Monetary

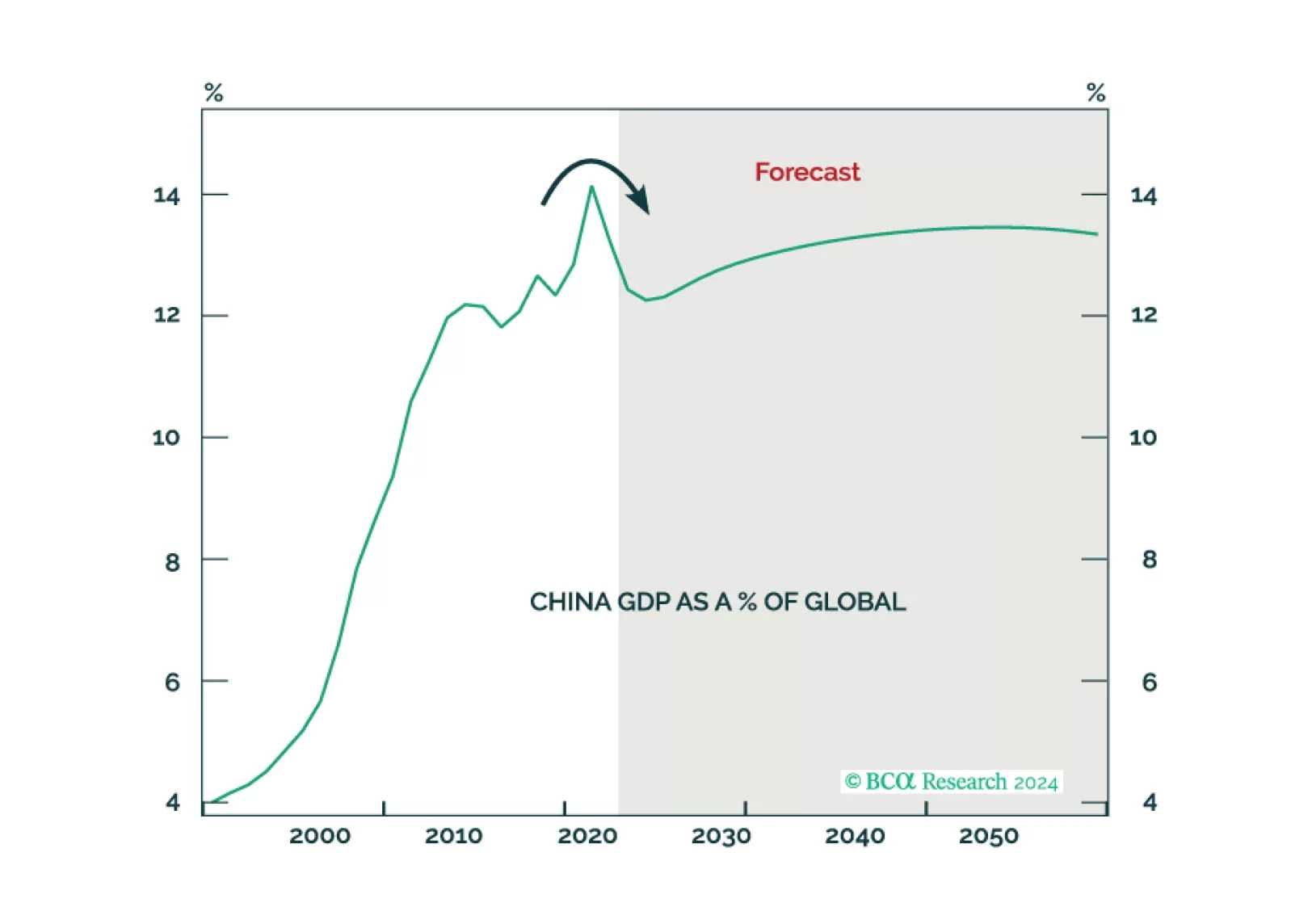

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

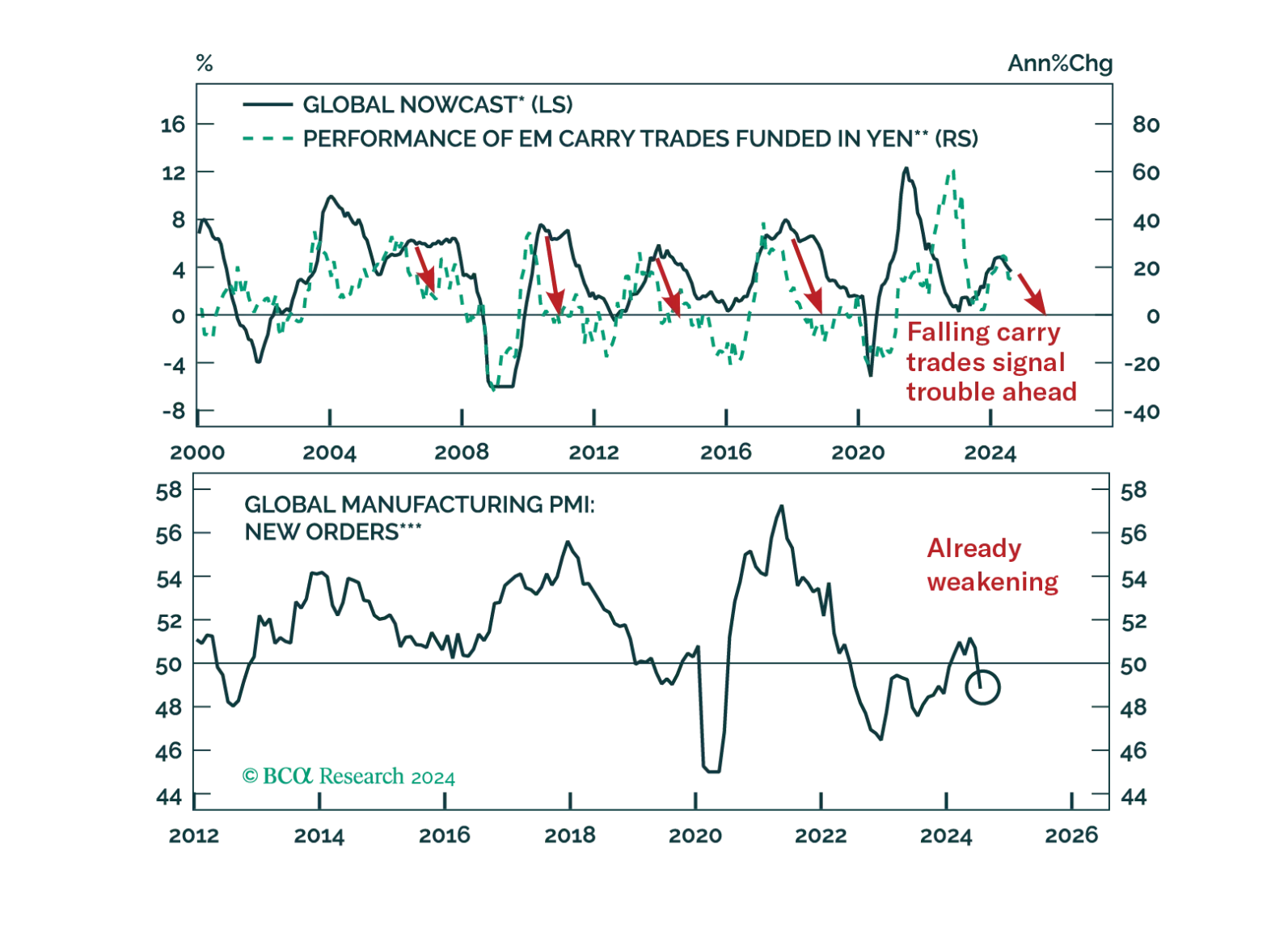

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?

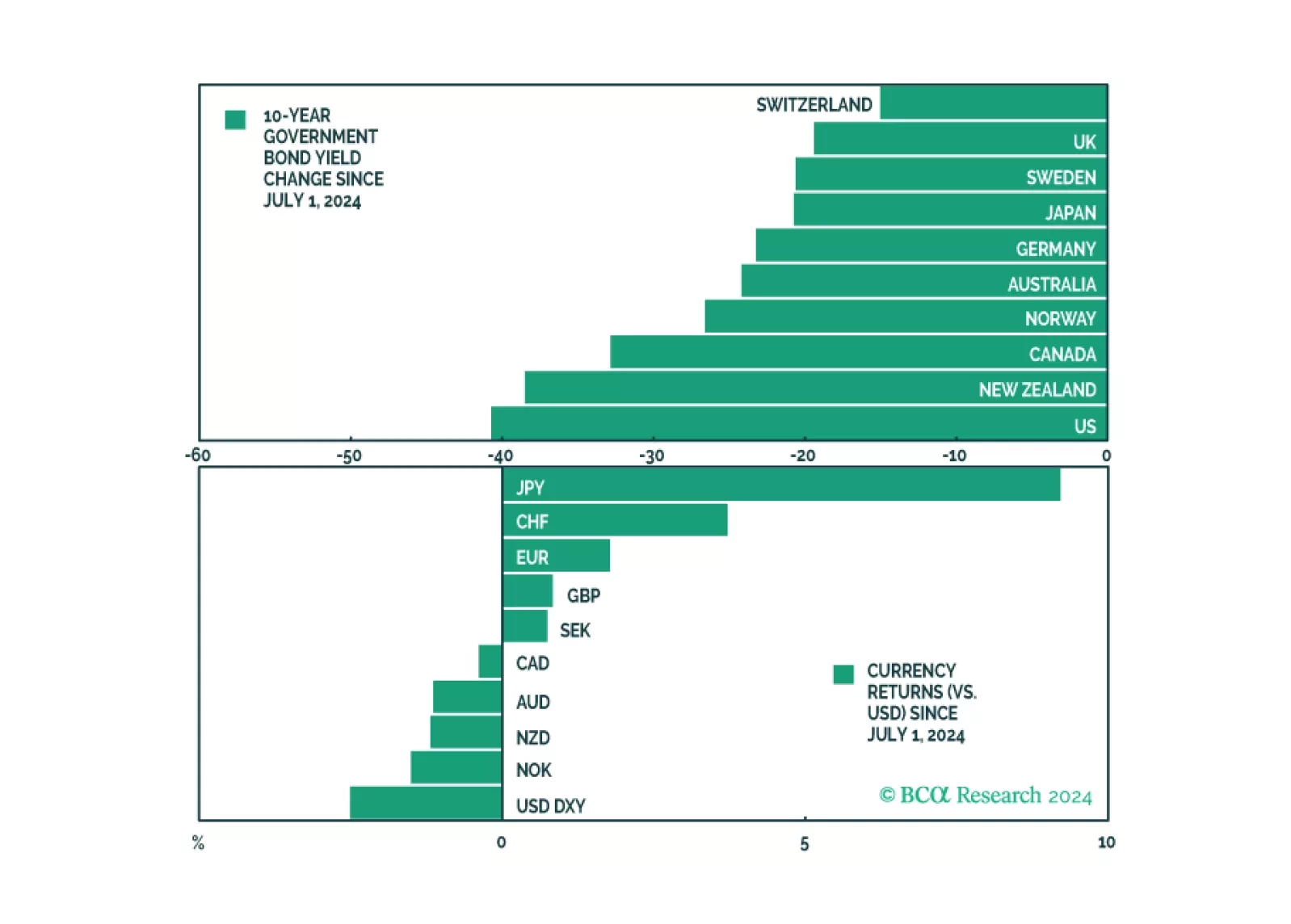

In this monthly review, we give our take on where bond yields and the dollar are headed. This is within the lens of revisiting our fundamental indicators.

Over the past few weeks, global equities have been hit by rising scepticism over the bullish AI narrative and increasing concerns over global growth. Stocks should stabilize in the near term, but the medium-term direction is to the downside. We expect the S&P 500 to drop to 3750 in 2025 and the 10-year Treasury yield to fall to 3%.