Monetary

The DXY hit a 2024 low on Wednesday. The decline which totaled nearly 5% from its April highs, gathered pace this month (a 3% decline in August) when labor market worries spooked markets. The Fed had already telegraphed it was getting closer to cutting…

Canadian headline CPI decelerated from 2.7% y/y to 2.5% in July, the slowest pace in over 3 years. Notably, core median and trimmed-mean CPI eased further than expected, to 2.4% and 2.7% y/y respectively, 0.1 ppt below anticipations. Lower prices for…

In a widely expected move, the Riksbank lowered its policy rate from 3.75% to 3.5% in August. It had kept rates on hold in June, after having led many other major DM central banks in easing policy in May. The Riksbank also signaled it could cut as many as…

According to BCA Research’s US Investment Strategy and US Bond Strategy services, the drivers of the structural downtrend in real interest rates include: demographic trends (declining fertility rates, longer life expectancy and a rising dependency…

Housing starts and permits both disappointed in July. New construction contracted 6.8% m/m, from a 1.1% expansion in June. Permits, which typically lead housing starts, declined 4.0% m/m in July from 3.9% growth in the previous month. Concurrently, the NAHB…

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

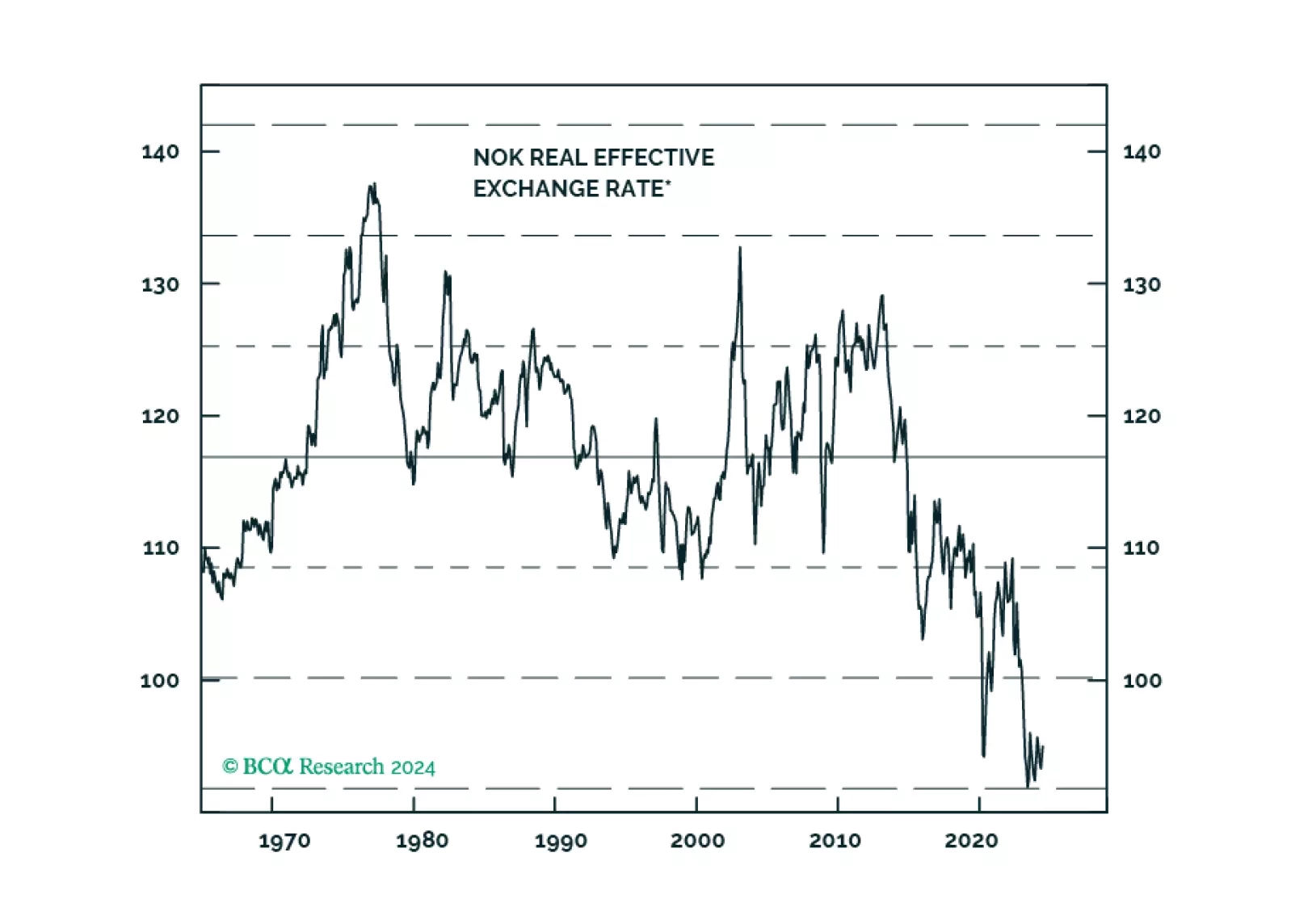

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

US industrial production fell by a larger-than-expected 0.6% m/m in July, the largest monthly decline so far this year. Capacity utilization also decreased a full percentage point to 77.8% Although Hurricane Beryl distorted these nationwide July numbers,…

Headline and core CPI eased for the fourth consecutive month in July, ticking down 0.1 ppt to 2.9% and 3.2% y/y, respectively. The 3-month and 6-month moving averages continued to edge lower as a result, with the former now reaching a three-and-half-year low…

The Reserve Bank of New Zealand unexpectedly embarked on an easing pivot in August, cutting the Official Cash Rate by 25 bps to 5.25%. The central bank also signaled further rate cuts by lowering its rate benchmark forecast to 4.92% by December 2024 and 3.85%…