Monetary

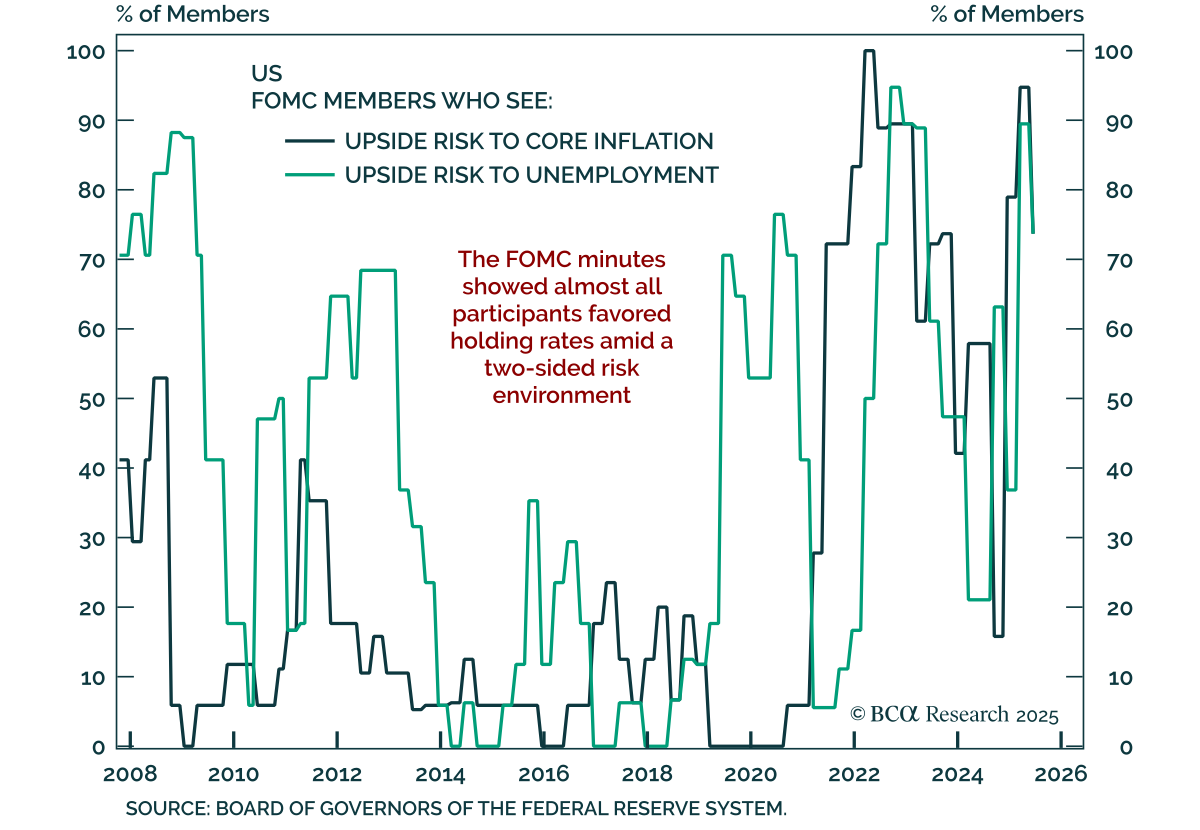

FOMC minutes showed broad support to hold in July, but the committee remains divided between proactive doves and reactive hawks. “Almost all members” favored leaving the funds rate unchanged, though two dissented for an immediate 25 bps cut. Doves want…

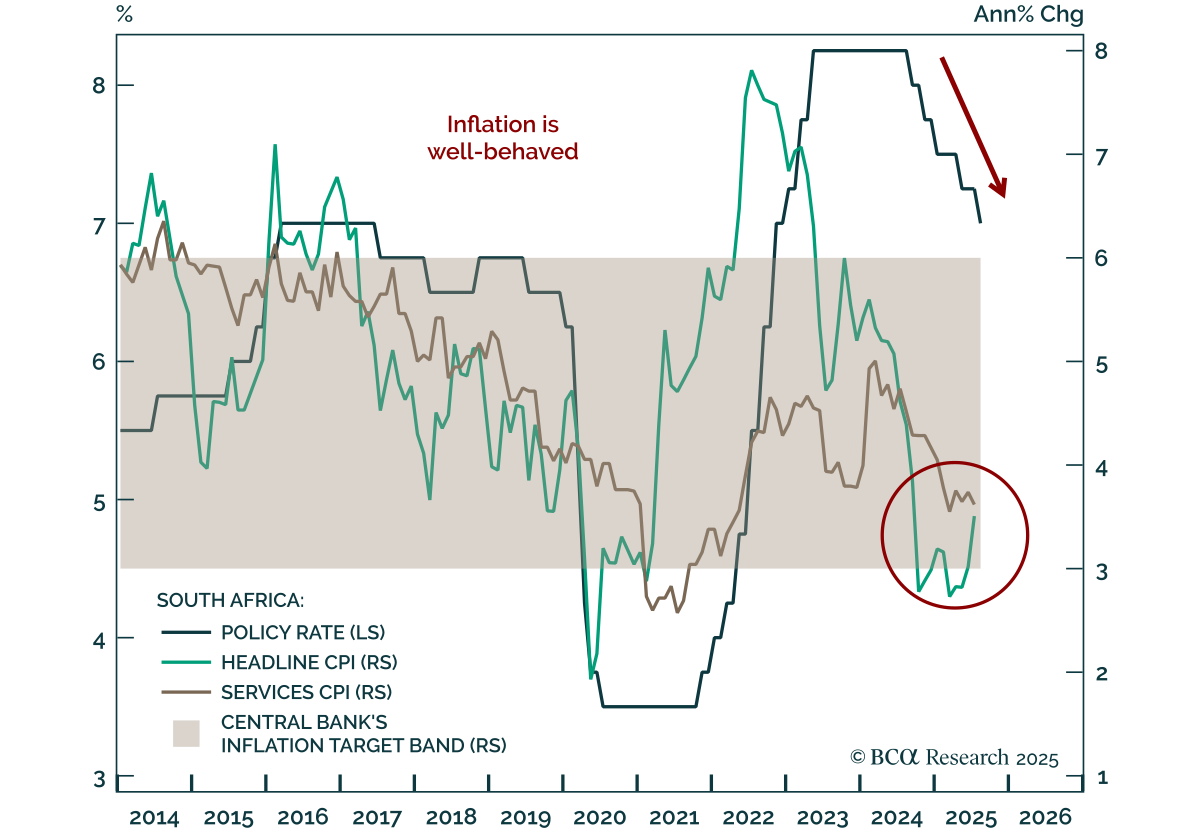

South African inflation will remain at the bottom of the SARB target range, allowing further easing. July CPI came in line with expectations at 3.5% y/y, with core at 3.0%. Our Emerging Markets strategists expect the central bank to keep cutting in…

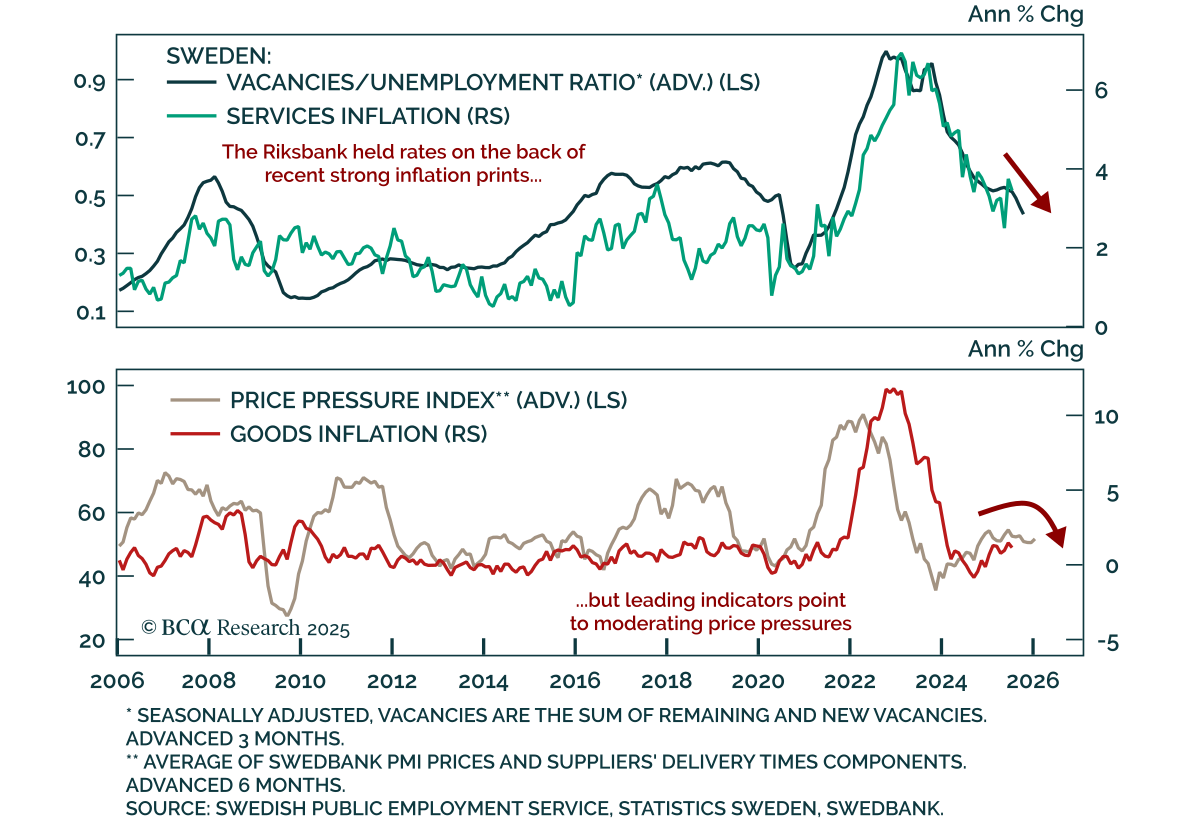

The Riksbank held at 2.0% as core inflation remains above target, though easing pressures are building. July headline inflation had slightly cooled, but core remains above both the bank’s forecast and the 1-3% target band. Inflation drivers point to…

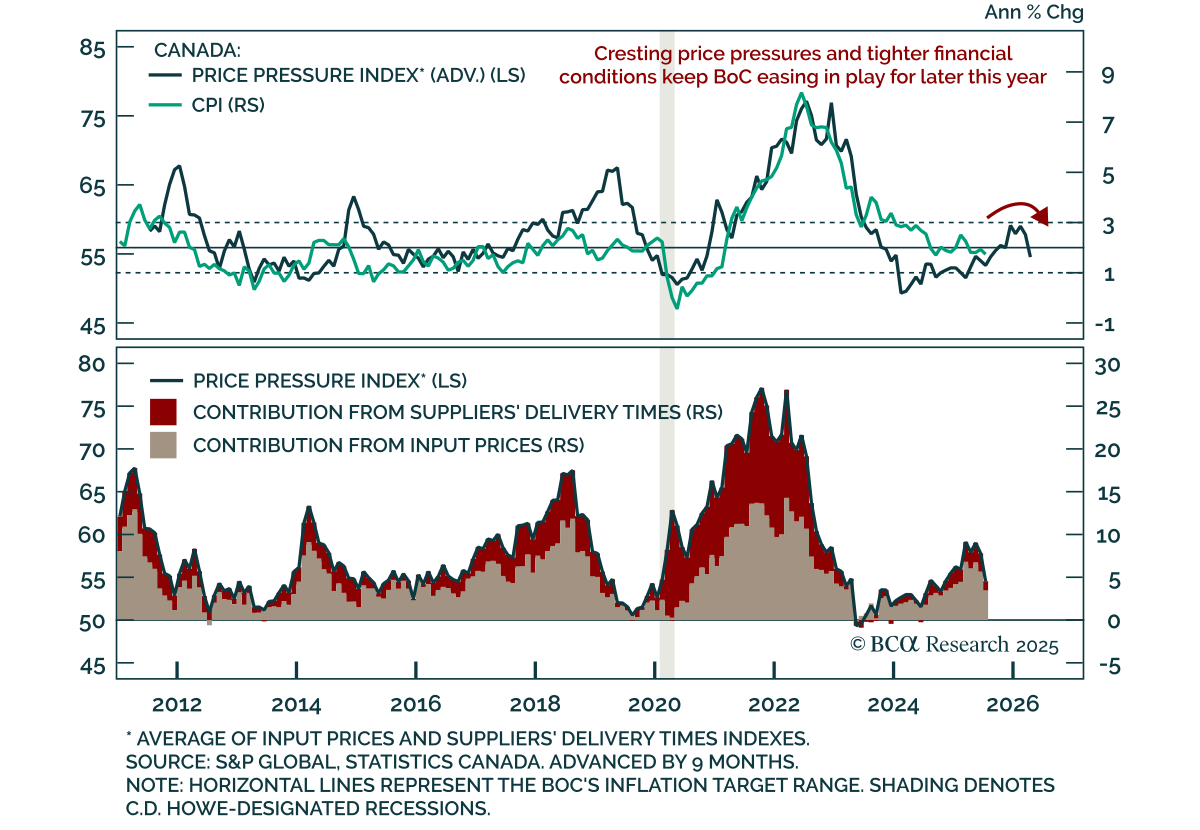

July’s softer Canadian inflation, set against lingering macro weakness, reinforces the case for more BoC easing than markets are currently pricing. Headline CPI slowed to 1.7% y/y from 1.9%, below expectations, driven by lower gasoline prices. The BoC’s…

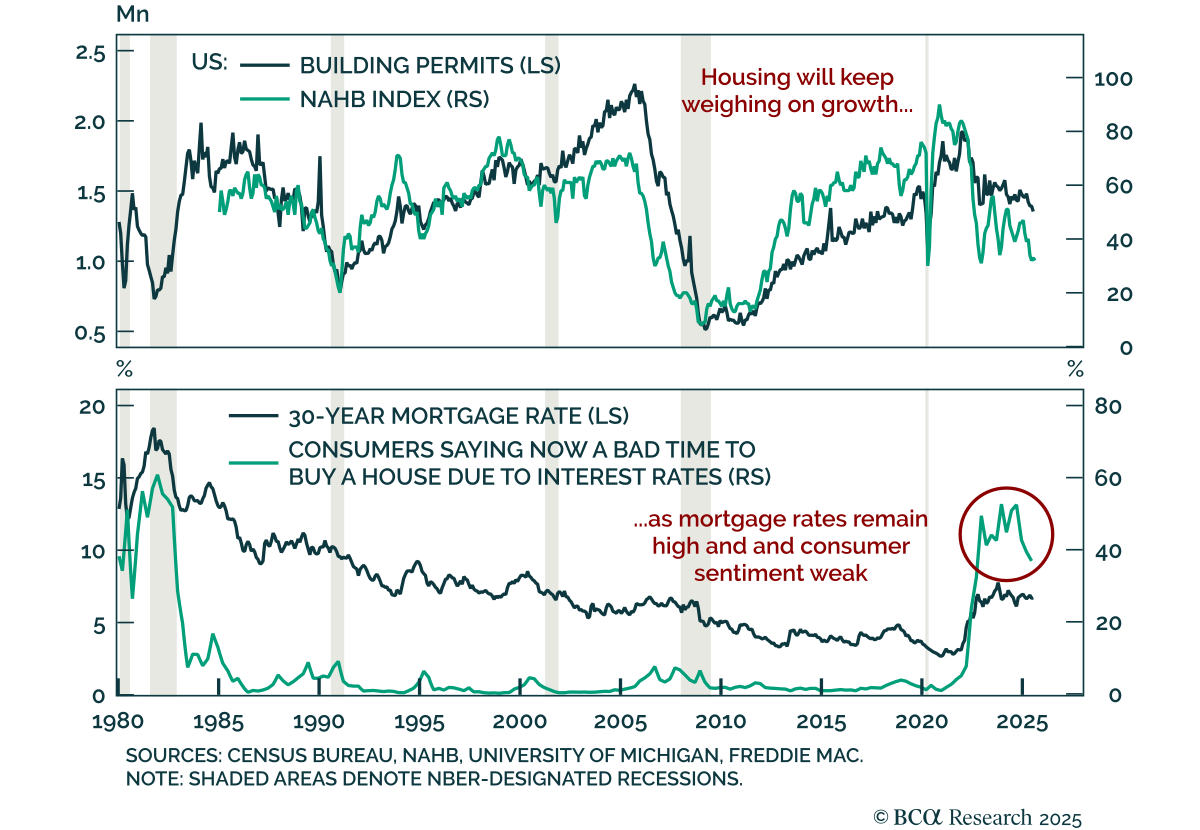

US housing data remain weak, reinforcing a fragile growth backdrop and the need for equity downside protection. July housing starts rose 5.2% m/m (annualized), but building permits fell 2.8% following a small June decline. The August NAHB Housing Market…

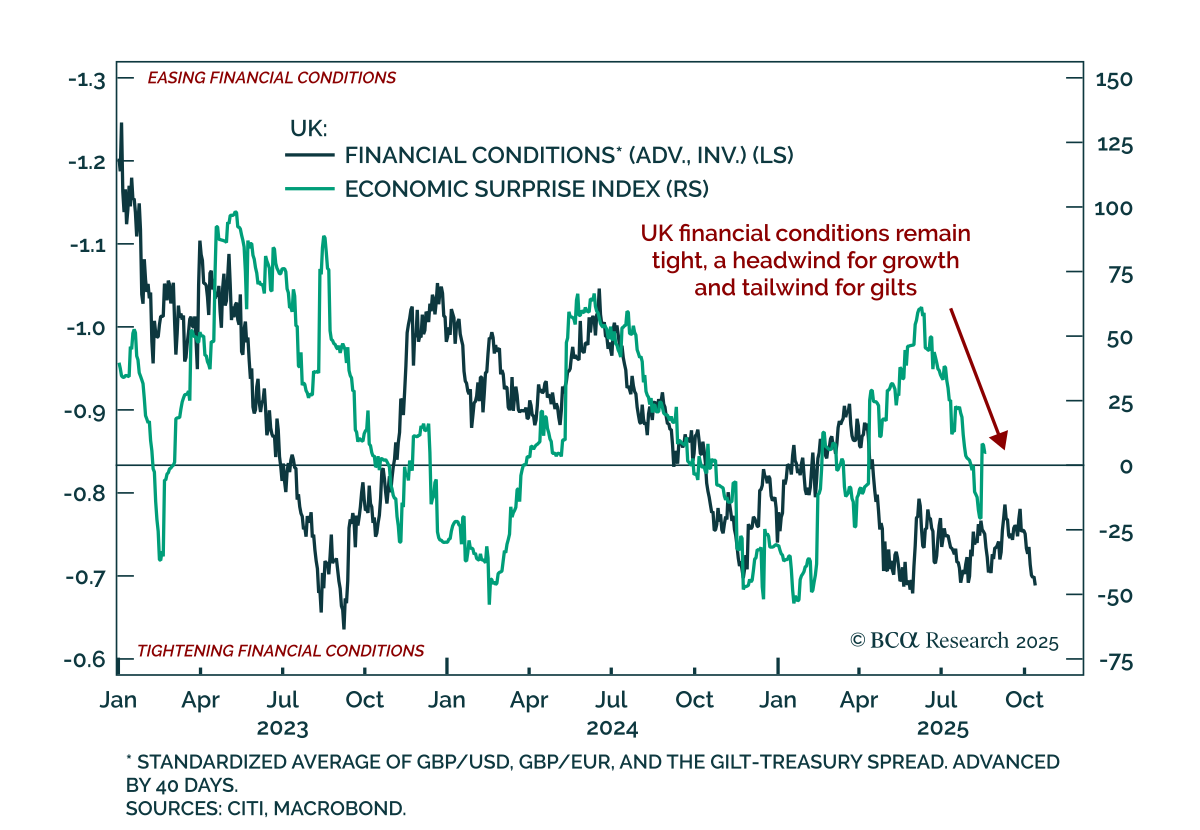

UK data momentum is fading, keeping Gilts attractive and GBP vulnerable. At 5.60%, 30-year Gilts trade at their highest yields since the late 1990s, reflecting persistent pressure on the long end across DMs. The Bank of England has lagged the ECB in its…

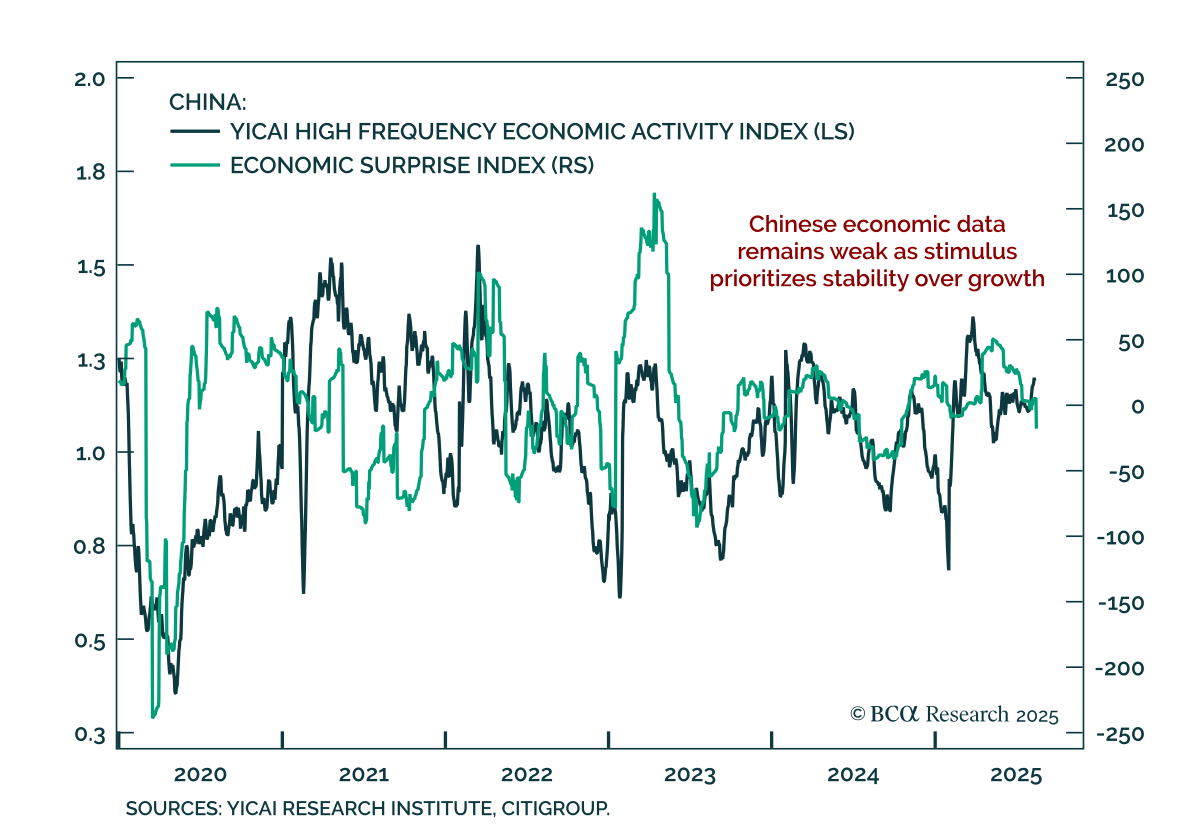

July data confirm China’s weak growth, with no near-term shift toward meaningful stimulus. New home prices fell 0.31% m/m, retail sales slowed to 3.7% y/y from 4.8%, and industrial production eased. Flooding in July disrupted infrastructure spending…

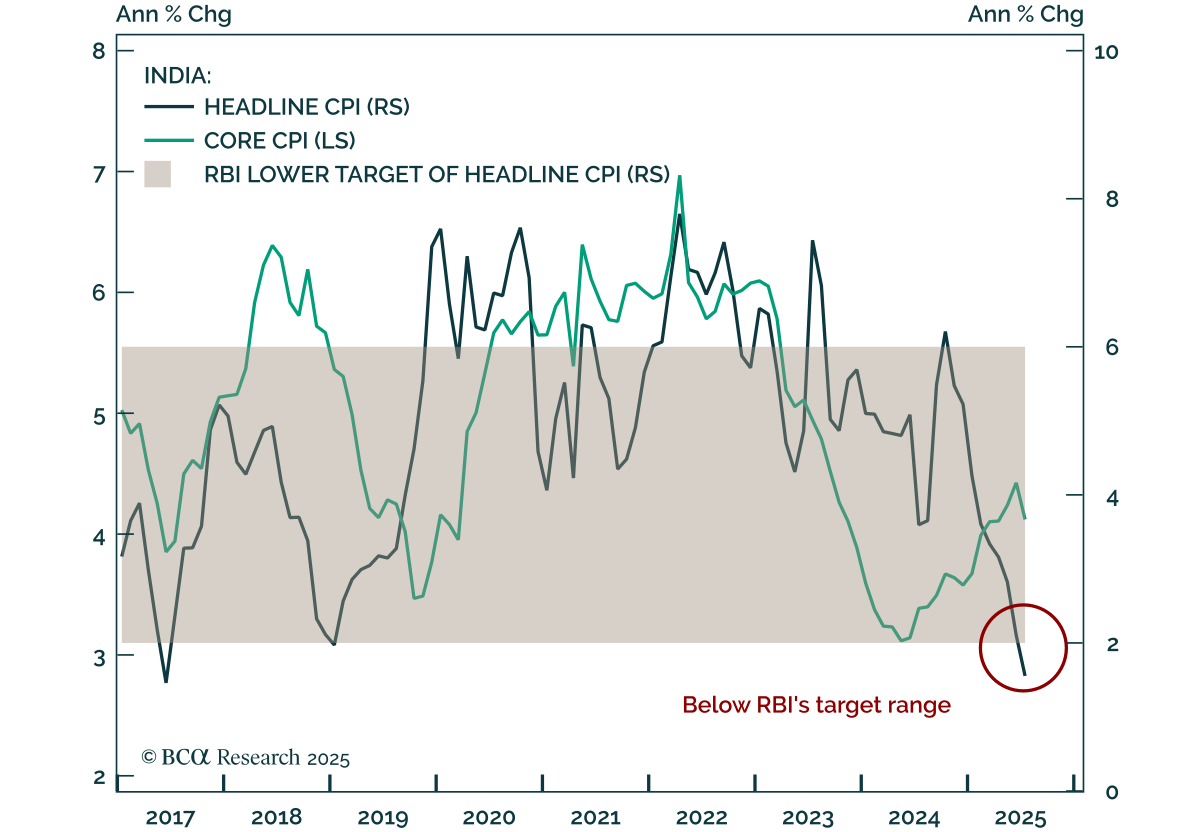

India’s sharp CPI undershoot will bring forward rate cuts, supporting a long on local bonds. Headline CPI fell to 1.55%, well below the RBI’s 2-6% target range, pointing to earlier and deeper easing than markets price. Our Emerging Markets strategists…

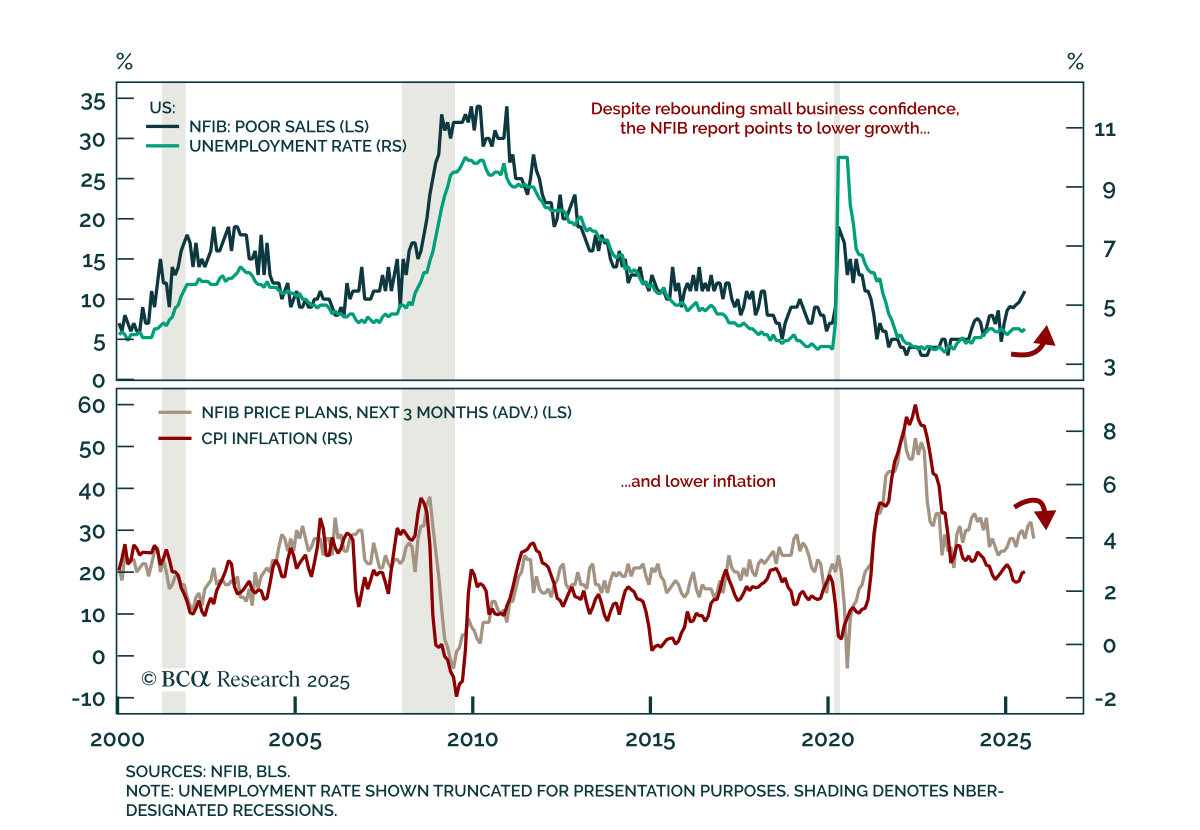

The July NFIB survey showed a rebound in expectations, but underlying weakness reinforces left-tail risks and supports a moderate risk-off allocation. The headline index rose to 100.3, a five-month high, but remains below December 2024 levels. The…

July US CPI met expectations as leading indicators point to disinflation, supporting our long duration stance and preference for 2s5s steepeners. Headline CPI rose 0.2% m/m (2.7% y/y), while core increased 0.3% m/m and accelerated to 3.1% y/y. Both goods…