Monetary

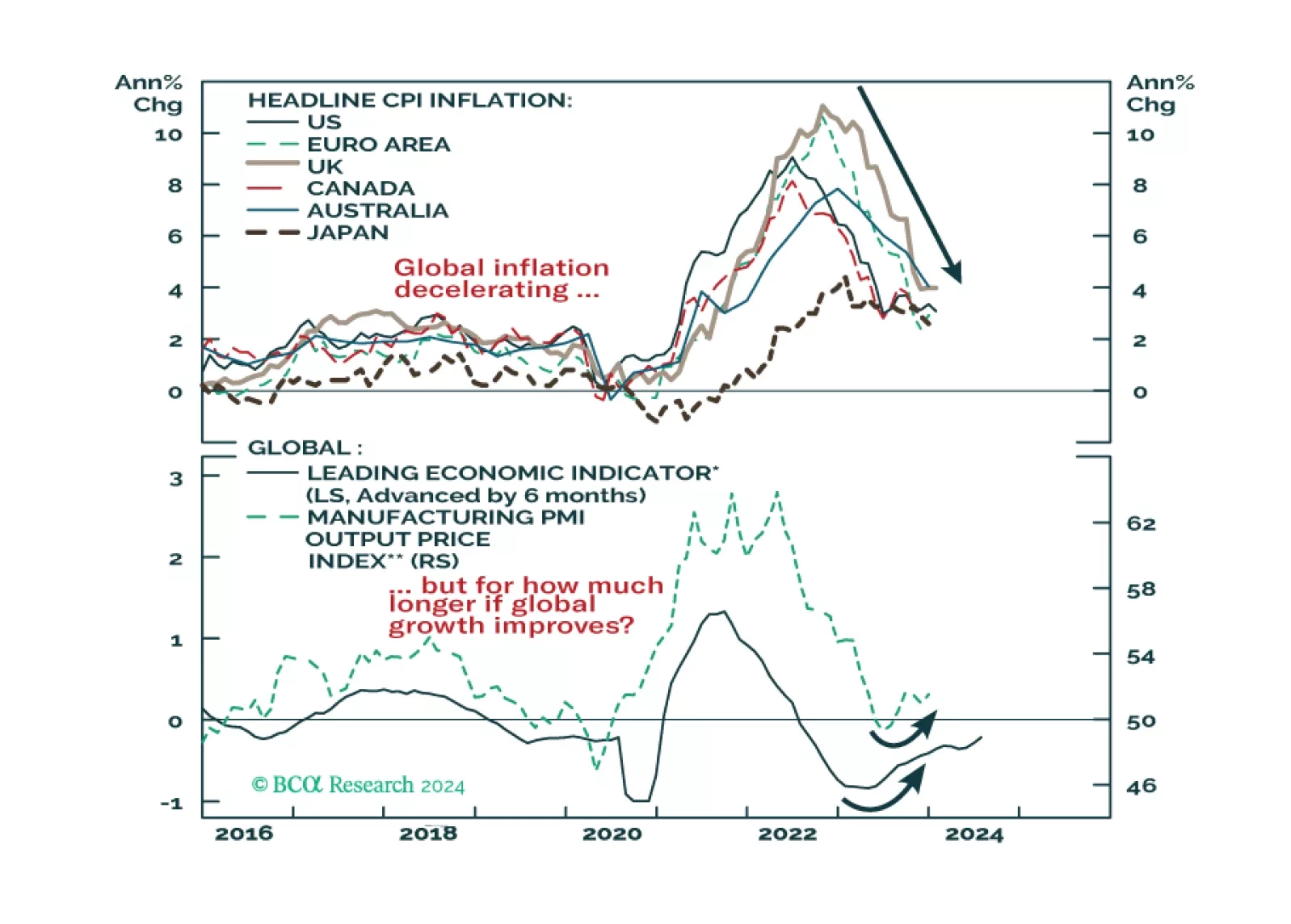

Could a second wave of global inflation be underway? The latest inflation prints in the US and UK showed upside surprises, while there is evidence of increased price pressures in global manufacturing. Combined with the improvements seen in economic sentiment measures and leading economic indicators in the US and Europe, and potential upside risks to oil prices, we see a strong case for owning more inflation protection in global bond portfolios. Inflation-linked bonds look attractive in this environment, especially in the US.

The hotter-than-anticipated US PPI report for January prompted a selloff in Treasuries on Friday. The monthly and annual changes in both the headline as well as the core measures of final demand PPI came in above expectations. Core PPI’s 0.5% m/m increase…

According to BCA Research’s Global Investment Strategy service, although the next recession is likely to be mild-to-moderate, the ensuing financial avalanche will be more severe. Valuations are highly stretched and hopes that today’s tech leaders will…

The first two regional fed manufacturing surveys for February delivered strong upside surprises. The New York Fed’s Empire Index surged from -43.7 to -2.4, unwinding its January slump. Similarly, the Philly Fed current activity index jumped by 15.8 points to…

The UK inflation release for January came in slightly softer than anticipated. Both headline and core CPI were unchanged on year-over-year basis at 4.0% and 5.1%, respectively – below expectations of slight accelerations. The 0.6% m/m decline in the headline…

In a recent Insight we looked at the performance of equities following the start of monetary easing cycles. Specifically, we looked at the historical performance of US cyclical sectors versus defensive sectors at various points in time after the Fed’s first…

Prices of agricultural commodities have come under intensified downward pressure this year. Corn, soybean, and wheat prices have fallen by 8.6%, 8.3%, and 4.9% respectively so far this year. Multiple factors are behind the selloff. First, ag prices…

The US CPI report for January showed inflation did not cool as much as anticipated. Headline inflation accelerated from 0.23% to 0.31% on a month-over-month basis, higher than anticipations of 0.2% m/m. It fell from 3.4% to 3.1% on a year-over-year basis,…