Monetary

Highlights This week’s FOMC statement, together with the accompanying press conference, signaled a clear change in tone from the Fed. Despite the fact that underlying growth remains well above trend, a rate cut in July is now more likely than not. An additional “insurance cut” is also probable in September. Right now, rising inflation is not much of a risk. However, the Fed’s dovish turn almost guarantees that the U.S. economy will overheat. This reinforces our view that Fed policy will unfold in a two-stage process: A period of excessively easy monetary policy stretching past the next presidential election, followed by a burst of inflation that ultimately forces the Fed to hike rates. While stocks will perform well during the first stage, they will suffer during the second. We turned positive on global equities last December, but initiated a tactical hedge in May of this year. We are now extinguishing this hedge. The dollar is likely to weaken over the coming months. Cyclical equity sectors will start outperforming defensives, while international stocks will outperform their U.S. peers. We went long gold on April 17th. The trade is up 9.2% since then. Stick with it. Feature Redefining Dovish I have had the pleasure of meeting clients in the U.S. southeast this week. Unsurprisingly, the Fed has been a hot topic of discussion. Had one been told two months ago that the Federal Reserve would drop the word “patient” from the FOMC statement, one would have plausibly concluded that the Fed was about to hike rates. Little would one have known that what constitutes dovishness would change so much so quickly. Today, a dovish Fed means one that is about to cut rates. In a complete inversion of the original connotation of the term, patient is now considered hawkish. This change in tone was not immediately evident in the median 2019 interest rate dot in the June Summary of Economic Projections released this week. Just as in March, it remains stuck at 2.4%, implying a flat profile for rates over the remainder of the year. However, underneath the surface, there was a whirlwind of change. We are inclined to believe that if the Fed cuts rates in July, it will also cut rates again in September. In March, not a single FOMC member expected rates to fall this year. In the June statement, eight members penciled in rate cuts, seven of whom now expect 50 basis points of easing in the remainder of 2019 (Chart 1). The only reason the median dot did not budge was because eight members continued to cling to the expectation that the Fed would be able to keep rates at current levels throughout this year, with an additional member predicting a rate hike (down from six members who expected at least one rate hike in March).

Chart 1

Tellingly, a slim majority (9 out of 17) FOMC members now expect rates to be lower in 2020 than they are currently. This tells us that some of the members who elected not to show cuts in the dot plot for 2019 have a very low bar for cutting rates. Most likely, they are looking to see how the trade talks play out before pulling the trigger on rate cuts. Our baseline expectation is that there will be enough progress in the trade negotiations at the G20 summit to keep the U.S. from imposing a further $300 billion in tariffs on Chinese imports. However, an all-encompassing deal, which rolls back existing tariffs, is not in the cards. In such a muddle-through scenario, we think a rate cut in July is still more likely than not. The fact that Jay Powell did little to push back against market expectations of rate cuts this year during his press conference this week indicates that the Fed is preparing to cut rates. How Much More Easing?

Chart 2

Now that a July cut is looking increasingly like a done deal, the question is how low will rates go? Historically, when the Fed has cut rates, it has done so multiple times. Thus, it is not surprising that the market is currently assigning a 97% chance of two or more rate cuts this year and a 75% chance of three or more cuts (Chart 2). The entire futures curve is pointing to a fed funds rate of only 1.25% at end-2020 (Chart 3).

Chart 3

We are inclined to believe that if the Fed cuts rates in July, it will also cut rates again in September. However, we doubt that the Fed will deliver as much easing as is currently priced in. For one thing, it is not clear that the economy needs it. According to the Atlanta Fed’s GDPNow model, real final domestic demand is on course to accelerate from 1.5% in Q1 to 3.1% in Q2 (Chart 4). Real consumer spending is on track to rise by a whopping 3.9% in Q2.

Chart 4

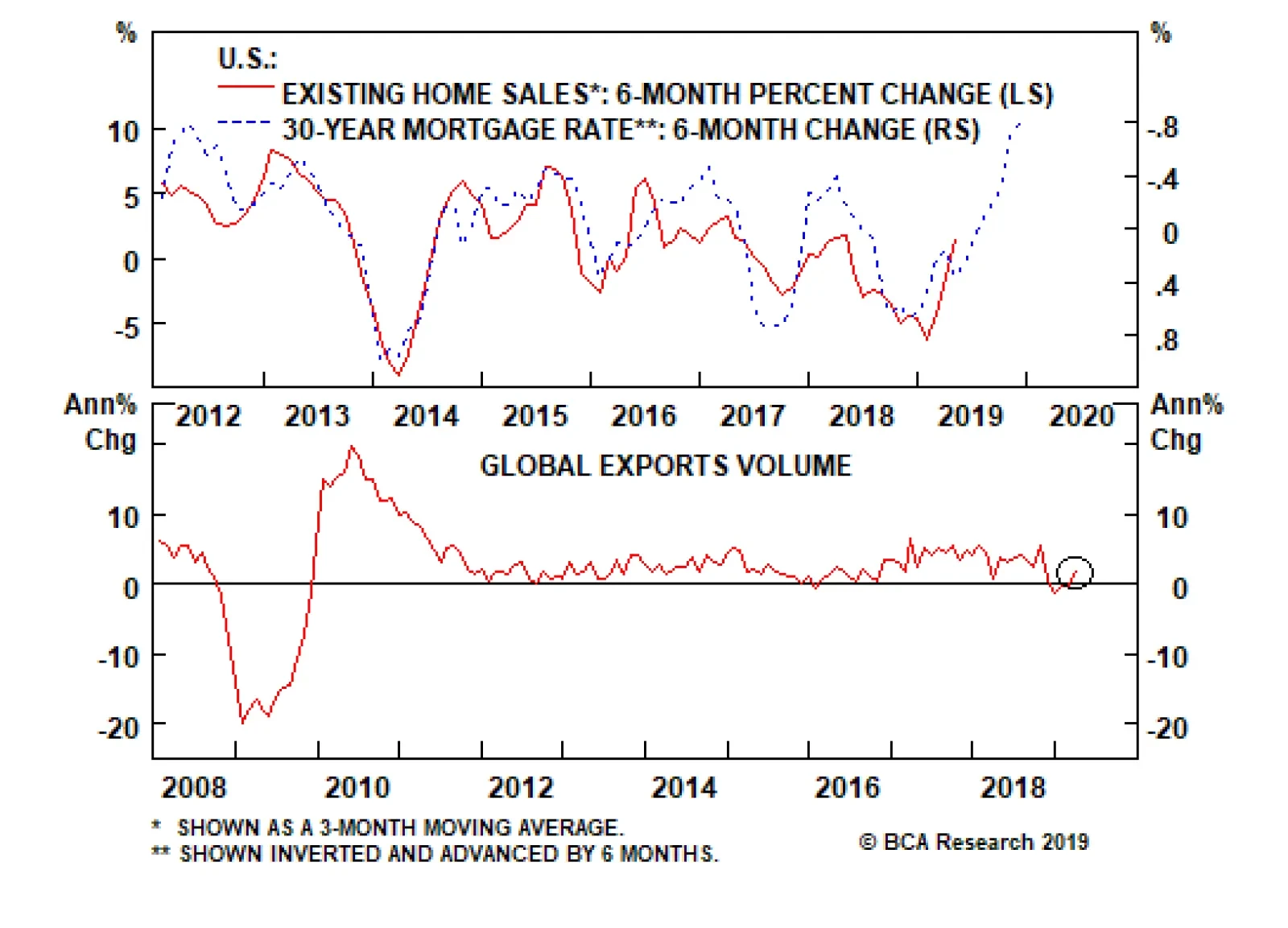

Chart 5Declining Yields Bode Well For Housing

Declining Yields Bode Well For Housing

Declining Yields Bode Well For Housing

The only reason that headline GDP growth is set to decline in Q2 is because inventory destocking will detract from growth, having contributed to it in Q1. Keep in mind that inventory destocking is a positive indicator for future output growth because it means that final sales are running above current production levels. As we get into the second half of the year, inventories will start making a positive contribution to growth. The lagged effects from the substantial decline in bond yields will also be hitting the economy with full force. Housing, in particular, stands to benefit (Chart 5). Meanwhile, Chinese stimulus will be working its way through the global economy, likely lifting global growth in the process. Take Out Some Insurance? Chart 6Inflation Expectations Have Dropped

Inflation Expectations Have Dropped

Inflation Expectations Have Dropped

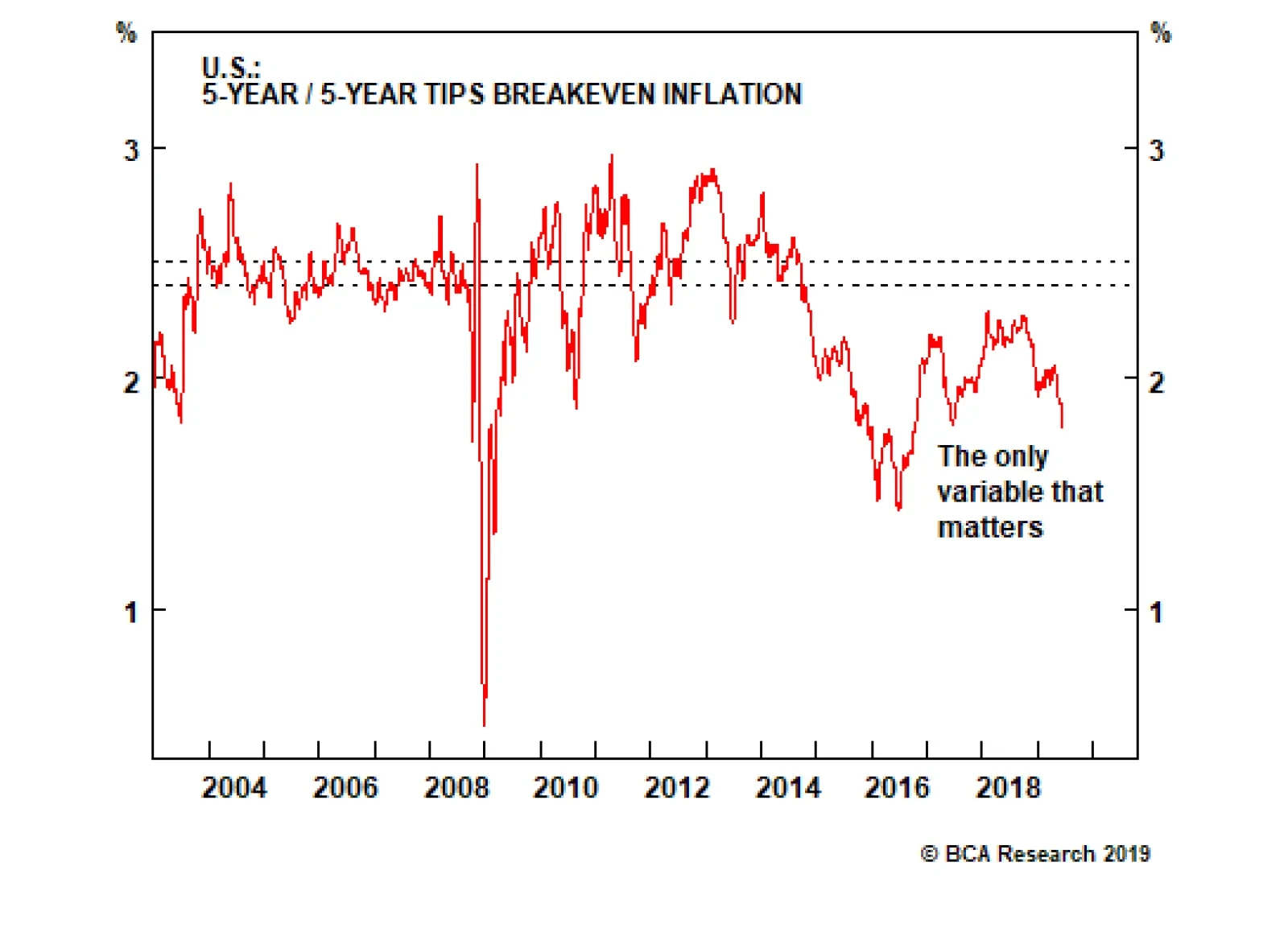

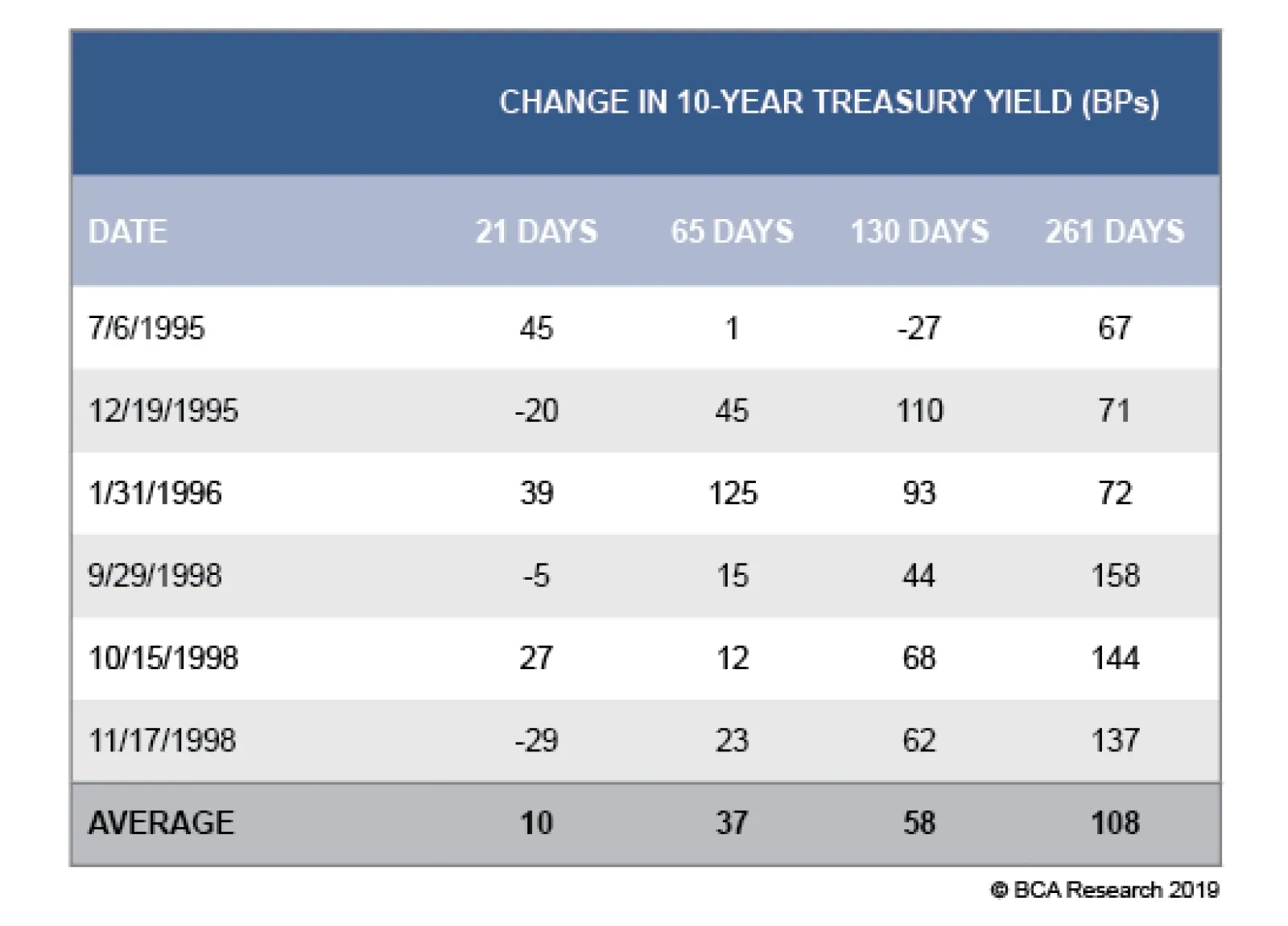

Some monetary easing could still be justified on precautionary grounds, even if growth does seem to be holding up. The zero bound constraint remains a formidable threat. It does make sense to try to raise inflation expectations in order to allow real rates to fall deeper into negative territory in the event that a recession occurs. The fact that market-based inflation expectations have dropped sharply since last autumn has clearly influenced the Fed’s thinking (Chart 6). Right now, inflation is not a significant risk. An escalation of the trade war would push up import prices, but this is unlikely to have a lasting effect on inflation, given that Chinese imports account for only 2.5% of U.S. GDP. Indeed, a severe trade war could actually reduce U.S. inflation by causing global growth to slow which would push down commodity prices and push up the dollar. Still, we would not push the “insurance” argument too hard. Current policy rates are close to neutral according to the widely-cited Laubach Williams model, and somewhat below the “longer run” range of 2.4%-to-3.3% in the Fed's latest projections. In 1995 and 1998, the last two episodes in which the Fed engaged in precautionary easing, real rates reached 4% (Chart 7). This was well above their equilibrium level. Chart 7The Fed Embarked On Precautionary Easing In The 1990s Amid Restrictive Real Rates

The Fed Embarked On Precautionary Easing In The 1990s Amid Restrictive Real Rates

The Fed Embarked On Precautionary Easing In The 1990s Amid Restrictive Real Rates

Of course, if it turns out that the Fed’s estimate of the real neutral rate of interest, low as it is at 0%, is still too high, continued rate cuts will be necessary. However, as we discussed last week,1 the evidence, if anything, suggests that the neutral rate is higher than what the Fed thinks. This implies that monetary policy is currently very expansionary and will only become more so if the Fed cuts rates. A Two-Stage Cycle The discussion above suggests that Fed policy will unfold as a two-stage process: A period of excessively easy monetary policy stretching past the next presidential election, followed by a burst of inflation that ultimately forces the Fed to hike rates. Chart 8No Imminent Threat Of A Wage-Price Inflationary Spiral

No Imminent Threat Of A Wage-Price Inflationary Spiral

No Imminent Threat Of A Wage-Price Inflationary Spiral

It is difficult to be precise about when inflation will reach a level that starts to worry the Fed. Wage growth has picked up, but so far, this has been more than offset by a cyclical revival in productivity growth. In fact, unit labor cost inflation, which leads core inflation by around 12 months, has decelerated sharply (Chart 8). However, if the unemployment rate continues to drop, wage growth will begin to outstrip productivity gains. A wage-price spiral could develop. This is not a major risk for the next 12 months, but could become an issue in late-2020 or early-2021. Implications For Investment Strategy The Fed determines rates in the short run, but it is the economy that dictates rates in the long run. If the Fed keeps rates too low for too long, as we expect will be the case, inflation will eventually rise, forcing the Fed to hike rates. Ironically, the Fed’s decision to cut rates over the coming months means that the terminal rate during this cycle will be higher than if they had just stood pat. The longer-term investment implications for bonds are clear: Treasury yields will rise much more than expected over a horizon of two-to-three years. Investors should reduce duration risk and favor inflation-protected securities over nominal bonds. Gold should also be bought as a hedge. We went long gold on April 17th. The trade is up 9.2% since then. Stick with it. The picture for bonds is more nuanced over a shorter-term horizon of six-to-nine months. Now that the Fed has decided to cut rates, it will be difficult for yields to rise anywhere close to last year’s highs. Still, given our expectation of accelerating U.S. and global growth, the Fed is likely to cut rates by less than what is currently discounted. A modest short duration stance is thus still warranted. We turned bullish on global equities in December following the steep market sell off and have remained structurally overweight stocks throughout this entire year. We did, however, initiate a tactical hedge to short the S&P 500 on May 10 following what we regarded as an overly complacent reaction by investors to President Trump’s decision to further raise tariffs on Chinese imports. While our decision to put on the hedge initially looked prescient, the combination of the Fed’s dovish turn, a shift toward easier monetary policy by other central banks (such as the ECB this week), and growing optimism over a resolution to the trade war have caused stocks to rally above our entry point. We are thus closing this hedge for a loss of 3.8%. Ultimately, if our view that the neutral rate of interest in the U.S. is higher than widely believed turns out to be correct, equities will perform well. This is simply because a higher neutral rate implies that monetary policy is currently expansionary. Recessions rarely occur when monetary policy is accommodative, while equity bear markets rarely happen outside of recessionary periods (Chart 9). Ergo, stocks are more likely to rise than fall until interest rates increase significantly (which is unlikely to happen anytime soon). Chart 9Recessions And Bear Markets Usually Overlap

Recessions And Bear Markets Usually Overlap

Recessions And Bear Markets Usually Overlap

Chart 10The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

The Dollar Is A Countercyclical Currency

As a countercyclical currency, the dollar will probably weaken over the coming months as global growth picks up (Chart 10). Cyclical equity sectors will start outperforming defensives, while international stocks will outperform their U.S. peers. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1 Please see Global Investment Strategy Weekly Report, “A Two-Stage Fed Cycle,” dated June 14, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Chart 11

Tactical Trades Strategic Recommendations Closed Trades

Highlights The unifying chorus among global central banks is currently for more monetary stimulus. In the race towards lower interest rates, the ultimate winners will be pro-cyclical currencies. Italian 10-year real government bond yields are rapidly joining those in Spain and Portugal in being below the neutral rate of interest for the entire euro zone. This is hugely reflationary. That said, growth barometers remain in freefall, suggesting some patience is still warranted. We are watching like hawks a few key crosses that are sitting at critical technical levels. A break below will signal we are entering a deflationary bust. A bounce could be a prologue to a reflationary rally. Watch the bond-to-gold ratio to gauge where the balance of forces are shifting for the U.S. dollar. Tepid action by the BoJ this week reinforces our view that the path towards additional stimulus will be lined by a stronger yen. Stay short USD/JPY. We were a few pips away from our stop loss on long GBP/USD this week. Stand aside if triggered. The Norges Bank has emerged as the most hawkish G10 central bank. Hold long NOK/SEK and short CAD/NOK positions. Feature As early as 1625, Hugo De Groot, then a Dutch philosopher, saw the act of pre-emptively striking an enemy as a move of self-defense. With a mandate of self-preservation, it made sense for a country to wage war for injury not yet done, if sufficient evidence pointed to colossal damage from no action. So faced with some important central bank meetings this week, and European manufacturing data well into freefall, the European Central Bank pulled a trick out of an old playbook. At an ECB forum in Sintra, Portugal, President Mario Draghi highlighted that if the inflation outlook failed to improve, the central bank had considerable headroom to launch a fresh expansion of its balance sheet. With its next policy meeting not until July 25th, it sure did feel like the ECB was cornered. What followed was as expected, a more dovish Federal Reserve, Bank Of Japan and Bank of England. Paradoxically, those two words might have opened a reflationary window and triggered one of the necessary catalysts for a sharp selloff in the U.S. dollar (Chart I-1). Time Lags The key question today is whether central banks have sufficiently eased policy to stem the decline in manufacturing data. Obviously, the trade war remains a key risk to whatever direction indicators might be pointing to today, but a few key observations are in order. Chart I-1A Countertrend Rally Underway

A Countertrend Rally Underway

A Countertrend Rally Underway

Chart I-2Dovish Central Banks Should Help Growth

Dovish Central Banks Should Help Growth

Dovish Central Banks Should Help Growth

Our global monetary policy barometer tends to lead the PMI by about six months. It tracks 29 central banks, gauging which have tightened policy over the last three months and which have not. Since the global financial crisis, whenever the measure has hit the critical threshold of 15-20%, it has correctly signaled that the pace of manufacturing activity is likely to slow. It is entirely another debate whether or not the world we live in today can tolerate higher interest rates, but our barometer has clearly plunged into reflationary territory – below the 20% threshold. This has usually been followed by a pick-up in manufacturing activity (Chart I-2). Data out of Singapore has been a timely tracker of global trade and warrants monitoring. Most real-time measures of economic activity remain weak, especially in the export sector, but it appears shipping activity may have been picking up pace over the past few months. Both the Harpex Shipping Index and the Baltic Dry Index have been perking up. Similarly, vessel arrivals into Singapore that tend to lead exports have stopped their pace of deceleration. It is still too early to read much into this data, since it could be a reflection of re-stocking ahead of possible tariffs. That said, data out of Singapore has been a timely tracker of global trade and warrants monitoring (Chart I-3). Chart I-3ASigns Of Life Along Shipping Lanes

Signs Of Life Along Shipping Lanes

Signs Of Life Along Shipping Lanes

Chart I-3BWatch Activity At Singaporean Ports

Watch Activity At Singaporean Ports

Watch Activity At Singaporean Ports

Chinese money growth, especially forward-looking liquidity indicators such as M2 relative to GDP, has bottomed. Historically, this has lit a fire under cyclical stocks, and by extension pro-cyclical currencies. This is also consistent with the fall in Chinese bond yields that has historically tended to be supportive for money growth in the ensuing months (Chart I-4). Overall industrial production remains weak, but the production of electricity and steel, inputs into the overall manufacturing value chain, are inflecting higher. Intuitively, these tend to lead overall industrial production. In recent weeks, both steel and iron ore prices have been soaring. Many commentators have attributed these increases to supply bottlenecks and/or seasonal demand. However, it is evident from both the manufacturing data and the trend in prices that demand is also playing a role. Overall residential property sales remain soft, but the evidence from tier-1 and even tier-2 cities is that this may be behind us. A revival in the property market will support construction activity, investment and imports (Chart I-5). Chart I-4A Bullish Signal For Chinese Liquidity

A Bullish Signal For Chinese Liquidity

A Bullish Signal For Chinese Liquidity

Chart I-5

Finally, high-beta currencies such as the RUB/USD, ZAR/USD and BRL/USD have stopped falling and are off their lows of the year. These currencies are usually good at sniffing out a change in the investment landscape, specifically one becoming more favorable to carry trades. The message so far is that the drop in U.S. bond yields may have been sufficient to make these currencies attractive again (Chart I-6). On a similar note, if currencies in emerging Asia that sit closer to the epicenter of Chinese stimulus can rally from here, it would indicate that policy stimulus is sufficient, and that the transmission mechanism is working. Chart I-6High-Beta Currencies Have Stopped Falling

High-Beta Currencies Have Stopped Falling

High-Beta Currencies Have Stopped Falling

Chart I-7AUD/JPY Near A Critical Level

AUD/JPY Near A Critical Level

AUD/JPY Near A Critical Level

Importantly, the AUD/JPY cross is sitting at an important technical level. Ever since the financial crisis, 72.5 has proven to be formidable intra-day resistance, with the cross failing to break below both during the euro area debt crisis in 2011-2012 and the China slowdown of 2015-2016. Speculators are neutral on the cross, suggesting any move in either direction could be powerful and significant. A break below will signal we are entering a deflationary bust. A bounce could be a prologue to a reflationary rally (Chart I-7). Bottom Line: We are watching a few key reflationary indicators to gauge whether it pays to be contrarian. The message is tipping in favor of pro-cyclical currencies, and further improvement will give us the green light to adopt a more pro-cyclical stance. The Message From The U.S. Dollar The market interpreted the Fed’s latest monetary policy announcement as dovish, even though the central bank kept rates on hold. What transpired during the conference was the market increasing its bets for more aggressive rate cuts. The swaps market is currently pricing in 94 basis points of rate cuts over the next 12 months, versus 76 basis points a fortnight ago. This shift has pushed down the dollar, lifting other currencies and gold in the process. U.S. bond yields have also punched below 2%. Interest rate differentials are moving against the dollar, but our important takeaway – that gold continues to outperform Treasurys – is an ominous sign. Even before the financial crisis, a long-standing benchmark for gauging ultimate downside in the dollar was the bond-to-gold ratio. This is because gold has stood as a viable threat to dollar liabilities, capturing the ebbs and flows of investor confidence in the greenback tick for tick. Any sign that the balance of forces are moving away from the U.S. dollar will favor a breakout in the bond-to-gold ratio. Chart I-8Major Peak In The Bond-To-Gold Ratio?

Major Peak In The Bond-To-Gold Ratio?

Major Peak In The Bond-To-Gold Ratio?

The rationale is pretty simple. Investors who are worried about U.S. twin deficits and the crowded trade of being long Treasurys will shift into gold, since pretty much every other major bond market (Germany, Switzerland, Japan) have negative yields. That favors gold at the expense of the dollar. The reverse is true if investors consider Treasurys more of a safe haven. The bond-to-gold ratio and dollar tend to move tick for tick, so a breakout in one can be a signal for what will happen to the other. This is why we are watching this ratio like hawks, and the breakdown this week is a bad omen for the U.S. dollar (Chart I-8). The euro might be the biggest beneficiary from the fall in the dollar. The standard dilemma for the euro zone is that interest rates have always been too low for the most productive nation, Germany, but too expensive for others such as Spain and Italy.1 As such, the euro has typically been caught in a tug-of-war between a rising equilibrium rate of interest for Germany, but a very low neutral rate for the peripheral countries. The silver lining is that the ECB may now have finally lowered domestic interest rates and eased policy to the point where they are accommodative for almost all euro zone countries: 10-year government bond yields in France, Spain, Portugal and even Italy now sit close to or below the neutral rate (Chart I-9). The ECB may now have finally lowered domestic interest rates and eased policy to the point where they are accommodative for almost all euro zone countries. Chart I-9The ECB May Have Won The Euro Battle

The ECB May Have Won The Euro Battle

The ECB May Have Won The Euro Battle

The drop in the euro since 2018 has also eased financial conditions and made euro zone companies more competitive. This is a tailwind for European stocks. Fortunately for investors, European equities, especially those in the periphery, remain unloved, given they are trading at some of the cheapest cyclically adjusted price-to-earnings multiples in the developed world. Analysts began aggressively revising up their earnings estimates for euro zone equities earlier this year, relative to the U.S. If they are right, this could lead into powerful inflows into the euro over the next nine to 12 months (Chart I-10). Chart I-10The Euro May Be On The Verge Of A Major Pop

The Euro May Be On The Verge Of A Major Pop

The Euro May Be On The Verge Of A Major Pop

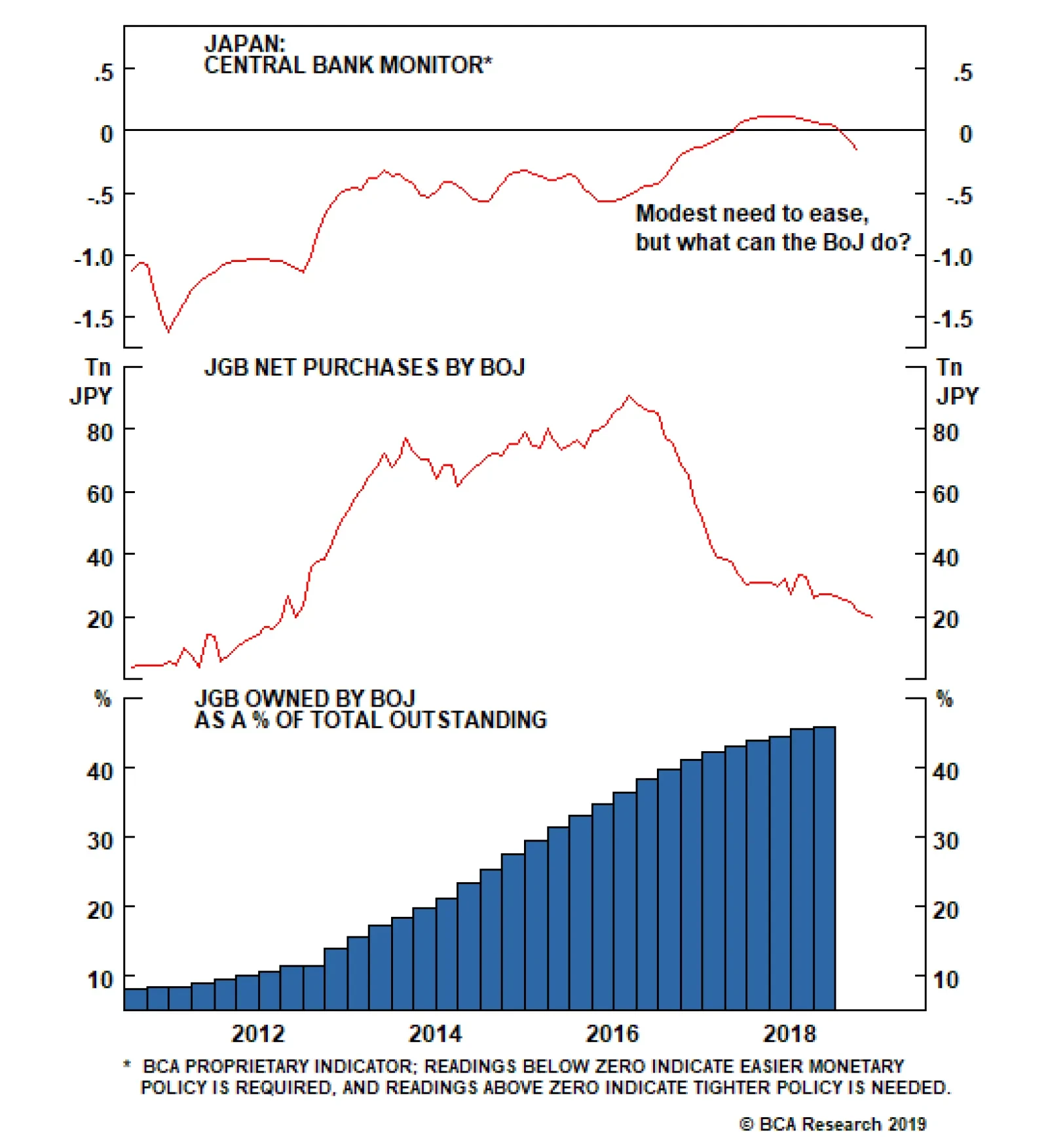

Bottom Line: Falling rate expectations relative to policy action have historically been bearish for the dollar with a lag of about nine to 12 months. The dollar has been relatively resilient, despite interest rate differentials are moving against it, but has started to converge towards lower rates. One winner will be EUR/USD. Stay Short USD/JPY The BoJ kept monetary policy on hold this week, but the message was cautious, even encouraging fiscal support. It looks like the end of the Heisei era2 has brought forward a well-known quandary for the central bank, which is that additional monetary policy options are hard to come by, since there have been diminishing economic returns to additional stimulus. This puts short USD/JPY bets in an enviable “heads I win, tails I do not lose too much” position. Chart I-11Stealth Tapering By The BoJ

Stealth Tapering By The BoJ

Stealth Tapering By The BoJ

The BoJ maintained Yield Curve Control (YCC), stating it will continue to “conduct purchases of JGBs in a flexible manner so that their amount outstanding will increase at an annual pace of about 80 trillion yen.”3 But with the BoJ owning 46% of outstanding JGBs, about 75% of ETFs and almost 5% of JREITs, this will be a tall order (Chart I-11). The supply side obviously puts a serious limitation on how much more stimulus the central bank can provide. Total annual asset purchases by the BoJ are currently running at about ¥27 trillion, while JGBs purchases are running at ¥20 trillion. This is a far cry from the central bank’s soft target of ¥80 trillion, and unlikely to change anytime soon, given bond yields closing in on the -20 basis-point floor. This means interest rate differentials are likely to move in favor of a stronger yen short term (Chart I-12). The BoJ targets an inflation rate of 2%, but it is an open question as to whether it can actually achieve this. The overarching theme for prices in Japan is a rapidly falling (and ageing) population leading to deficient demand. More importantly, almost 40% of the Japanese consumption basket is in tradeable goods, meaning domestic inflation is as much driven by the influence of the BoJ as it is by globalization. Even for prices within the BoJ’s control, an ageing demographic that has a strong preference for falling prices is a powerful conflicting force. For example, transportation and telecommunications make up 17% of the core consumption basket in Japan, a non-negligible weight. This is and will remain a powerful drag on CPI, making it very difficult for the BoJ to re-anchor inflation expectations upward. The risk to short USD/JPY positions is that the BoJ will eventually act, but it may first require a riot point. On the other side of the coin, YCC and negative interest rates have been an anathema for Japanese net interest margins and share prices. This, together with QE, has pushed banks to search for yield down the credit spectrum. Any policy shift that is increasingly negative for banks could easily tip them over. Chart I-12Can Japan Drop Rates Further?

Can Japan Drop Rates Further?

Can Japan Drop Rates Further?

Chart I-13MMT Might Be What The Doctor Ordered

MMT Might Be What The Doctor Ordered

MMT Might Be What The Doctor Ordered

Bottom Line: Inflation expectations remain at rock-bottom levels in Japan, at a time when the BoJ may be running out of policy bullets. Meanwhile, the margin of error for the BoJ is non-trivial, since a small external shock could tip the economy back into deflation. The risk to short USD/JPY positions is that the BoJ will eventually act, but it may first require a riot point (Chart I-13). A Final Note On The Pound A new conservative leadership is at the margin more negative for the pound (the assessment of our geopolitical strategists is that the odds of a hard Brexit have risen from 14% to 21%). However, our simple observation is that the pound is below where it was after the 2016 referendum results, yet more people are now in favor of staying in the union (Chart I-14). Chart I-14Support For Brexit Is Low, But Has Risen

Support For Brexit Is Low, But Has Risen

Support For Brexit Is Low, But Has Risen

Chart I-15Low Rates Could Help British Capex

Low Rates Could Help British Capex

Low Rates Could Help British Capex

The BoE kept rates on hold following its latest policy meeting and will continue to err on the side of caution until the Brexit imbroglio is resolved. The reality is that the pound and U.K. gilt yields should be much higher solely on the basis of hard incoming data. Yes, the data has softened, but employment growth has been holding up very well, wages are inflecting higher and the average U.K. consumer appears in decent shape. Investment and construction have been the weak spot in the U.K. economy but may marginally improve on low rates (Chart I-15). We remain long the pound, given lower overall odds of a no-deal Brexit. That said, our long GBP/USD position was a few pips from being stopped out this week. Stand aside if triggered. Housekeeping Our stop-loss on long EUR/CHF was triggered at 1.11 yesterday. Stand aside for now, but we will be looking for opportunities to put this trade back on. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, titled “EUR/USD And The Neutral Rate Of Interest,” dated June 14, 2019, available at fes.bcaresearch.com. 2 The Heisei era refers to the period of Japanese history corresponding to the reign of Emperor Akihito from 8 January 1989 until his abdication on 30 April 2019. 3 Please refer to the Bank of Japan “Minutes of The Monetary Policy Meeting,” dated June 20, 2019, page 1. Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been mostly negative: Retail sales grew by 0.5% month-on-month in May. University of Michigan consumer sentiment and expectation indices both fell to 97.9 and 88.6 in June. However, current conditions index increased to 112.5. NY empire state manufacturing index came in at -8.6 in June, falling below 0 for the first time since October 2016. NAHB housing market index fell to 64 in June. Housing starts contracted by 0.9% month-on-month in May, while building permits increased by 0.3% month-on-month. Current account deficit decreased to $130.4 billion in Q1. Philadelphia Fed Business Outlook survey index fell to 0.3 in June. DXY index fell by 1% this week. This Wednesday, the Fed has kept interest rates steady at 2.5%, but left the door open for rate cuts in the future as Powell stated that “Many participants now see the case for somewhat more accommodative policy has strengthened.” The dollar has weakened in response to the dovish pivot. Report Links: EUR/USD And The Neutral Rate Of Interest - June 14, 2019 Where To Next For The U.S. Dollar? - June 7, 2019 President Trump And The Dollar - May 9, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been negative with muted inflation: Trade surplus narrowed to €15.3 billion in April. Headline and core inflation fell to 1.2% and 0.8% year-on-year respectively in May. ZEW survey expectations index fell to -20.2 in June. Current account surplus decreased to €20.9 billion in April. Construction output growth fell to 3.9% year-on-year in April. Consumer confidence fell further to -7.2 in June. EUR/USD increased by 0.7% this week. The cross fell initially on Draghi’s dovish message that ECB would ease policy again should inflation fail to accelerate, then rebounded on broad dollar weakness this Wednesday following the Fed’s dovish pivot. However, the euro has weakened further against other currency pairs. Our EUR/CHF trade was stopped out at 1.11 on Thursday morning. Report Links: EUR/USD And The Neutral Rate Of Interest - June 14, 2019 Take Out Some Insurance - May 3, 2019 Reading The Tea Leaves From China - April 12, 2019 The Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been mostly negative: Industrial production was unchanged at -1.1% year-on-year in April. Total adjusted trade balance decreased to -¥609.1 billion in May. Imports fell by 1.5% year-on-year, while exports contracted by 7.8% year-on-year. All industry activity index increased by 0.9% month-on-month in April. Machine tool orders continued to contract by 27.3% year-on-year in May. USD/JPY fell by 1.1% this week. BoJ kept the interest rate unchanged at -0.1% this week. In the monetary statement, the BoJ stated that the Japanese economy would likely continue expanding at a moderate rate, despite exogenous shocks. The current policy rates will be maintained at least through the spring of 2020. Report Links: Short USD/JPY: Heads I Win, Tails I Don’t Lose Too Much - May 31, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been mixed: Retail price index increased by 3% year-on-year in May. Headline and core inflation fell to 2% and 1.7% year-on-year respectively in May. Total retail sales growth fell to 2.3% year-on-year in May. GBP/USD increased by 0.9% this week. The MPC voted unanimously to keep the interest rate unchanged at 0.75% this week. However, some policymakers have suggested that borrowing costs should be higher. The BoE however cut its growth forecast in the second quarter of 2019 amid rising global trade tensions and a fear of “no-deal” Brexit. Report Links: A Contrarian View On The Australian Dollar - May 24, 2019 Take Out Some Insurance - May 3, 2019 Not Out Of The Woods Yet - April 5, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

There is little data from Australia this week: House price index contracted by 7.4% year-on-year in Q1. Westpac leading index fell by 0.08% month-on-month in May. AUD/USD rose by 0.7% this week. Our long AUD/USD came close to the stop-loss at 0.68 this Tuesday, then rebounded on dollar weakness and is now trading around 0.69. RBA governor Philip Lowe said that it was unrealistic to think that the single quarter-point cut to 1.25% would work to achieve its growth target, signaling more rate cuts and fiscal stimulus in the future. We are holding on to the long AUD/USD position from a contrarian perspective, and believe that the Aussie dollar will benefit as a pro-cyclical currency if the global growth outlook turns positive. Report Links: A Contrarian View On The Australian Dollar - May 24, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been mixed: REINZ house sales keep contracting by 7.8% year-on-year in May. Business Manufacturing PMI fell to 50.2 in May. Westpac consumer confidence fell to 103.5 in Q2. Current account surplus widened to N$0.675 billion in Q1. GDP growth was unchanged at 0.6% in Q1 on a quarter-on-quarter basis. However, it increased to 2.5% on a year-on-year basis. NZD/USD increased by 1.1% this week. Our bias remains that the New Zealand dollar has less room to rise compared to other pro-cyclical currencies if global growth picks up. Our SEK/NZD position is 1.3% in the money since initiated. Report Links: Where To Next For The U.S. Dollar? - June 7, 2019 Not Out Of The Woods Yet - April 5, 2019 Balance Of Payments Across The G10 - February 15, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been mixed: Foreign portfolio investment in Canadian securities fell by C$12.8 billion in April. Bloomberg Nanos confidence increased to 56.9 in June. Manufacturing sales fell by 0.6% month-on-month in April. Headline and core inflation both increased to 2.4% and 2.1% year-on-year respectively in May, surprising to the upside. USD/CAD fell by 1.6% this week. The surprising Canadian inflation print, and oil price recovery are all underpinning the Canadian dollar in the short term. This Thursday, Iran shot down a the U.S. drone in Gulf, and fears have been rising of a military confrontation between the U.S. and Iran, which is bullish for oil prices and the Canadian dollar. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Into A Transition Phase - March 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been positive: Exports and imports increased to CHF 21.5 billion and CHF 18.1 billion respectively in May, resulting in a higher trade surplus of CHF 3.4 billion. USD/CHF fell by 1.7% this week. The Swiss franc has strengthened significantly against the U.S. dollar and the euro following the more-than-expected dovish shifts by the ECB and the Fed this week. Our bias remains that the SNB will use the currency as a weapon to defend the economy. Report Links: What To Do About The Swiss Franc? - May 17, 2019 Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been negative: The trade surplus narrowed to 11.3 billion NOK in May. USD/NOK fell by 1.6% this week. The Norges bank raised interest rates from 1% to 1.25%, the third rate hike during the past 12 months, and the Bank is also signaling more to come in the future. The Norges Bank remains the only hawkish central bank among all the G10 countries at this moment. The widening interest rate differentials and bullish oil outlook have been pushing the Norwegian krone higher. Our long NOK/SEK position is now 4.5% in the money. Report Links: Currency Complacency Amid A Global Dovish Shift - April 26, 2019 A Shifting Landscape For Petrocurrencies - March 22, 2019 Balance Of Payments Across The G10 - February 15, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been neutral: Headline and core inflation increased to 2.2% and 2.1 year-on-year respectively in May. Consumer confidence increased to 93.8 in June, while manufacturing confidence fell to 100.2. Unemployment rate increased to 6.8% in May. USD/SEK fell by 0.7% this week. Easing financial conditions worldwide remain a tailwind for global growth. Risk assets are rebounding with higher hopes of a trade deal as Trump will meet Xi at the G20 summit. We believe that the Swedish krona will benefit if global growth picks up in the second half of this year. Report Links: Where To Next For The U.S. Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights As long as the global long bond yield stays near 2 percent or below, European equities will end the year at broadly the same level as now… …but they will experience a dip of at least 4-5 percent along the way. All central banks have pivoted to dovish but the Fed has more easing armoury than the ECB. This means that the recent outperformance of 10-year U.S. T-bonds versus 10-year German bunds can continue. It also means that the euro has a sound structural underpinning versus the dollar. Feature At the start of this year we explained Why 2019 Is A Pivotal Year For Monetary Policy. Today we want to elaborate on that report, and its key observations: Since 2008, no developed economy central bank has been able to hike interest rates sequentially by more than 2 percent before needing to take a breather… and then reverse course. The current vulnerability to tightening emanates from the hyper-sensitivity of financial conditions to rate hikes, rather than from the direct impact on rate-sensitive sectors in the economy. Since October 2017, no stock market rally or sell-off has lasted more than three months or so (Chart Of The Week). These observations are as relevant – or more relevant – now, as they were at the time of our original report.1 Since the Global Financial Crisis, no developed economy central bank has been able to hike interest rates sequentially by more than 2 percent. Chart Of The WeekSince October 2017, No Rally Or Sell-Off Has Lasted More Than Three Months

Since October 2017, No Rally Or Sell-Off Has Lasted More Than Three Months

Since October 2017, No Rally Or Sell-Off Has Lasted More Than Three Months

A 2 Percent Tightening Is The Post-2008 Limit Since the Global Financial Crisis, no developed economy central bank has been able to hike interest rates sequentially by more than 2 percent before having to reverse course (Chart I-2 and Chart I-3). Chart I-2A 2 Percent Sequential Tightening Is The Post-2008 Limit

A 2 Percent Sequential Tightening Is The Post-2008 Limit

A 2 Percent Sequential Tightening Is The Post-2008 Limit

Chart I-3A 2 Percent Sequential Tightening Is The Post-2008 Limit

A 2 Percent Sequential Tightening Is The Post-2008 Limit

A 2 Percent Sequential Tightening Is The Post-2008 Limit

In 2008, Swedish interest rates peaked near 5 percent before collapsing to the zero bound in the financial crisis. But when the Riksbank started its so-called ‘policy normalisation’ in 2010, the interest rate could only reach 2 percent before the central bank had to backtrack; Norway could manage just 1 percent of tightening before its volte-face. Though admittedly, both Sweden and Norway were caught in the maelstrom of the euro debt crisis in 2011-12. However, on the other side of the world and relatively immune to the crisis in Europe, New Zealand could achieve a tightening also of only 1 percent; Korea could manage just 1.25 percent; the Reserve Bank of Australia marched interest rates up by 1.75 percent before taking a breather… and then marched them down again. The consensus was taking far too rosy a view on the global financial system’s capacity to tolerate further tightening. The Federal Reserve raised interest rates sequentially by 2 percent through December 2016 to December 2018, and guess what – it is now on the cusp of reversing course. The ultimate course will have a huge bearing on investment strategy for European equities, bonds and currencies. The Neutral Real Rate Of Interest Is Zero Many economists and strategists expected the Fed to continue hiking through 2019, but this publication pushed back hard. The consensus was taking far too rosy a view on the global financial system’s capacity to tolerate further tightening. Central to this publication’s resistance was, and is, a high-conviction view that the so-called ‘neutral’ real rate of interest – the real interest rate that is neither accommodative nor restrictive, the real interest rate consistent with an economy maintaining full employment while keeping inflation constant – is zero. The neutral rate of interest is very low. In our Special Report Why The Neutral Rate Of Interest Is Zero we proposed that the neutral rate is global rather than region-specific, that it refers to the bond yield rather than to the policy rate, and that it is extremely low. As it happens, the Fed broadly concurs. With the policy rate, bond yield, and inflation all at around 2 percent, the real policy rate and real bond yield are both near zero. At this level the central bank claims that “the policy stance is now in the Committee’s estimates of neutral… and when you get to that range we have to let the data speak to us.”2

Chart I-4

However, the data that is speaking most loudly is not necessarily the economic data, it is the financial market data. Jay Powell has said that if there is a sustained change in financial conditions through any one or more of its components then “that has to play into our thinking.” We think it has (Chart I-4). Comparing Today’s Rich Valuations With 2007 In the aftermath of the dot com bubble burst in 2000, policy interest rates collapsed to very low levels but, crucially, long bond yields did not. This contrasts with the aftermath of the Global Financial Crisis in 2008, during which both policy interest rates and bond yields have plunged to all-time lows (Charts I-5 - I-7). Funny things happen when the long bond yield gets to, and remains, at ultra-low nominal levels. Chart I-5In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

Chart I-6In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

Chart I-7In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

In The Aftermath Of 2000, Bond Yields Did Not Collapse; But In The Aftermath Of 2008, They Did

The difference between the post-2000 and post-2008 policy responses can be summarized in two letters: QE. For all its apparent complexity, QE is actually a very simple monetary policy tool. It is just a mechanism for signalling that the policy interest rate will remain low for an extended period. Thereby, QE pulls down the long-term interest rate, which is to say the long bond yield. The double-digit rally over the past six months is technically extended. But as we have consistently pointed out on these pages, funny things happen when the long bond yield gets to, and remains, at ultra-low nominal levels. We refer readers to our other reports for the details, but in a nutshell the risk of owning bonds converges to the risk of owning equities and other so-called ‘risk-assets’. The upshot of this risk convergence is that investors price these risk-assets to deliver the same ultra-low nominal return as bonds, meaning that the valuation of the risk-assets soars.3 Chart I-8Since 2015, The Global Long Bond Yield Has Been Unable To Remain Above 2.5 Percent

Since 2015, The Global Long Bond Yield Has Been Unable To Remain Above 2.5 Percent

Since 2015, The Global Long Bond Yield Has Been Unable To Remain Above 2.5 Percent

All of which brings us to the crucial point. The post-2000 extreme policy easing distorted the real economy. It engineered a credit boom. So the fragility to the subsequent policy tightening emanated from the real economy, and particularly the most rate-sensitive sectors in the economy such as mortgage lending and housing. In contrast, the post-2008 extreme policy easing – driven by QE – has distorted the valuation of risk-assets. Moreover, the value of global risk-assets, at $400 trillion dwarfs the $80 trillion global economy by five to one. So the current fragility to policy tightening does not emanate from the real economy, it emanates from the hyper-sensitivity of financial conditions to higher bond yields (Chart 8). Some European Investment Implications The integration of global capital markets means that the valuation anchor for European – and all regional – stock markets now comes from the global long bond yield, which we define as the simple average of the 10-year yields in the euro area, U.S., and China. Through the past five years, the inability of the global long bond yield to remain above 2.5 percent confirms the hyper-sensitivity of financial conditions to higher interest rates. And it suggests that the ‘neutral’ rate on this measure is around 2 percent. The good news is that this measure now stands slightly below neutral at 1.9 percent. The euro has a sound structural underpinning versus the dollar. At around this level of the global long bond yield, the rich valuation of European equities has some support. That said, the double-digit rally over the past six months is technically extended, as most of the things that could go right did go right – central banks pivoted to dovish, euro area growth rebounded, and, until recently, geopolitical risks were easing. Hence, as long as the global long bond yield stays near 2 percent or below, we expect European equities to end the year at broadly the same level as now, though our technical signals do strongly suggest a dip of at least 4-5 percent along the way (Chart I-9). Chart I-9The Double-Digit Rally In Stock Markets Over The Past Six Months Is Technically Extended

The Double-Digit Rally In Stock Markets Over The Past Six Months Is Technically Extended

The Double-Digit Rally In Stock Markets Over The Past Six Months Is Technically Extended

Chart I-10The Fed Has More Easing Armoury Than The ECB

The Fed Has More Easing Armoury Than The ECB

The Fed Has More Easing Armoury Than The ECB

As regards bonds and currencies, all central banks have pivoted to dovish but the Fed has more easing armoury than the ECB (Chart I-10). This means that the recent outperformance of 10-year U.S. T-bonds versus 10-year German bunds can continue. It also means that the euro has a sound structural underpinning versus the dollar. However, this structural underpinning also applies to the yen, and until we get some clarity on Brexit we prefer the yen over the euro. Fractal Trading System* In line with the main body of this report and Chart 9, we see evidence that the double-digit rally in stock markets over the past six months is technically extended. Accordingly, this week’s recommended trade is to short the MSCI All-Country World index, setting the profit target at 4 percent with a symmetrical stop-loss. This leaves us with four open positions. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes.

Global Financial Services Vs. Market

Global Financial Services Vs. Market

* For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Please see the European Investment Strategy Weekly Report ‘Why 2019 Is A Pivotal Year For Monetary Policy’ February 7, 2019 available at eis.bcaresearch.com. 2 Please see the European Investment Strategy Special Report ‘Why The Neutral Rate Of Interest Is Zero’ June 6, 2019 available at eis.bcaresearch.com. 3 Please see the European Investment Strategy Weekly Report ‘Risk: The Great Misunderstanding Of Finance’ October 25, 2018 available at eis.bcaresearch.com. Fractal Trading System

Image

Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

The Bank of Japan did little to feed expectations of a monetary policy easing. Governor Kuroda acknowledged that risks surrounding global trade are elevated, but nonetheless also mentioned that he expects Chinese growth to accelerate in the second half of…

The Fed refrained from cutting rates yesterday, but has set a very high bar not to do so in July. Not only was dropping the word “patience” an important signal, but also, the “dot plot” now shows that seven FOMC members are calling for two rate cuts this year…

Analysis on Thailand is available below. Feature Last week we were on the road meeting with some of our U.S. clients. This week’s report presents some of the key topics of our discussions in a Q&A format. Question: You have been downplaying the potentially positive impact of lower bond yields in advanced economies on EM risk assets. Why do you think lower bond yields in developed markets (DM) and potential rate cuts by DM central banks won’t suffice to lift EM markets on a sustainable basis? Answer: Falling interest rates are positive for share prices when profits are growing, even at a slower rate. When corporate profits are contracting, lower interest rates typically do not preclude equity prices from dropping. Presently, EM and Chinese corporate earnings are shrinking rapidly (Chart I-1). This is the primary reason why we believe DM monetary easing will not help EM share prices much. Furthermore, EM exchange rates follow relative EPS cycles in local currency terms (Chart I-2). In short, EM currencies are driven by relative corporate profitability between EM and the U.S. – not by interest rate differentials. Chart I-1EM & China EPS Are Contracting

EM & China EPS Are Contracting

EM & China EPS Are Contracting

Chart I-2Relative EPS And Exchange Rate

Relative EPS And Exchange Rate

Relative EPS And Exchange Rate

The contraction in EM and China EPS has not been caused by higher interest rates and slump in DM domestic demand. Rather, the EM/China profit contraction has been due to China’s economic slowdown spilling over to the rest of EM. Crucially, there is no empirical evidence that interest rate cuts and QEs in DM preclude EM selloffs when EM/Chinese growth is slumping. Specifically: Chart I-3A and I-3B illustrate that neither the level of G4 central banks’ assets nor their annual rate of change correlates with EM share prices or EM local bonds’ total returns in U.S. dollar terms. Hence, QEs have not always guaranteed positive returns for EM financial markets. Chart I-3APace Of QE And EM Performance

Pace Of QE And EM Performance

Pace Of QE And EM Performance

Chart I-3BPace Of QE And EM Performance

Pace Of QE And EM Performance

Pace Of QE And EM Performance

Chart I-4U.S. Treasury Yields And EM Performance

U.S. Treasury Yields And EM Performance

U.S. Treasury Yields And EM Performance

Chart I-4 demonstrates the correlation between U.S. 5-year Treasurys yields on the one hand and EM spot exchange rates, EM sovereign credit spreads and EM share prices on the other. There has been no stable relationship – at times it has been positive, and at other times negative. We are not implying that DM interest rates have no bearing on EM financial markets. Our point is that lower interest rates and QEs in DM do not constitute sufficient conditions for EM financial markets to rally. Even though DM monetary policy has not been the driving force of cyclical fluctuations in EM financial markets, it has had a structural impact. QEs and lower bond yields in DM have prompted an expanded search for yield and have produced substantial compression in risk premia worldwide. For example, Chart I-5 demonstrates that excess returns on EM corporate bonds have historically been correlated with the global manufacturing cycle, but the correlation has diminished in recent years. The widening gap between the two lines is due to investors’ search for yield. Investors have bought and continue to hold securities of “zombie” companies and countries that have low productivity and poor fundamentals. In short, QEs have undermined the efficiency of global capital allocation. This is marginally adverse for productivity in the global economy in the long run. Question: But doesn’t DM monetary policy influence DM demand, which in turn affects EM corporate profits? Answer: DM monetary policy influences DM domestic demand, but there is little correlation between DM domestic demand and EM corporate profits. For example, U.S. import volumes have been growing at a decent pace, yet EM corporate profits have shrunk (Chart I-6). Indeed, robust growth in U.S. imports did not preclude EM EPS contraction in 2012, 2014-‘15 and 2018-‘19, as shown in this chart. Chart I-5Fundamentals Have Become Less Important Due To QE Programs

Fundamentals Have Become Less Important Due To QE Programs

Fundamentals Have Become Less Important Due To QE Programs

Chart I-6EM EPS And U.S. Imports

EM EPS And U.S. Imports

EM EPS And U.S. Imports

Chart I-7 reveals additional evidence of the diminished impact of U.S. growth on Asian exports. Korean, Taiwanese, Japanese and Singaporean exports to the U.S. are growing at 7% rate, while their shipments to China are contracting at an 11% rate from a year ago as of May. As a result, these countries’ overall exports are shrinking because they ship to China considerably more than they do to the U.S. We are not implying that DM interest rates have no bearing on EM financial markets. Our point is that lower interest rates and QEs in DM do not constitute sufficient conditions for EM financial markets to rally. The current global slowdown did not originate in the U.S. or Europe. Rather, it originated in China and has spilt across the world, affecting the economies that sell to China the most. The deceleration in global trade can be tracked to Chinese imports contraction (Chart I-8). Chart I-7Asia's Exports To China And U.S.

Asia's Exports To China And U.S.

Asia's Exports To China And U.S.

Chart I-8Chinese Imports And Global Trade

Chinese Imports And Global Trade

Chinese Imports And Global Trade

U.S. manufacturing is the least exposed to China, which is the main reason why it was the last shoe to drop in the global manufacturing recession. Question: So, what drives EM business cycles if it is not DM growth and DM interest rates? Chart I-9China's Credit & Fiscal Impulse And EM EPS

China's Credit & Fiscal Impulse And EM EPS

China's Credit & Fiscal Impulse And EM EPS

Answer: The key and dominant driver of EM risk assets – stocks, credit markets and currencies – has been the global trade and EM/China growth cycles. There is a much stronger correlation between EM financial markets and the global business cycle in general, and Chinese imports in particular than with DM interest rates. In turn, Chinese imports are driven by its capital spending cycle. 85% of the mainland’s good imports are composed of industrial goods and devices, machinery, chemicals, various commodities and autos. Only 15% are non-auto consumer goods. Meanwhile, the credit/money cycles drive capital spending. That is why China’s credit and fiscal spending impulse leads EM corporate profits (Chart I-9). This is also why we spend a significant amount of time analyzing and discussing China's credit cycle. Question: Why has the policy stimulus in China not revived growth in its economy and its suppliers around the world? Answer: Our aggregate credit and fiscal spending impulse bottomed in January of this year, but its recovery has so far been timid. In the past, this indicator led China’s business cycle and the global manufacturing PMI by an average of about nine months (Chart I-10, top panel) and EM corporate profits by 12 months (Chart I-9). According to this pattern, the bottom in global manufacturing should occur in August of this year. However, global share prices have not led global manufacturing PMI during this decade; they have instead been coincident (Chart I-10, bottom panel). Hence, there was no historical justification for global share prices to rally since early January - well ahead of a potential bottom in the global manufacturing PMI in August. The current global slowdown did not originate in the U.S. or Europe. Rather, it originated in China and has spilt across the world, affecting the economies that sell to China the most. That said, due to the U.S.-China confrontation and other structural reasons currently prevailing in China – including high levels of indebtedness and more regulatory scrutiny over shadow banking as well as local government debt – a recovery in mainland household and corporate spending is likely to be delayed. Crucially, as we have documented in previous reports, the marginal propensity to spend for consumers and companies continues to fall (Chart I-11). This is the opposite of what occurred in early 2016. Chart I-10Chinese Stimulus, Global Manufacturing And Global Stocks

Chinese Stimulus, Global Manufacturing And Global Stocks

Chinese Stimulus, Global Manufacturing And Global Stocks

Chart I-11China: What Is Different From 2016

China: What Is Different From 2016

China: What Is Different From 2016

Overall, a revival in China’s growth will likely take longer to unfold and EM risk assets will likely sell off anew before bottoming. Chart I-12Global Slowdown Is Not Yet Over

Global Slowdown Is Not Yet Over

Global Slowdown Is Not Yet Over

Chart I-13Global Semiconductor Demand Is Shrinking

Global Semiconductor Demand Is Shrinking

Global Semiconductor Demand Is Shrinking

Question: Apart from China’s credit and fiscal spending impulse and marginal propensity to spend among households and companies, what other indicators are you monitoring to gauge a bottom in the global manufacturing cycle? Answer: Among many variables and indicators we continuously monitor, there are a few we have been paying particular attention to: The difference between global narrow (M1) and broad money growth correlates well with global corporate earnings (Chart I-12). The rationale for this indicator is that it is akin to the marginal propensity to spend: When demand deposits (M1) outpace time/savings deposits, it is indicative that households and companies are getting ready to spend on large-ticket items or kick off capital spending, and vice versa. Presently, this narrow-to-broad money growth differential continues to point to lower global growth. Last week we published a report on the global semiconductor industry, arguing that upstream demand for semiconductors is withering as sales of servers, smartphones, PCs and autos are all shrinking globally (Chart I-13). With consumption of these goods contracting, demand for semiconductors remains lackluster, and semiconductor prices are still deflating (Chart I-14). Hence, semiconductor prices can be used as an indicator of final demand dynamics in many important segments of the global economy. China’s Container Freight Index – the price to ship containers – is also currently lackluster, reflecting weak global trade dynamics (Chart I-15, top panel). Chart I-14Semiconductor Prices Are Still Deflating

Semiconductor Prices Are Still Deflating

Semiconductor Prices Are Still Deflating

Chart I-15Global Shipments Are Very Weak

Global Shipments Are Very Weak Global Shipments Are Very Weak

Global Shipments Are Very Weak Global Shipments Are Very Weak

In the U.S., both total intermodal carloads and railroad carloads excluding petroleum and coal are tanking, reflecting subsiding growth (Chart I-15, middle and bottom panel). In turn, Chinese imports continue to contract. This is the primary channel in terms of how the Middle Kingdom affects the rest of the world economy. From the rest of the world’s perspective, China is in recession because their shipments to the mainland are shrinking. In China and Taiwan, the seasonally adjusted manufacturing PMI new orders have rolled over after the temporary pick up early this year (Chart I-16). Finally, we are monitoring our Reflation Indicator and Risk-On/Safe-Haven Currency Ratio (Chart I-17). Both are market-based indicators and are very sensitive to global growth conditions – especially to the dynamics in commodities markets – making them very pertinent to EM investors. Chart I-16Manufacturing PMI: New Orders Seasonally-Adjusted

Manufacturing PMI: New Orders Seasonally-Adjusted

Manufacturing PMI: New Orders Seasonally-Adjusted

Chart I-17Market-Based Indicators

Market-Based Indicators

Market-Based Indicators

As with any marked price-based signals, both are very volatile. Even though both indicators have rebounded in recent days, only a major trend reversal matters for macro investors. Technically speaking, the profile of both indicators is consistent with a breakdown rather than a breakout. Question: You have highlighted that EM corporate EPS is contracting. How widespread is the profit contraction, and how long will it persist? Answer: EM corporate EPS contraction is widespread across almost all sectors. Chart I-18A and I-18B illustrate EPS growth in U.S. dollar terms for all sectors. EPS growth is negative for most sectors, close to zero for three (technology, financials and materials) and still positive for the energy sector. However, technology, materials and energy EPS are heading into contraction, given the drop in semiconductor, industrial metals and oil prices, respectively. Chart I-18ASynchronized EM EPS Contraction

Synchronized EM EPS Contraction

Synchronized EM EPS Contraction

Chart I-18BSynchronized EM EPS Contraction

Synchronized EM EPS Contraction

Synchronized EM EPS Contraction

Consequently, all EM equity sectors will soon be experiencing synchronized profit contraction. EM corporate EPS contraction is widespread across almost all sectors. Our credit and fiscal spending impulse for China leads EM EPS growth by about 12 months, and it currently entails that the profit contraction will continue to deepen all the way through December (Chart I-9 on page 6). It would be surprising if EM share prices stage a major rally amid a hastening decline in corporate EPS (please refer to Chart I-1 on page 1). Arthur Budaghyan Chief Emerging Markets Strategist arthurb@bcaresearch.com Thailand: A Defensive Play Within EM The Thai parliament has elected to keep the ex-military general Prayuth Chan-ocha as the country’s prime minister. This will instill political stability for now, which is positive for investor confidence. In absolute terms, Thai financial markets are leveraged to global trade and will, therefore, sell off if our negative views on the latter and EM risk assets play out. Chart II-1Thailand's Current Account Is In Surplus

Thailand's Current Account Is In Surplus

Thailand's Current Account Is In Surplus

Relative to their EM peers, Thai equities, credit, currency and domestic bonds will continue outperforming: The Thai current account balance remains in large surplus, which provides a large cushion for the Thai baht amid the slowdown in global growth (Chart II-1). Critically, Thailand is less exposed to China and is more leveraged to the U.S. and Europe than its EM peers. Thailand’s shipments to China account for 12% of the former’s total exports, while exports to the U.S. and EU together account for 21%. Both U.S. and European imports are holding up better than those of China. Thailand also has the lowest foreign debt obligations (FDO) among EM countries. FDOs measure the sum of short-term claims, interest payments and amortization over the next 12 months. The country’s current FDOs stand at 8% relative to its exports of goods and services and 12% relative to the central bank’s foreign exchange reserves. The rest of EM countries have much higher ratios. In addition, foreign ownership of local currency bonds is amongst the lowest in the region (18%). As a result, currency depreciation will not trigger major portfolio outflows and a self-reinforcing downtrend in Thai financial markets. Thailand also has the lowest foreign debt obligations (FDO) among EM countries. Chart II-2Thailand: Moderate Growth In Private Consumption

Thailand: Moderate Growth In Consumption

Thailand: Moderate Growth In Consumption

Thailand’s private consumption is growing reasonably well (Chart II-2, top panel). Likewise, passenger and commercial vehicle sales are rising and so is household credit (Chart II-2, bottom two panels). The Thailand MSCI index carries a large weight in domestic and defensive stocks such as transportation, utilities, telecommunication, and consumer staples. These sectors will benefit from moderate consumption growth. In fact, Thai equity outperformance versus EM has been justified by its non-financial companies’ EBITDA outpacing that of EM non-financials (Chart II-3). This trend remains intact. Concerning banks, Thailand’s commercial banks suffer from credit excesses, as do many of their EM peers. However, Thai commercial banks have been responsible in terms of recognizing NPLs and have been properly provisioning for them (Chart II-4). This is contrary to many other EM banks. This means that share prices of Thai commercial banks will outperform their EM counterparts. Finally, although the Thai bourse is more expensive than its EM counterparts, relative equity valuation will likely get even more stretched before a major reversal occurs. Given our cautious view on overall EM, we continue to prefer this richly valued and defensive bourse to the more cyclical, albeit cheaper, but fundamentally vulnerable EM peers. Chart II-3Equity Outperformance Has Been Justified By Earnings

Equity Outperformance Has Been Justified By Earnings

Equity Outperformance Has Been Justified By Earnings

Chart II-4Thai Commercial Banks Are Well Provisioned

Thai Commercial Banks Are Well Provisioned

Thai Commercial Banks Are Well Provisioned

Bottom Line: Investors should keep an overweight position in Thai equities, currency, domestic bonds and credit markets. Ayman Kawtharani, Editor/Strategist ayman@bcaresearch.com Footnotes Equity Recommendations Fixed-Income, Credit And Currency Recommendations

While the Fed might deliver a rate cut at one of the next few meetings, it is unlikely to lower rates by more than the 84 bps that are priced into the yield curve for the next 12 months. Ultimately, we expect Treasury yields to be higher on a 6-12 month…

Highlights Fed: Depressed U.S. Treasury yields now discount more rate cuts than the FOMC is likely to deliver, even for “insurance” purposes to offset the negative growth impacts from trade policy uncertainty. Maintain a below-benchmark strategic U.S. duration stance, and stay underweight the U.S. in global hedged government bond portfolios. JGBs: The low yield beta of Japanese government bonds can be a useful diversifier of duration risk in global government bond portfolios. We recommend taking advantage of this by increasing allocations to Japan, out of U.S. Treasuries, on a currency-hedged basis (in USD). Feature June FOMC Preview: Hawks & Doves, Living Together, Mass Hysteria! The next two days will be critical for global bond markets, with the U.S. Federal Reserve set to update its outlook for U.S. monetary policy. The only logical interpretation of current market pricing is that bond investors now expect a major hit to U.S. (and global) business confidence and economic growth from a U.S.-China trade war - without any lasting pickup in U.S. inflation from the tariffs. The Fed is stuck in a difficult position at the moment. Looking purely at the state of the economy, there is no immediate need for rate cuts. The unemployment rate is still low at 3.6%; real GDP growth was a solid 3.1% in Q1 and the Atlanta Fed’s GDPNow model estimates Q2 growth will be a trend-like 2.1%; and consumer confidence remains healthy. Our Global Duration Indicator has hooked up, driven by an improving global leading economic indicator and stabilizing economic sentiment surveys. Yet despite this, U.S. Treasury yields have melted down to levels consistent with much weaker economic growth and inflation, with -83bps of Fed rate cuts now discounted over the next twelve months (Chart of the Week). Chart of the WeekToo Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Too Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Too Much Economic Pessimism Now Discounted In U.S. Treasury Yields

Chart 2U.S. Business Confidence: Fraying On The Edges

U.S. Business Confidence: Fraying On The Edges

U.S. Business Confidence: Fraying On The Edges

The only logical interpretation of current market pricing is that bond investors now expect a major hit to U.S. (and global) business confidence and economic growth from a U.S.-China trade war - without any lasting pickup in U.S. inflation from the tariffs. Reducing interest rates now would be the appropriate pre-emptive policy response, even if the current health of the economy does not justify a need to ease. A look at various U.S. business confidence surveys confirms that interpretation. Both the NFIB Small Business Confidence index and the Duke CFO U.S. Economic Outlook index are still at fairly high levels, but have clearly softened in recent months (Chart 2, top panel). The deterioration in the Duke CFO measure has come from a sharp fall in the percentage of respondents who are more optimistic on the U.S. economic outlook – a move mirrored by the deterioration in the Conference Board’s survey of CEO Confidence (second panel). On the inflation side, the Duke CFO survey shows that companies have dramatically cut back on their planned increases for labor compensation over the next year, from 5.1% in the March survey to 3.8% in the June survey (third panel). Plans for price increases over the next year have also collapsed from 2.7% to 1.4% in the June survey (bottom panel). As the FOMC deliberates, the doves will make the following case for an insurance rate cut now (Chart 3): The U.S. manufacturing sector has caught up with the global downturn. Market-based inflation expectations remain below levels consistent with the Fed’s 2% PCE inflation target (between 2.3% and 2.4% using CPI-based TIPS breakevens). The 10-year/3-month U.S. Treasury yield curve remains inverted, typically a sign that monetary policy has become restrictive. The trade-weighted dollar remains near the post-crisis highs, even as U.S. bond yields have plunged. Global economic policy uncertainty remains elevated. Meanwhile, the hawks on the FOMC will argue that easing would be premature (Chart 4): Chart 3The Case For Fed Rate Cuts

The Case For Fed Rate Cuts

The Case For Fed Rate Cuts

Chart 4The Case Against Fed Rate Cuts

The Case Against Fed Rate Cuts

The Case Against Fed Rate Cuts

U.S. equities are only 2% below the all-time high. High-yield spreads are stable and nowhere close to the peaks seen during previous bouts of market turmoil. A similar argument applies for market volatility, with the VIX index also relatively subdued in the mid-teens. Global leading economic indicators are bottoming out. Underlying realized inflation trends – average hourly earnings growth, trimmed mean inflation measures – are sticky, at cyclical highs. Given the compelling arguments on both sides, the most likely outcome tomorrow will be the Fed holding off on cutting rates, but making a clear case for what it will take to ease at the July 30-31 FOMC meeting. We imagine that checklist to include: a) Failure of U.S.-China trade talks at the G-20 summit later this month to progress toward an agreement. b) The June U.S. Payrolls report, to be released on July 5th, confirming that the soft May reading was not a one-off. c) The June Consumer Price Index report to be released on July 11th, and the May PCE deflator reading out on July 28th, showing no acceleration of some of the “transitory” components that the Fed believes has been dampening U.S. core inflation. d) A major pullback in U.S. equities and/or a widening of U.S. corporate bond spreads, leading to tighter U.S. financial conditions. Chart 5The Market & FOMC Disagree On The Terminal Rate

The Market & FOMC Disagree On The Terminal Rate

The Market & FOMC Disagree On The Terminal Rate

A new set of FOMC economic projections will be unveiled at this meeting, providing the intellectual cover for the Fed to signal that a rate cut is imminent. A new set of interest rate projections will also be provided. While this current edition of the FOMC has been downplaying the importance of the message implied by those interest rate projections, any movement in the “dots” will be noticed by the markets. The dot plot has only existed in a phase of expected Fed tightening. A shift to a projected ease would be momentous. In particular, any shift in the longer run “terminal rate” dot would be critical to ascertaining the Fed’s reaction function (Chart 5). This is especially true given the wide gap between our estimate of the market expectation of the terminal funds rate for this cycle (the 5-year U.S. Overnight Index Swap rate, 5-years forward, which is currently at 2%) and the median FOMC member estimate of the terminal rate from the last set of economic projections in March (2.8%). If the Fed were to make the case for an insurance rate cut tomorrow, while also lowering the terminal rate estimate, this would suggest that the FOMC was growing more concerned over the medium-term economic outlook as fewer future rate hikes would be needed. More dovish guidance on near-term rate moves, but without any change in the terminal rate projection, would imply that the Fed would view any insurance rate cut as a temporary measure that would need to be reversed at a later date if global uncertainty abates, U.S. growth recovers and U.S. inflation rebounds. Whatever the outcome of this week’s FOMC meeting, U.S. Treasury yields now discount a lot of bad news on both growth and inflation. Both the real and inflation expectations component of the benchmark 10-year Treasury yield are at critical support levels (Chart 6), suggesting that yields can only decline further in the face of incrementally more bearish economic data. Given the risk/reward tradeoff of yields at current levels, we do not recommend chasing this Treasury market rally, and prefer to position for an eventual rebound in yields. Chart 6Not Much Downside Left For Treasury Yields

Not Much Downside Left For Treasury Yields

Not Much Downside Left For Treasury Yields