Monetary

We highlighted in a recent Insight that positive economic surprises are prompting economists to revise up their US economic growth expectations. The Goldilocks narrative is supporting the rally in risk assets. However, results of the January NFIB survey…

The German economy was a laggard at the end of last year, posting a 0.3% q/q real GDP contraction in Q4 2023 while the broader Eurozone economy stagnated. Importantly, while economists have been revising up their 2024 forecasts for the US economy, they have…

The Swiss franc is among the worst performing major currencies so far this year. This marks a reversal following its stellar performance last year. The Swiss National Bank’s (SNB) support for the domestic currency is behind last year’s strength.…

China will continue to suffer from a “triple crisis”. Though there could be a tactical bounce, cyclically we still recommend underweighting Chinese equities.

China’s credit data update for January delivered a mixed signal on Friday. The CNY 6.50 trillion increase in aggregate financing beat expectations of CNY 5.60 trillion and marked a significant acceleration from CNY 1.94 trillion in December. Similarly, the…

The latest Canadian data suggest that although demand is cooling down, the Canadian economy is not in freefall. The unemployment rate fell for the first time since December 2022, declining by 0.1 percentage points to 5.7%, compared to consensus…

Our Emerging Markets team believes that the risk-reward profile of the US dollar remains very attractive. First, if US growth stays robust, US interest rate expectations will rise because rate cuts priced in will not be realized. Rising interest rates will…

BCA Research’s Global Investment Strategy service’s revised forecast is centered on a recession starting in late 2024 or early 2025. The strong pace of US growth has continued into early 2024. Preliminary estimates from the Atlanta Fed’s GDPNow model…

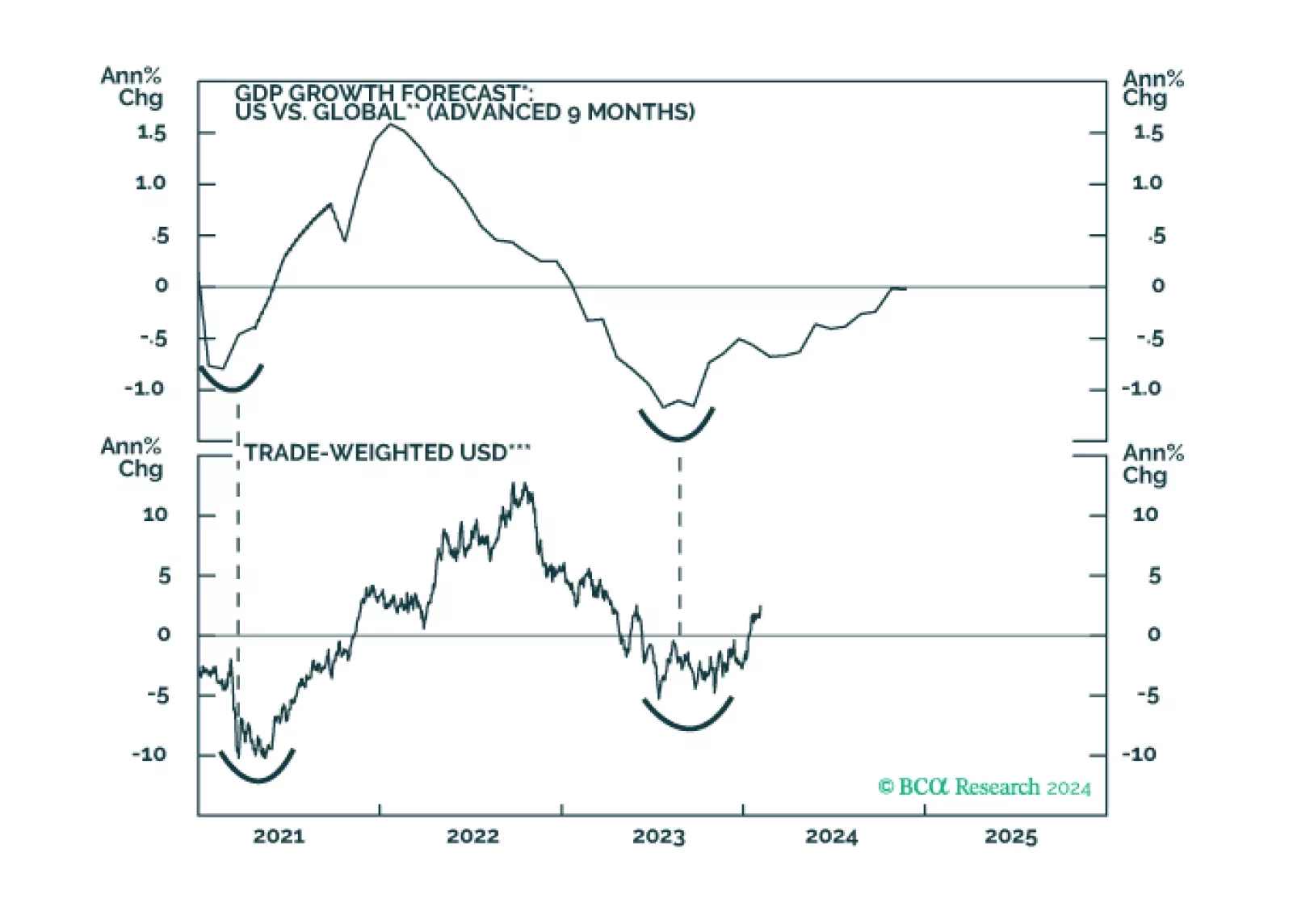

This week’s report explores factors behind the recent rise in the dollar, and whether this could continue in the next month.

Easier financial conditions, rising home prices, rebounding consumer sentiment, and a stabilization in manufacturing activity all augur well for near-term US growth prospects. An unsustainably low savings rate is a key risk to the US economic outlook. Our revised forecast is centered on a recession starting in late 2024 or early 2025.