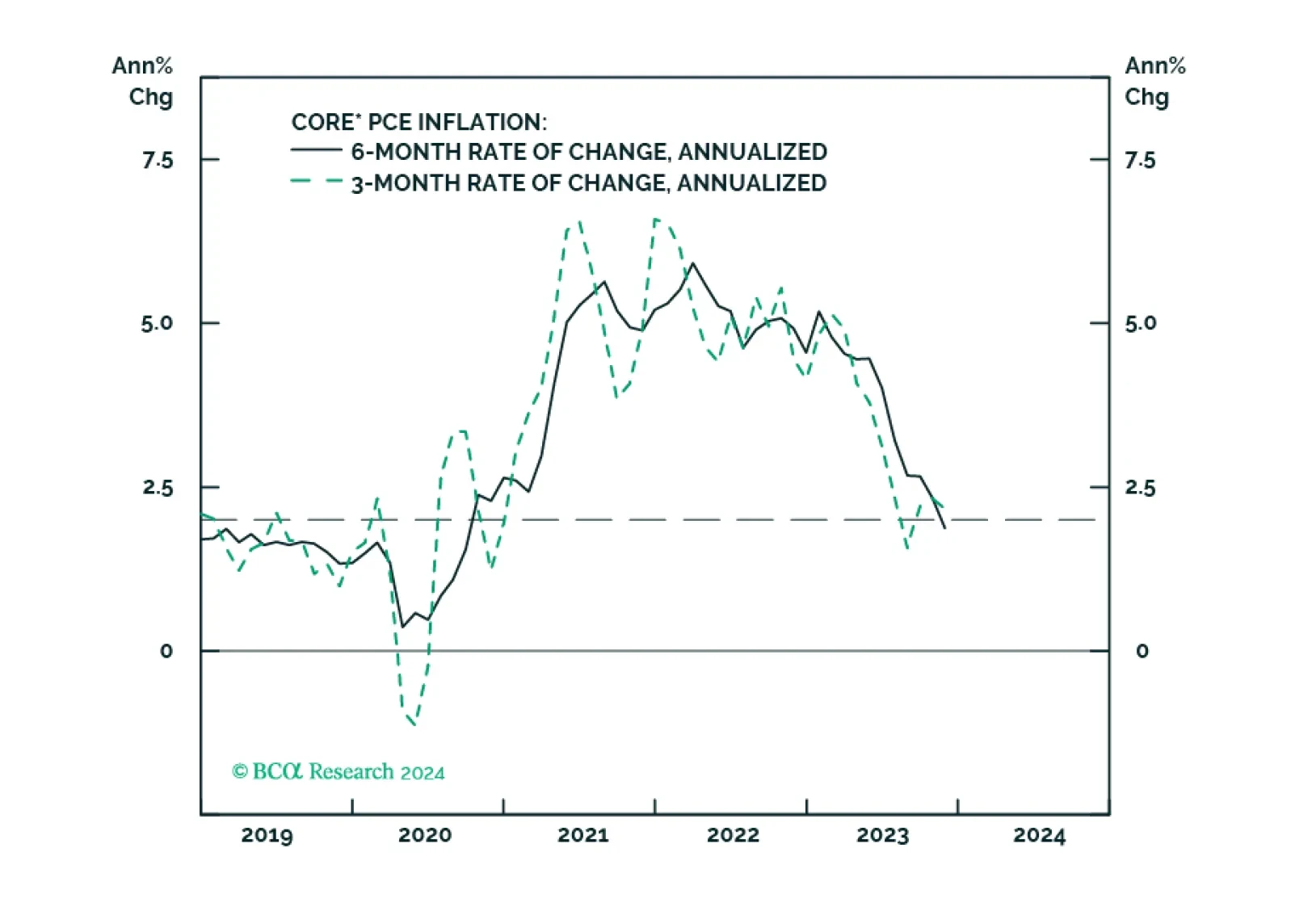

Monetary

An update to our outlooks for the Fed’s interest rate and balance sheet policies following this week’s remarks from Fed Governor Waller.

Recent data suggest that the US housing market is resilient. In particular, a strong rebound in homebuilder sentiment is sending a positive signal. The NAHB Housing Market Index jumped from 37 to 44 in January – handily beating expectations of 39 on the back…

The Fed’s latest Beige Book delivered a lukewarm message on the US economy. Growth, employment, and prices were all relatively stable since the previous release in late-November. Eight districts reported little or no change in activity, three districts…

The US retail sales release delivered a positive signal about the US economy in December. The 0.6% m/m increase in overall retail sales beat expectations of a more muted acceleration from 0.3% m/m to 0.4% m/m. Importantly, the improvement was broad-based with…

The British pound was the best performing G10 currency on Wednesday as UK gilts sold off meaningfully with the 10-year yield ending the day nearly 19 basis points higher. An unexpected acceleration in CPI inflation in December prompted the move. Notably,…

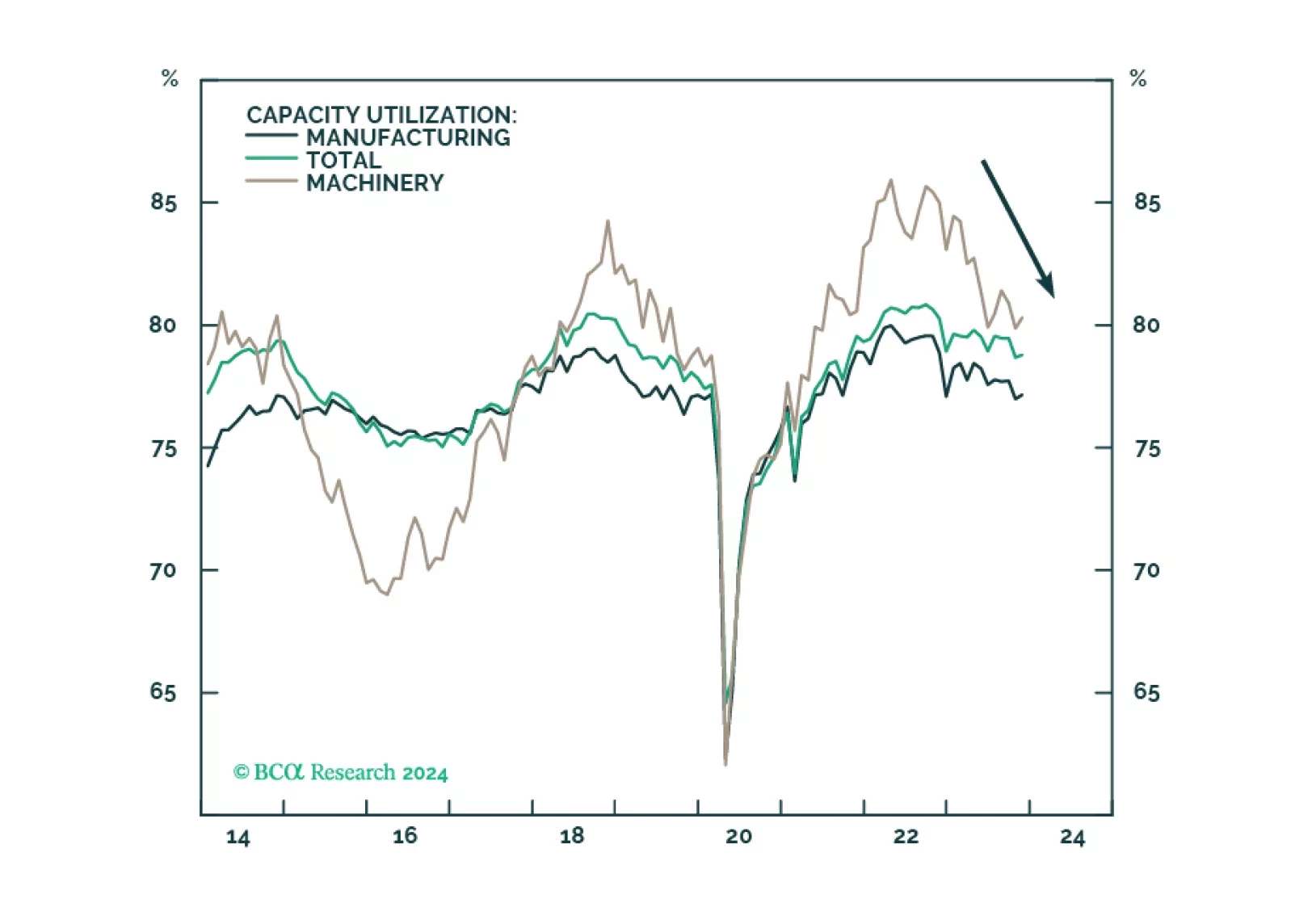

The performance of the Industrials sector tends to lag the business cycle, as companies invest in capex on the heels of economic expansion. But demand is not entirely cyclical, as the need to replace obsolete or aging equipment or machines is relatively…

Canadian government bond yields jumped on Tuesday, with the 10-year yield rising by nearly 14 basis points. While most other major DM government bonds also sold off, the move in Canadian yields was relatively more pronounced. Both global and domestic forces…

Results of the ZEW survey sent a slightly positive signal on German investor sentiment. The economic expectations indicator rose to an 11-month high in January – beating consensus estimates of a decline. This increased optimism about the outlook reflects an…

The US manufacturing renaissance, spurred on by reshoring, automation, and government spending, is running its course but progress has slowed on the back of tight monetary conditions and the manufacturing recession. The deceleration of these positive trends weighs on the outlook for the Capital Goods industry group, impeding its performance over the short term. However, we reiterate that positive long-term trends for the industry remain intact. We downgrade Capital Goods to a tactical underweight. It remains a strategic overweight.

Canada’s Business Outlook Survey (BOS) indicator increased slightly in Q4, suggesting that sentiment stabilized at the end of 2023. In particular, easing inflationary pressures amid weaker demand and greater competition drove the 0.3-point uptick. Notably,…