Monetary

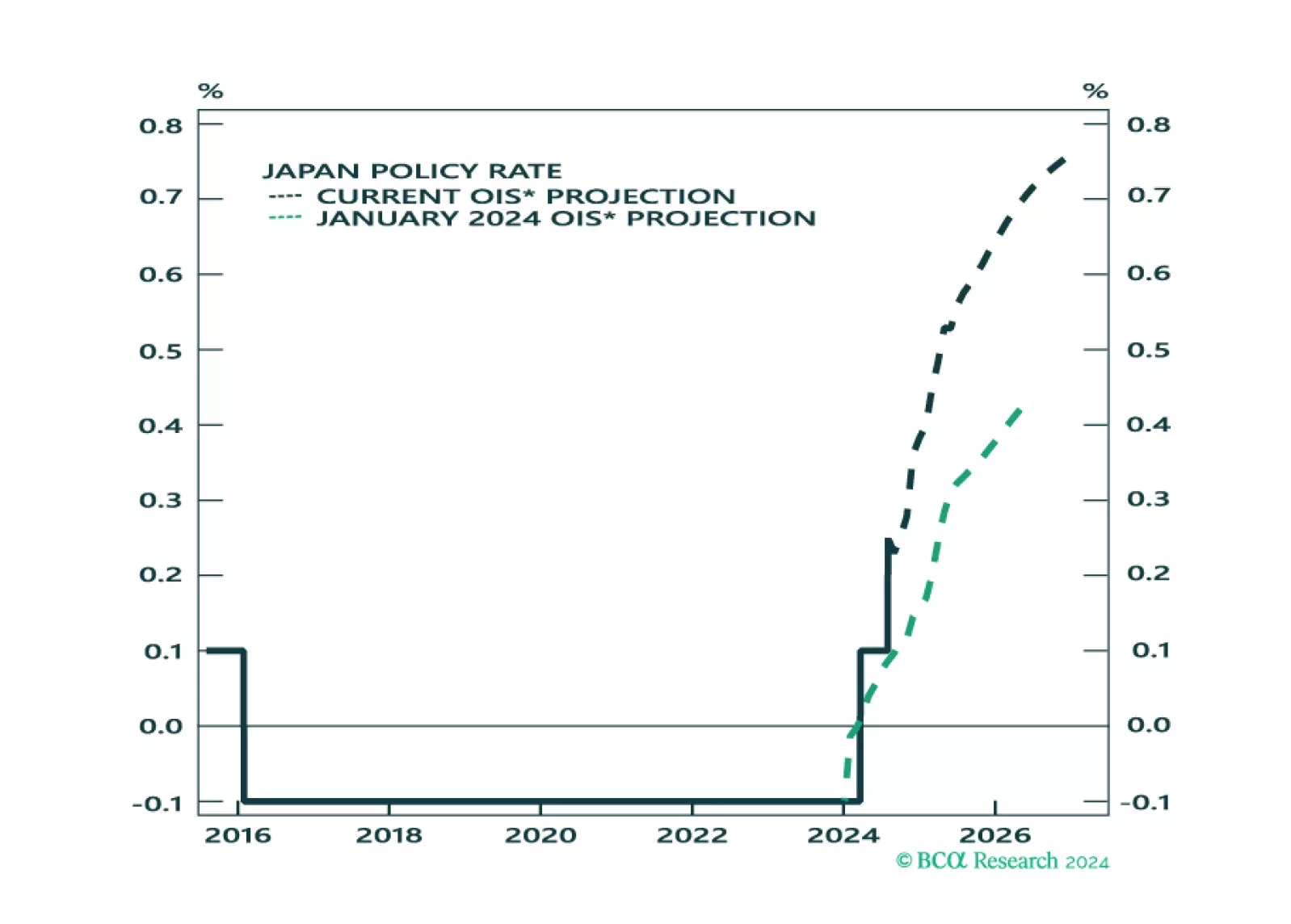

The BoJ delivered a surprise rate hike last week, then proceeded to sending a more dovish signal on Wednesday. Deputy Governor Shinichi Uchida strongly hinted at a central bank that would refrain from hiking further in times of market instability. The yen,…

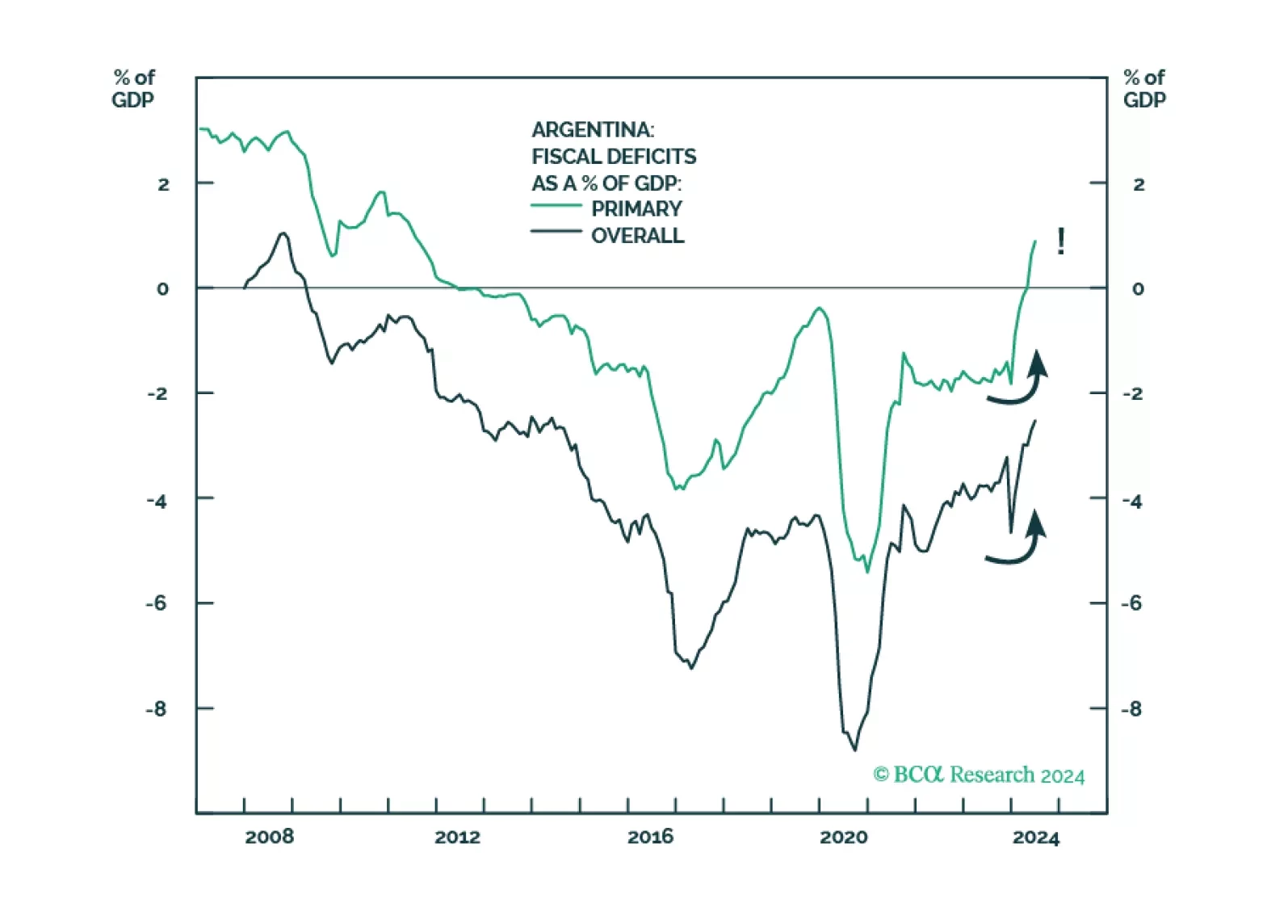

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

Our Portfolio Allocation Summary for August 2024.

The Australian CPI release for Q2 came in broadly within expectations. Headline CPI reaccelerated to 3.8%y/y from 3.6%y/y the previous quarter. Some of the narrower measures of inflation — trimmed-mean and weighted median CPI — came in below market…

July nonfarm payrolls expanded by 114 thousand workers, a sharp slowdown from June’s downwardly revised 179 thousand, and significantly disappointing expectations of 175 thousand. The unemployment rate unexpectedly edged 0.2ppt higher to 4.3% in July,…

The Bank of England (BoE) lowered its policy rate by 25 basis points to 5% at its meeting on Thursday. While the move was expected, the governing board was split, voting 5 – 4 in favor of reducing the key interest rate. The BoE cut its policy rate despite…

According to BCA Research’s Global Asset Allocation service, there are clear signs that growth is weakening. BCA’s Global Nowcast has been slowing for three months. Behind this slowdown is the fact that the US consumer – the biggest factor keeping growth…

We assess the investment implications of the BoJ and Fed meetings, and give our take on the next policy moves. We also assess the impact on asset markets.

Eurozone headline CPI inflation unexpectedly accelerated in July, from 2.5% y/y to 2.6%. Core CPI remained stable at 2.9% despite expectations it would ease. EU Harmonized CPI accelerated in the regions’ three largest economies, surprising by a large margin…

FOMC members unanimously voted in favor of keeping rates on hold in July but signaled that a September cut is on the table. Inflationary pressures have indeed continued to ease over the past several months. Notably, the Employment Cost Index (ECI) – the…