Monetary Policy

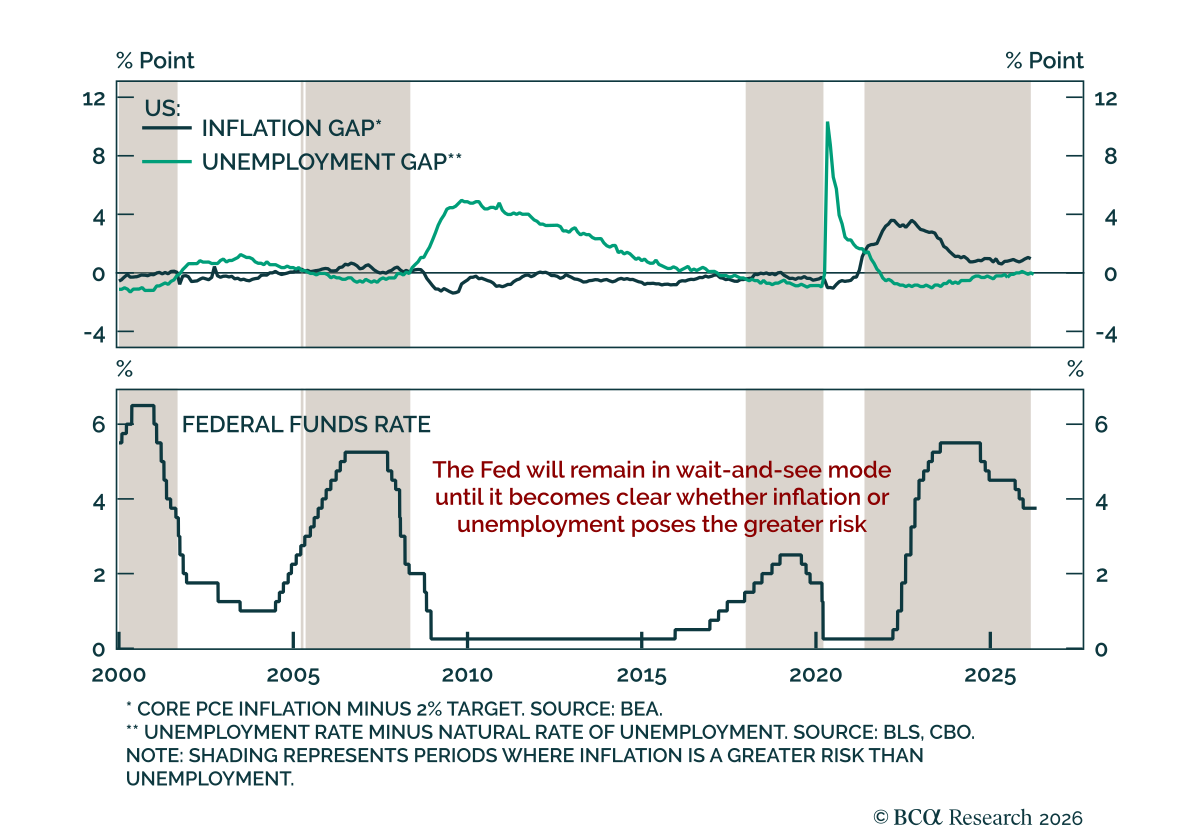

The Fed held rates for a third consecutive meeting and signaled no urgency to cut. The Fed left rates at 3.5-3.75%, with a 8-4 vote in favor of the relatively unchanged statement. Dissents were two-sided, with Governor Miran favoring a 25 bps cut, and…

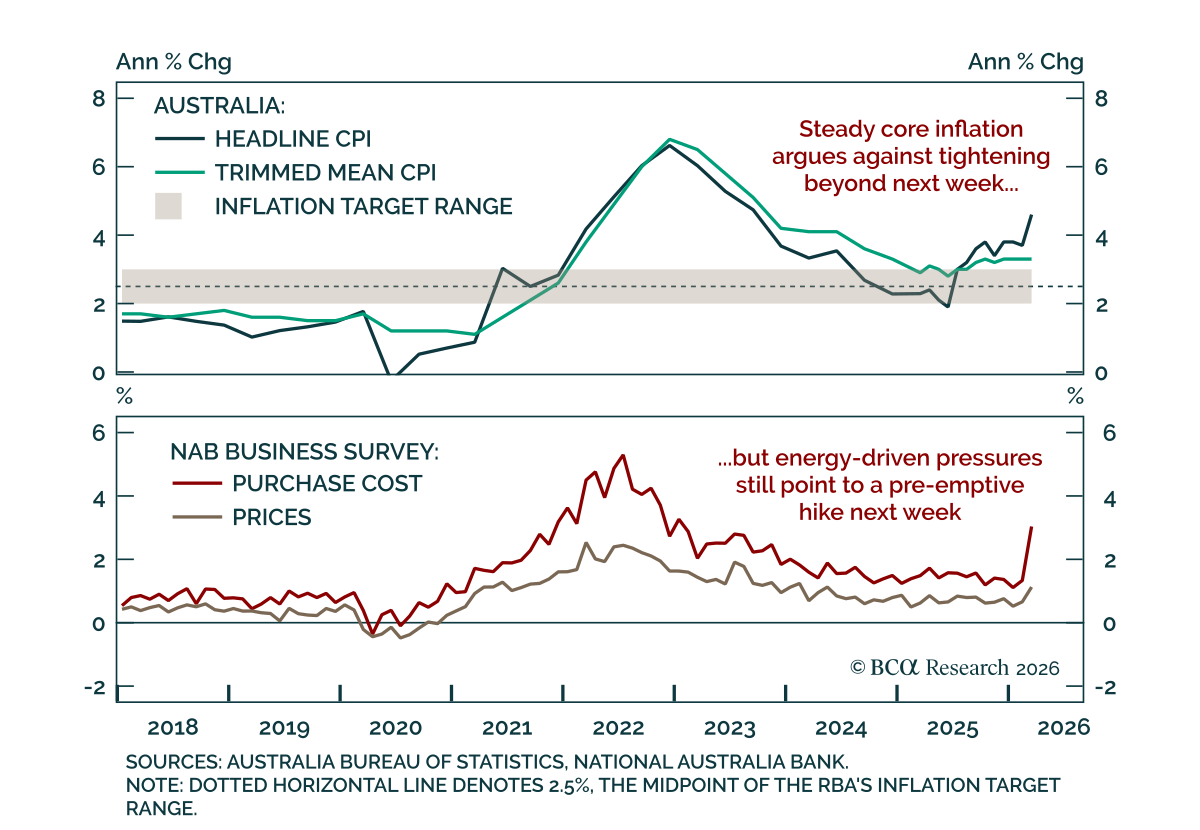

Australia's Q1 CPI showed energy-driven headline acceleration, but steady core inflation suggests markets are over-pricing RBA tightening. Headline inflation accelerated to 4.1% y/y (1.4% q/q) from 3.6% (0.6%), while the trimmed mean was largely unchanged at…

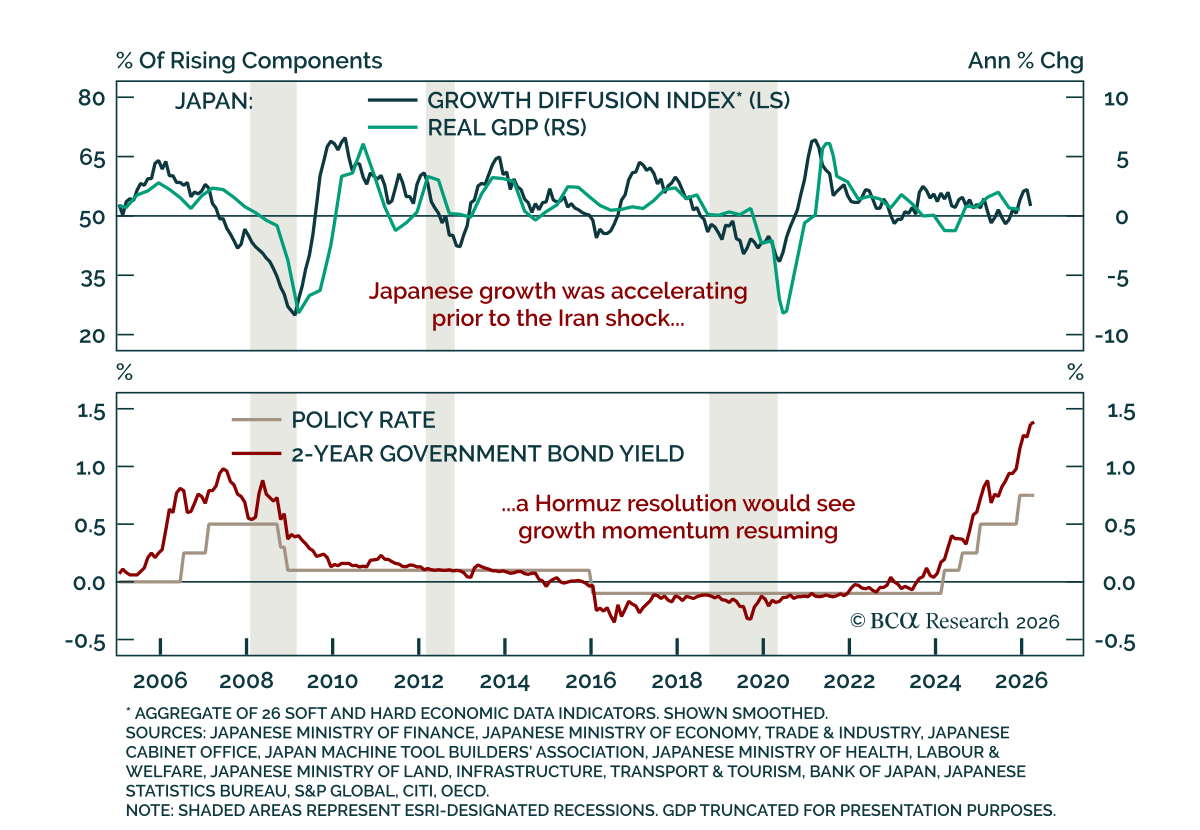

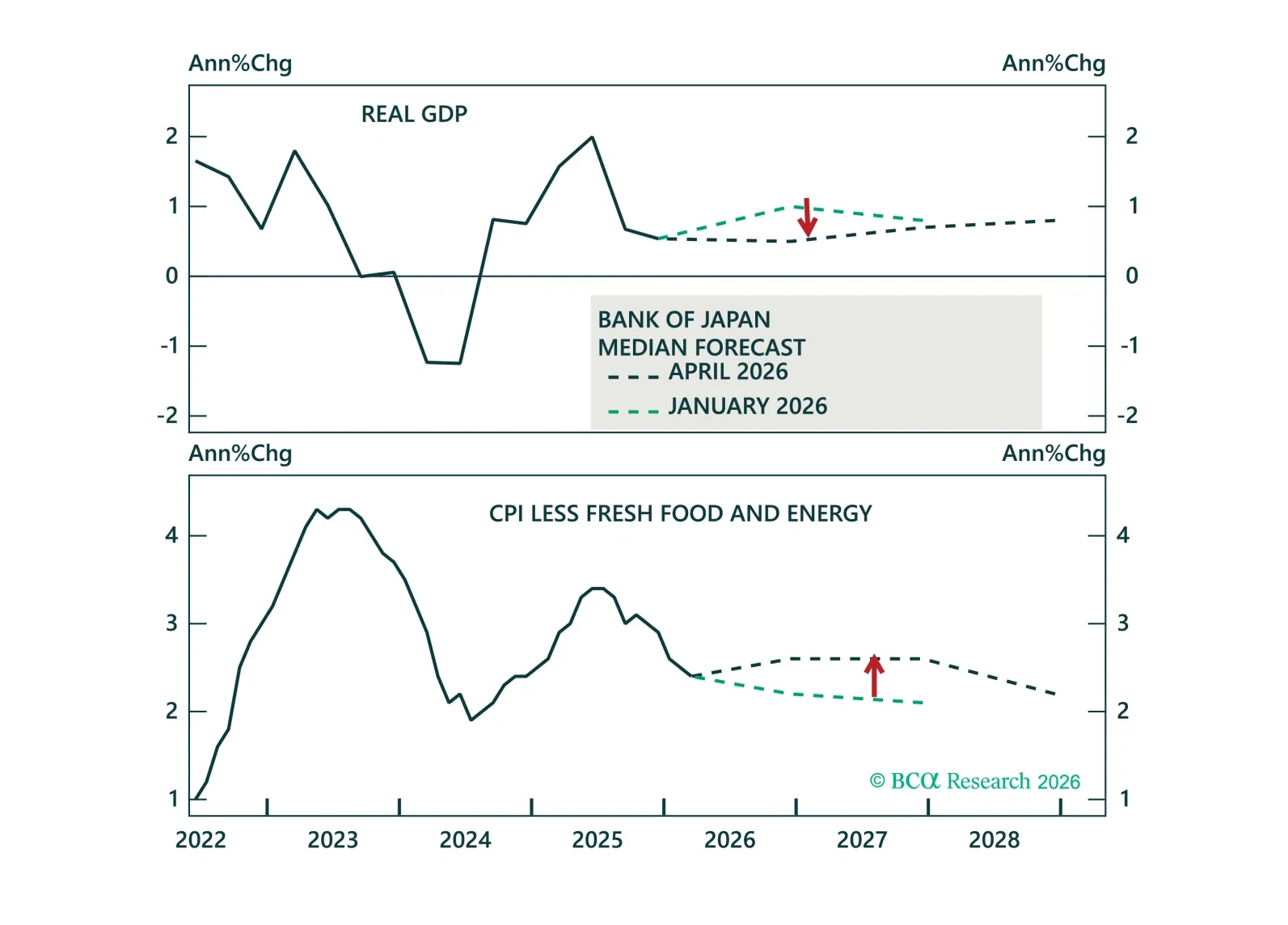

The Bank of Japan held rates at 0.75%, but the meeting still leaned hawkish. The hold was expected, but had a hawkish tone with 3 dissents in favor of a hike. That signal came alongside upward revisions to the BoJ’s inflation forecasts for 2026 and 2027, and…

The BoJ held rates overnight, but the direction of travel hasn’t changed. We discuss how stronger wages, rising inflation, and a weak yen point to further tightening ahead.

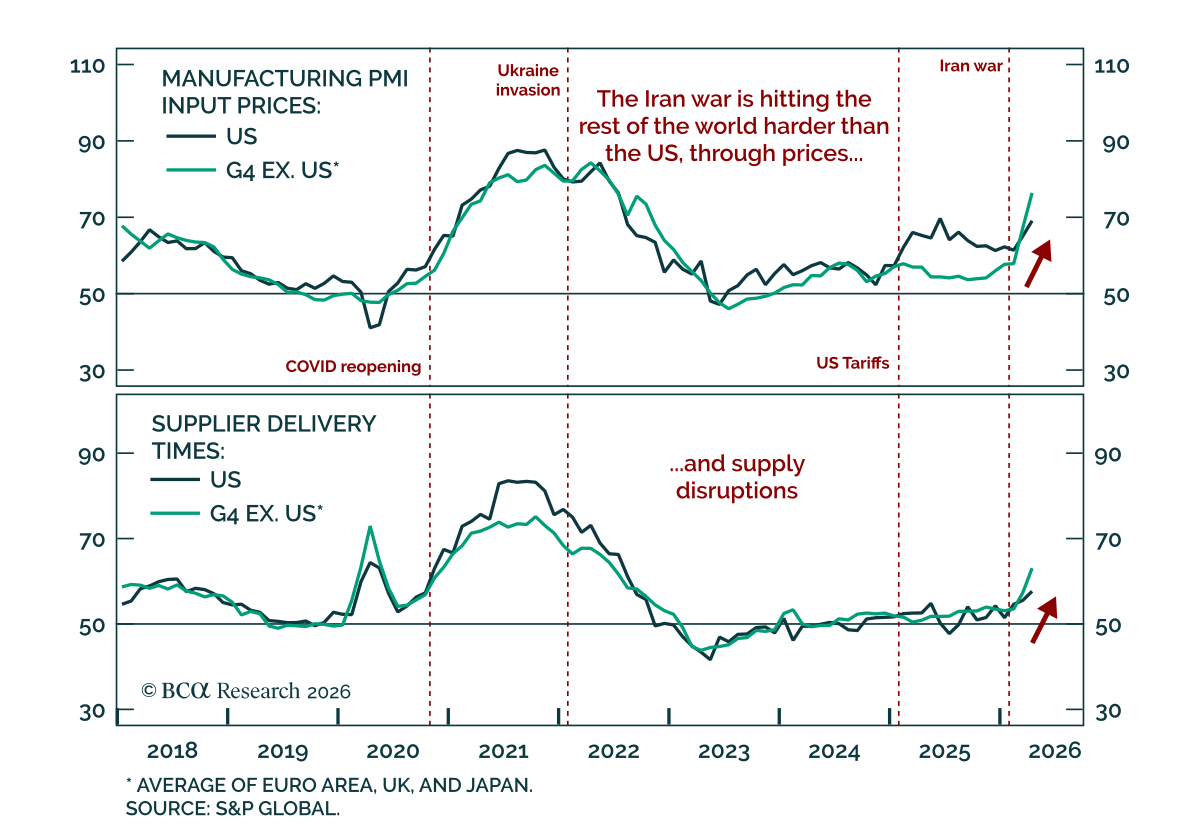

The April flash PMIs show that the global energy shock is feeding through unevenly, with sharper price pressures outside the US. Longer delivery times were widespread across developed markets, and input prices rose. One of our most timely tools for tracking…

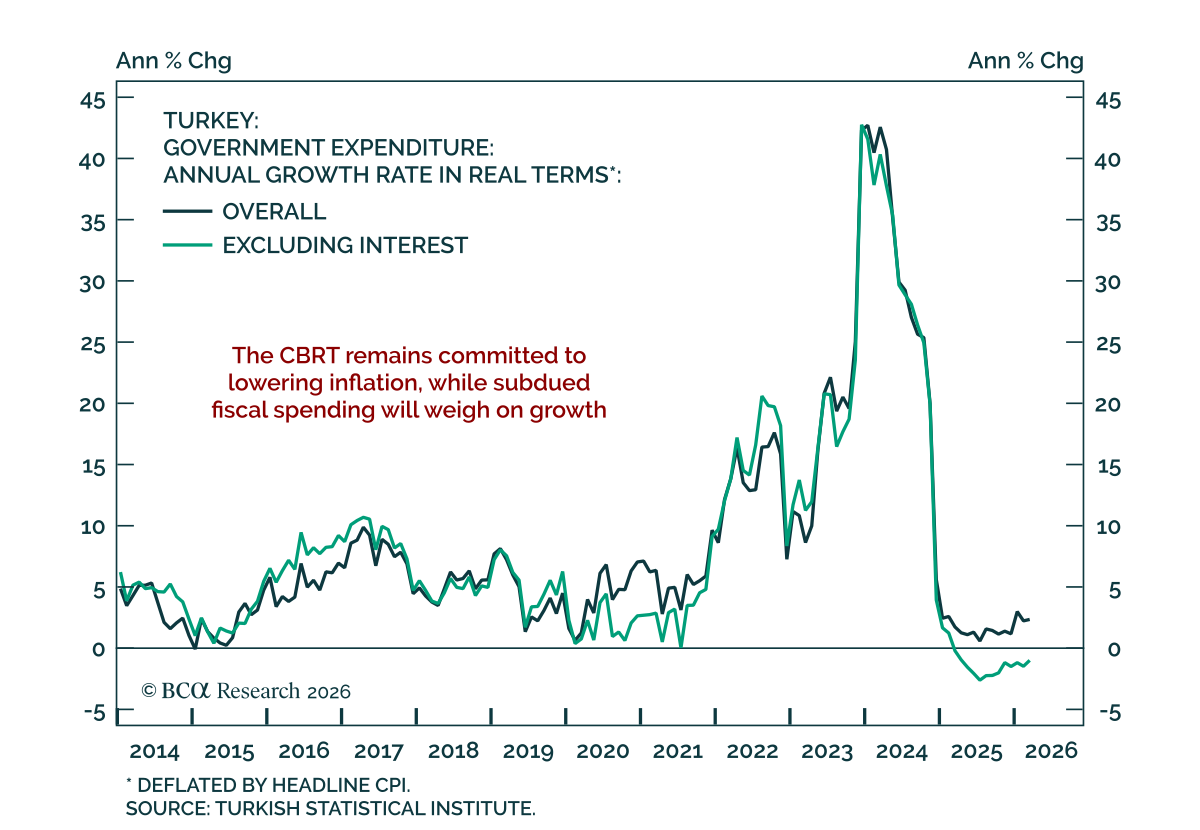

The Turkish Central Bank held rates at 37% this week, in line with expectations. While the energy shock may halt disinflation and delay near-term CBRT easing, the structural background remains disinflationary. An easing pause coupled with a slowing domestic…

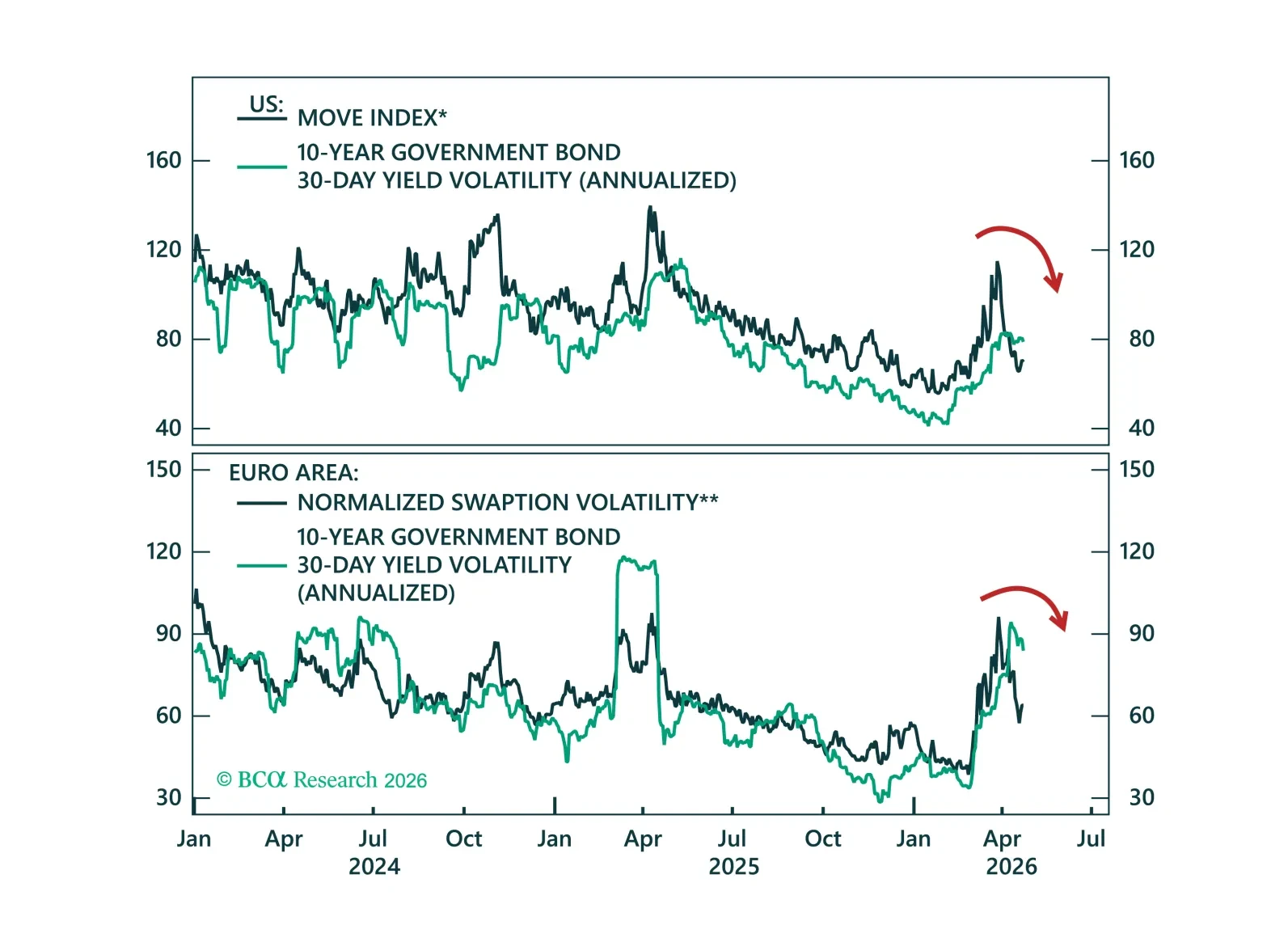

With central banks largely on hold, the return of a lower volatility environment is bringing carry trades back into focus. We outline the most attractive carry opportunities across global fixed income markets.

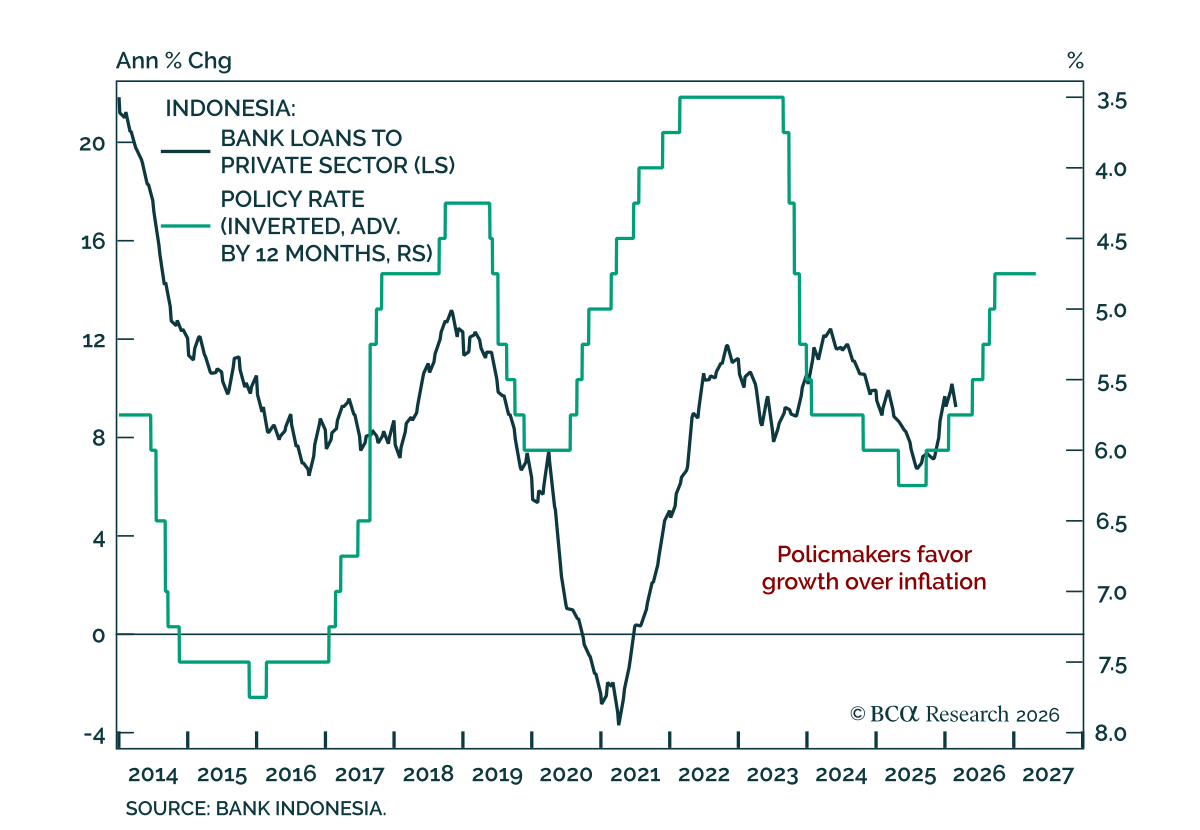

Indonesia’s policy mix remains negative for the rupiah and local fixed income. The central bank kept rates unchanged at 4.75%, in line with expectations and with our Emerging Markets strategists’ view that authorities remain unwilling to tighten policy…

Kevin Warsh’s confirmation hearing focused on how he would conduct policy, not on committing to a specific policy path. While the Fed Chair nominee avoided committing to a specific rate path, some of his comments on the conduct of policy are worth…

Fed Governor Waller’s latest speech suggests the FOMC’s dovish wing is moving away from the case for cuts. While Waller was one of the most dovish members before the energy shock, his tenure has been marked by prescience at key inflection points on both the…