Monetary

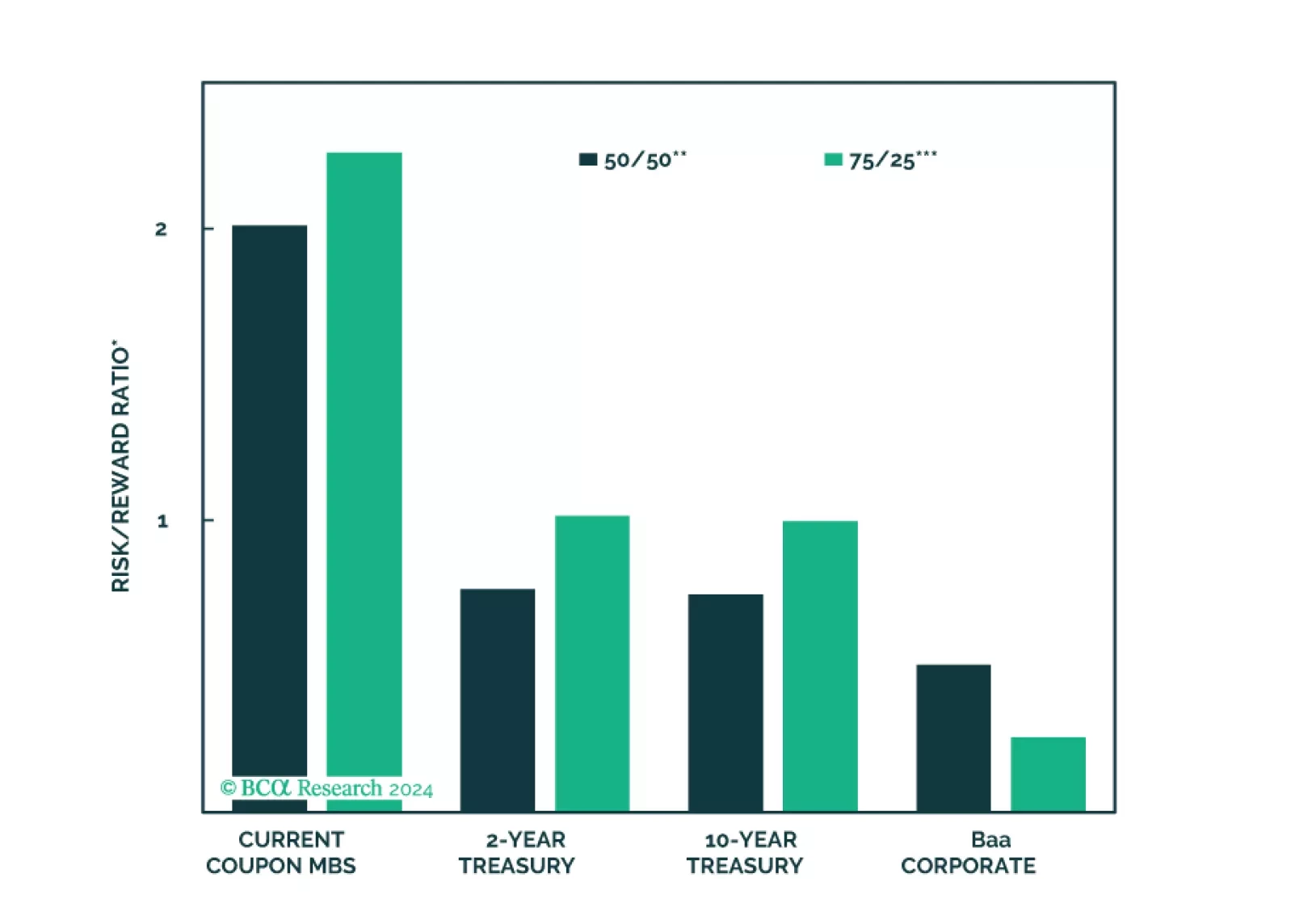

We consider the relative merits of four different fixed income investments in the current economic environment: 2-year Treasuries, 10-year Treasuries, Baa-rated corporate bonds and current coupon Agency MBS.

On the surface, UK inflation appears to be on the right track. The May CPI release came in broadly within expectations. Headline inflation eased from 2.3%y/y to 2.0%y/y – directly on the BoE’s target for the first time since July 2021. Core CPI (excluding…

The ECB delivered its first rate cut in June, moderating the degree of restriction rather than pivoting outright to easy monetary policy settings. Indeed, the rate cut was accompanied by an upward revision of inflation and growth forecasts. Since then,…

The Reserve Bank of Australia kept its cash rate at 4.35% at its policy meeting on Tuesday, in line with market expectations. Australia’s monthly measure of headline inflation came in at 3.6% in April, still considerably above the midpoint of the RBA’s 2-3%…

According to BCA Research’s Commodity & Energy Strategy service, a Fed pivot to rate cuts will provide gold prices with a tailwind. At first blush, the historical evidence is mixed. While gold rallied in the three months leading up to the start of…

Housing is the most interest-rate-sensitive sector of the economy. Yet, the very aggressive monetary tightening cycle has only had a muted effect on home prices. While recent housing market data have been mixed, prices have not tumbled. Indeed, a tight…

According to BCA Research’s Geopolitical Strategy service, the South African election presents a window of opportunity for productivity-boosting structural reforms, such as privatization, to coincide with monetary and fiscal easing necessary to fend off…

In this insight, we update our thinking on the recent BoJ move in terms of positioning for the yen and JGB yields.

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

The BoE had to deal with a stagflationary headache in the second half of 2023. Inflation was stickier and growth was weaker in the UK than in many of its DM peers. This trend turned around earlier this year with a late-cycle growth reacceleration. The UK…