Monetary Policy

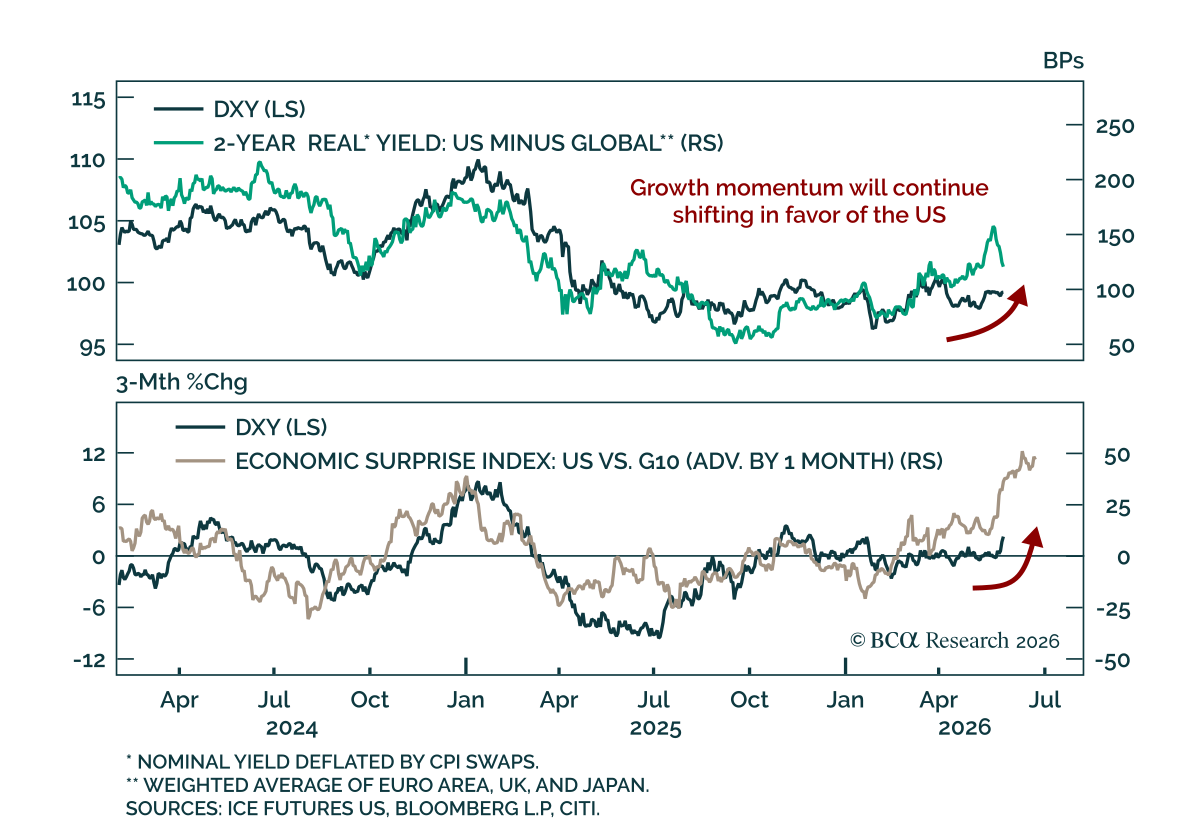

The cyclical outlook for the US dollar is improving and reinforces positioning for further dollar strength in the near term against energy importers. As a net energy exporter, the US economy remains more resilient to the terms-of-trade shock and the risks of…

In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.

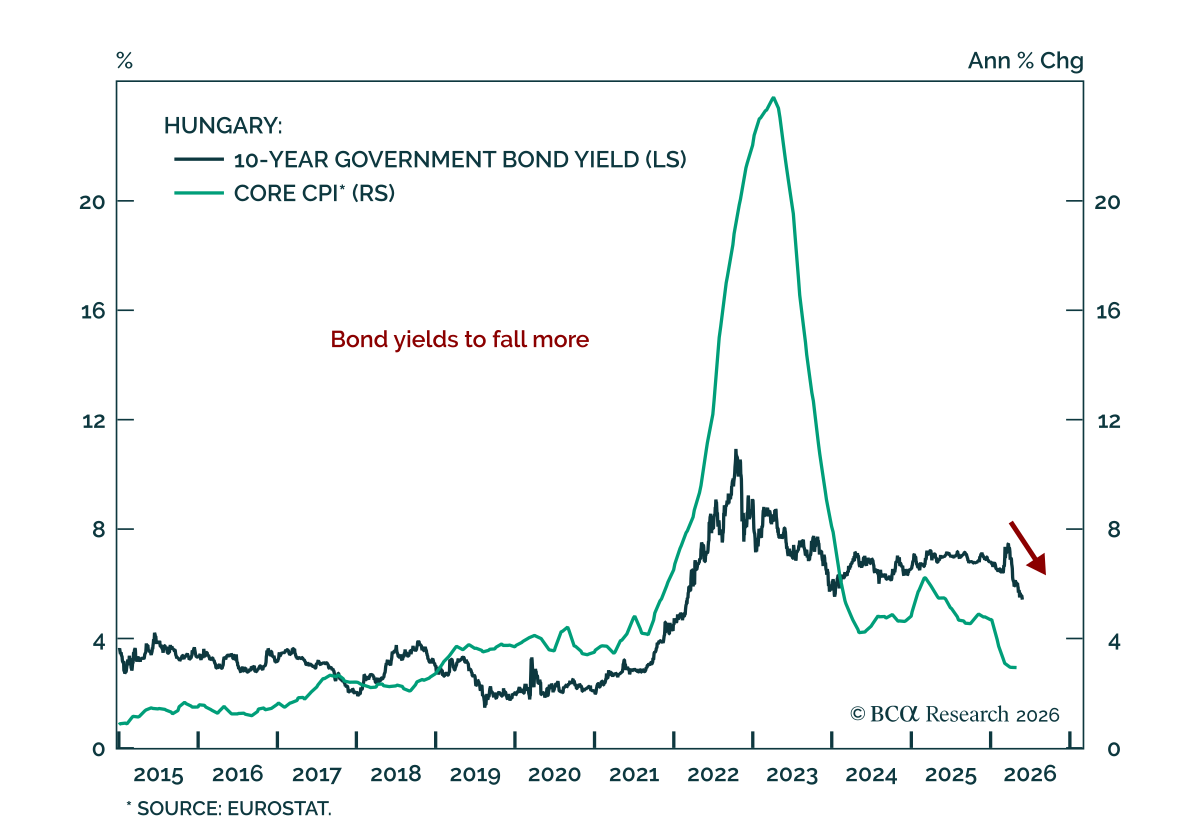

Hungary’s policy mix is turning bond-friendly. The Hungarian National Bank held rates at 6.25%, citing a better inflation outlook supported by a stronger forint and the delayed phaseout of regulated fuel prices. Our EM strategists expect the forint to…

Bank Indonesia raised its policy rate by 50 bps to 5.25% last week, 25 bps above expectations, as a response to persistent rupiah weakness. The recent sell-off in the rupiah and local bonds was partly triggered by the finance minister's plan to spend an…

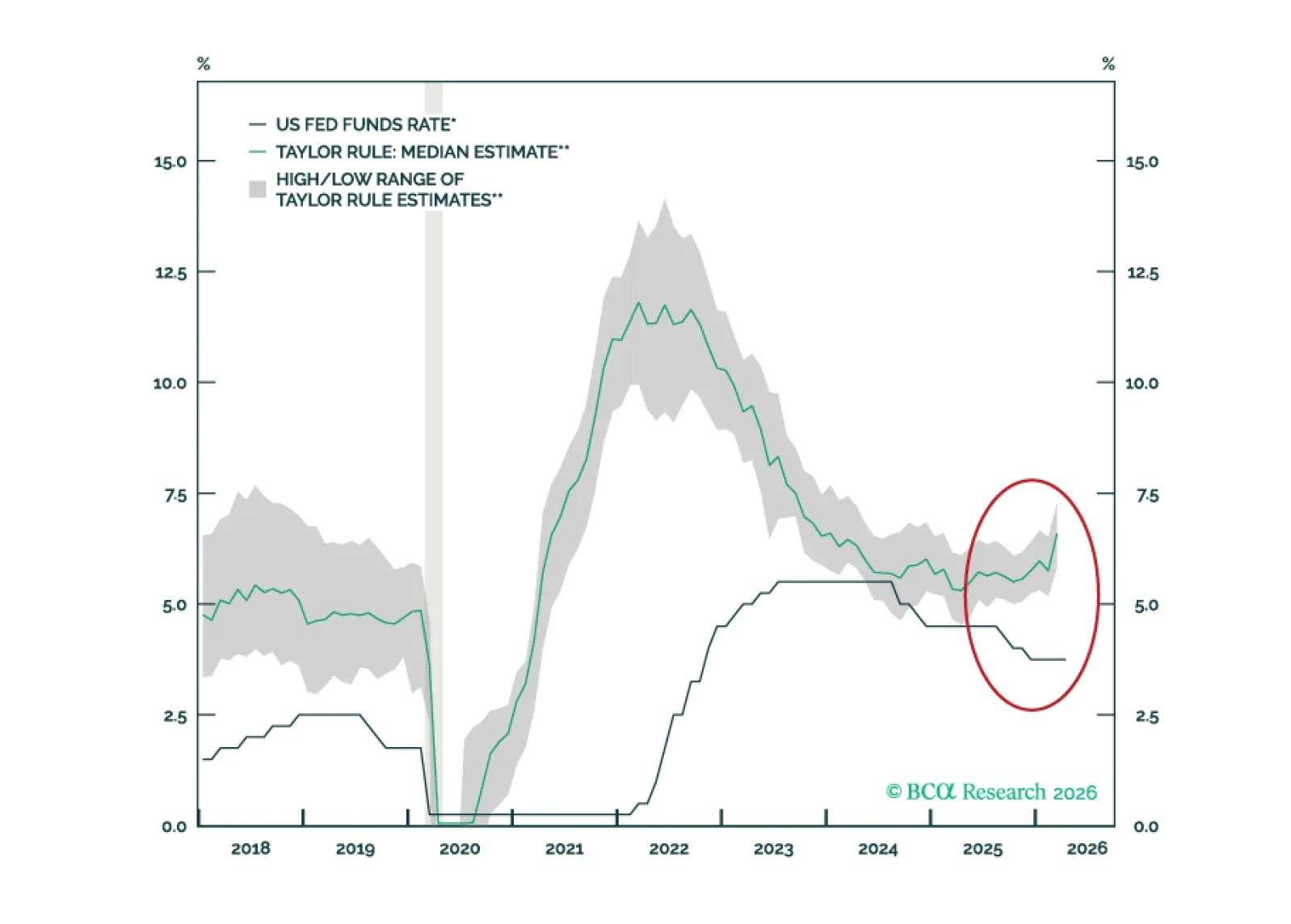

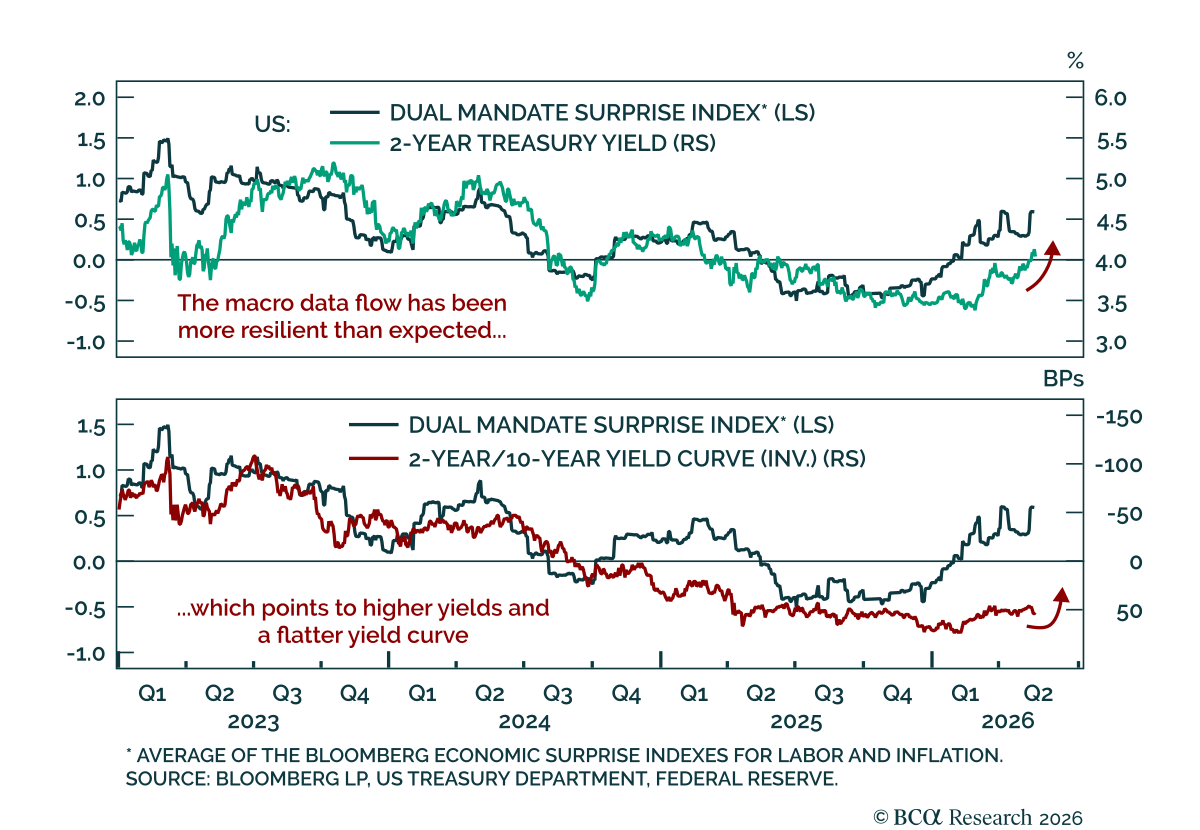

The April FOMC minutes clarified the hawkish shift that marked the meeting. The Fed held at its last meeting, but there were four dissents. While Governor Miran favored a 25 bps cut, regional presidents Hammack, Kashkari, and Logan supported a hold but voted…

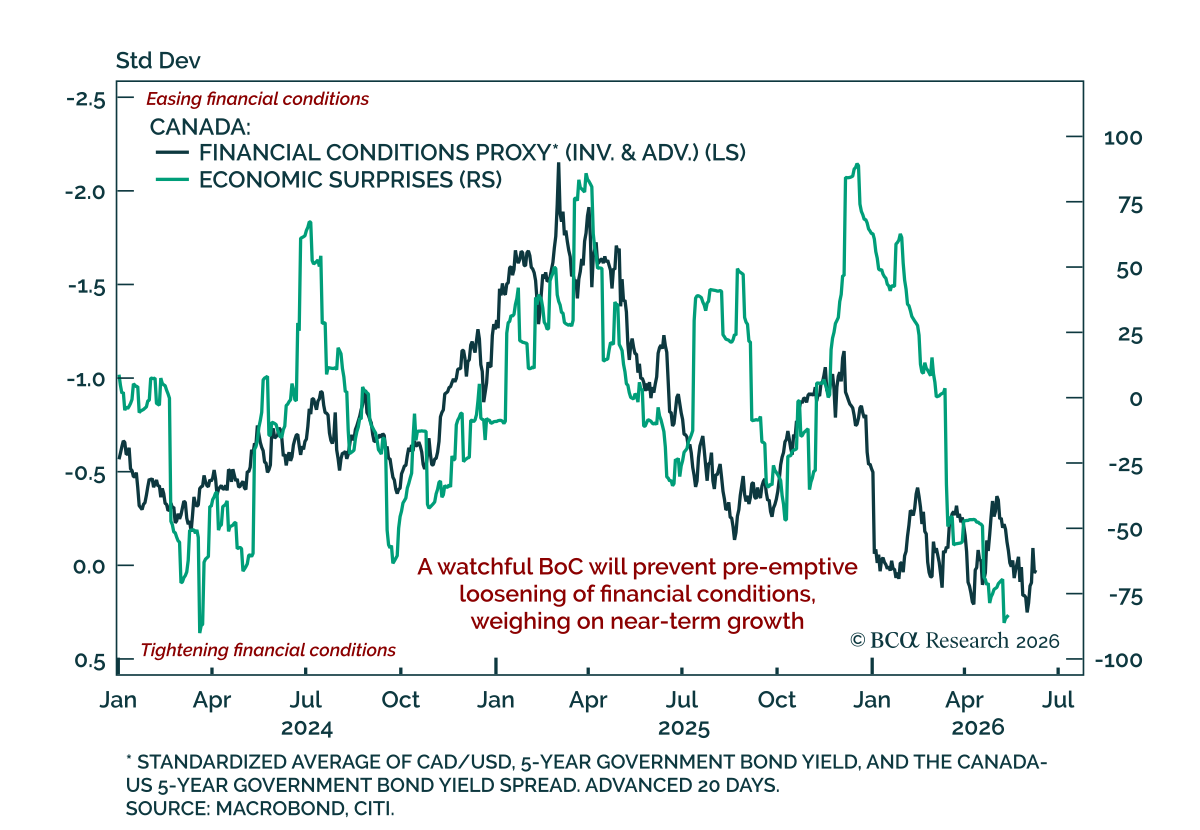

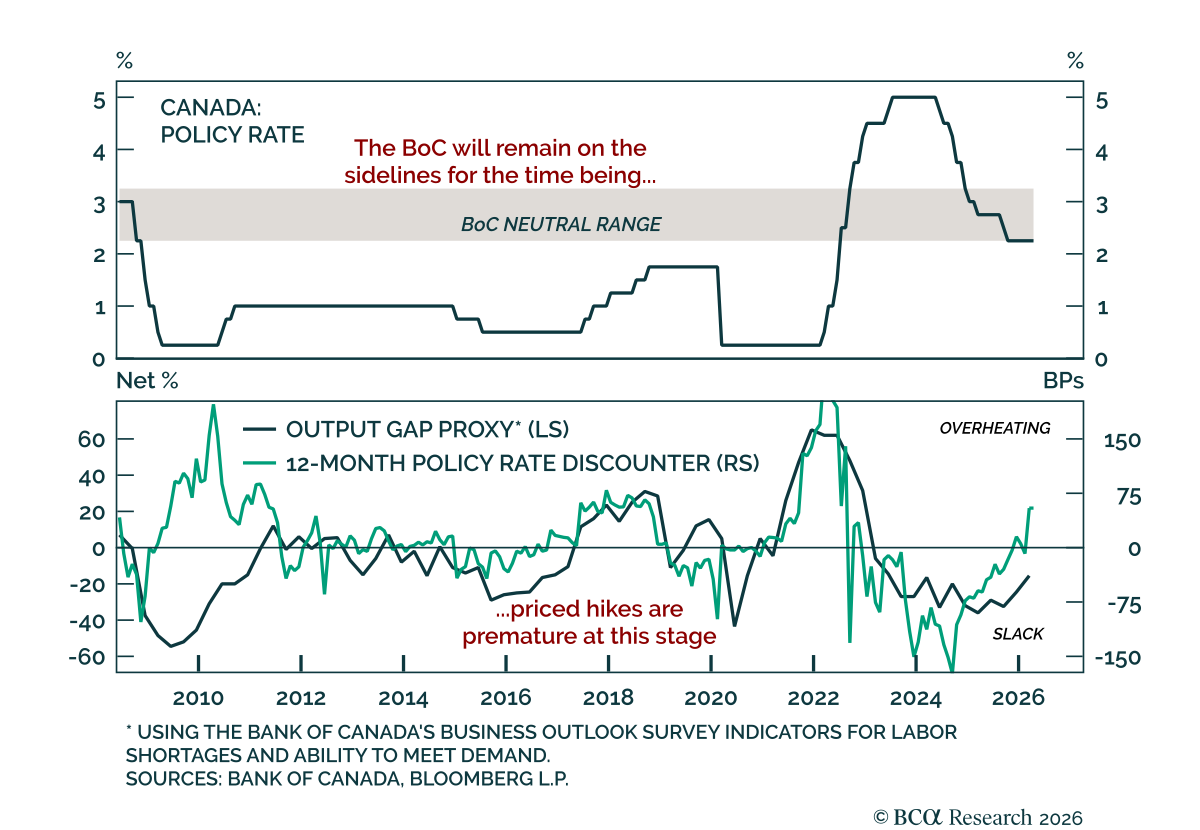

Canada’s data keep disappointing, and stable but still-restrictive financial conditions point to subdued growth ahead. As we recently highlighted, Canadian economic surprises turned negative earlier this year and have kept falling. Canada also faces several…

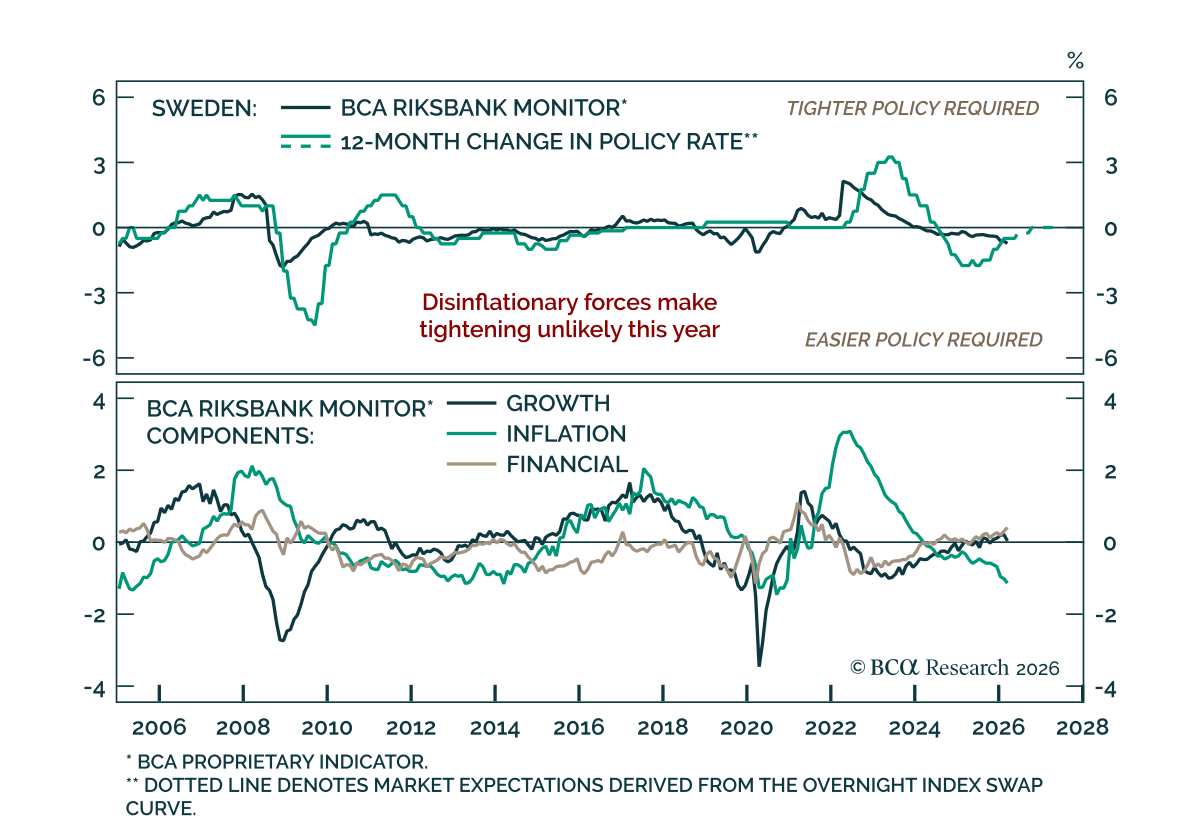

The Riksbank left rates unchanged and is likely to stay on hold, as soft inflation and weaker growth leave little case for tightening. The policy rate was left at 1.75%, as expected, and the Riksbank signaled it will remain on hold in the near term. This…

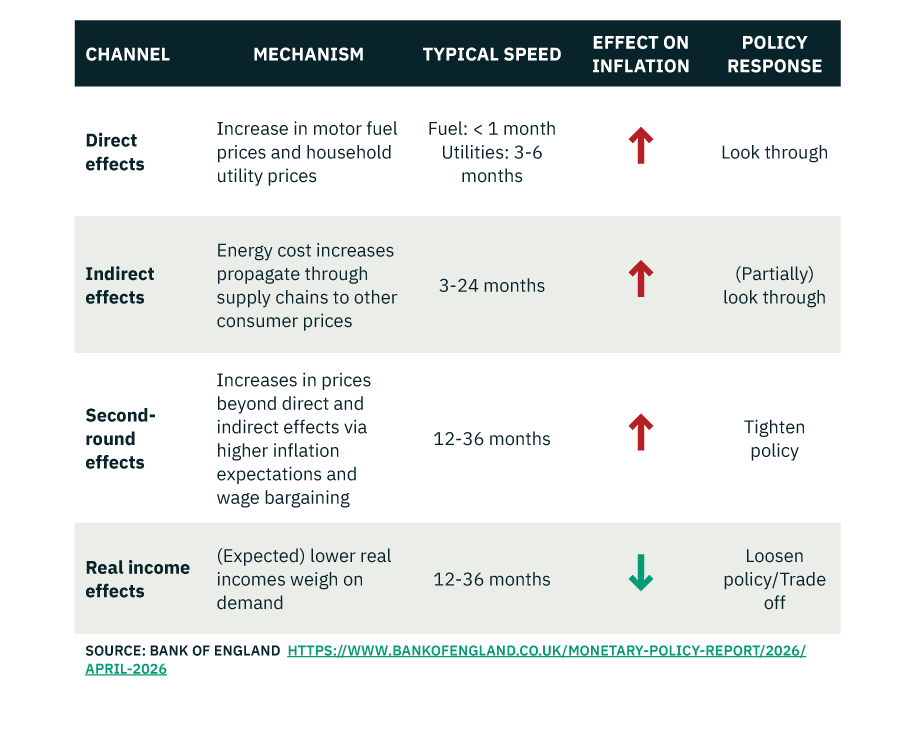

The Bank of England’s latest Monetary Policy Report offers a clean framework for thinking through an oil shock and the appropriate policy response. The first channel is the direct effect of higher energy prices on inflation such as higher gas and utilities…

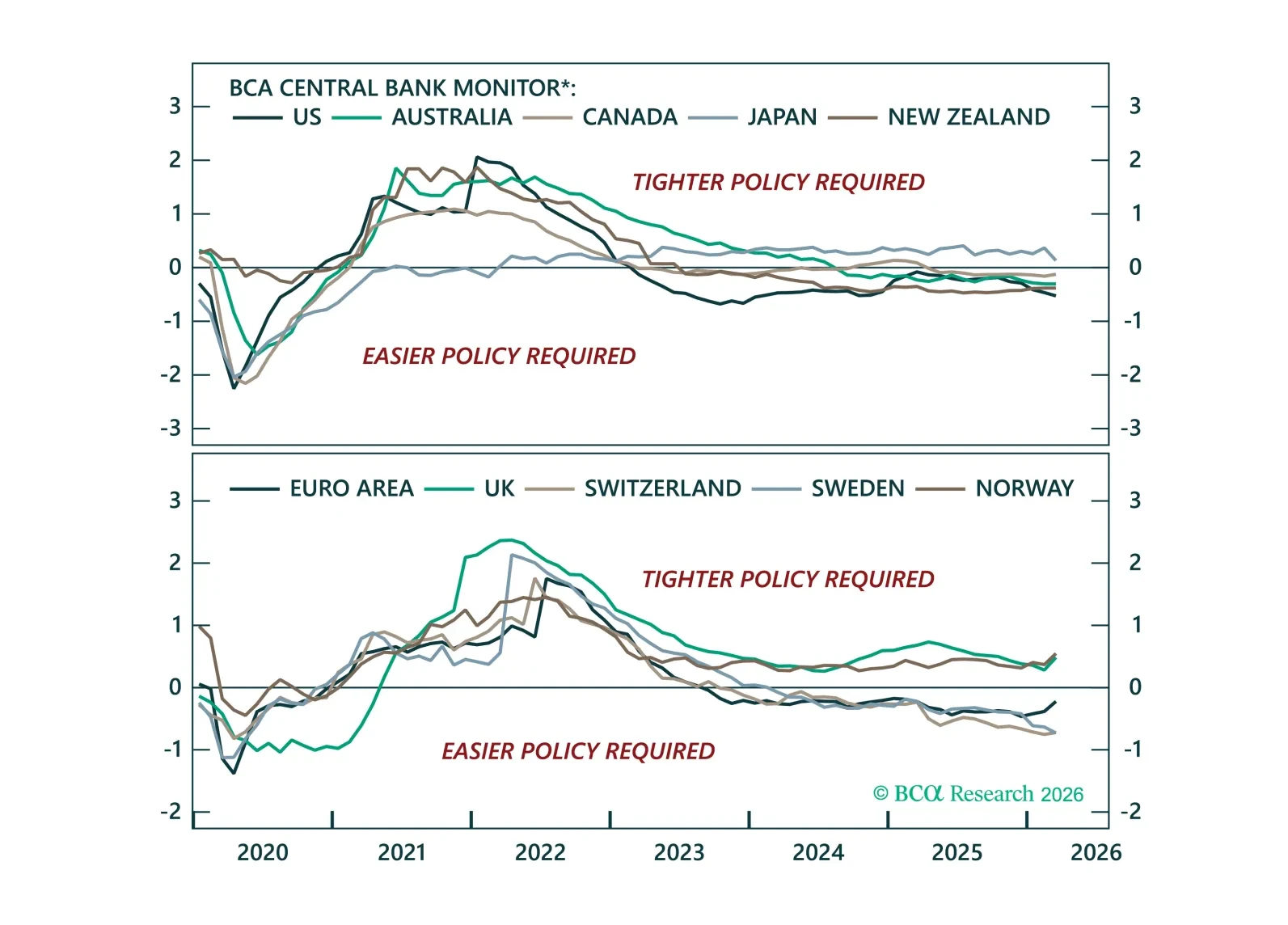

Central banks remain on hold amid heightened uncertainty. We rely on BCA’s Central Bank Monitors to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

The Bank of Canada held rates at 2.25% for a fourth consecutive meeting; a weak domestic economy still argues for looking through supply-side inflation. The hold was expected, and at 2.25%, the policy rate sits at the bottom of the BoC’s estimated 2.25%-3.25%…