Monetary

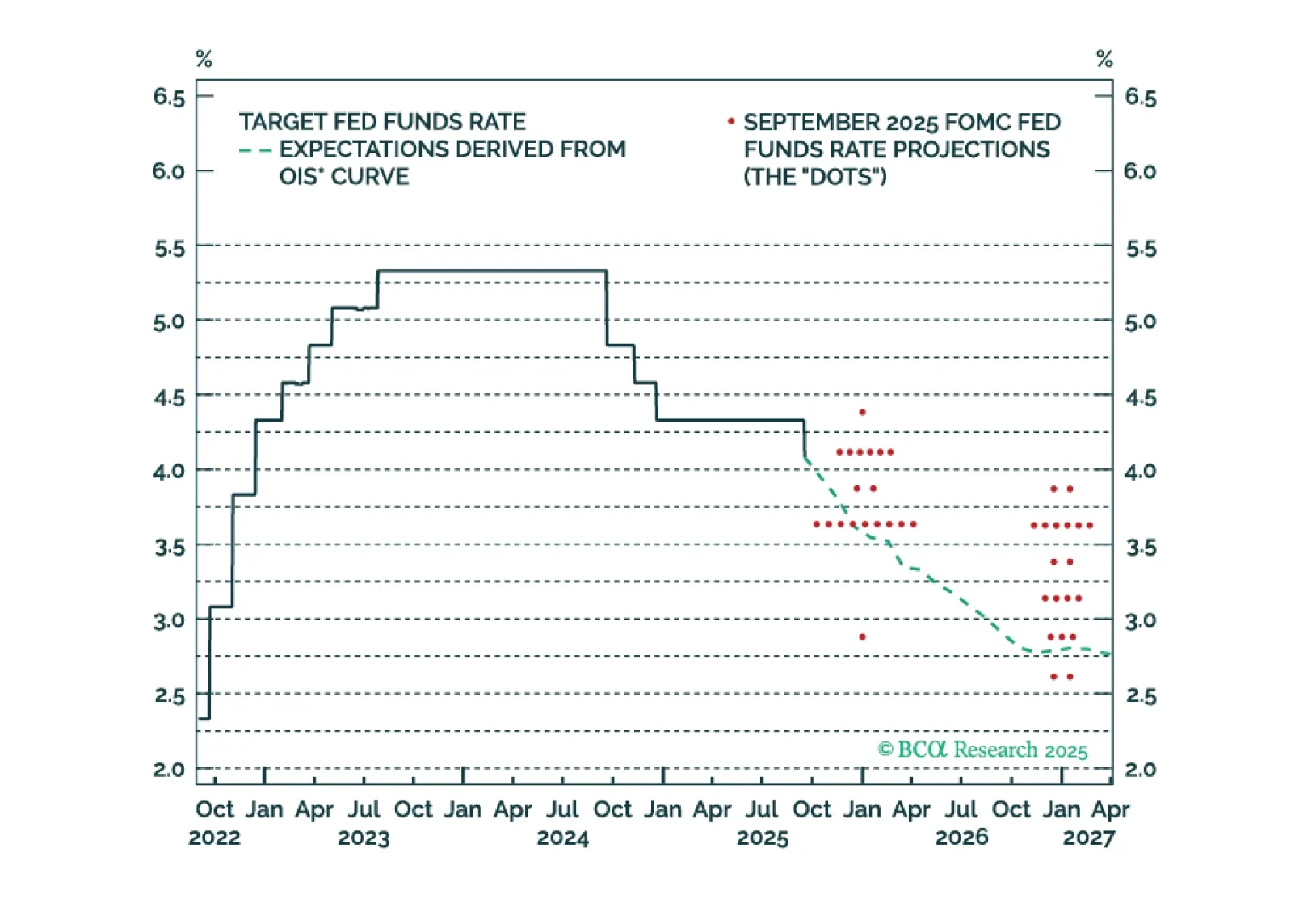

Post-FOMC speeches reveal divisions across the committee, reinforcing long duration as policy remains mildly restrictive. The September dots showed a split, with half of participants expecting at most one 25 bps cut and the rest seeing at least two. Gov.…

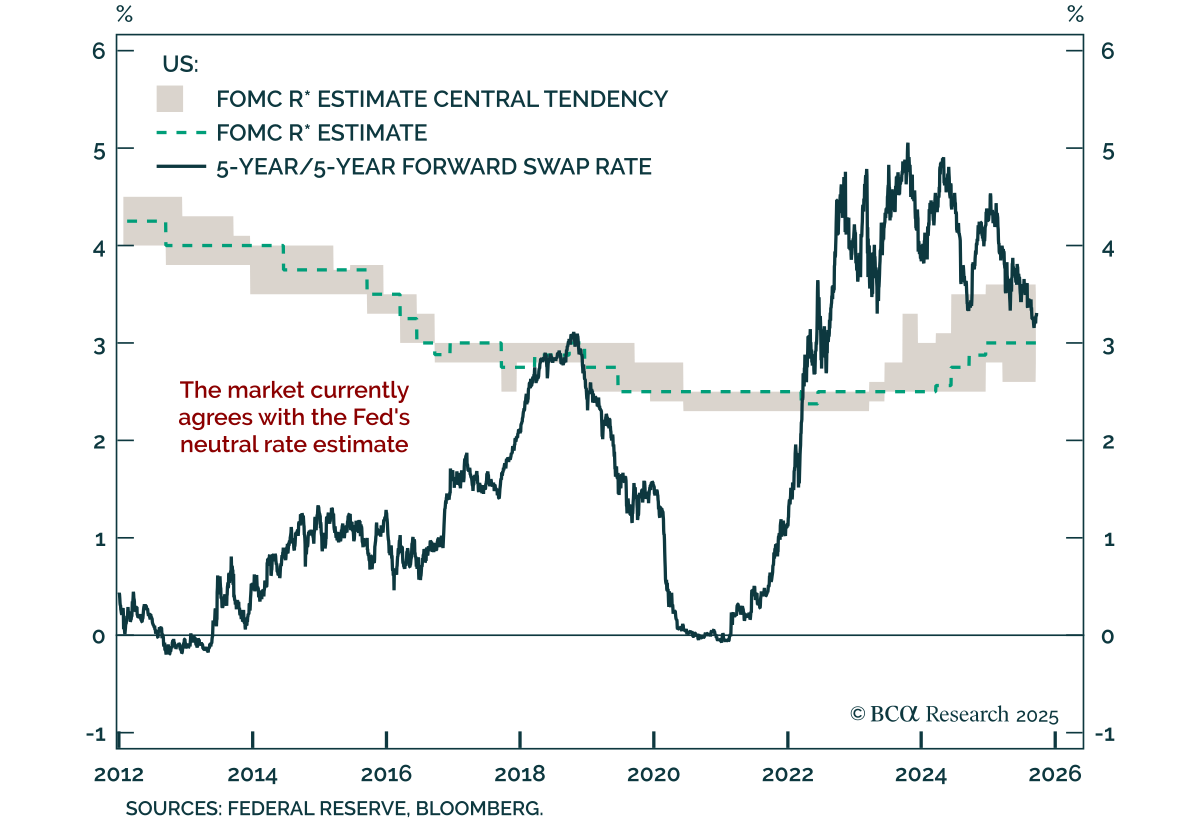

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

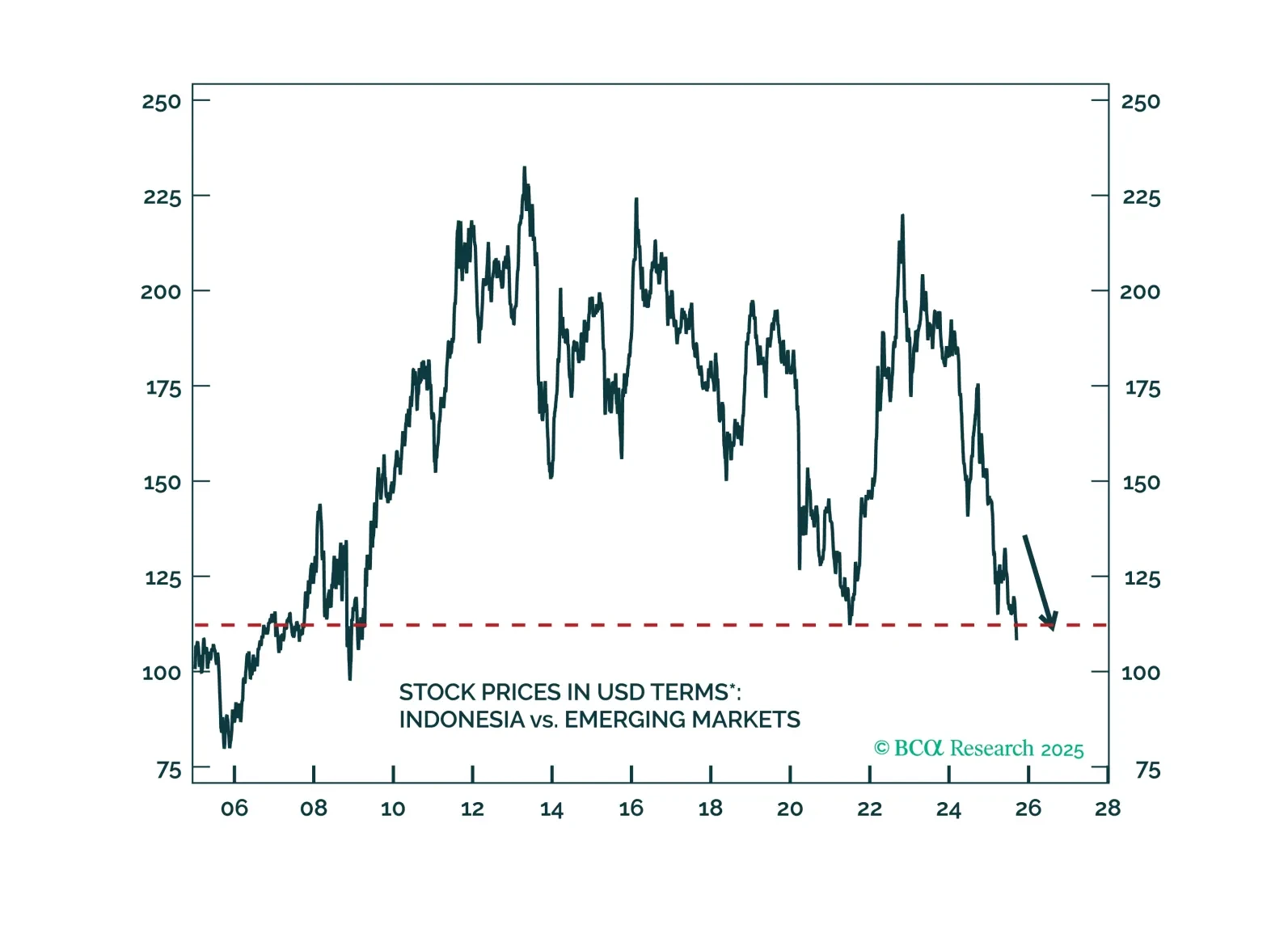

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

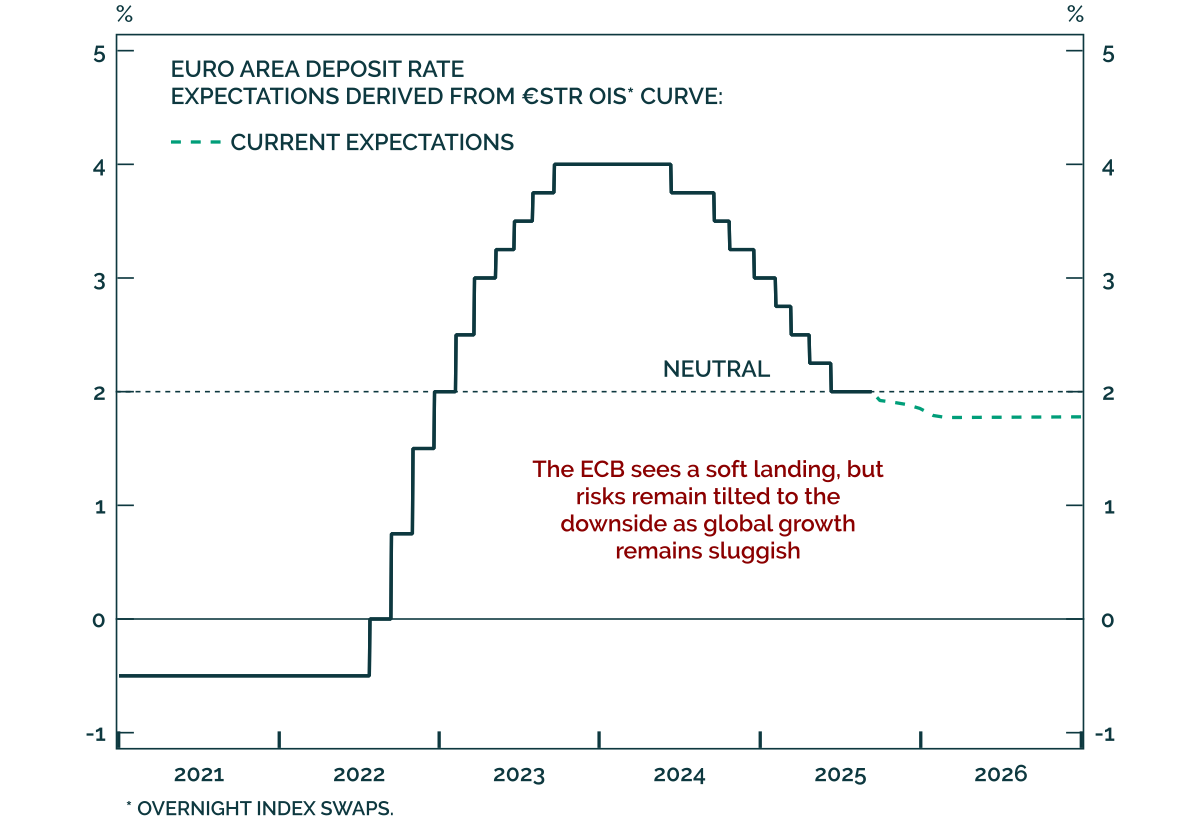

The ECB left policy unchanged in September, reiterating a data-dependent stance and signaling no urgency to ease. Markets barely reacted, consistent with a fully discounted decision. The Governing Council appears confident in a soft landing, making a December…

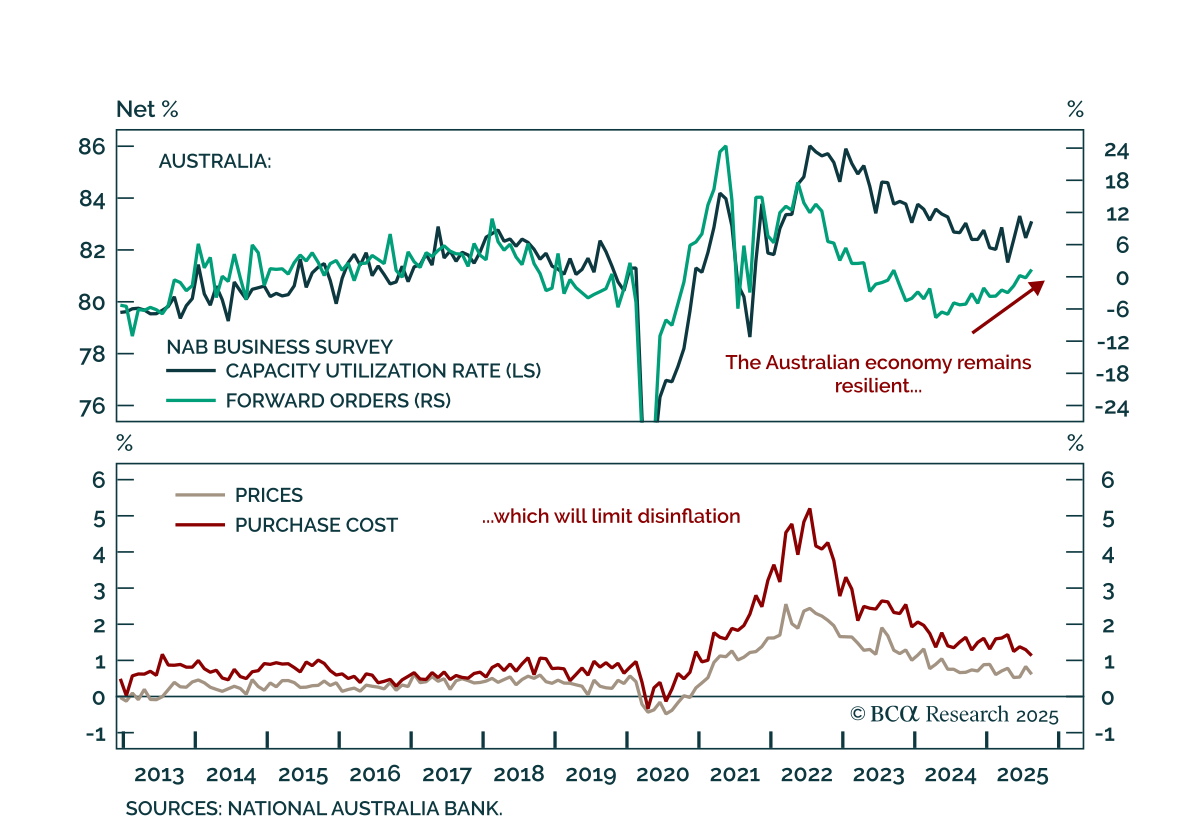

Australia’s NAB survey shows underlying resilience, reinforcing our underweight on ACGBs and the case for AUD flatteners vs. CAD steepeners. The August survey was mixed, with current conditions improving to 7 from 5, while business confidence softened to 4…

Japan’s Eco Watchers Survey points to stabilization; JGBs remain unattractive and the yen’s near-term setup is less favorable versus USD. The August survey modestly beat expectations, with the current component rising to 46.7 from 45.2 and expectations…

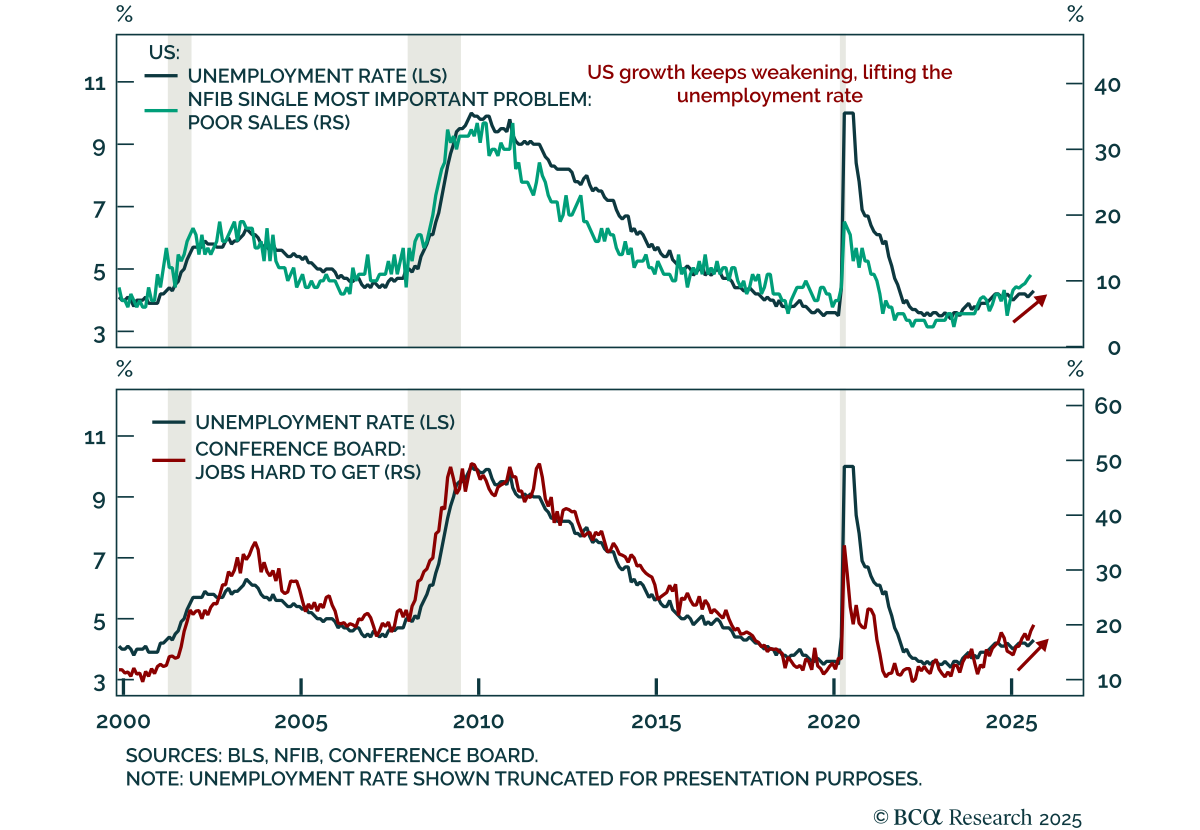

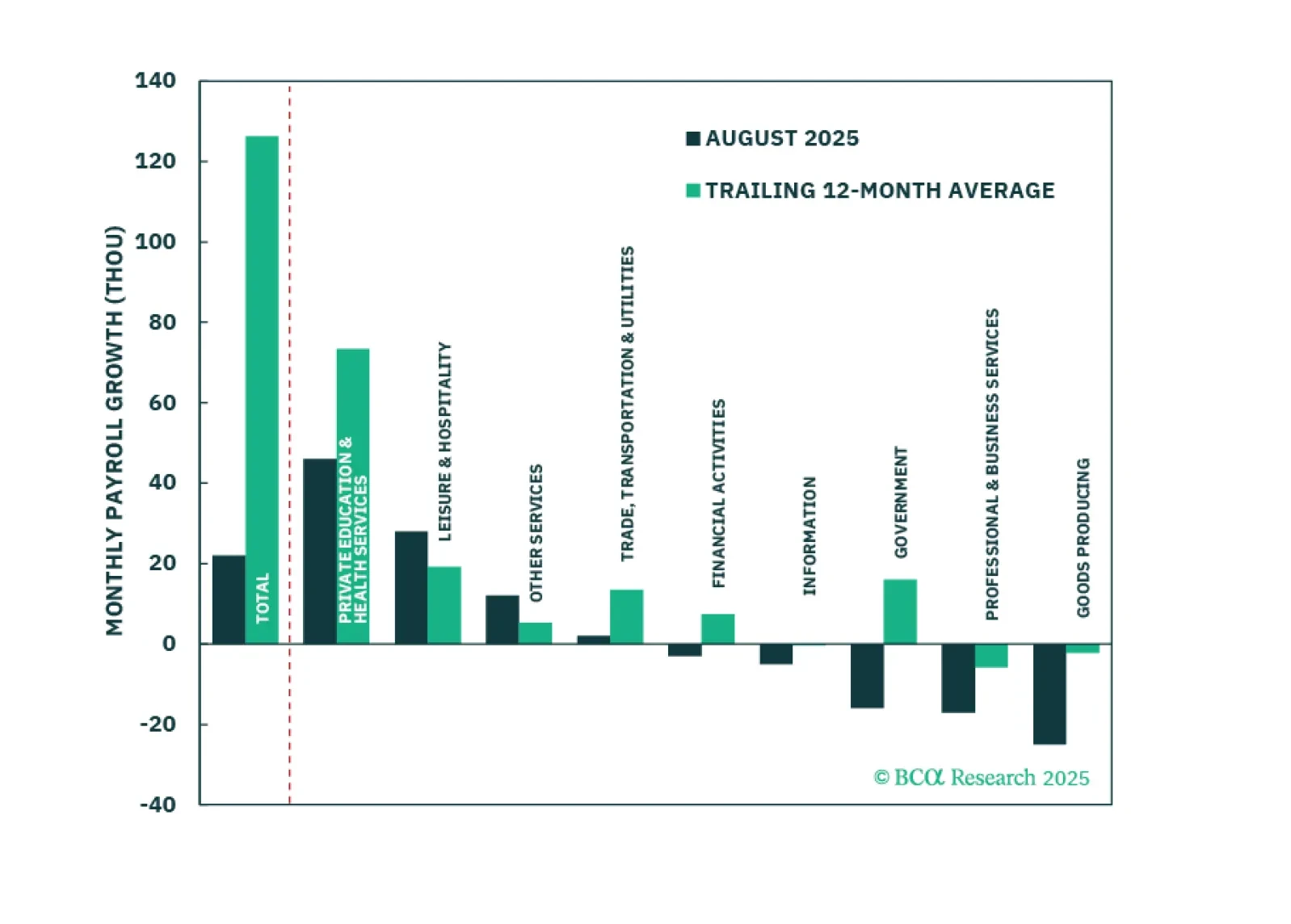

The August US employment report confirmed a significant labor market deceleration, keeping us modestly defensive. Nonfarm payrolls rose just 22k after 79k in July, while net revisions subtracted 21k from prior months. The 3-month average slowed to 29k,…

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

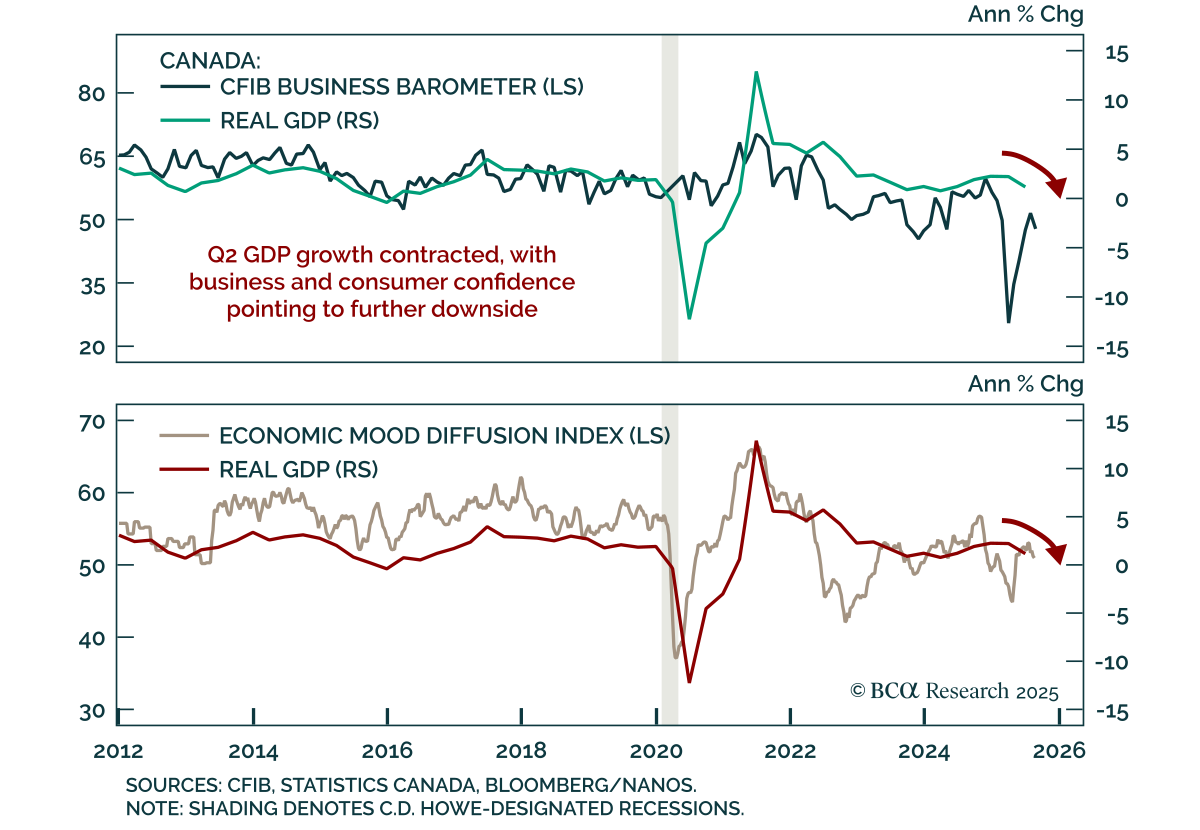

Canada’s Q2 GDP contraction underscores a fragile backdrop where growth risks will outweigh inflation, supporting further BoC easing. Real GDP contracted at an annualized 1.6% after expanding 2.2% in Q1, consistent with survey data showing weaker confidence…

Euro area August flash HICP was slightly hotter than expected, reinforcing the case for the ECB to stay put in September. Headline inflation rose to 2.1% y/y from 2.0%, with the monthly print surprising at 0.2% m/m. Core inflation held at 2.3% y/y despite…