Monetary

It is too early for the RBA to begin cutting rates. Inflation remains above target, with core CPI currently standing at 3.4%, one of the highest numbers amongst major economies. The labor market is also fundamentally strong. Australia’s unemployment rate…

Flash estimates for Euro Area inflation in March surprised to the downside. Headline inflation slowed from 2.6% to 2.4% versus expectations of 2.5% and core inflation eased from 3.1% to 2.9% versus expectations of 3%. While the stickiness of services…

The extraordinary performance of AI companies has pushed US growth stocks to new highs. So far, the MSCI US Growth Index has returned almost 11% since the start of the year, outperforming global stocks by over 3%. No growth index from the rest of the world…

The Dallas Fed released its trimmed mean PCE inflation rate for February on Friday. The trimmed mean PCE is a measure of underlying inflation which excludes the top 31% and the bottom 25% of the PCE basket and then uses a weighted average of the remaining…

Friday’s PCE report showed a resilient US economy. Real personal consumption increased by 0.4% m/m in February, beating expectations of 0.1% m/m and remaining above its pre-pandemic trend. Both services and goods contributed positively. Real personal…

The Bank of Canada released its Business Outlook Survey for the first quarter of this year on Monday. While there are some early signs of stabilization, overall demand continues to be weak. The indicator for future sales growth remains well below its…

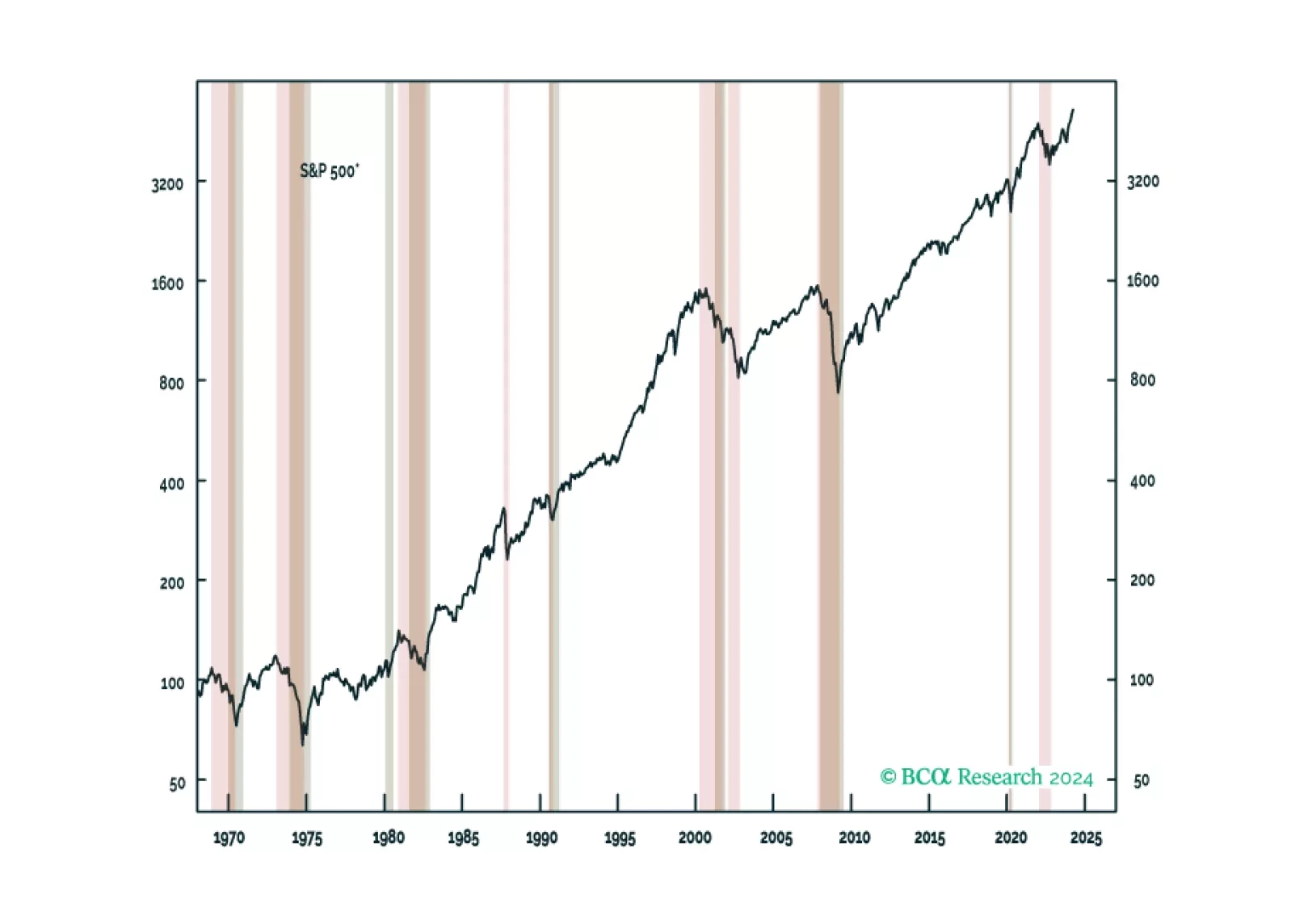

We are not yet ready to downgrade equities on a tactical basis but continue to expect we will eventually do so. We present a checklist of indicators that we are watching to determine when to de-risk.

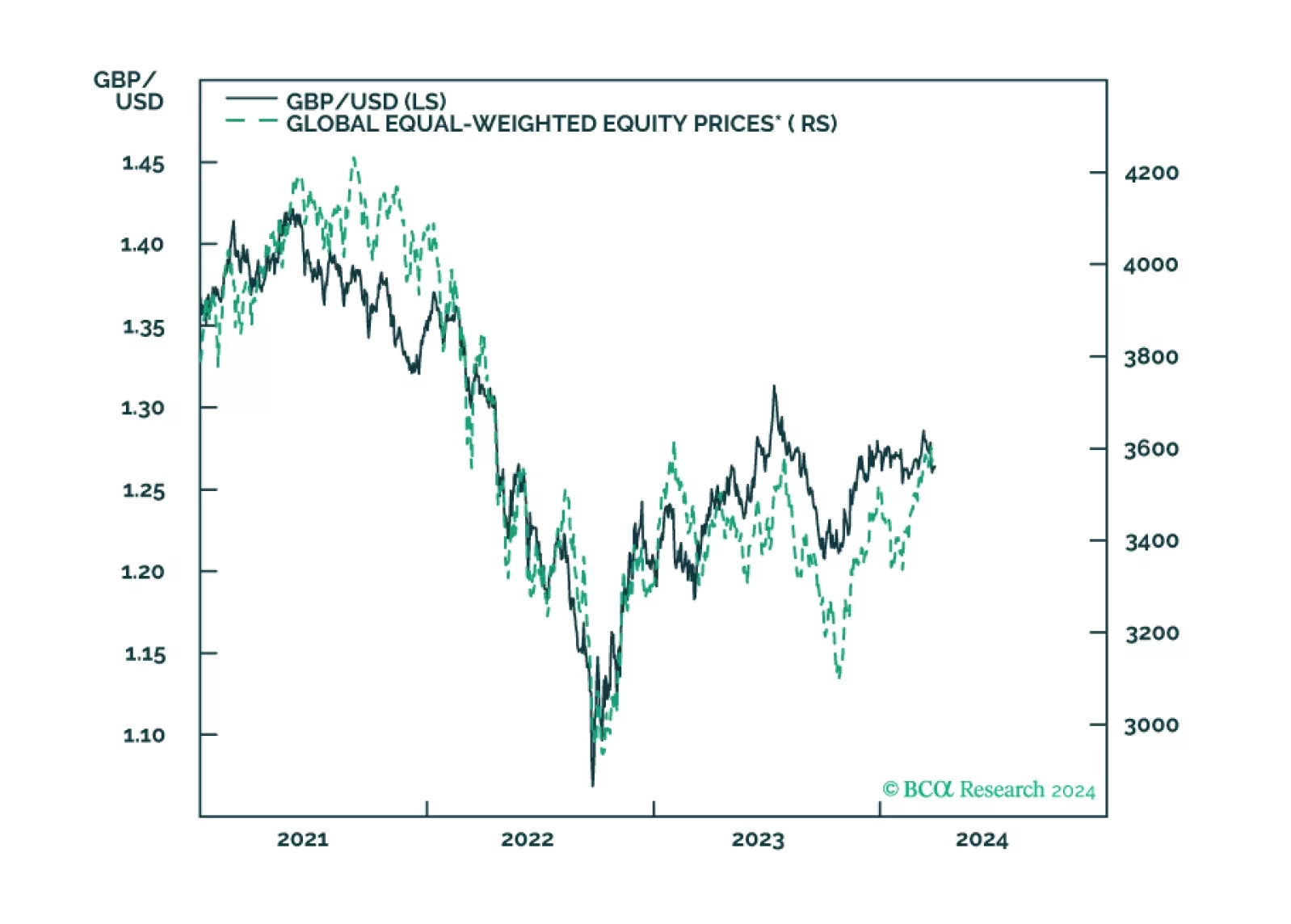

In this Insight, we discuss our rationale for a short sterling position.

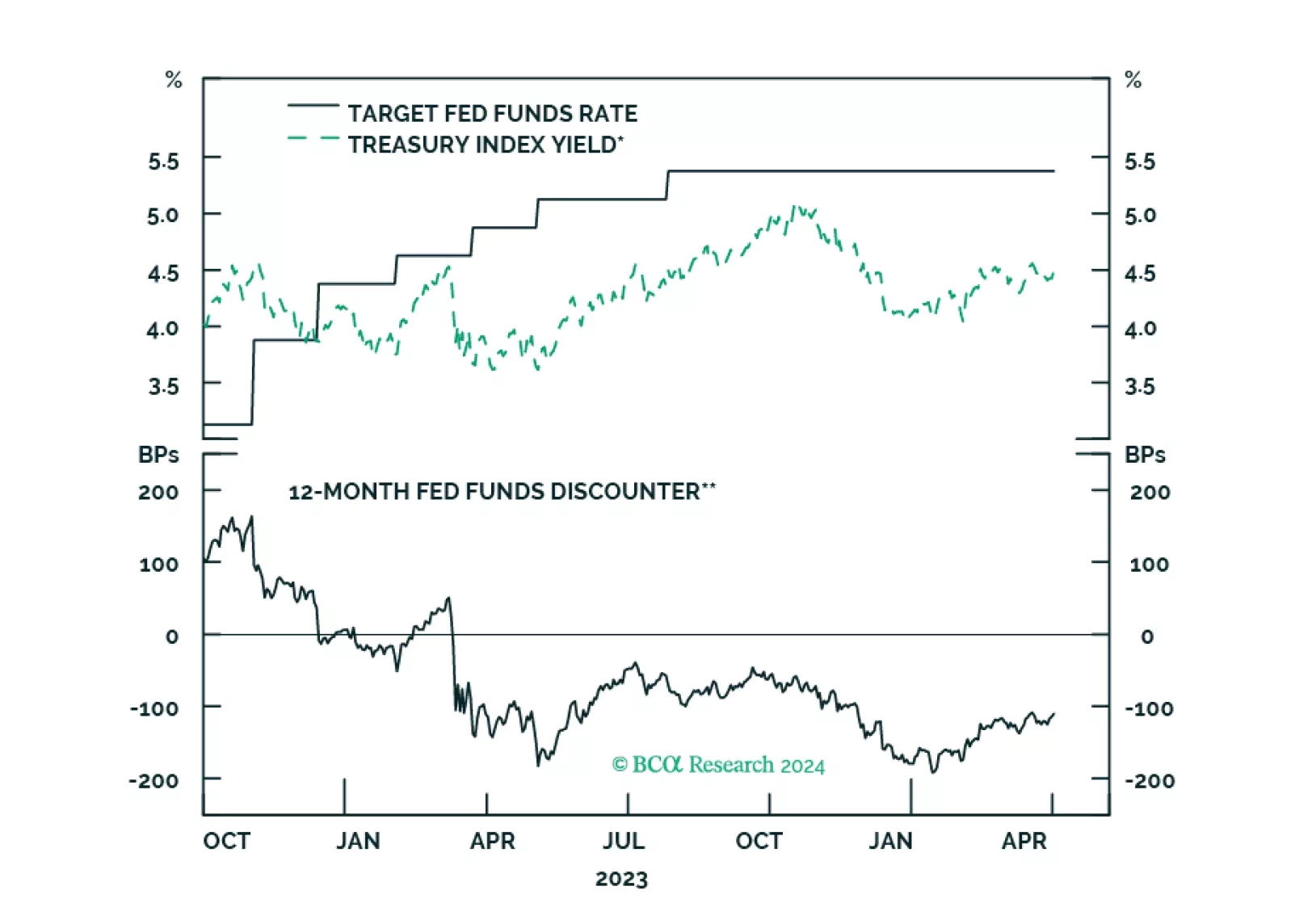

The message from Fed Governor Christopher Waller’s speech on Wednesday could not be clearer: there’s still no rush. While market participants as well as the FOMC are still pricing in three rate cuts this year, the recent hotter-than-anticipated inflation data…