Monetary

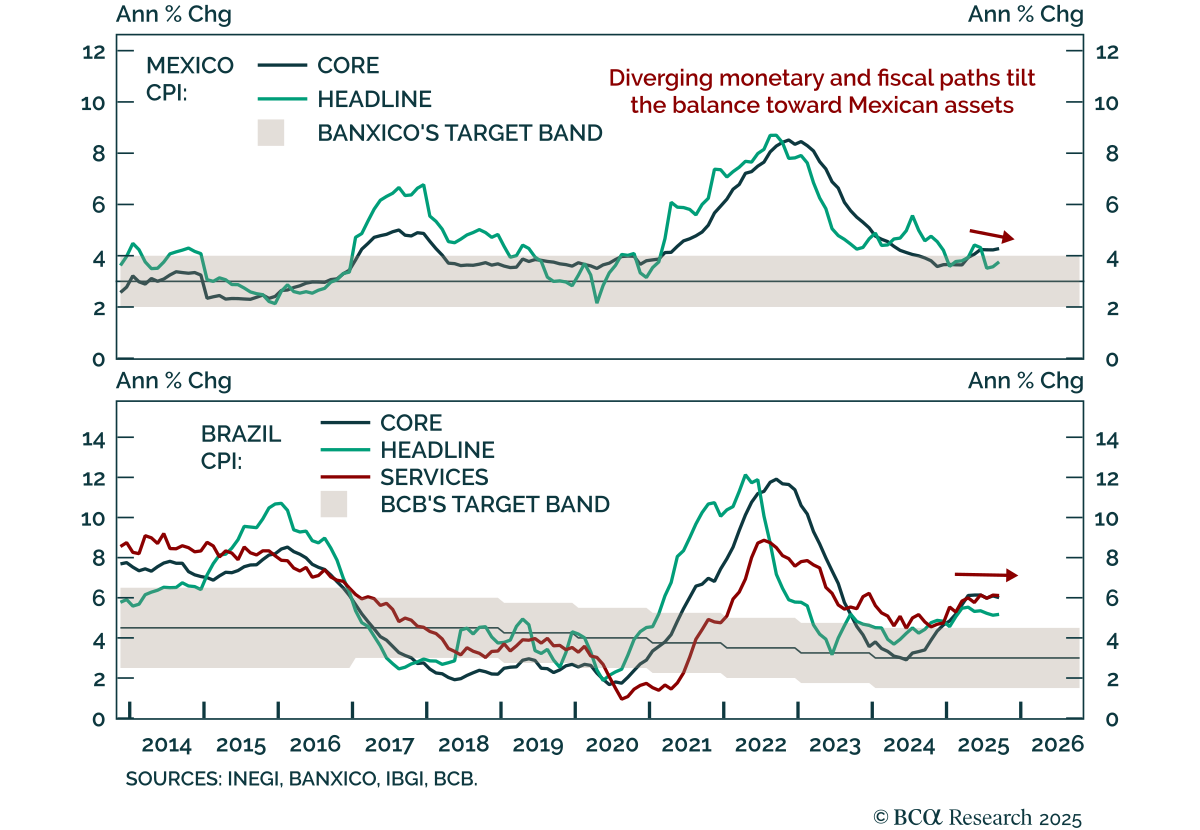

September CPI releases in Brazil and Mexico reinforce a divergent inflation and policy outlook that supports an overweight stance in Mexican local bonds and currency relative to Brazilian assets. Brazil’s headline CPI at 5.2% was slightly higher than in…

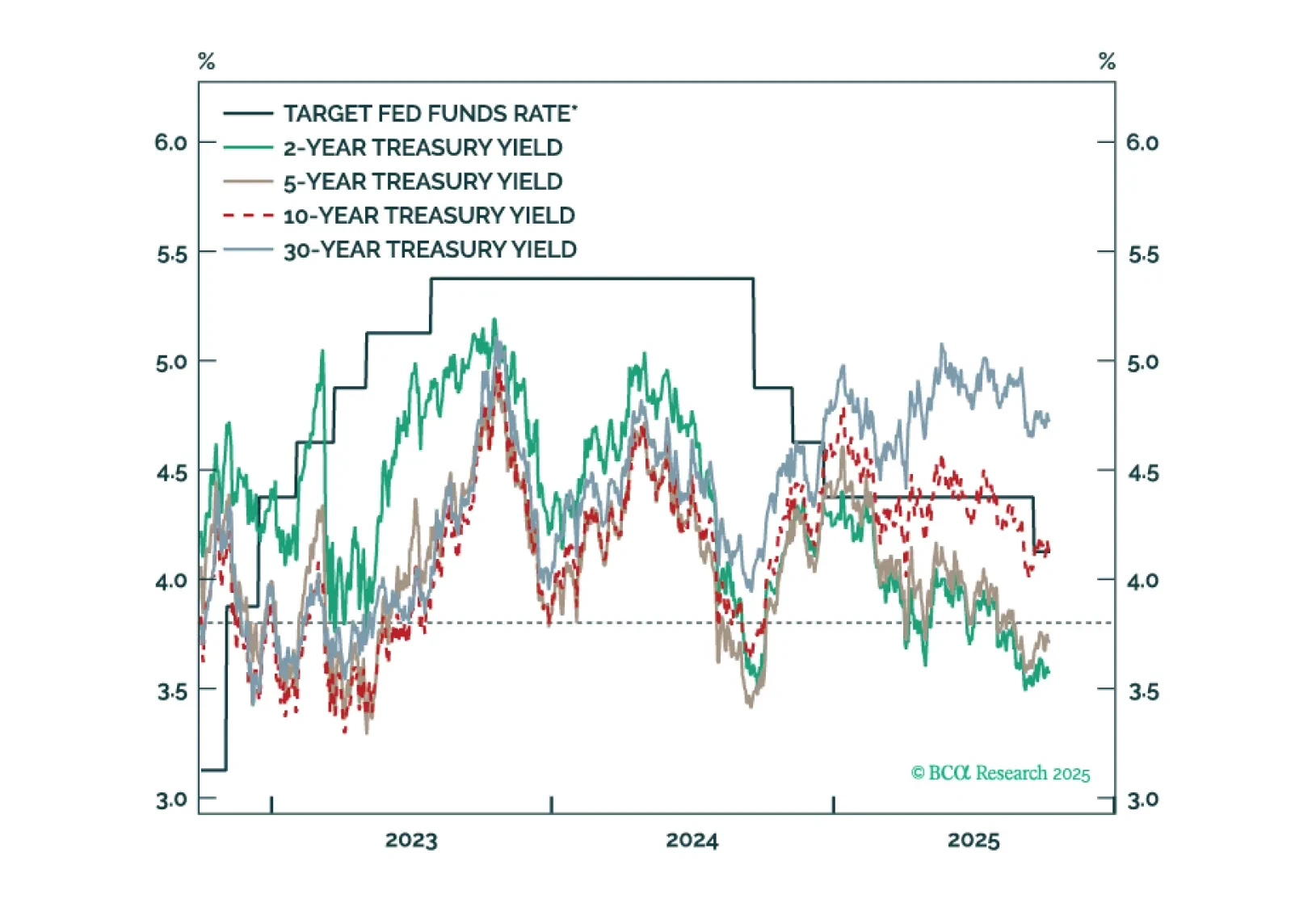

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

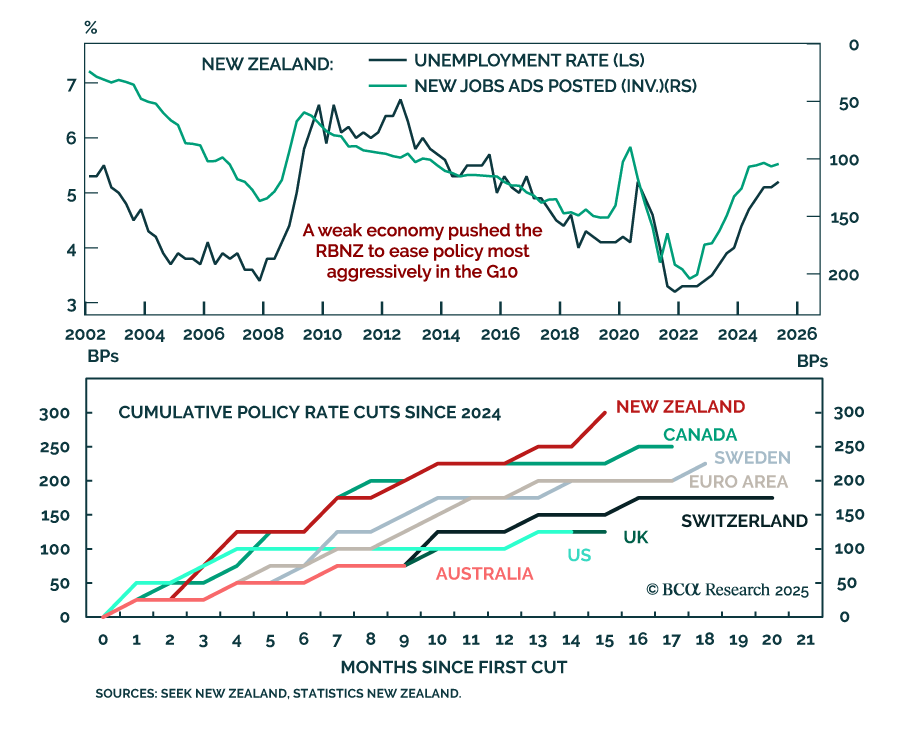

The Reserve Bank of New Zealand (RBNZ) cut the policy rate by 50 basis points to 2.5% and signaled further easing ahead, supporting an overweight stance in New Zealand government bonds and underweight in the NZD.The larger-than-expected move followed the 0.9%…

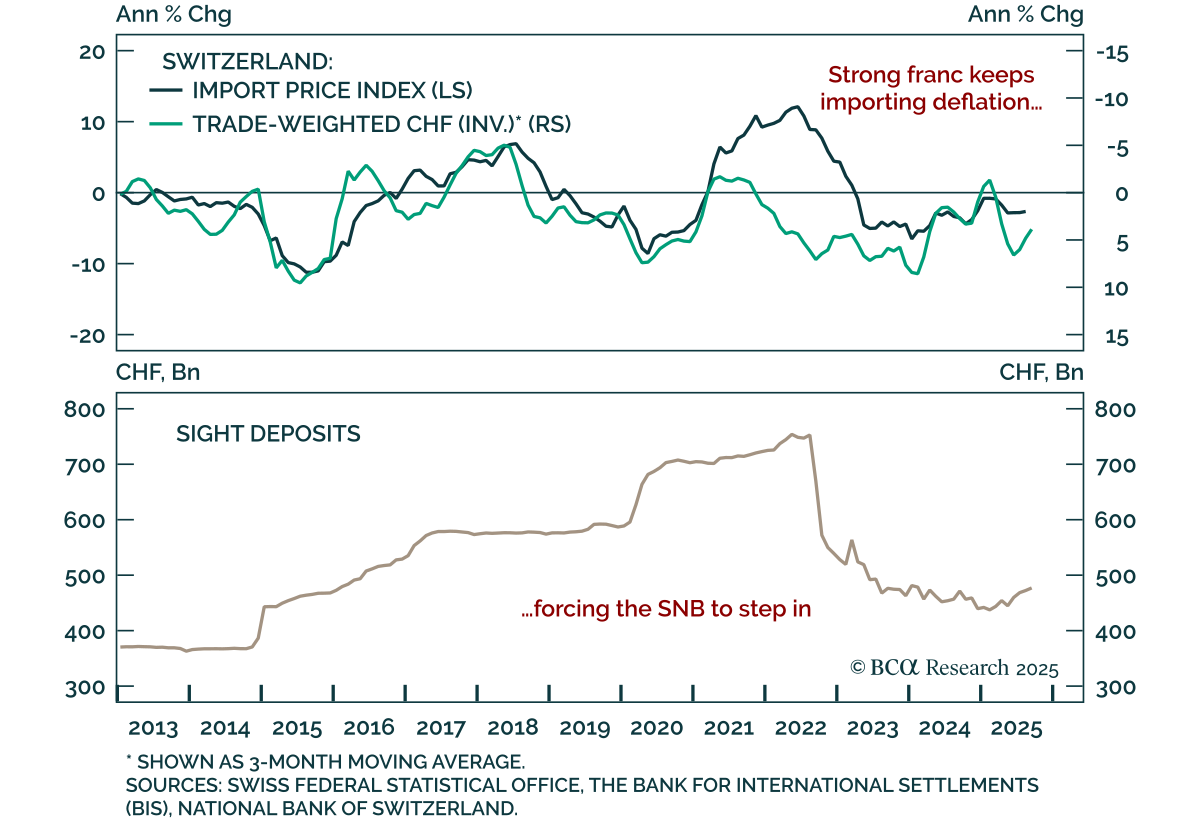

Expect greater currency interventions and negative policy rates from the Swiss National Bank (SNB), reinforcing a neutral stance on CHF and Swiss sovereign debt over the next 12 months. In recent joint statement on foreign exchange practices, the…

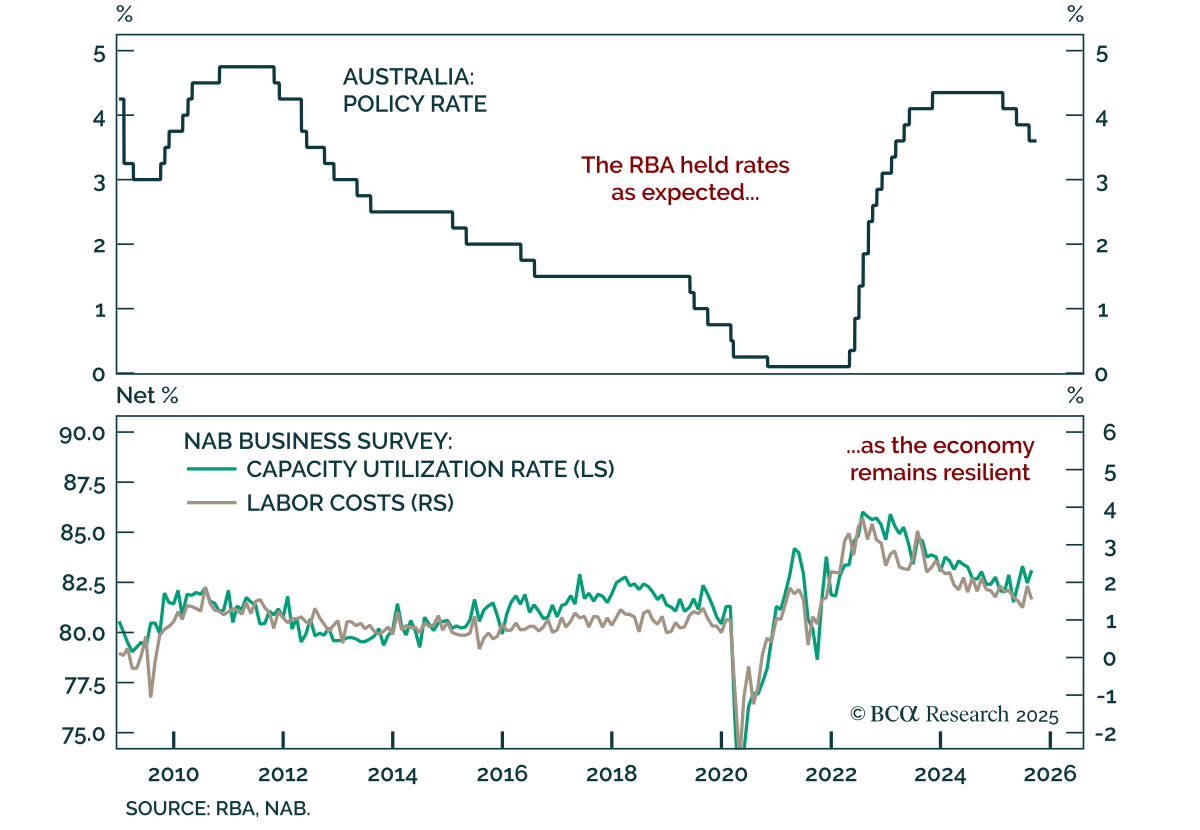

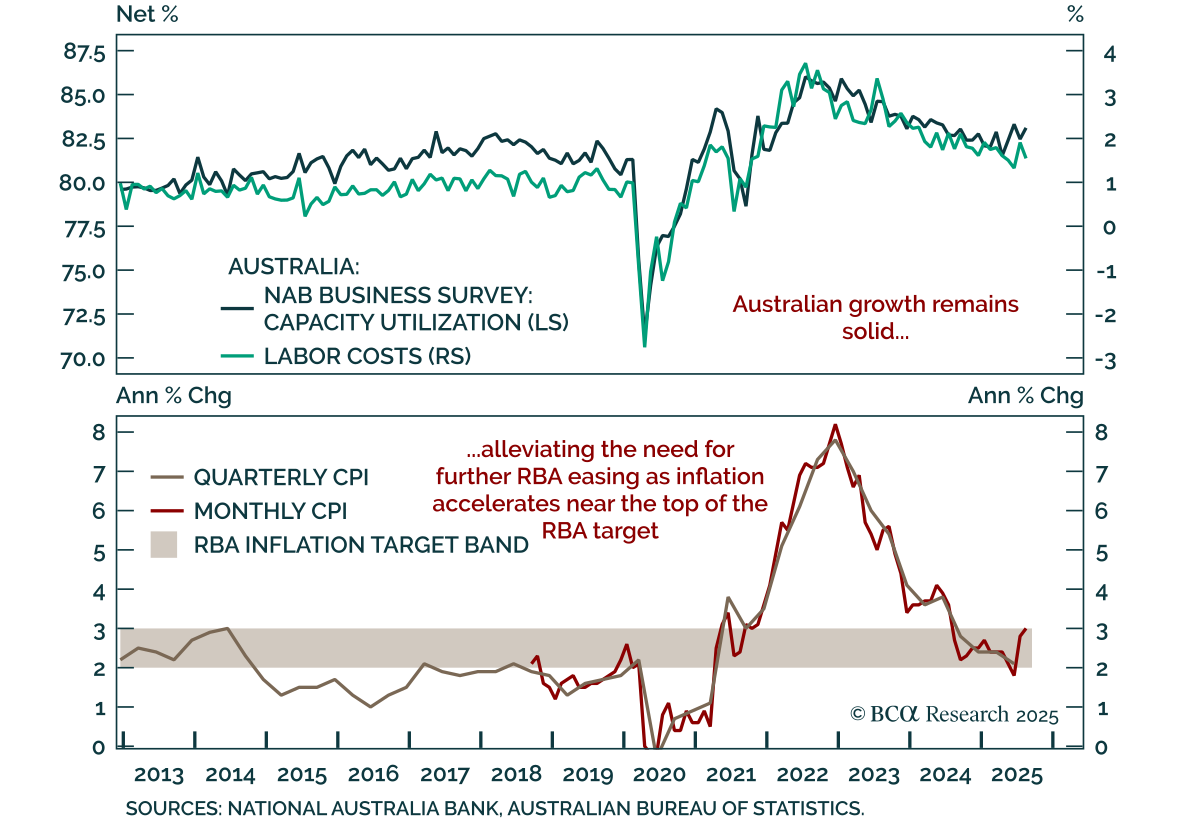

The RBA held rates at 3.6% as expected, maintaining caution as inflation could prove stronger than expected. Policy remains slightly restrictive, and at most one additional cut is on the table as the central bank has achieved a soft landing. While the RBA has…

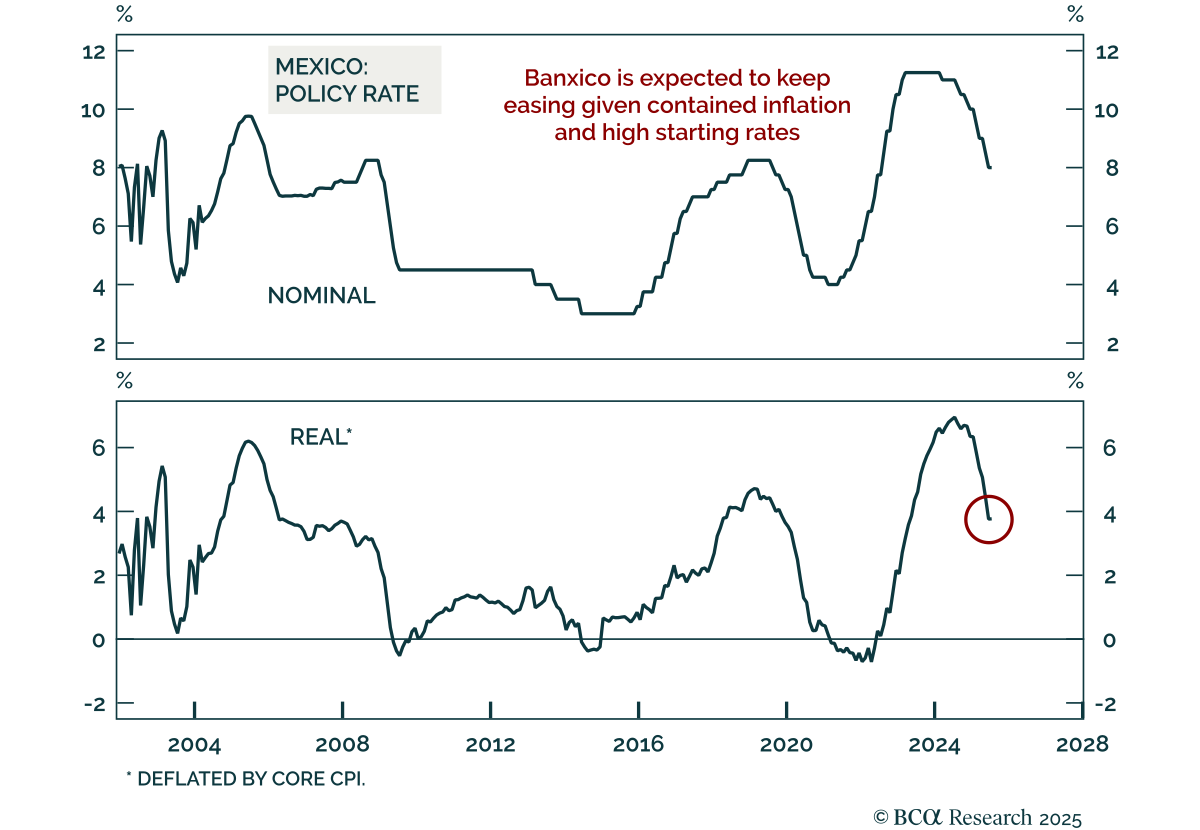

Banxico cut rates to 7.5%, reinforcing our call to go long Mexican local bonds and overweight Mexico across EM portfolios. Inflation is within target, giving policymakers space to ease. Sound fiscal management and strong external accounts continue to support…

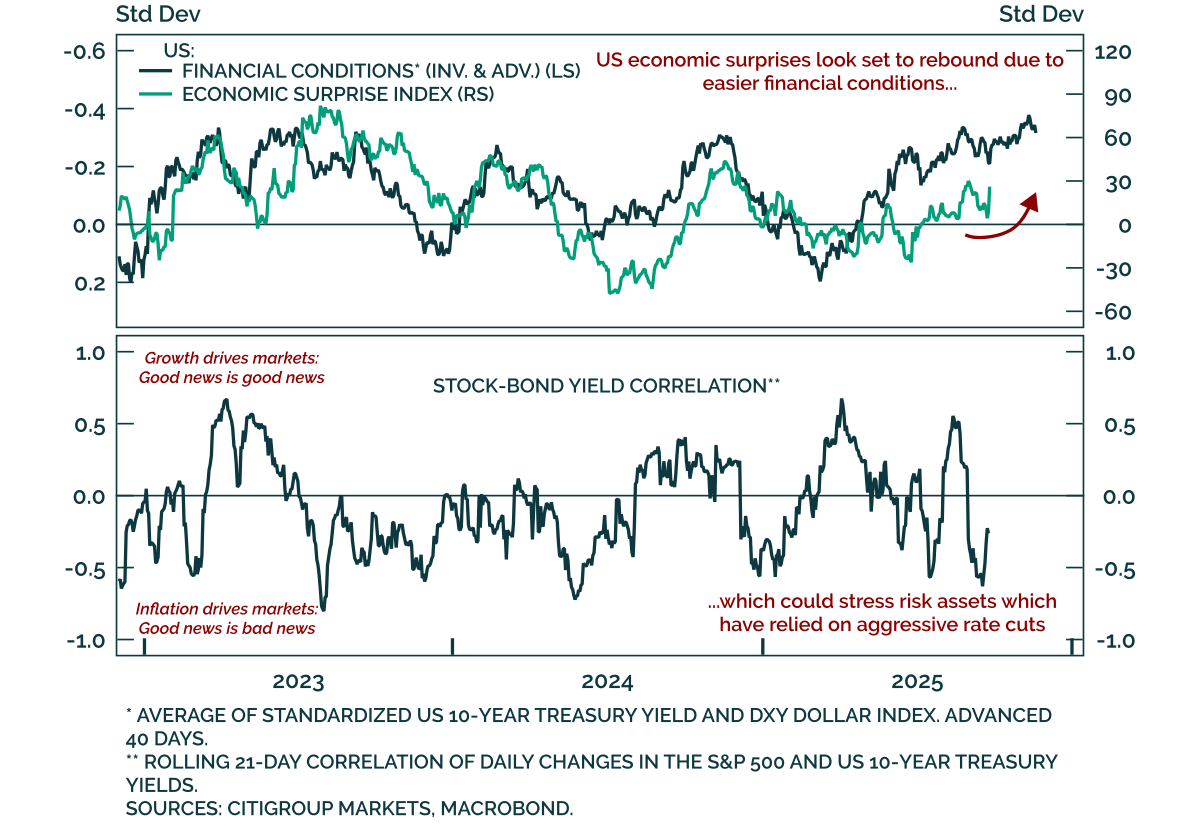

Our tactical framework, which tracks the reflexive loop between financial conditions and economic surprises, points to stronger near-term growth, leaving equities vulnerable if inflation re-accelerates. Data surprises move markets, while bond yields and the…

Australian inflation surprised higher in August, validating the RBA’s cautious stance and supporting an underweight on ACGBs. Headline CPI rose to 3.0% y/y from 2.8%, the highest in a year and at the top of the RBA’s 2-3% target range. While the central bank…

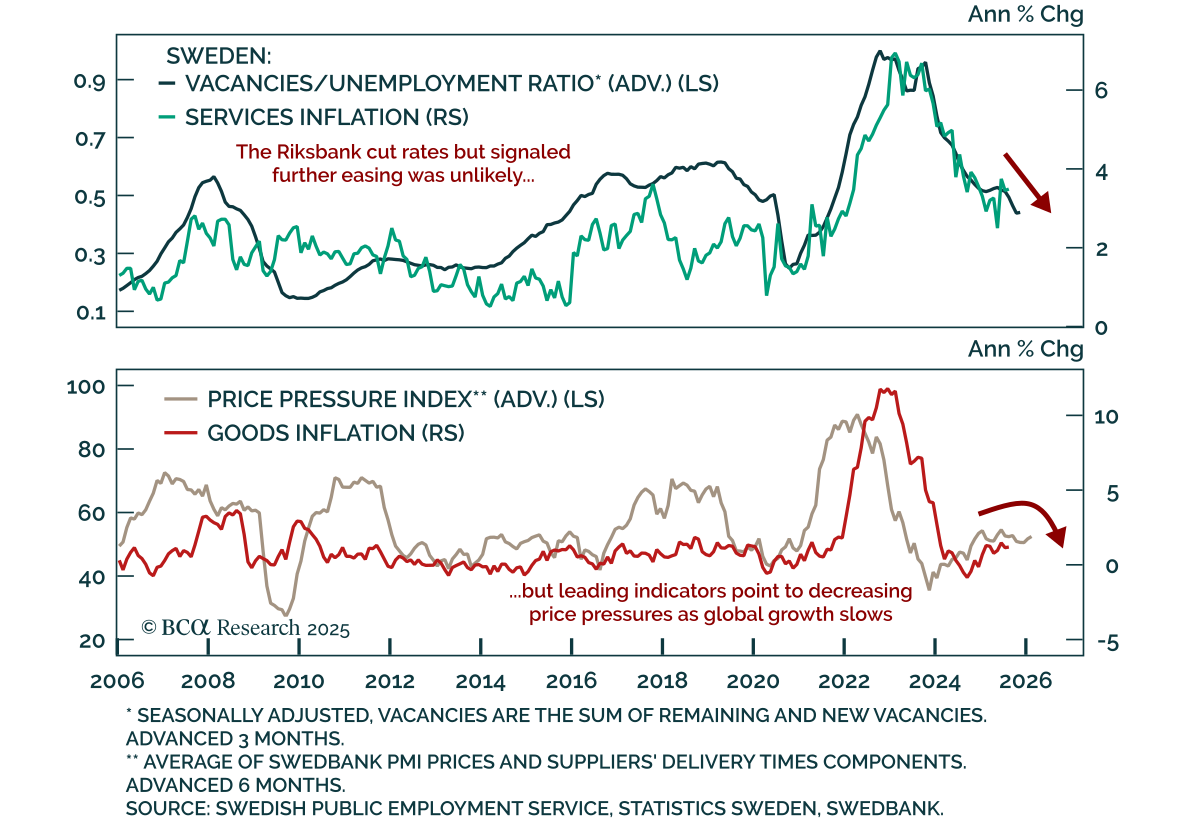

The Riksbank surprised with a 25 bps cut to 1.75%, signaling no further easing for now but keeping the door open to additional cuts as growth weakens. The move came despite recent inflation prints above the central bank’s forecasts. Leading indicators,…

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.