Monetary

We comment on whether Treasury market valuation is sufficiently attractive to get long bonds and consider some of the common arguments for why yields may yet make new highs.

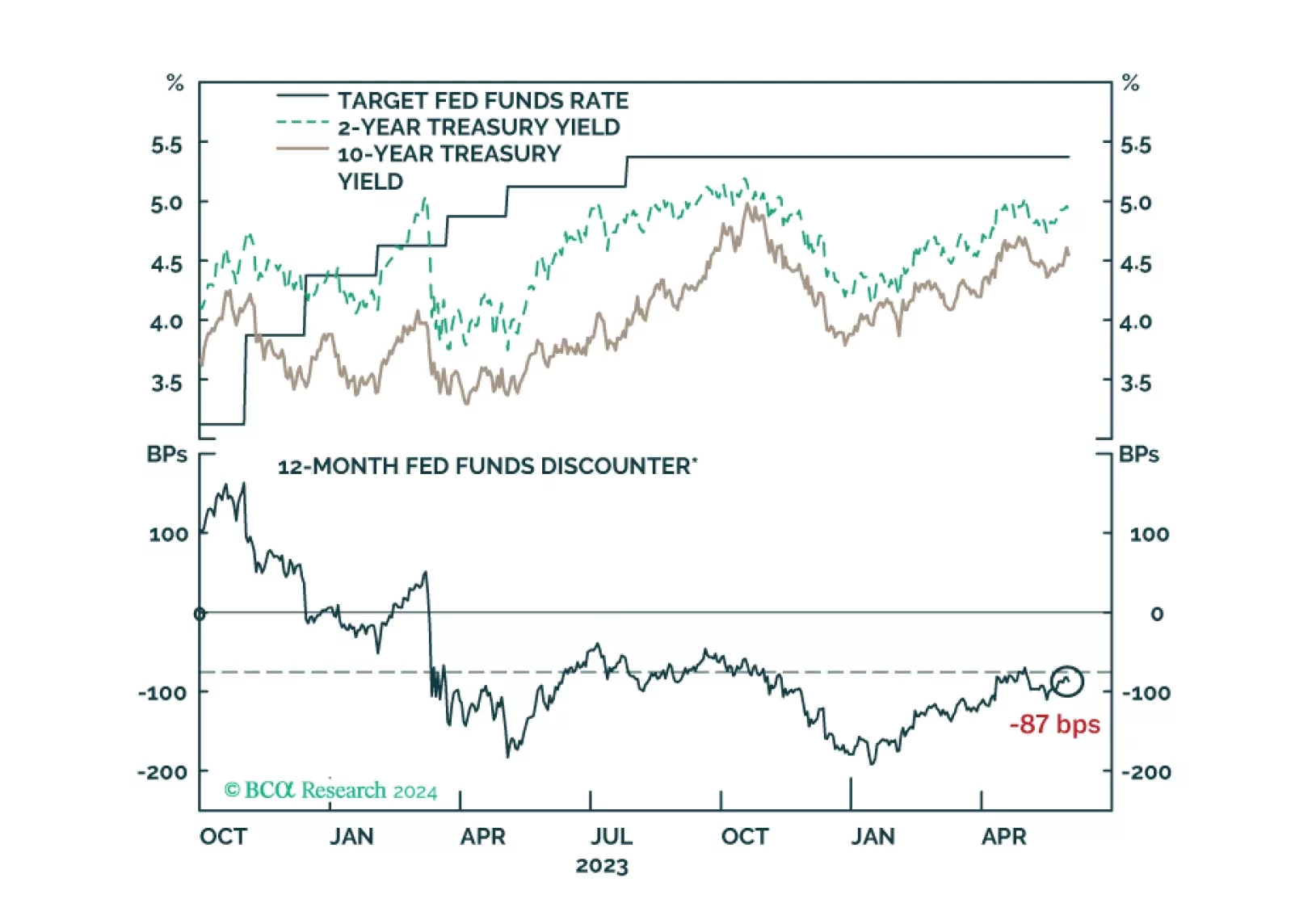

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

The signs of an approaching recession are starting to emerge. We will turn tactically defensive once they all fall into place.

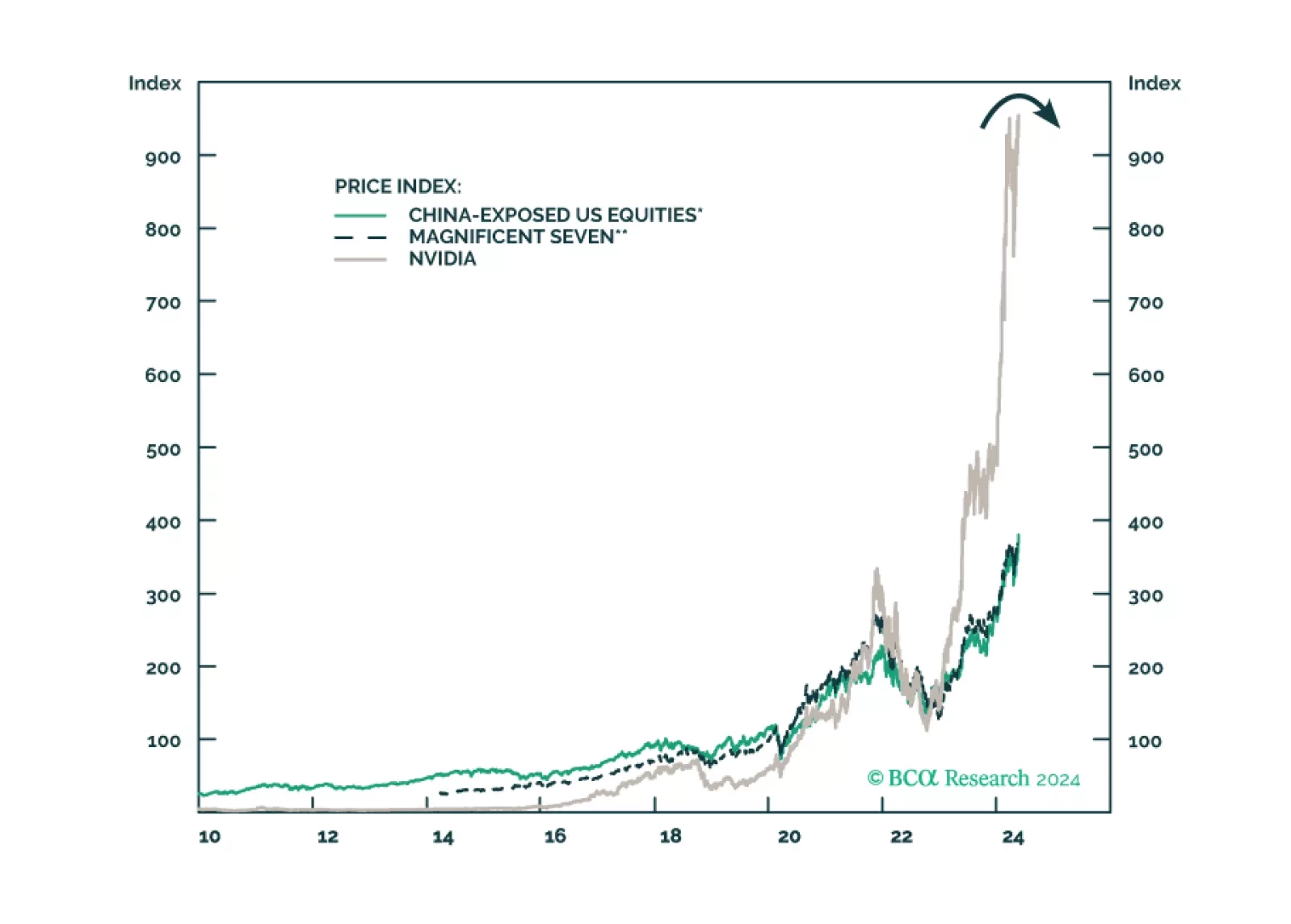

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

In this Insight, we revisit our "higher for longer" theme for the Reserve Bank of New Zealand, in light of the latest central bank meeting. In conclusion, we are inching towards a more dovish RBNZ ahead. Ergo, we recommend some fixed income and currency trades.