Monetary Policy

This is a follow-up report on Bessenomics – the policy mix that US Treasury Secretary Scott Bessent plans to pursue. The direction of US and global financial markets depends on the amount of fiscal tightening required to bring down US interest rates. Can the Trump administration cut fiscal spending just enough to bring down US bond yields but not cause a recession?

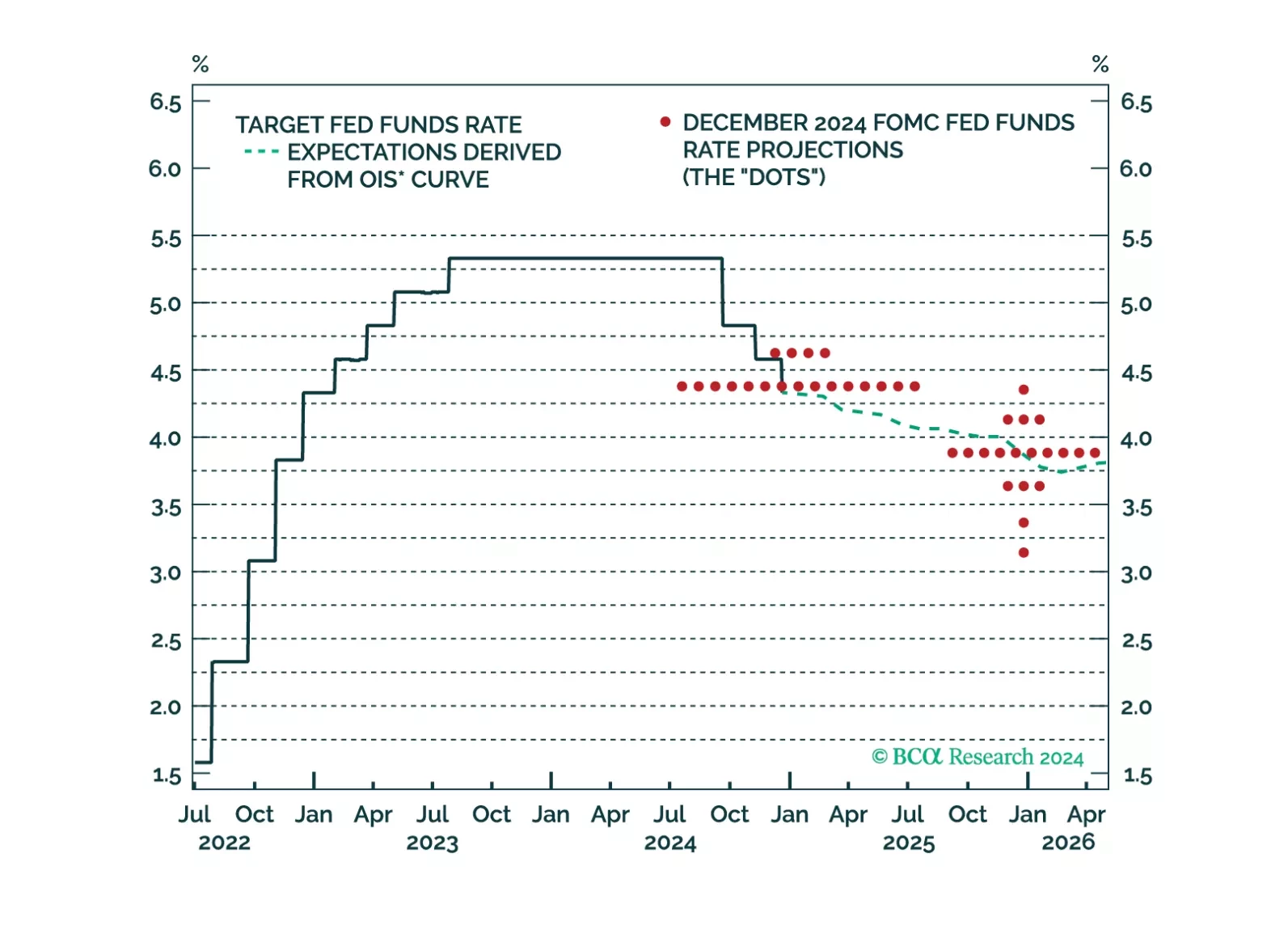

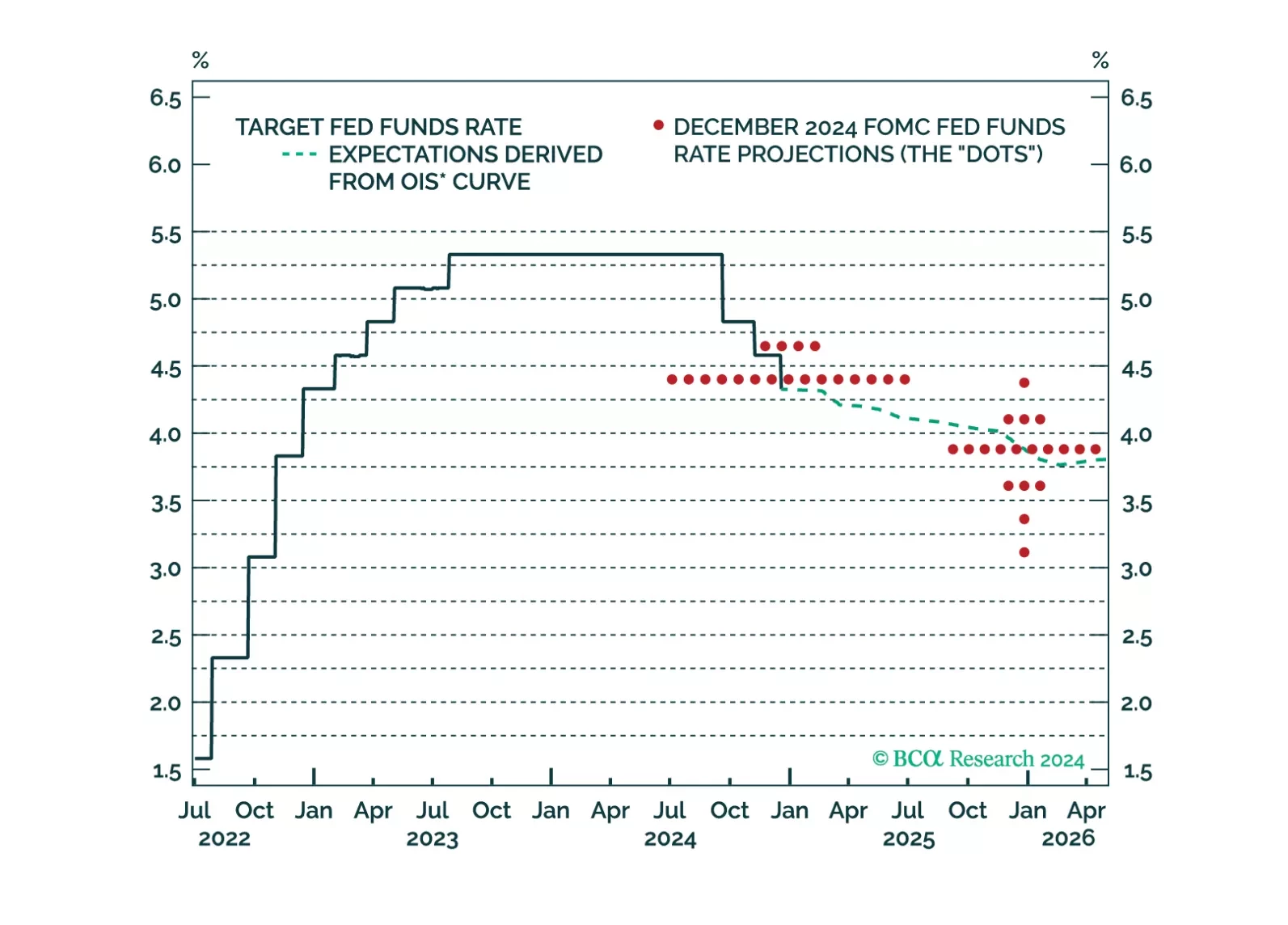

Jay Powell didn’t say much at this afternoon’s FOMC press conference, and monetary policy will continue to take a back seat to fiscal for the next few months.

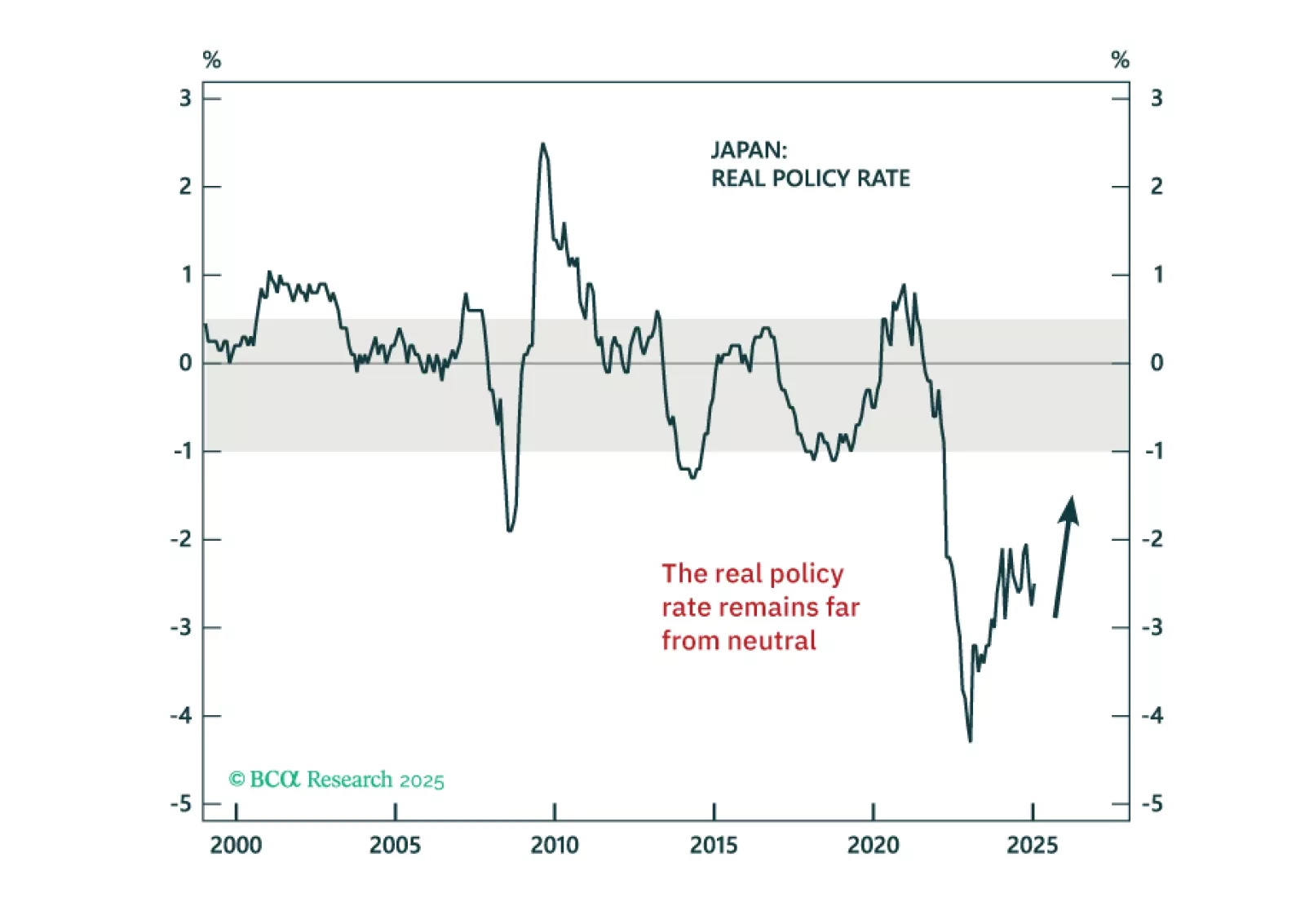

In today’s Strategy Insight, we discuss the monetary policy outlook for the Bank of Japan, following the 25-bps rate hike overnight, and what it means for JGBs and the yen.

There is no better way to gauge the macro policies of the new US administration than being privy to President Donald Trump’s discussions with the new Treasury Secretary, Scott Bessent. While we do not have inside information, we have put the pieces of the puzzle together to help clients see the big picture. This report presents our take on a hypothetical conversation between President Trump and Scott Bessent that led to the latter’s appointment as Treasury secretary.

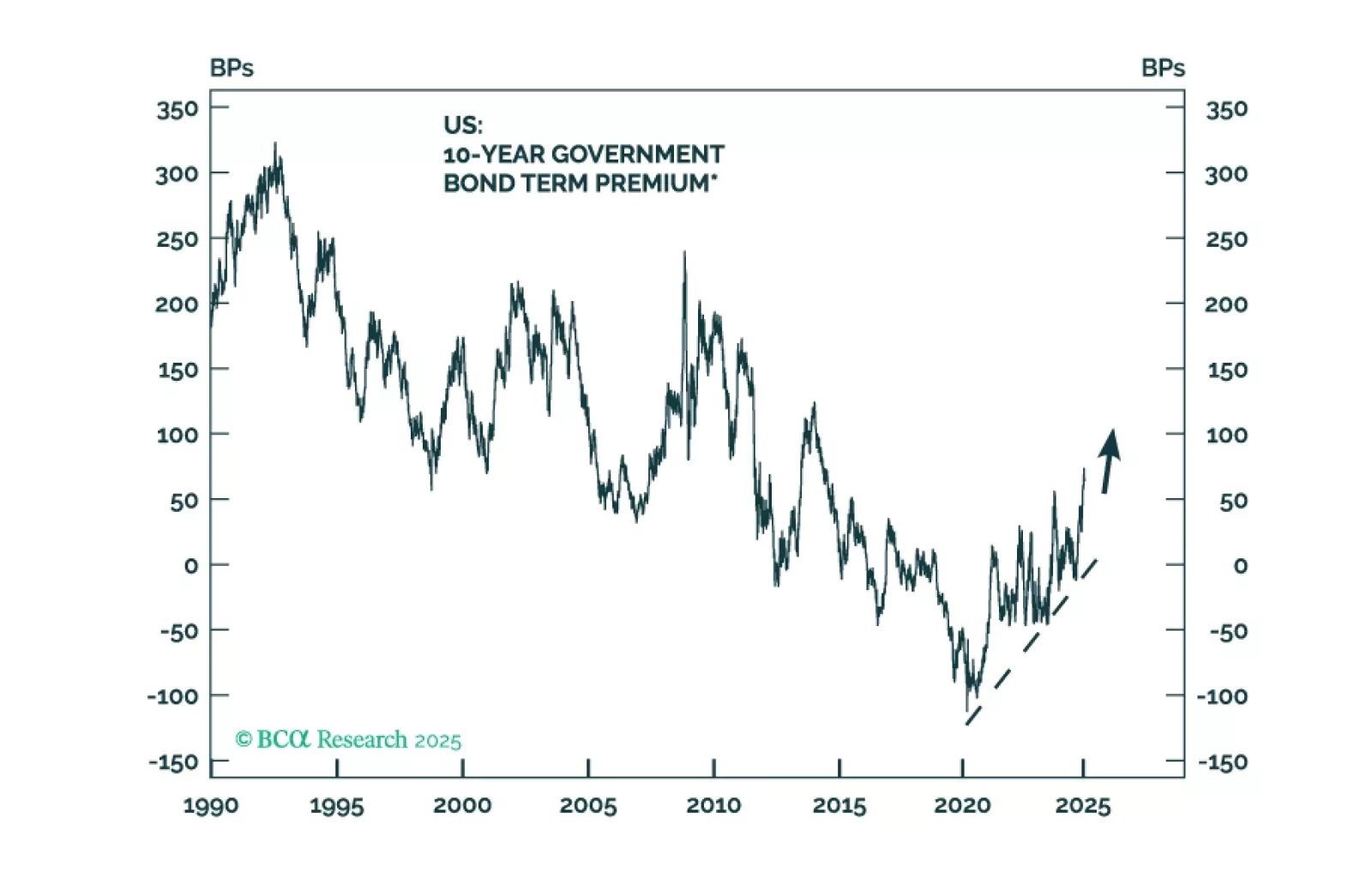

Today, we publish our Quarterly Model Bond Portfolio report. We review the performance of the portfolio in 2024 and discuss how to best position a global fixed income portfolio following the sharp rise in yields during the last months.

Our outlook for Fed policy in 2025 discusses our expectations for interest rates, the Fed’s balance sheet and the 2025 strategic review.

Our thoughts on this afternoon’s Fed decision and the bond market reaction.

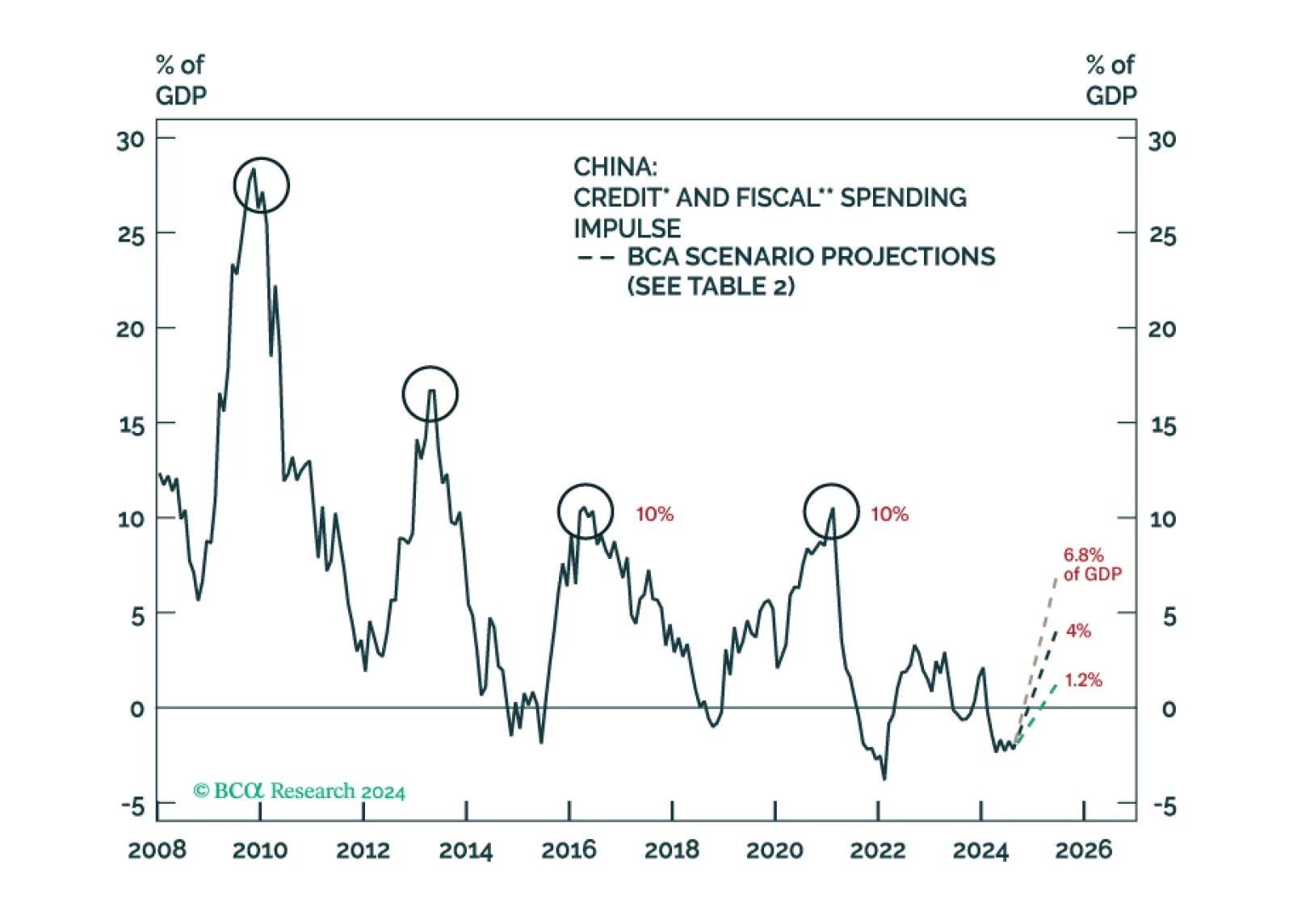

To produce a moderate economic recovery, at least RMB 3 trillion in additional government expenditures is needed in H1 2025. Our bias is that Beijing is not yet ready to launch such a massive fiscal support measure. Hence, volatility-adjusted equity returns in China will be poor.