Monetary

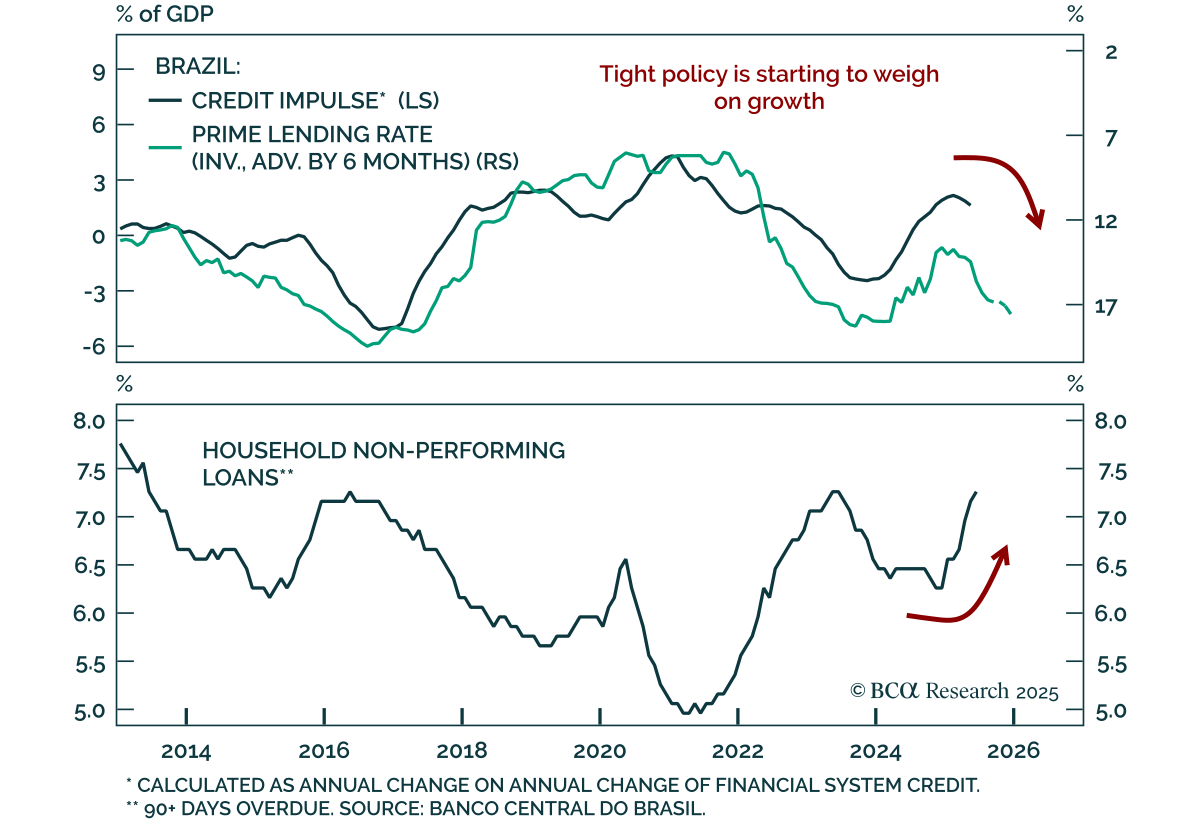

The Central Bank of Brazil (BCB) held rates at 15%, guaranteeing a sharp growth slowdown and reinforcing our underweight stance on Brazilian equities versus EM. All Copom board members voted to maintain an ultra-hawkish policy due to unanchored inflation…

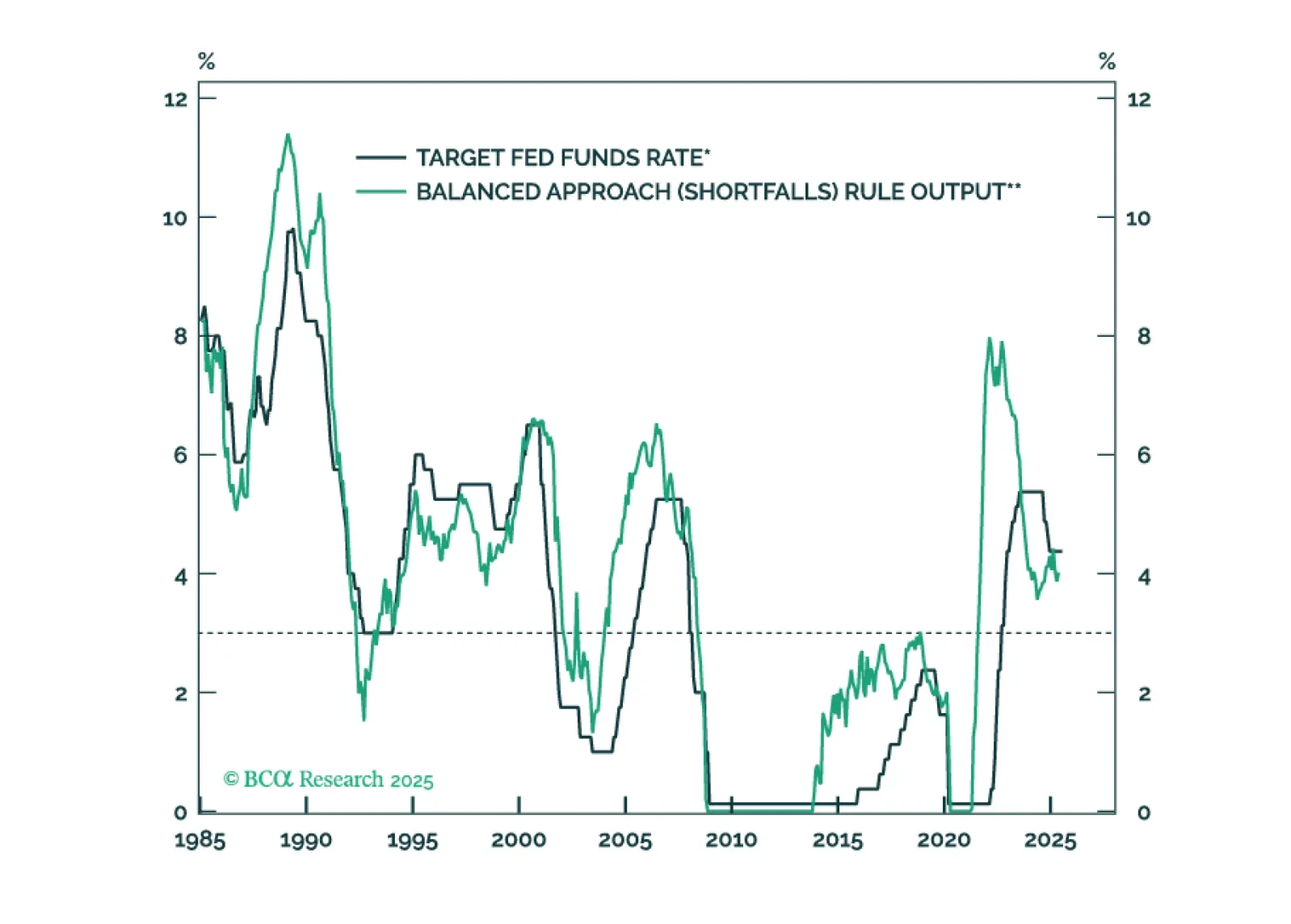

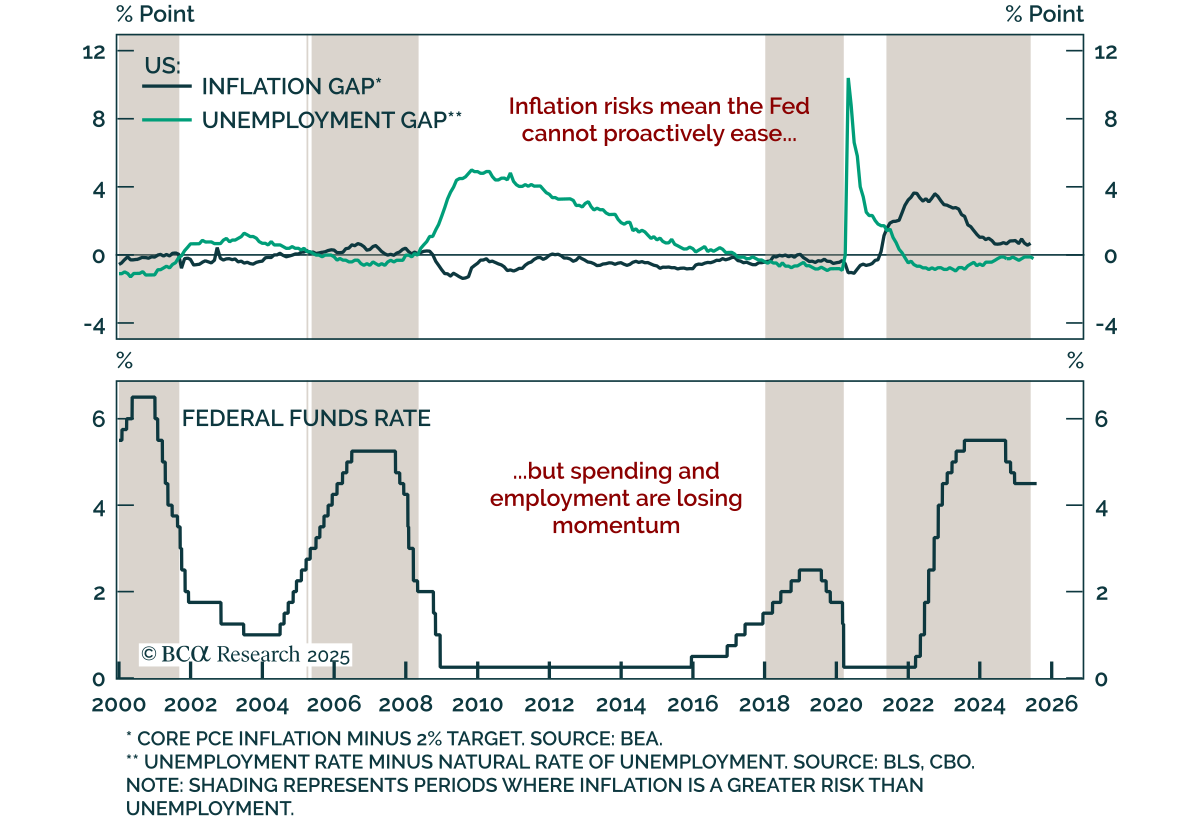

The Fed will keep rates on hold until the unemployment rate forces its hand.

The Fed held rates steady for a fifth straight meeting, with a divided FOMC and resilient growth keeping policy on hold, supporting our long-duration stance. The target range remains at 4.25%–4.50%, with the statement reflecting only a modest downgrade to the…

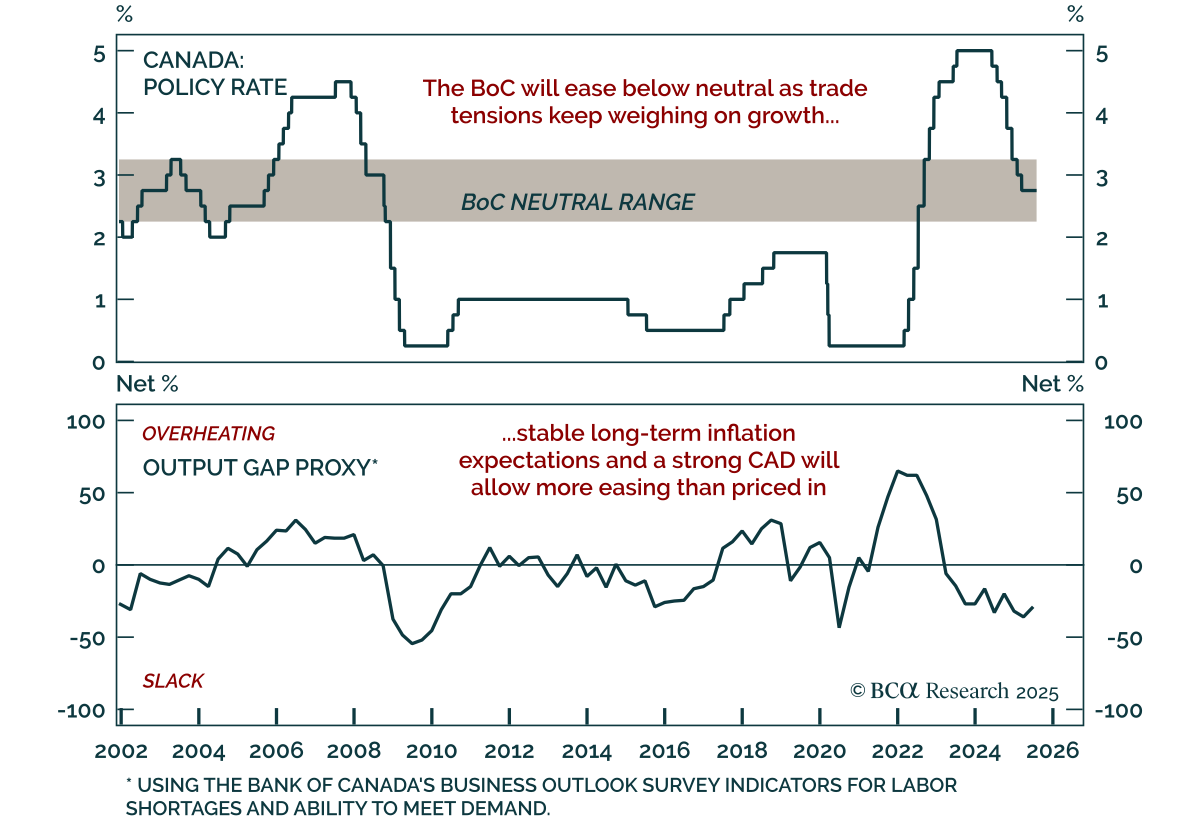

The BoC held rates at 2.75% for a third consecutive meeting, but a weak growth outlook and contained inflation reinforce our overweight in Canadian bonds. With policy within the 2.25%–3.25% neutral range, the BoC remains comfortable waiting for clarity…

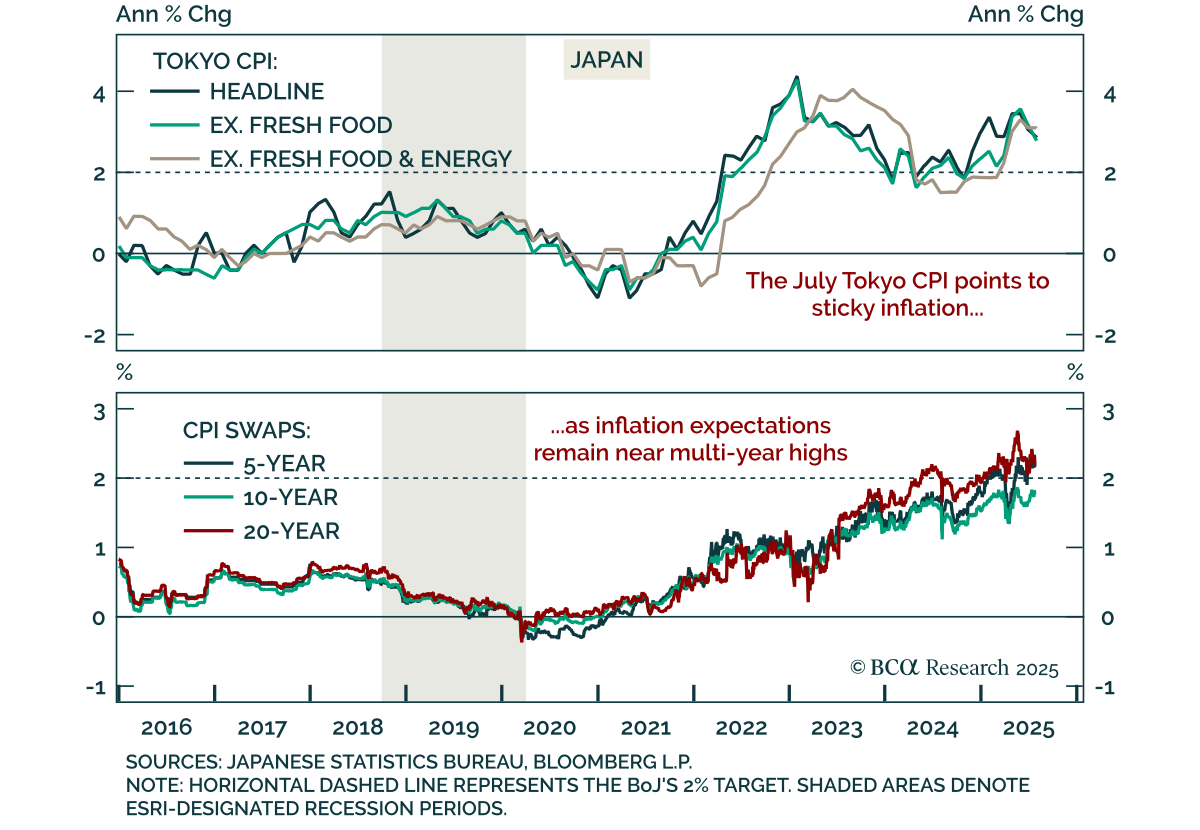

Tokyo CPI data confirms persistent inflation pressures in Japan, keeping the BoJ on a hawkish footing and reinforcing our underweight in JGBs and bullish stance on the yen. July Tokyo CPI came in broadly in line, falling to 2.9% y/y from 3.1%, with core and…

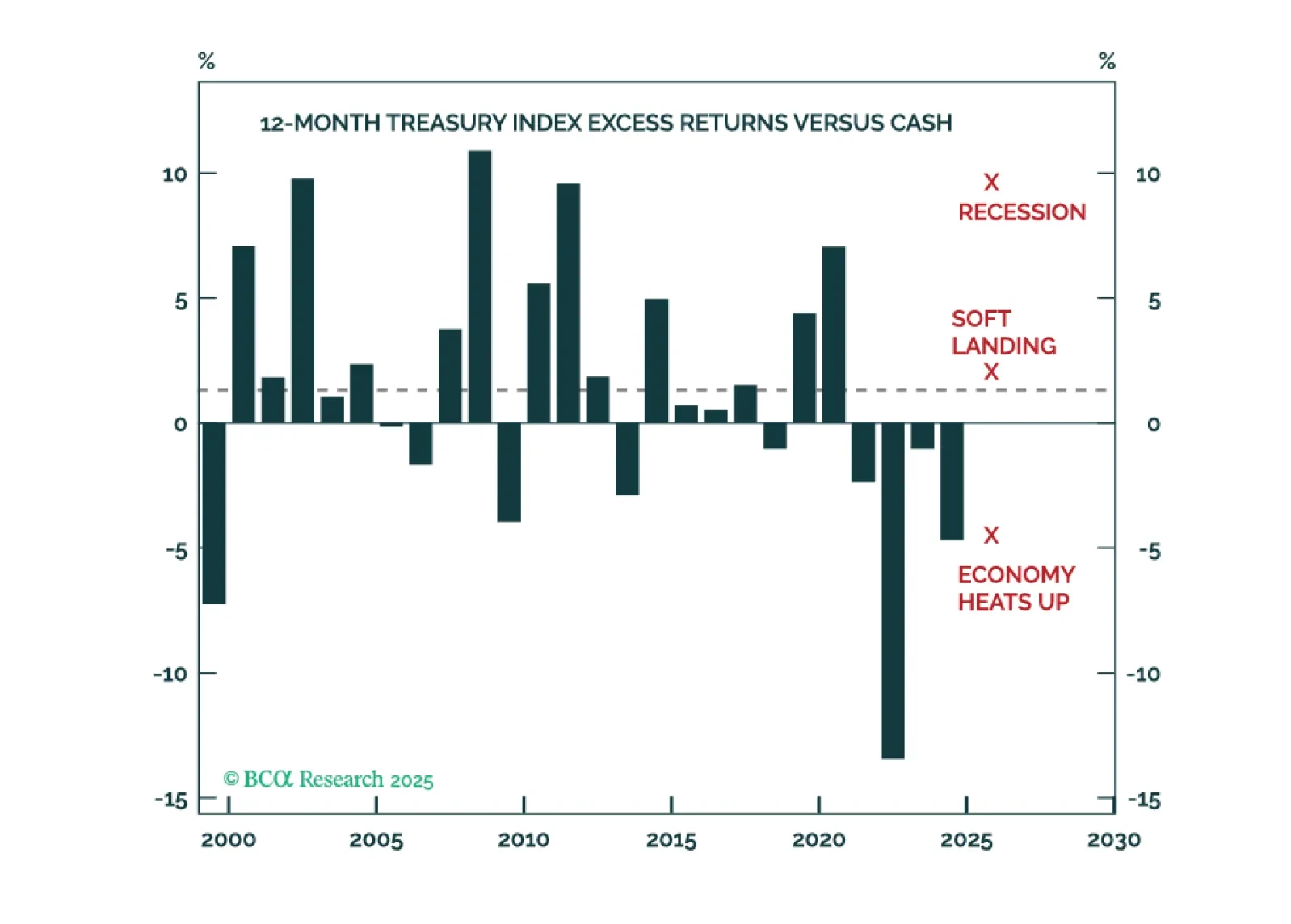

Investors should anticipate above average Treasury returns during the next 12 months, and curve steepeners will continue to profit.

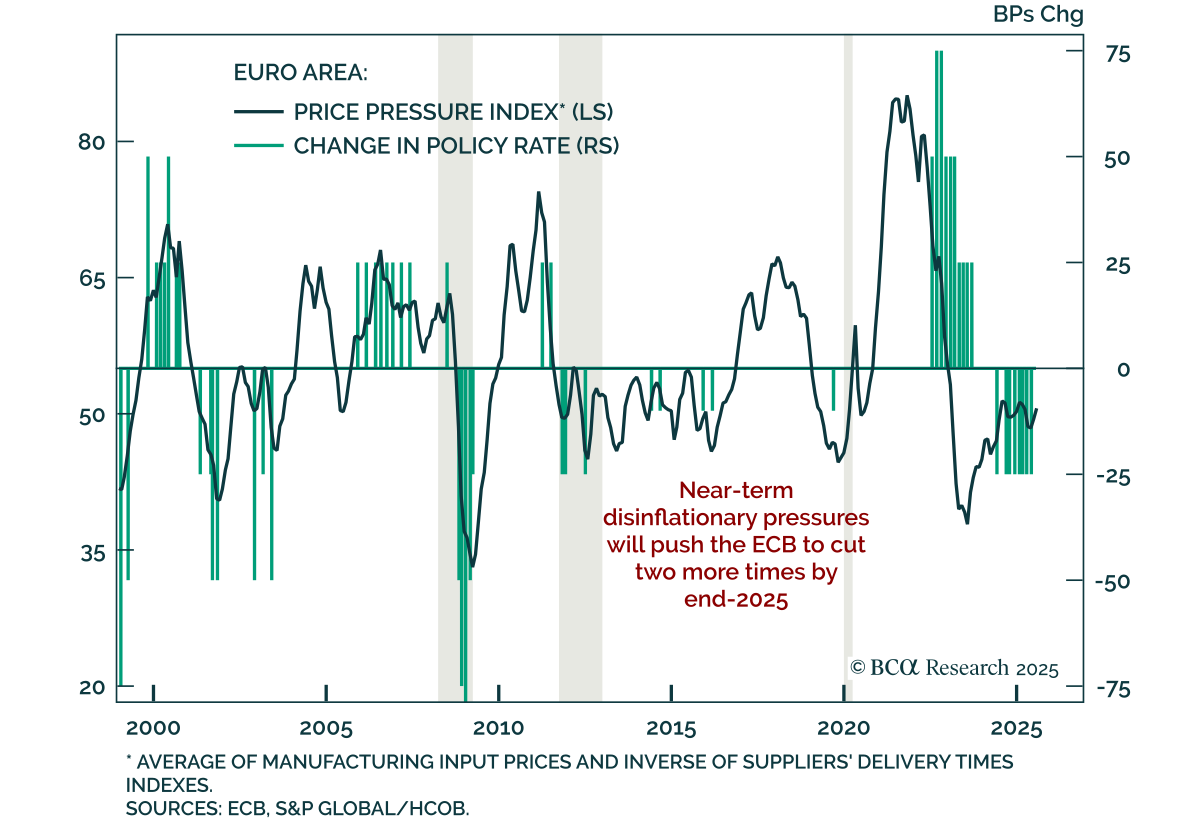

The ECB held rates steady for the first time in eight meetings, signaling a slower pace of easing while downside risks and entrenched disinflation support positioning for further cuts. The deposit facility rate remains at 2.0%, with the ECB adopting a…

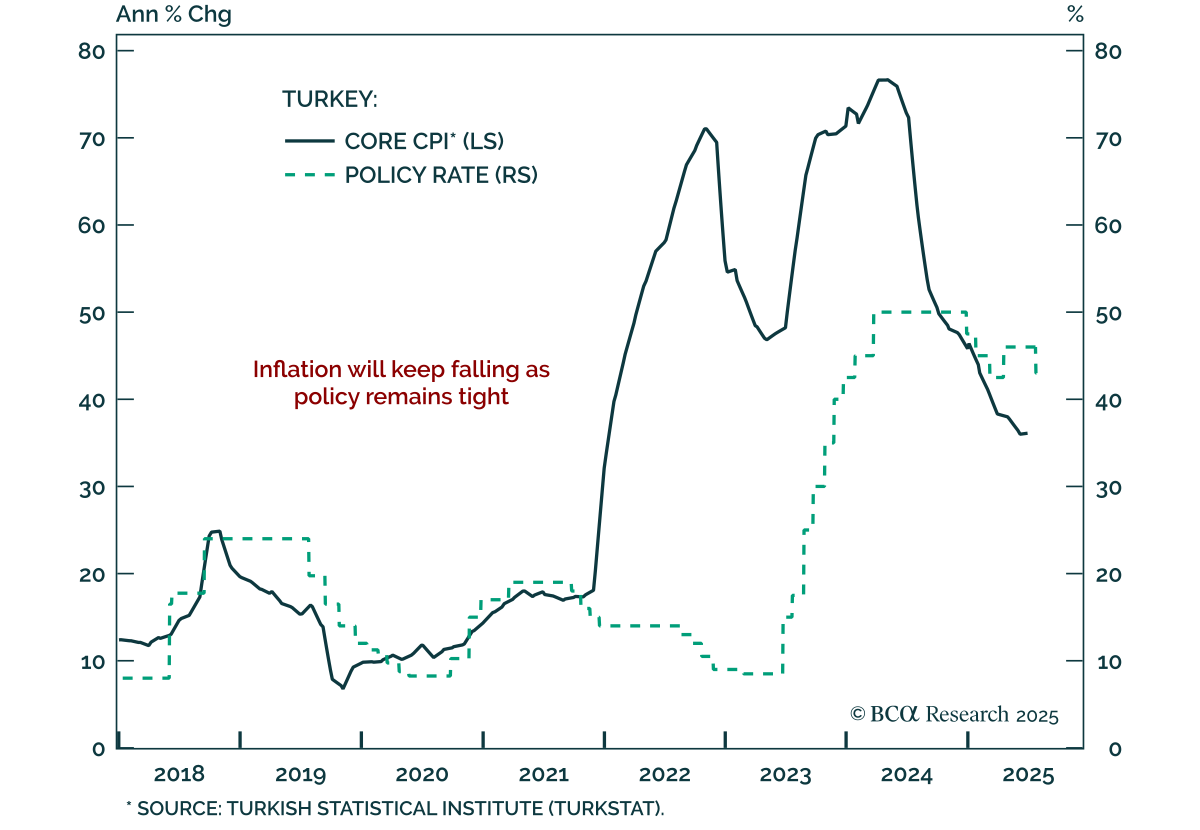

Our Emerging Markets strategists upgraded Turkey across assets, citing falling inflation, tight policy, and limited external imbalances. The Central Bank of Turkey cut its benchmark 1-week repo rate by 300 bps to 43%, citing easing inflation and slowing…

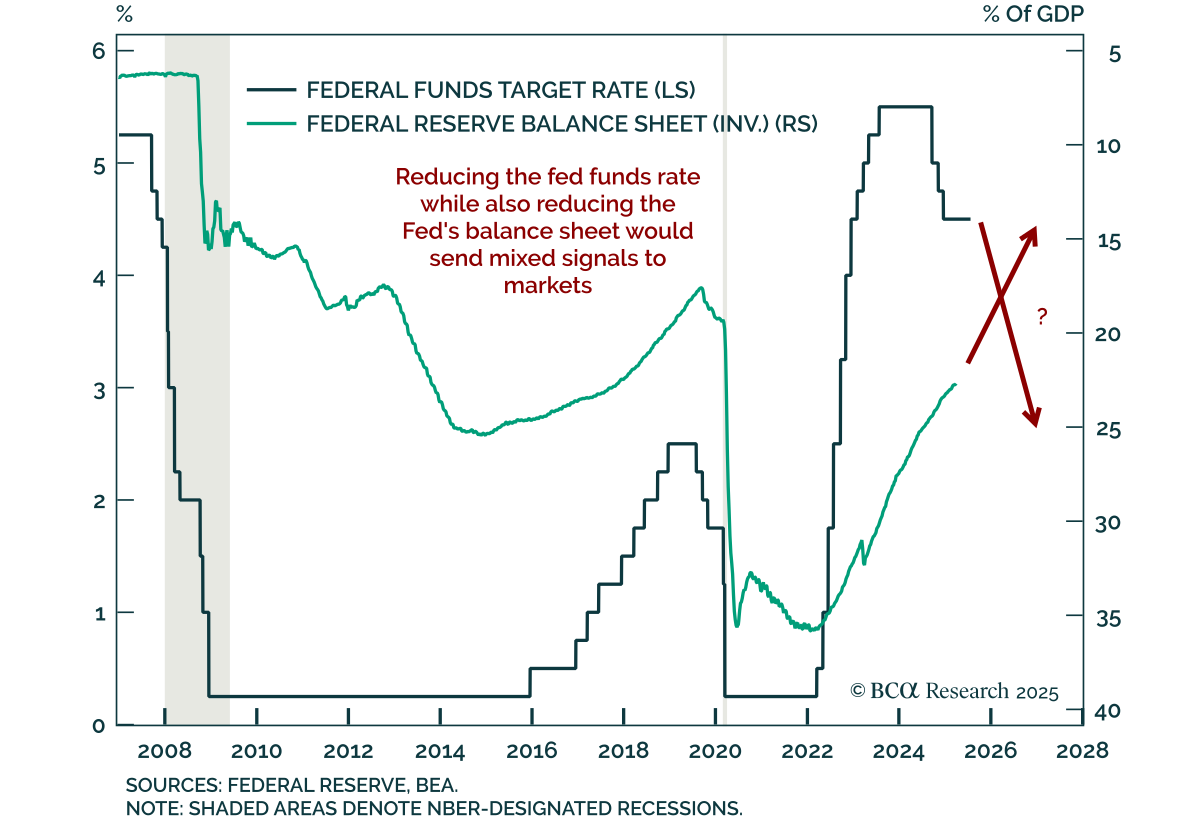

Recent criticism of the Fed centers on post-GFC policy, but proposed solutions would risk policy incoherence and higher long-end yields. Criticism covers the Fed’s reliance on balance sheet policies aimed at easing financial conditions after hitting the…

RBA minutes confirmed a cautious approach to easing, reinforcing our underweight in ACGBs and long AUD/NZD stance. The decision to hold at 3.85% surprised markets expecting a 25 bps cut. Governor Bullock had framed the decision as one of timing, but…