Monetary

Friday’s US Personal Income and Outlays report for December delivered a positive update on the US economy. On the growth side, the data confirm the signal from the Q4 GDP release that consumer spending continues to power the US economy. The robust 0.5%…

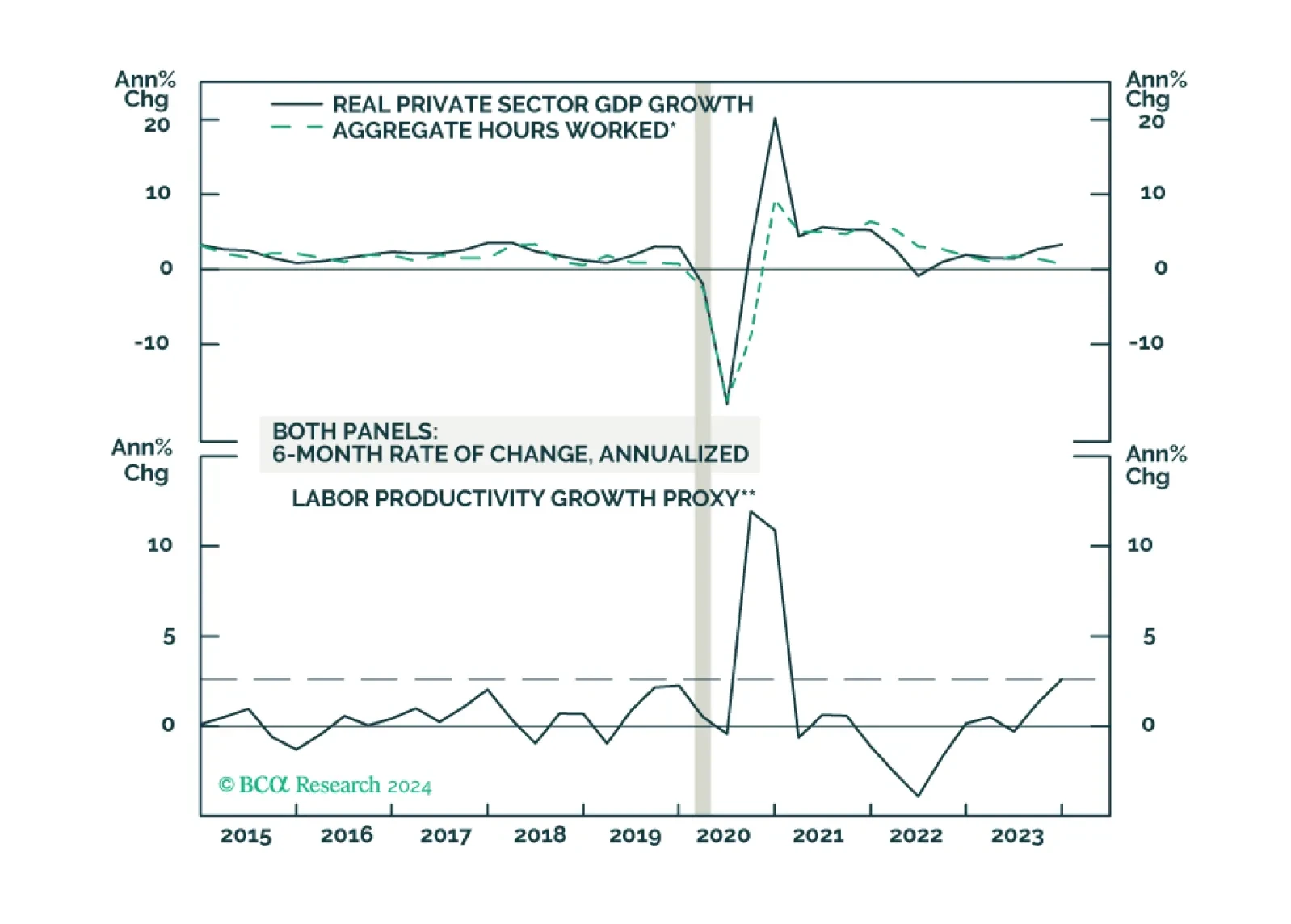

According to BCA Research’s The Bank Credit Analyst service, there are two important flaws in the market’s “Goldilocks” narrative. First, investors are assuming inflation will fully return to target this year because core inflation ex-housing is already at…

Low inflation argues for the Fed to move relatively quickly toward rate cuts. Continued above-trend GDP growth poses a risk to this view, but leading indicators point to slower growth in the coming quarters.

We look at the implications for FX from the slew of central bank meetings this week.

Government bond yields rallied and yield curves steepened across the Eurozone on Thursday following a less hawkish than anticipated tone from the ECB. As expected, the central bank kept policy rates unchanged and reiterated that it is still premature to…

Chinese policymakers have ramped up their efforts to support the economy and financial markets over the past few days. On Wednesday, the People’s Bank of China (PBoC) announced that on February 5 it will cut the reserve requirement ratio by 0.5 percentage…

The Bank of Canada (BoC) kept rates steady at yesterday’s monetary policy meeting, leaving its policy rate at 5%. The central bank presented updated economic projections in a new Monetary Policy Report (MPR), which were little changed from the last MPR in…

Results of the ECB’s quarterly Bank Lending Survey suggest that the tight monetary policy stance is still weighing on the Eurozone economy. Banks tightened credit standards for businesses and consumers further in Q4 2023, contributing to the substantial…

As expected, the Bank of Japan maintained its ultra-easy monetary policy stance at its meeting on Tuesday, making no changes in interest rates or yield curve control. The monetary policy statement highlighted that elevated uncertainty around the economic…

Ahead of today’s Bank of Canada (BoC) meeting and the Reserve Bank of Australia (RBA) meeting on February 6th, our Global Fixed Income Strategists compared the monetary policy outlooks for both central banks. In Canada, core inflation has already fallen…