature Chart I-1EM Share Prices: Decision Time

EM Share Prices: Decision Time

EM Share Prices: Decision Time

EM share prices are at a critical juncture (Chart I-1). Their ability to hold their recent lows and break above their April highs will signify that a sustainable cyclical rally is in the making. Failure to punch through April’s highs will pose a major breakdown risk. In brief, EM is facing a make-it-or-break-it moment. Fundamentally, the outlook for EM risk assets and currencies largely hinges on economic growth in general and corporate profits in particular. In our June 20 report, we illustrated that the primary drivers of EM risk assets and currencies have historically been their business cycles and profit growth – not U.S. interest rates. Falling interest rates are positive for share prices when profits are expanding, even if at a slower rate. However, when corporate profits are contracting, lower interest rates typically do not preclude equity prices from dropping. Hence, lower global interest rates in of themselves are not a sufficient condition to foster a sustainable cyclical EM rally. As to EM corporate profits, the rate of their contraction will continue deepening. Since early this year, we have been arguing that expectations of recovery in the Chinese economy and global trade are unwarranted. That is why BCA’s Emerging Markets Strategy team contends that EM risk assets and currencies, as well as China-plays, face the risk of a breakdown. This differs from BCA’s house view, which is positive on global risk assets in general. Global And Chinese Business Cycles: No Recovery So Far Chart I-2Chinese A-Share EPS Is Heading Into Contraction

Chinese A-Share EPS Is Heading Into Contraction

Chinese A-Share EPS Is Heading Into Contraction

The rebound in EM risk assets and currencies since last December has occurred despite no improvement in both China’s business cycle and global trade, and despite the deepening contraction in EM corporate profits. Since early this year, we have been arguing that expectations of recovery in the Chinese economy and global trade are unwarranted. So far, our baseline economic view has played out – mainland growth has been rather weak, and global trade has contracted. Yet EM financial markets have done better than we had anticipated. China’s domestic industrial new orders lead Chinese A-share earnings per share growth rate by about nine months and point to intensifying profit slump into early 2020 (Chart I-2). Furthermore, China’s adjusted narrow money(M1+)1 growth leads Chinese investable stocks earnings per share (EPS) by about nine months, and is also pointing to further compression (Chart I-3). Finally, Korea’s exports are shrinking, as are EM EPS (Chart I-4, top panel). Chart I-3Chinese Investable Companies' EPS Is Already Shrinking

Chinese Investable Companies' EPS Is Already Shrinking

Chinese Investable Companies' EPS Is Already Shrinking

Chart I-4Korean Exports And EM EPS

Korean Exports And EM EPS

Korean Exports And EM EPS

Notably, both Korean exports values and EM EPS in U.S. dollars terms are on par with their early 2011 levels (Chart I-4, bottom panel). This indicates that neither Korean exports nor EM EPS have expanded sustainably over the past eight years. Chart I-5Global Stocks Did Not Lead Global PMI Historically

Global Stocks Did Not Lead Global Manufacturing PMI Historically

Global Stocks Did Not Lead Global Manufacturing PMI Historically

Is it possible that the current gap between global share prices and global manufacturing is due to the fact that financial markets are forward-looking and lead business cycles? Historical evidence suggests that global share prices have not led the global manufacturing PMI, as exhibited in Chart I-5. In fact, global share prices have actually been coincident with the global manufacturing PMI not only throughout this decade but before that as well. The de-coupling between share prices and the manufacturing PMI is currently also present in EM, albeit in a less-striking form. Chart I-6 illustrates that the EM manufacturing PMI has slipped below 50 line, yet share prices have recently rebounded and sovereign spreads have tightened. In a nutshell, the divergence between global share prices and the global manufacturing PMI is unprecedented. This cannot be explained by falling global bond yields either. The latter were falling in the previous business cycle downtrends (2011-12 and 2015), yet share prices did not deviate from the global manufacturing PMI during those episodes (Chart I-5). Chart I-6EM PMI And EM Risk Assets

EM PMI And EM Risk Assets

EM PMI And EM Risk Assets

Chart I-7The Rest Of World's Exports To China Will Continue Shrinking

The Rest Of Worlds' Exports To China Will Continue Shrinking

The Rest Of Worlds' Exports To China Will Continue Shrinking

It seems that the global equity and credit markets expect an imminent recovery in the global business cycle in general and in China in particular. As we elaborated in the previous reports, the current global manufacturing recession stems primarily from China. Our leading indicators of the mainland business cycle suggest that more growth disappointments are likely before China’s growth and other economies’ shipments to the mainland hits a bottom (Chart I-7). For example, Korea’s exports to China in June were still dropping by 24% from a year ago. The primary reason for the lack of revival in growth is that China’s stimulus efforts have so far not been large enough, and the marginal propensity to spend among households and companies is diminishing, offsetting the positive effect of the stimulus, as we have discussed in previous reports. Will the recent G20 trade truce between the U.S. and China boost business confidence worldwide and in China? In our view, it is unlikely to produce a quick and meaningful recovery in business confidence among multinational companies and Chinese businesses. Corporate managers have probably come to realize that the U.S.-China row is not about import tariffs but rather geopolitical confrontation between the existing hegemon and a rising superpower. Hence, there is no easy solution that will satisfy both parties. An acceptable resolution for China will be unacceptable for the U.S., and vice versa. Hence, it will be hard to find a formula that gratifies both sides politically and economically. Overall, we reckon there are low odds in the next six months of an agreement between the U.S. and China that removes tariffs, addresses structural issues and satiates both nations. Korea’s exports are shrinking, as are EM EPS. Finally, even though the S&P 500 is hovering around its previous highs, under-the-surface dynamics have been less upbeat. Specifically, the equal-weighted share price index of U.S. high-beta stocks in cyclical sectors such as industrials, technology and consumer discretionary versus the S&P 500 has been tame and has not yet broken above its 200-day moving average (Chart I-8, top panel). The same holds true for the relative performance of an equal-weighted stock index of global cyclical sectors such as industrials, materials and semiconductors against the overall global equity benchmark (Chart I-8, bottom panel). Conversely, despite its recent setback, the U.S. dollar has technically not yet broken down (Chart I-9, top panel). In fact, our composite momentum indicator for the broad trade-weighted dollar has troughed at zero – a sign that downside is limited and another up-leg will likely emerge soon (Chart I-9, bottom panel). Chart I-8Cyclical Stocks Have Been Underperforming

bca.ems_wr_2019_07_04_s1_c8

bca.ems_wr_2019_07_04_s1_c8

Chart I-9The U.S. Dollar Has Technically Not Broken Down

The U.S. Dollar Has Technically Not Broken Down

The U.S. Dollar Has Technically Not Broken Down

Bottom Line: The EM equity and currency rebounds should be faded. As EM currencies depreciate, sovereign and corporate credit spreads will likely widen. Asset allocators should continue underweighting EM equities and credit markets relative to their DM peers. Too Much Money Chasing Too Few Assets? Many investors identify “liquidity” as the main reason why global equity and credit markets have done so well this year, despite the relapsing global business cycle. Yet there are as many definitions of “liquidity” as there are investors. Many commentators use the term “liquidity” to denote balance sheet expansion by global central banks. As part of their quantitative easing programs, central banks in the U.S., U.K., Japan, the euro area, Switzerland and Sweden have expanded their balance sheets enormously. In line with their asset expansion, their liabilities – the monetary base, consisting primarily of commercial banks’ excess reserves – have also mushroomed. Nevertheless, broad money supply has grown only modestly in these economies.2 The principal reason behind this phenomenon has been a collapse in the money multiplier due to both banks’ unwillingness to boost lending proportionally to their swelling excess reserves, and a persistent lack of demand for credit among households and businesses. This computation casts doubt on the “too much money chasing too few assets” hypothesis. Broad money supply includes all types of deposits at commercial banks and cash in circulation. Crucially, it does not include commercial banks’ excess reserves at central banks. This differentiation between broad money and excess reserves at central banks is vital because excess reserves are not used to purchase goods, services or assets/securities. Hence, a true measure of purchasing power for assets, goods and services is broad money supply. Consistently, the pertinent liquidity ratio for financial markets can be computed by dividing global broad money supply by the value of all securities outstanding excluding those owned by central banks. The top panel of Chart I-10 depicts the ratio of the sum of broad money supply in 12 economies3 - excluding China - to the market value of investable global equities and bonds. The latter is calculated as the market cap of the Datastream World Equity Index plus the market value of the Barclays Aggregate Bond Index, excluding securities owned by central banks (Chart I-11). Bonds include both government and corporate issues. Chart I-10Comparing Global Broad Money And Market Value Of Outstanding Securities

Comparing Global Broad Money And Market Value Of Outstanding Securities

Comparing Global Broad Money And Market Value Of Outstanding Securities

Chart I-11Broad Money, Securities Absorbed By QEs And Value Of Outstanding Securities

Broad Money, Securities Absorbed By QE And Value Of Outstanding Securities

Broad Money, Securities Absorbed By QE And Value Of Outstanding Securities

We exclude China from this calculation because its money supply (deposits) is not internationally “mobile” – i.e., due to capital controls, Chinese residents cannot convert their renminbi deposits to other currencies, or use them to purchase international securities. Likewise, we exclude Chinese on-shore equity and bond markets from the calculation because they are not easily accessible to all foreign investors. This broad money supply-to-asset values ratio can be regarded as a rough proxy for available liquidity for financial markets.4 Our interpretation is that a lower ratio means investors have lower cash balances relative to the value of financial assets they hold, and vice versa. Interestingly, the ratio of global broad money to the current value of securities worldwide is at an all-time low (Chart I-10, top panel). Hence, this computation casts doubt on the “too much money chasing too few assets” hypothesis. By flipping this ratio, we compute the ratio of market value of all investable securities (excluding the ones owned by central banks) to broad money supply (Chart I-10, bottom panel). It is at all-time high entailing that the market value of globally investable publically-traded securities has expanded much more than global broad money supply/deposits. Bottom Line: We recognize that this is a simplistic macro exercise, and a more comprehensive methodology is required to compute global cash balances that are available to purchase securities worldwide. However, at minimum the above casts doubt on the hypothesis that “too much money is chasing too few assets”. Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Footnotes 1 M1+ is calculated as M1 plus household demand deposits and deposits at third-party payment platforms. 2 Note that when a central bank purchases securities from commercial banks, this operation originates excess reserves, but not a new deposit at commercial banks. However, when a central bank acquires securities from a non-bank entity, such as a pension fund or an insurance company, this transaction creates both excess reserves and a bank deposit that did not exist before. Hence, QE programs have created some deposits but less so than excess reserves. 3 Economies included into this aggregate are the U.S., the euro area, the UK, Japan, Canada, Australia, Switzerland, Sweden, Korea, Taiwan, Hong Kong and Singapore. 4 This calculation does not strip out transactional demand for money, i.e., how much money is required to finance regular economic activity. Given transactional demand for money is not stable, it is hard to estimate and adjust for it. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Chart I-

Highlights Corporate Spreads: The Fed’s dovish pivot prolongs the period of time before the yield curve inverts, thus extending the window for corporate bond outperformance. Investors should remain overweight corporate bonds, with a preference for securities rated Baa and below, where spreads remain wide relative to our fair value estimates. Yield Curve: Investors should barbell their U.S. bond portfolios, favoring long-maturity (> 10 years) and short-maturity (< 2 years) securities while avoiding the 5-year and 7-year notes. This positioning will boost average portfolio yield and will benefit from any future hawkish re-assessment of Fed policy. MBS: Lower mortgage rates have led to a jump in mortgage refinancings and wider MBS spreads. However, MBS spreads remain quite low compared to history. Maintain a neutral allocation to MBS in U.S. bond portfolios. Feature Last December, we laid out our key fixed income themes for 2019 in a Special Report.1 In that report we also introduced a framework for splitting the economic cycle into three phases based on the slope of the yield curve. Specifically, we use the 3-year/10-year Treasury slope to divide each cycle into the following three phases:2 Phase 1 runs from the end of the last recession until the 3/10 slope flattens to below 50 bps. Phase 2 encompasses the period when the 3/10 slope is between 0 bps and 50 bps. Phase 3 begins after the 3/10 slope inverts and ends at the start of the next recession. Clearly, as is illustrated in Chart 1, we are smack dab in the middle of a Phase 2 environment. This has implications for how we should think about positioning a U.S. bond portfolio. Chart 1Firmly In Phase 2

Firmly In Phase 2

Firmly In Phase 2

What Makes The Middle Phase Awkward? Table 1 shows annualized excess returns for Treasuries and corporate bonds (both investment grade and high-yield) in each phase of every cycle stretching back to the mid-1970s. Treasury excess returns are calculated relative to cash, as a proxy for the returns from taking duration risk. Corporate excess returns are relative to a duration-matched position in Treasury securities. Table 1Bond Performance In Different Yield Curve Regimes

The Long Awkward Middle Phase

The Long Awkward Middle Phase

A look at Table 1 reveals why we call Phase 2 the “awkward” middle phase of the cycle. The excess returns earned from taking both duration and corporate spread risk tend to be underwhelming. On duration, we observe that in three of the four complete cycles in our sample, Treasury excess returns are lowest in Phase 2. This lines up well with intuition. The flatter yield curve means that Treasuries offer a lower term premium in Phase 2 than in Phase 1. Meanwhile, Phase 3 periods tend to coincide with rapid Fed rate cuts, and thus large capital gains. Phase 2 periods, in contrast, often contain Fed tightening cycles. On corporate credit, we observe that excess returns tend to be lower in Phase 2 than in Phase 1, but are usually still positive. Returns tend not to turn consistently negative until after the 3/10 slope inverts and we enter Phase 3. Overall, if we know nothing other than that we are in Phase 2 of the cycle, our results suggest that we should take less duration risk in our portfolio than in Phases 1 or 3. Overall, if we know nothing other than that we are in Phase 2 of the cycle, our results suggest that we should take less duration risk in our portfolio than in Phases 1 or 3. The results also suggest that we should prefer corporate credit over Treasuries, though to a lesser extent than in Phase 1. What Makes The Middle Phase Long? In last December’s Special Report, we argued that the U.S. economy would remain in a Phase 2 environment for a long time, at least until late 2019. Our reasoning was that, in the absence of inflationary pressures, the Fed would be reluctant to tighten policy enough to invert the 3/10 curve. The Fed’s recent dovish pivot, and the resultant steepening of the curve (see Chart 1), only prolongs the current Phase 2 environment. We now think it will be well into 2020, and possibly later, before the 3/10 slope inverts and the economy enters Phase 3. One obvious investment implication of an extended Phase 2 environment is that we should remain overweight corporate bonds relative to duration-matched Treasuries. However, we also need to consider valuation before drawing too firm of a conclusion. Charts 2A and 2B show spreads for each corporate credit tier, encompassing both investment grade and high-yield, along with our spread targets. The spread targets are the median levels observed in prior Phase 2 environments, adjusted for changes in the average duration of the bond indexes over time.3 The charts reveal that Aaa-rated bonds already look expensive, while Aa and A-rated bonds are close to fairly valued. Baa-rated bonds are 13 bps cheap relative to our target, while the high-yield credit tiers offer significantly more value. Chart 2AInvestment Grade Spread Targets

Investment Grade Spread Targets

Investment Grade Spread Targets

Chart 2BHigh-Yield Spread Targets

High-Yield Spread Targets

High-Yield Spread Targets

As discussed in last week’s report, the Fed’s dovish pivot will cause corporate spreads to tighten in the near-term, but it will take longer before Treasury yields respond by moving higher.4 For Treasury yields to move higher, investors must first become convinced that the Fed’s reflationary efforts are translating into stronger global economic growth. Ultimately, we expect this will occur in the second half of this year and Treasury yields will be higher 12 months from now, as the Fed will fail to deliver the 92 bps of rate cuts that are currently priced. The flat yield curve means that the yield give-up is small, and we expect global growth to improve in the second half of the year. Bottom Line: The Fed’s dovish pivot prolongs the period of time before the yield curve inverts, thus extending the window for corporate bond outperformance. Investors should remain overweight corporate bonds, with a preference for securities rated Baa and below, where spreads remain wide relative to our fair value estimates. Investors should also keep portfolio duration low. The flat yield curve means that the yield give-up is small, and we expect global growth to improve in the second half of the year. Barbell Your Portfolio Chart 3Barbell Your Portfolio

Barbell Your Portfolio

Barbell Your Portfolio

For those unwilling or unable to deviate portfolio duration significantly from benchmark, there is another way to bet on the Fed delivering fewer cuts than are currently priced into the market. Investors can run a barbelled portfolio, favoring short-maturity (< 2 years) and long-maturity (> 10 years) securities, while avoiding the belly (5-year/7-year) of the curve. This sort of positioning has a few advantages. First, since the financial crisis, the yield curve has tended to steepen out to the 5-year/7-year point and flatten beyond that point whenever our 12-month Fed Funds Discounter rises (Chart 3). Conversely, whenever the market prices in more cuts/fewer hikes and our discounter falls, the yield curve has flattened out to the 5-year/7-year maturity point and steepened beyond that point. This correlation has been very consistent during the past few years, and continued to hold during the most recent decline in rate expectations. Notice that the 5-year yield has fallen by more than either the 2-year or 10-year yields since our Discounter's early-November peak (Table 2). Table 2The Belly Of The Curve Is Most Sensitive To Rate Expectations

The Long Awkward Middle Phase

The Long Awkward Middle Phase

The upshot is that, if rate expectations rise during the next 12 months, as we expect, the 5-year and 7-year notes will endure the most damage. The second reason why a barbelled portfolio makes sense is that valuation is very attractive. Chart 4 shows that the 5-year yield is below the yield on a duration-matched 2/10 barbell. It also shows that this 2/5/10 butterfly spread is very low relative to our model’s fair value.5 Chart 42/10 Barbell Is Attractive Versus 5-Year Bullet

2/10 Barbell Is Attractive Versus 5-Year Bullet

2/10 Barbell Is Attractive Versus 5-Year Bullet

We run similar fair value models for every possible bullet/barbell combination along the yield curve, and barbells appear universally cheap (see Appendix). Bottom Line: Investors should barbell their U.S. bond portfolios, favoring long-maturity (> 10 years) and short-maturity (< 2 years) securities while avoiding the 5-year and 7-year notes. This positioning will boost average portfolio yield and will benefit from any future hawkish re-assessment of Fed policy. MBS & Housing: The Implications Of Lower Mortgage Rates Alongside bond yields, mortgage rates have fallen sharply during the past few months, a trend that has important implications for both MBS spreads and future housing data. We consider the outlook for both. MBS Spreads Lower mortgage rates encourage homeowners to refinance their loans, and any increase in refinancing activity puts upward pressure on MBS spreads. Not surprisingly, as mortgage rates have declined we have seen a jump in the MBA Refinance Index and a widening of nominal MBS spreads (Chart 5). Chart 5MBS Spreads Still Historically Tight

MBS Spreads Still Historically Tight

MBS Spreads Still Historically Tight

While spreads have widened somewhat, they remain low compared to history (Chart 5, top panel). As such, we do not see a compelling buying opportunity in MBS. This is especially true relative to corporate credit where spreads are more attractive. Chart 6Limited Upside For Refis

Limited Upside For Refis

Limited Upside For Refis

With the mortgage rate now below 4%, our rough calculation suggests that approximately 44% of the Bloomberg Barclays Conventional 30-year MBS index is refinanceable. A regression of the MBA Refi Index versus the refinanceable share suggests a fair value of 2014 for the Refi Index, slightly above its actual level of 1950 (Chart 6). We also calculate that a further drop in the mortgage rate to below 3.5%, where it troughed in mid-2016, would increase the refinanceable share to 77%. Our regression translates this 77% share to a level of 3309 on the Refi Index. It should be noted that when the refinanceable share rose to 77% in 2016, the MBA Refi Index peaked at 2870. This means that our simple regression analysis probably overstates the surge in refis that would occur if mortgage rates fell another 50 bps. In addition, we think it’s unlikely that mortgage rates will actually fall back to 3.5%, as they did in 2016, and as such, we are hesitant to position for further MBS spread widening. The improvement in housing actitivty is not uniform across all indicators. We recommend maintaining a neutral allocation to MBS for now. If mortgage rates drop and spreads widen further in the near-term, then a buying opportunity may present itself. Housing Activity Chart 7Housing Activity: A Mixed Picture

Housing Activity: A Mixed Picture

Housing Activity: A Mixed Picture

The drop in mortgage rates will also have a significant impact on housing activity data. This is important because, as we have demonstrated in prior reports, housing activity data – particularly single-family housing starts and new homes sales – are reliable indicators of U.S. recessions and interest rates.6 By all measures, housing activity weakened significantly as mortgage rates surged in 2018. But it has improved somewhat now that mortgage rates have declined. However, the improvement is not uniform across all indicators (Chart 7): New home sales jumped sharply early this year, then fell back more recently. The current trend is neutral, with the latest monthly print very close to the 12-month moving average (Chart 7, top panel). Housing starts and permits are both trending below their respective 12-month moving averages, though by less than in 2018 (Chart 7, panel 2 & 3). Existing home sales have popped, and are now exerting upward pressure on the 12-month average (Chart 7, panel 4). Likewise for mortgage purchase applications (Chart 7, panel 5). Homebuilders also report that lower mortgage rates have led to a jump in sales activity (Chart 7, bottom panel). With mortgage rates still low, the tentative rebound in housing activity data should continue in the coming months. Looking further out, we see significantly more upside in single-family housing starts and new home sales as builders shift construction toward lower-priced properties. The Bifurcated Housing Market Beyond the large swings in mortgage rates, another trend has significantly influenced housing activity in recent years. For the past few years, homebuilders have focused their attention on higher priced homes, and that segment of the market now looks oversupplied. Data from the American Enterprise Institute Housing Center show that the recent deceleration in home prices has been driven by falling prices for the most expensive homes. Homes in the lowest price tier have seen prices accelerate (Chart 8).7 The divergence is also evident in the supply data. New home inventories are roughly consistent with average historical levels, while existing home inventories are incredibly low (Chart 9). In fact, new home inventories now represent 6.4 months of demand while existing home inventories represent 4.3 months of demand (Chart 9, panel 3). Such a wide divergence is historically rare. Chart 8An Oversupply Of High ##br##Priced Homes...

An Oversupply Of High Priced Homes...

An Oversupply Of High Priced Homes...

Chart 9...And An Undersupply Of Low Priced Homes

...And An Undersupply Of Low Priced Homes

...And An Undersupply Of Low Priced Homes

The divergence between an oversupply of new homes and an undersupply of existing homes is a result of new construction having focused on higher priced homes in recent years. The median price for a new home used to be only slightly above the median price for an existing home, but the difference shot up to above 75k during the past few years (Chart 9, bottom panel). More recently, the price differential between new and existing homes has started to fall, as builders are starting to recognize that the greater growth opportunity lies at the low-end of the market where demand is strong relative to supply. As this supply-side adjustment plays out, it will provide an additional boost to new homes sales and housing starts going forward. Appendix The following tables present the current read-outs from our butterfly spread models. We use these models to identify opportunities to take duration-neutral positions across the Treasury curve. The following two Special Reports explain the models in more detail: U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com U.S. Bond Strategy Special Report, “More Bullets, Barbells And Butterflies”, dated May 15, 2018, available at usbs.bcaresearch.com Table 3 shows the raw residuals from each model. A positive value indicates that the bullet is cheap relative to the duration-matched barbell. A negative value indicates that the barbell is cheap relative to the bullet. Table 3Butterfly Strategy Valuation: Raw Residuals In Basis Points (As of June 27, 2019)

The Long Awkward Middle Phase

The Long Awkward Middle Phase

Table 4 scales the raw residuals in Table 3 by their historical means and standard deviations. This facilitates comparison between the different butterfly spreads. Table 4Butterfly Strategy Valuation: Standardized Residuals (As of June 27 2019)

The Long Awkward Middle Phase

The Long Awkward Middle Phase

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Special Report, “2019 Key Views: Implications For U.S. Fixed Income”, dated December 11, 2018, available at usbs.bcaresearch.com 2 We use the 3/10 Treasury slope in place of the more commonly referenced 2/10 slope because it is a close proxy that provides an additional 14 years of historical data. 3 For more details on how we arrive at our spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy / Global Fixed Income Strategy Weekly Report, “The Fed’s Got Your Back”, dated June 25, 2019, available at usbs.bcaresearch.com 5 For more details on our yield curve models please see U.S. Bond Strategy Special Report, “Bullets, Barbells And Butterflies”, dated July 25, 2017, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “More Than One Reason To Own Steepeners”, dated September 25, 2018, available at usbs.bcaresearch.com 7 Low-tier homes are those in the bottom 40% of the price distribution in each metro area. High-tier homes are those that are both in the top 20% of the price distribution and exceed the GSE loan limit by more than 25%. For further details: http://www.aei.org/wp-content/uploads/2019/06/HPA_market_conditions_report_June_2019.pdf Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Central banks globally have turned dovish, with the Fed virtually promising to cut rates in July. But this will be an “insurance” cut, like 1995 and 1998, not the beginning of a pre-recessionary easing cycle. The global expansion remains intact, with the fundamental drivers of U.S. consumption robust and China likely to ramp up its credit stimulus over the coming months. The Fed will cut once or twice, but not four times over the next 10 months as the futures markets imply. Underlying U.S. inflation – properly measured – is trending higher to above 2%. U.S. GDP growth this year will be around 2.5%. Inflation expectations will move higher as the crude oil price rises. Unemployment is at a 50-year low and the U.S. stock market at an historical peak. These factors suggest bond yields are more likely to rise than fall from current levels. The upside for U.S. equities is limited, but earnings growth should be better than the 3% the bottom-up consensus expects. The key for allocation will be when to shift in the second half into higher-beta China-related plays, such as Europe and Emerging Markets. For now, we remain overweight the lower-beta U.S. equity market, neutral on credit, and underweight government bonds. To hedge against the positive impact of China stimulus, we raise Australia to neutral, and re-emphasize our overweights on the Industrials and Energy sectors. Feature Overview Precautionary Dovishness – Or Looming Recession? Recommendations

Quarterly Portfolio Outlook: Precautionary Dovishness – Or Looming Recession?

Quarterly Portfolio Outlook: Precautionary Dovishness – Or Looming Recession?

Central banks everywhere have taken a decidedly dovish turn in recent weeks. June’s FOMC statement confirmed that “uncertainties about the outlook have increased….[We] will act as appropriate to sustain the expansion,” hinting broadly at a rate cut in July. The Bank of Japan’s Kuroda said he would “take additional easing action without hesitation,” and hinted at a Modern Monetary Theory-style combination of fiscal and monetary policy. European Central Bank President Draghi mentioned the possibility of restarting asset purchases. There are two possible explanations. Either the global economy is heading into recession, and central banks are preparing for a full-blown easing cycle. Or these are “insurance” cuts aimed at prolonging the expansion, as happened in 1995 and 1998, or similar to when the Fed went on hold for 12 months in 2016 (Chart 1). Our view is that it is most likely the latter. The reason for this is that the main drivers of the global economy, U.S. consumption ($14 trillion) and the Chinese economy ($13 trillion) are likely to be strong over the next 12 months. U.S. wage growth continues to accelerate, consumer sentiment is close to a 50-year high, and the savings rate is elevated (Chart 2); as a result core U.S. retail sales have begun to pick up momentum in recent months (Chart 3). Unless something exogenous severely damages consumer optimism, it is hard to see how the U.S. can go into recession in the near future, considering that consumption is 70% of GDP. Moreover, despite weaknesses in the manufacturing sector – infected by the China-led slowdown in the rest of the world – U.S. service sector growth and the labor market remain solid. This resembles 1998 and 2016, but is different from the pre-recessionary environments of 2000 and 2007 (Chart 4). There is also no sign on the horizon of the two factors that have historically triggered recessions: a sharp rise in private-sector debt, or accelerating inflation (Chart 5). Chart 1Insurance Cuts, Or Full Easing Cycle?

Insurance Cuts, Or Full Easing Cycle?

Insurance Cuts, Or Full Easing Cycle?

Chart 2Consumption Fundamentals Are Strong...

Consumption Fundamentals Are Strong...

Consumption Fundamentals Are Strong...

Chart 3...Leading To Rebound In Retail Sales

...Leading To Rebound In Retail Sales

...Leading To Rebound In Retail Sales

Chart 4Manufacturing Weak, But Services Holding Up

Manufacturing Weak, But Services Holding Up

Manufacturing Weak, But Services Holding Up

Chart 5No Signs Of Usual Recession Triggers

No Signs Of Usual Recession Triggers

No Signs Of Usual Recession Triggers

China’s efforts to reflate via credit creation have been somewhat half-hearted since the start of the year. Investment by state-owned companies has picked up, but the private sector has been spooked by the risk of a trade war and has slowed capex (Chart 6). China may have hesitated from full-blown stimulus because the authorities in April were confident of a successful outcome to trade talks with the U.S., and a bit concerned that the liquidity was going into speculation rather than the real economy. But we see little reason why they will not open the taps fully if growth remains sluggish and trade tensions heighten.1 Chinese credit creation clearly has a major impact on many components of global growth – in particular European exports, Emerging Markets earnings, and commodity prices – but the impact often takes 6-12 months to come through (Chart 7). A key question is when investors should position for this to happen. We think this decision is a little premature now, but will be a key call for the second half of the year. Chart 6China's Half-Hearted Reflation

China's Half-Hearted Reflation

China's Half-Hearted Reflation

Chart 7China Credit Growth Affects The World

China Credit Growth Affects The World

China Credit Growth Affects The World

Chart 8Fed Won't Cut As Much As Market Wants...

Fed Won't Cut As Much As Market Wants...

Fed Won't Cut As Much As Market Wants...

The Fed has so clearly signaled rate cuts that we see it cutting by perhaps 50 basis points over the next few months (maybe all in one go in July if it wants to “shock and awe” the market). But the futures market is pricing in four 25 bps cuts by April next year. With GDP growth likely to be around 2.5% this year, unemployment at a 50-year low, trend inflation above 2%,2 and the stock market at an historical high, we find this improbable. Two cuts would be similar to what happened in 1995, 1998 and (to a degree) 2016 (Chart 8). In this environment, we think it likely that equities will outperform bonds over the next 12 months. When the Fed cuts by less than the market is expecting, long-term rates tend to rise (Chart 9). BCA’s U.S. bond strategists have shown that after mid-cycle rate cuts, yields typically rise: by 59 bps in 1995-6, 58 bps in 1998, and 19 bps in 2002.3 A combination of rising inflation, stronger growth ex-U.S., a less dovish Fed that the market expects, and a rising oil price (which will push up inflation expectations) makes it unlikely – absent an outright recession – that global risk-free yields will fall much below current levels. Moreover, June’s BOA Merrill Lynch survey cited long government bonds as the most crowded trade at the moment, and surveys of investor positioning suggest duration among active investors is as long as at any time since the Global Financial Crisis (Chart 10). Chart 9...So Bond Yields Are Likely To Rise

...So Bond Yields Are Likely To Rise

...So Bond Yields Are Likely To Rise

Chart 10Investors Betting On Further Rate Decline

Investors Betting On Further Rate Decline

Investors Betting On Further Rate Decline

The outlook for U.S. equities is not that exciting. Valuations are not cheap (with forward PE of 16.5x), but earnings should be revised up from the currently very cautious level: the bottom-up consensus forecasts S&P 500 EPS growth at only 3% in 2019 (and -3% YoY in Q2). We have sympathy for the view that there are three put options that will prop up stock prices in the event of external shocks: the Fed put, the Xi put, and the Trump put. Relating to the last of these, it is notable that President Trump tends to turn more aggressive in trade talks with China whenever the U.S. stock market is strong, but more conciliatory when it falls (Chart 11). For now, therefore, we remain overweight U.S. equities, as a lower beta way to play an environment that continues to be positive – but uncertain – for stocks. But we continue to watch for the timing to move into higher-beta China-related markets as the effects of China’s stimulus start to come through. Chart 11Trump Turns Softer When Market Falls

Trump Turns Softer When Market Falls

Trump Turns Softer When Market Falls

Garry Evans Chief Global Asset Allocation Strategist garry@bcaresearch.com What Our Clients Are Asking Chart 12Temporary Forces Drove Inflation Downturn

Temporary Forces Drove Inflation Downturn

Temporary Forces Drove Inflation Downturn

Why Is Inflation So Low? After reaching 2% in July 2018, U.S. core PCE currently stands at 1.6%, close to 18 month lows. This plunge in inflation, along with increased worries about the trade war and continued economic weakness, has led the market to believe that the Fed Funds Rate is currently above the neutral rate, and that several rate cuts are warranted in order to move policy away from restrictive territory. We believe that the recent bout of low inflation is temporary. The main contributor to the fall in core PCE has been financial services prices, which shaved off up to 40 basis points from core PCE (Chart 12, panel 1). However, assets under management are a big determinant of financial services prices, making this measure very sensitive to the stock market (panel 2). Therefore, we expect this component of core PCE to stabilize as equity prices continue to rise. The effect of higher equity prices, and the stabilization of other goods that were affected by the slowdown of global growth in late 2018 and early 2019, may already have started to push inflation higher. Month-on-month core PCE grew at an annualized rate of 3% in April, the highest pace since the end of 2017. Meanwhile, trimmed mean PCE, a measure that has historically been a more stable and reliable gauge of inflationary pressures, is at a near seven-year high (panel 3). The above implies that the market might be overestimating how much the Fed is going to ease. We believe that the Fed will likely cut once this year to soothe the pain caused by the trade war on financial markets. However, with unemployment at 50-year lows, and inflation set to rise again, the Fed is unlikely to deliver the 92 basis points of cuts currently priced by the OIS curve for the next 12 months. This implies that investors should continue to underweight bonds. Chart 13Turning On The Taps

Turning On The Taps

Turning On The Taps

Will China Really Ramp Up Its Stimulus? The direction of markets over the next 12 months (a bottoming of euro area and Emerging Markets growth, commodity prices, the direction of the USD) are highly dependent on whether China further increases monetary stimulus in the event of a breakdown in trade negotiations with the U.S. But we hear much skepticism from clients: aren’t the Chinese authorities, rather, focused on reducing debt and clamping down on shadow banking? Aren’t they worried that liquidity will simply flow into speculation and have little impact on the real economy? Now the government has someone to blame for a slowdown (President Trump), won’t they use that as an excuse – and, to that end, are preparing the population for a period of pain by quoting as analogies the Long March in the 1930s and the Korea War (when China ground down U.S. willingness to prolong the conflict)? We think it unlikely that the Chinese government would be prepared to allow growth to slump. Every time in the past 10 years that growth has slowed (with, for example, the manufacturing PMI falling significantly below 50) they have always accelerated credit growth – on the basis of the worst-case scenario (Chart 13, panel 1). Why would they react differently this time, particularly since 2019 is a politically sensitive year, with the 70th anniversary of the founding of the People’s Republic in October and several other important anniversaries? Moreover, the government is slipping behind in its target to double per capita income in the 10 years to end-2020 (panel 2). GDP growth needs to be 6.5-7% over the next 18 months to achieve the target. The government’s biggest worry is employment, where prospects are slipping rapidly (panel 3). This also makes it difficult for the authorities to retaliate against U.S. companies that have large operations, such as Apple or General Motors, since such measures would hurt their Chinese employees. Besides a significant revaluation of the RMB (which we think likely), China has few cards to play in the event of a full-blown trade war other than fully turning on the liquidity tap again.

Chart 14

Aren’t There Signs Of Bubbliness In Equity Markets? Clients have asked whether the current market environment has been showing any classic signs of euphoria. These usually appear with lots of initial public offerings (IPO), irrational M&A activity, and excess investor optimism. The IPO market has some similarities to the years leading up to the dot-com bubble, but it is important to look below the surface. The percentage of IPOs with negative earnings in 2018 was similar to the previous peak in 1999. However, the average first-day return of IPOs in 2019, while still above the historical average, has been much lower than that during the dot-com bubble period (Chart 14, panel 1). There is also a difference in the composition of firms going public. There are now many IPOs for biotech firms that have heavily invested in R&D, and so have relatively low sales currently but await a breakthrough in their products; by their nature, these are loss-making (panel 2). Cross-sector, unrelated M&A activity has also often been a sign of bubble peaks. It is a consequence of firms stretching to find inorganic growth late in the cycle. Such deals are characterized by high deal premiums, and are usually conducted through stock purchases rather than in cash. The current average deal premium is below its historical average (panel 3). Additionally, 2018 and 2019-to-date M&A deals conducted using cash represented 60% and 90% of the total respectively, compared to only 17% between 1996 and 2000. Investor sentiment is also moderately pessimistic despite the rally in the S&P 500 since the beginning of the year (panel 4). This caution suggests that investors are fearful of the risk of recession rather than overly positive about market prospects, despite the U.S. market being at an historical high. Given the above, we do not see any signals of the sort of euphoria and bubbliness that typically accompanies stock market tops. Will Japan Benefit From Chinese Reflation? Japan has been one of the worst-performing developed equity markets since March 2009, when global equities hit their post-crisis bottom in both USD (Chart 15) and local currency terms. Now with increasing market confidence in China’s reflationary policies, clients are asking if Japan is a good China play given its close ties with the Chinese economy. Our answer is No.

Chart 15

Chart 16Downgrade Japan To Underweight

Downgrade Japan To Underweight

Downgrade Japan To Underweight

It’s true that Japanese equities did respond to past Chinese reflationary efforts, but the outperformances were muted and short-lived (Chart 16, panel 1). Even though Japanese exports to China will benefit from Chinese reflationary policy (panel 5), MSCI Japan index earnings growth does not have strong correlation with Japanese exports to China, as shown in panel 4. This is not surprising given that exports to China account for only about 3% of nominal GDP in Japan (compared to almost 6% for Australia, for example). The MSCI Japan index is dominated by Industrials (21%) and Consumer Discretionary (18%). Financials, Info Tech, Communication Services and Healthcare each accounts for about 8-10%. Other than the Communication Services sector, all other major sectors in Japan have underperformed their global peers since the Global Financial Crisis (panels 2 and 3). The key culprit for such poor performance is Japan’s structural deflationary environment. Wage growth has been poor despite a tight labor market. This October’s consumption tax increase will put further downward pressure on domestic consumers. There is no sign of the two factors that have historically triggered recessions: a sharp rise in private-sector debt, or accelerating inflation. As such, we are downgrading Japan to a slight underweight in order to close our underweight in Australia (see page 16). This also aligns our recommendation with the output from our DM Country Allocation Quant Model, which has structurally underweighted Japan since its inception in January 2016. Global Economy Chart 17Is Consumption Enough To Prop Up U.S. Growth?

Is Consumption Enough To Prop Up U.S. Growth?

Is Consumption Enough To Prop Up U.S. Growth?