Monetary

After briefly weakening in January, AUD/CAD has once again been moving higher over the past few weeks. Indeed, BCA’s Intermediate Term Technical Indicator is back to neutral from overbought territory, paving the way for this rebound. The question going…

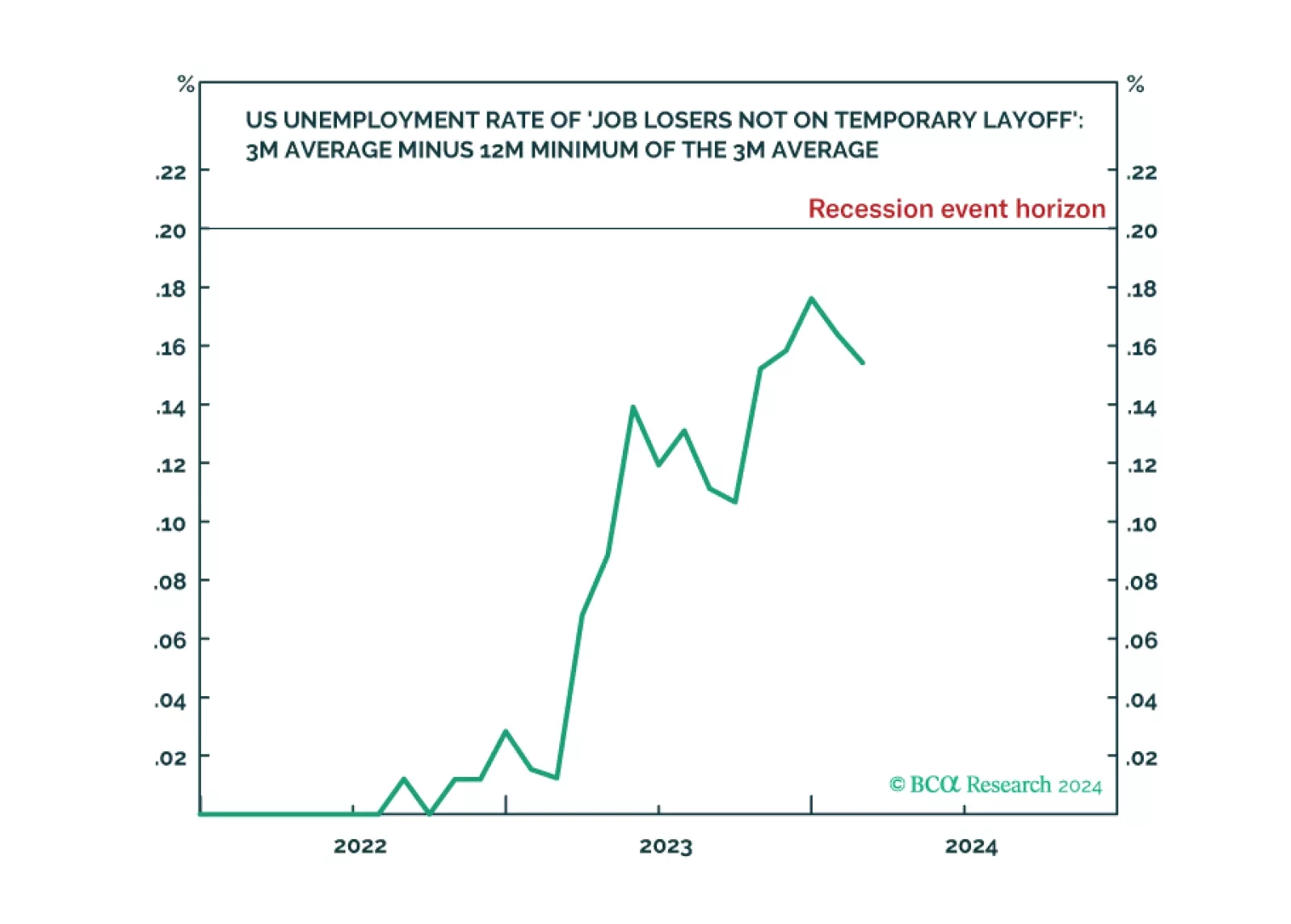

The Joshi rule real-time US recession indicator remains at an elevated 0.154 versus its recession event horizon of 0.200, indicating weakening US labour demand. With the last mile of US disinflation requiring labour demand to ‘catch down’ with labour supply, investors should watch the Joshi rule very closely to pre-empt a potential tipping-point. Plus: tactically long Portugal versus Europe, and wheat versus cotton; and tactically short USD/CLP, Qualcomm (QCOM), and Salesforce (CRM).

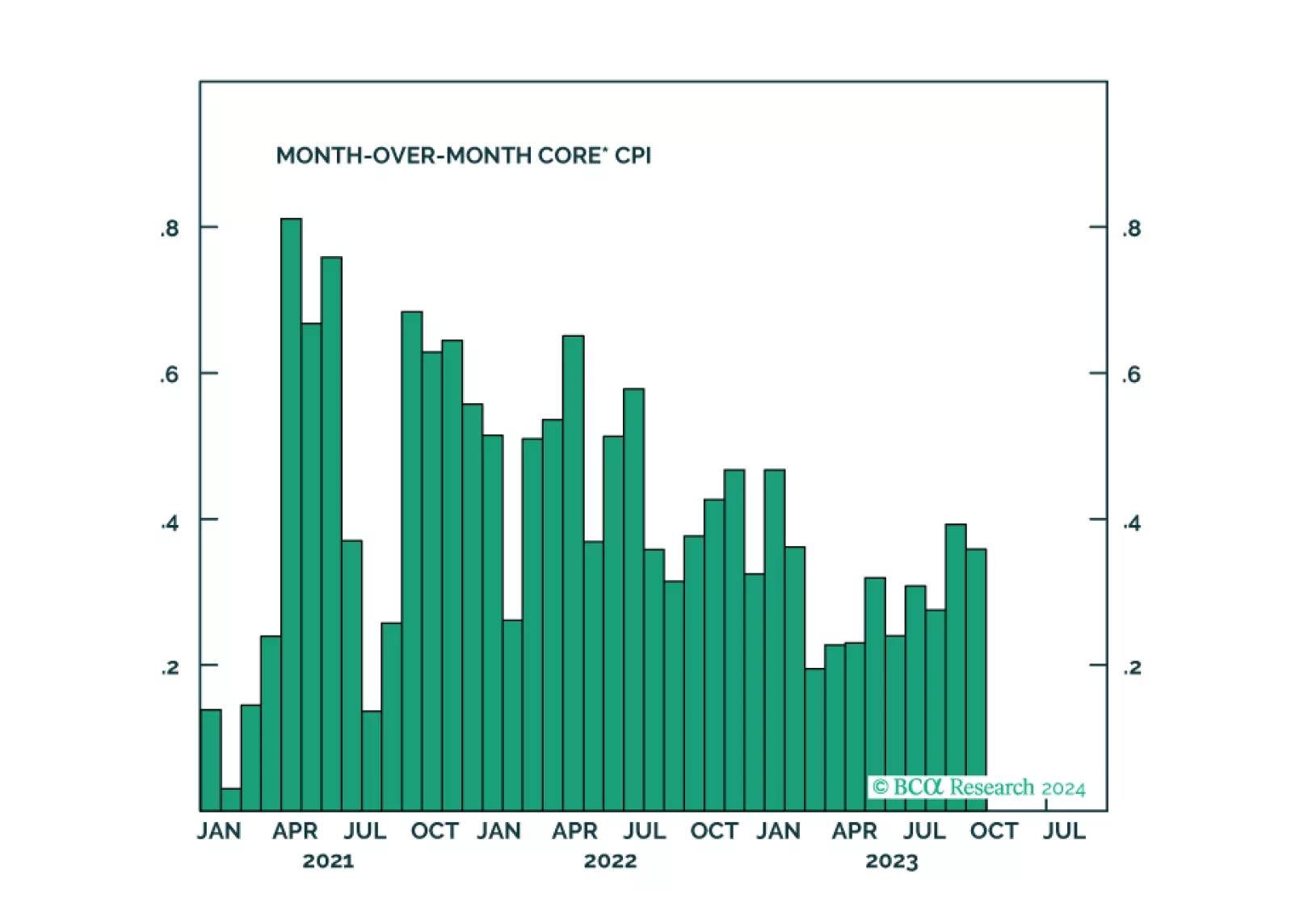

US headline CPI inflation accelerated from 0.3% m/m to 0.4% m/m in February, in line with expectations. A rise in gasoline prices and shelter inflation accounted for 60% of this increase. Meanwhile, the annual rate of change in the headline index unexpectedly…

Although the Atlanta Fed GDPNow estimates for Q1 have been trending lower, the latest 2.5% print (which is down from 3.4% a month ago) still suggests that economic conditions are resilient in the US. Yet small business owners are less optimistic. The results…

The British pound is the best performing G10 currency so far this year, gaining 0.7% vis-à-vis the US dollar. The outperformance of sterling over the past month coincides with an increase in Citigroup’s UK economic surprise index, both on an absolute basis as…

Results of the New York Fed’s Survey of Consumer Expectations showed an uptick in medium- and long-term inflation expectations in February. Specifically, the three-year ahead measure rebounded from a record low of 2.4% to 2.7% and the five-year ahead gauge…

The US employment situation report sent a mixed signal on Friday. While total nonfarm payrolls rose by 275 thousand jobs in February, exceeding the 200 thousand expected, the previous two months’ numbers were revised lower by 167 thousand jobs (see Indicator…

For the past year, relatively large downward revisions have been key features of the monthly US nonfarm payrolls reports. Friday’s release was no exception. Although it showed the magnitude of job gains beat expectations in February, estimates for December…

Japanese equities and government bonds sold off on Monday and the yen strengthened following the release of the revised Q4 GDP report showing the economy expanded by an annualized 0.4% q/q in Q4 2023 versus earlier estimates of a 0.4% contraction. A…