Monetary

Our Counterpoint Strategy team believes the equity bull market’s biggest risk is the reversal of the divergence between Japanese and US real yields. Japan’s real policy interest rate differential versus the US stands at an unprecedented and unsustainable…

Flash estimates for European consumer confidence met expectations at -12.5 in October, rising from -12.9 in September. Despite this positive development, Euro Area sentiment remains poor. Consumer confidence remains below its long-term average and near the…

After cutting three times already since June, the Bank of Canada fulfilled market expectations and cut the overnight rate by 50 bps to 3.75%. The BoC sees risks around inflation as roughly balanced over its projection horizon, and is focused on “sticking the…

The Federal Reserve’s Beige Book, its survey of business contacts, shows an economy that has seen little growth since early September. The Fed’s contacts confirmed the manufacturing recession reflected in other data sources. Loan demand was mixed, as…

The US dollar had a strong October thus far, breaching its 20-,50- and 200-day moving averages with a 4% increase and only three trading days in the red. The DXY now sits above where it was before the August selloff in risk assets. What’s behind this…

The US election is tightening in its final weeks, and the latest polls challenge our Geopolitical Strategy’s base case of a Democratic White House. The original thesis was built on the premise of a Democratic incumbent advantage, after only four years in…

A Donald Trump victory would send bond yields higher during the next few weeks, but yields will fall in 2025 no matter the election outcome.

Dear client, We are launching a new type of Daily Insight titled “Cross-Asset Focus”, where we delve into the dynamics between multiple asset classes, tying them to the current macro and market regimes. The inaugural entry looks at the dynamics between…

According to the latest estimate of the output gap, the US economy still operates above potential. Continued overheating – a no-landing scenario – would cause a drastic re-pricing across markets which expect a near-perfect soft-landing. The output gap is…

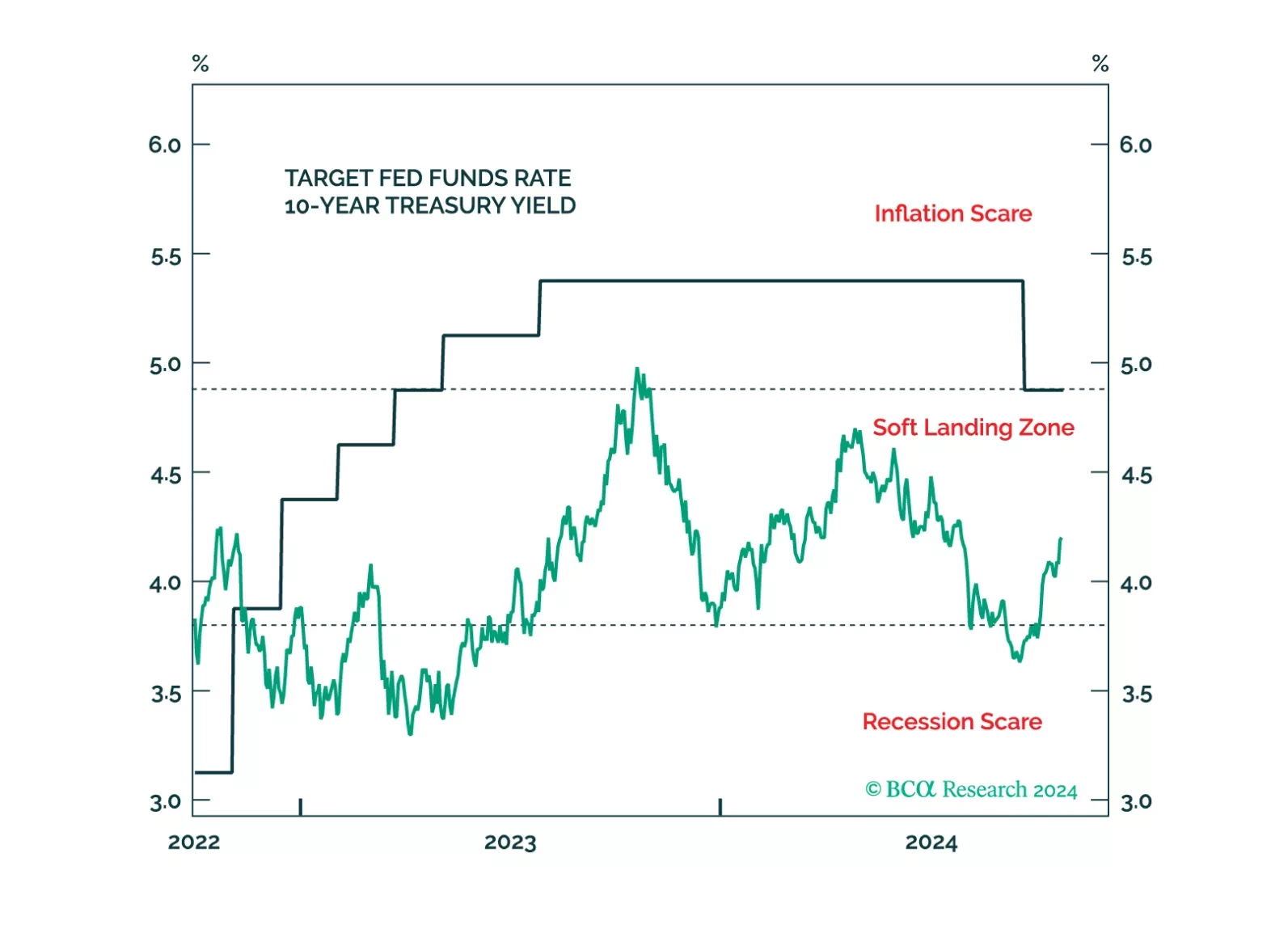

US Treasury yields rose nearly 60 bps since their September lows, with the 10-year maturity recently reaching 4.2%. This move was a bear steepening, the front of the curve did not rise as much. Positive economic surprises mainly drove this spike, but the…