Monetary Policy

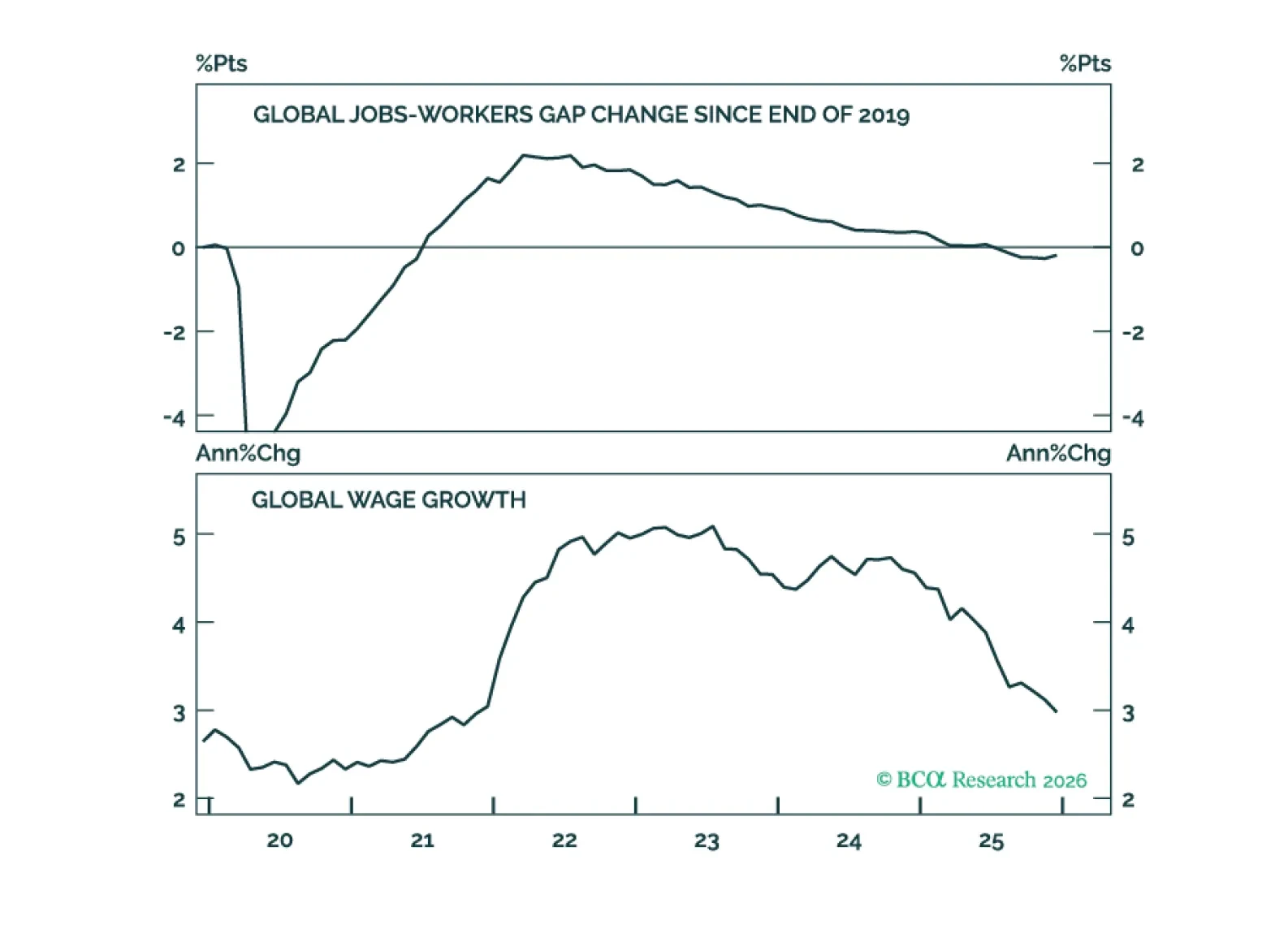

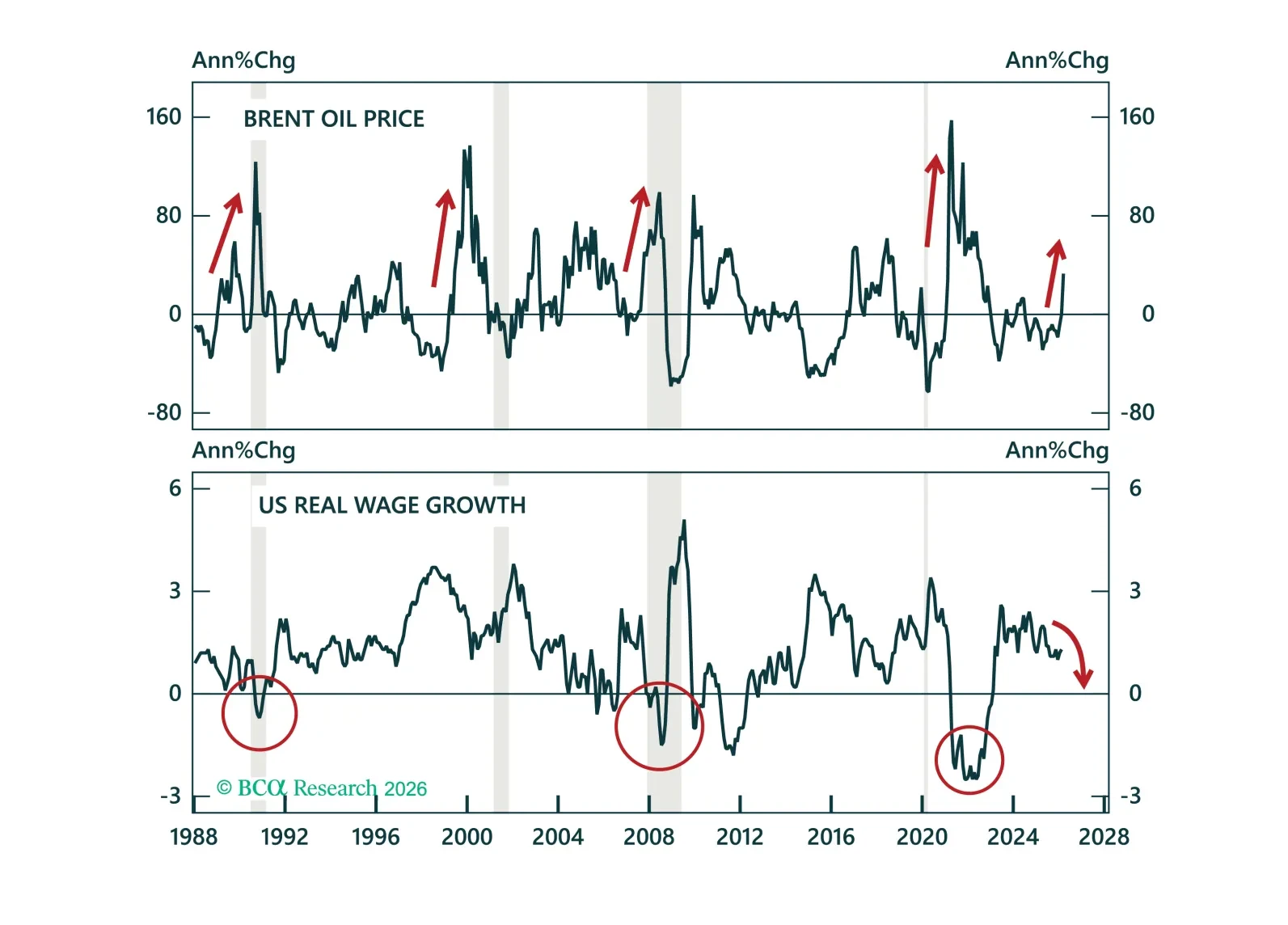

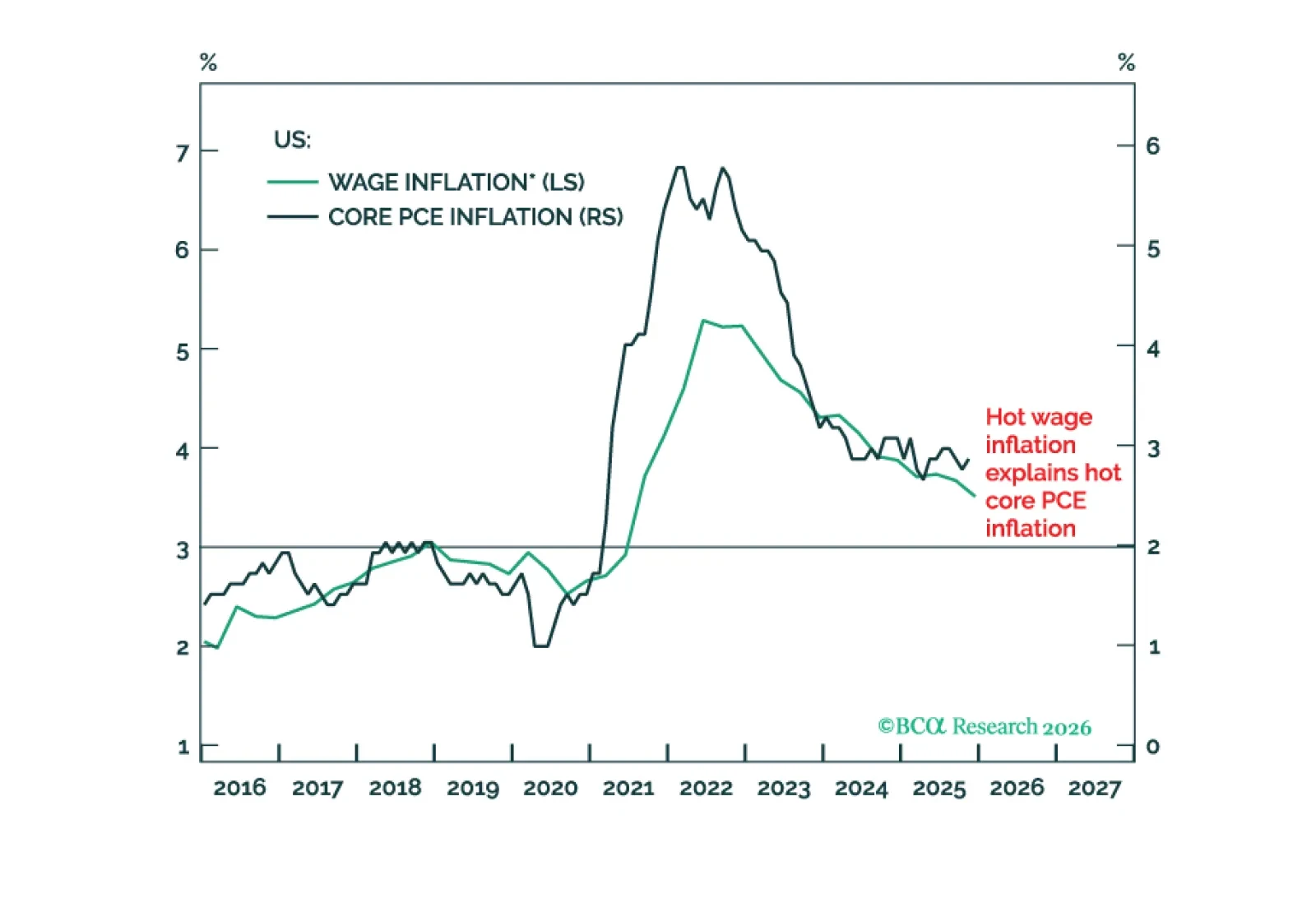

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.

In today’s Strategy Insight, we show why both a quick resolution and a prolonged crisis ultimately point to lower yields.

We discuss the takeaways from this week’s central bank meetings amidst the unfolding energy price shock.

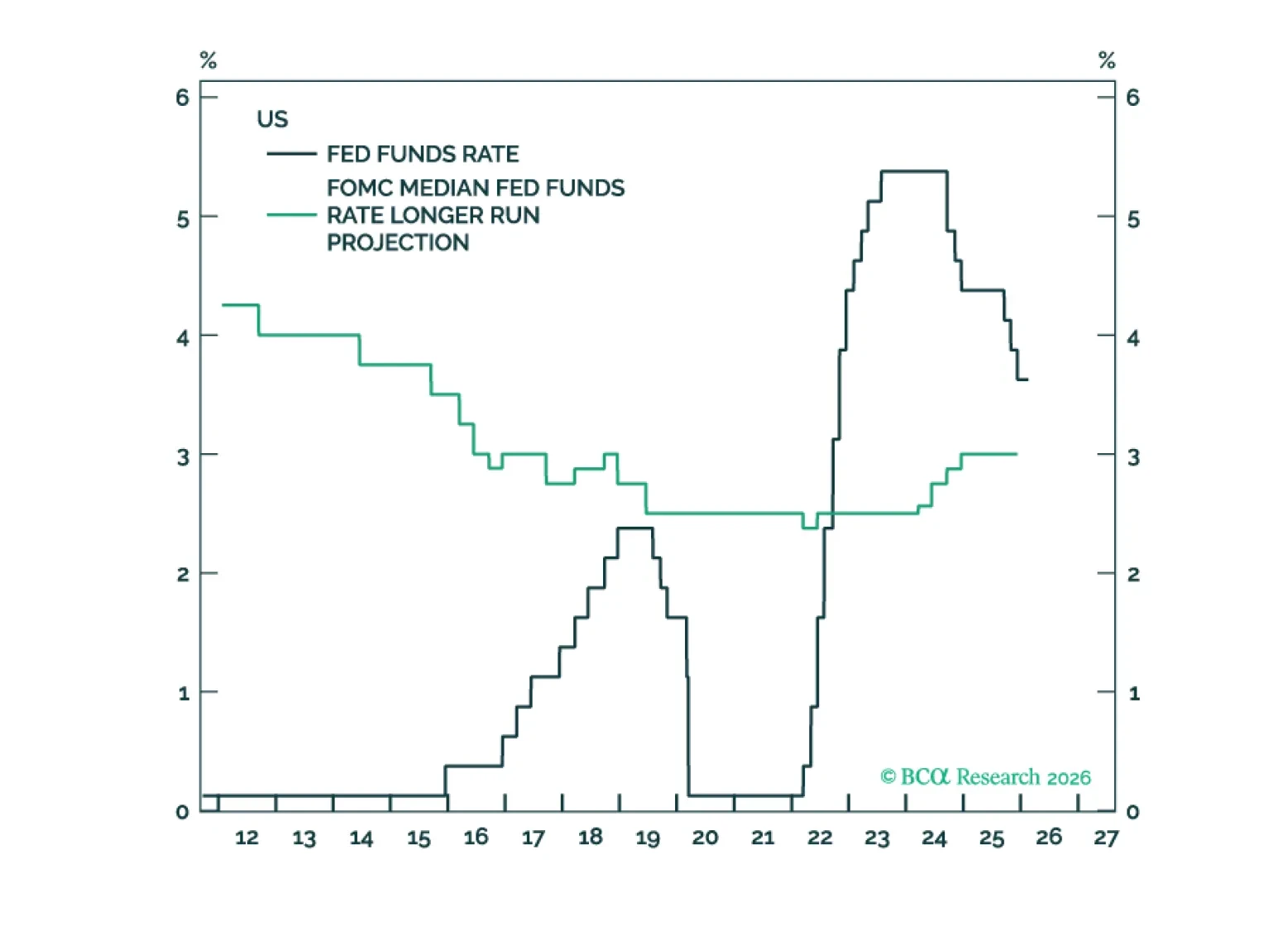

The Fed will not cut rates again until core inflation trends lower. This remains likely as the tariff impact on goods inflation wanes, but the recent energy price shock could delay any meaningful downtrend.

The neutral rate in the US is being propped up by a variety of forces that are at risk of reversing. These include the AI capex boom, large budget deficits, and the extraordinarily high level of household wealth. As such, interest rates are likely to surprise to the downside over the next few years.

The Warsh Fed will run the US economy hot. This is bad for T-bonds and the dollar, but good for stocks. Plus, a new tactical trade is overweight Consumer Discretionary (RXI) versus Industrials (EXI).

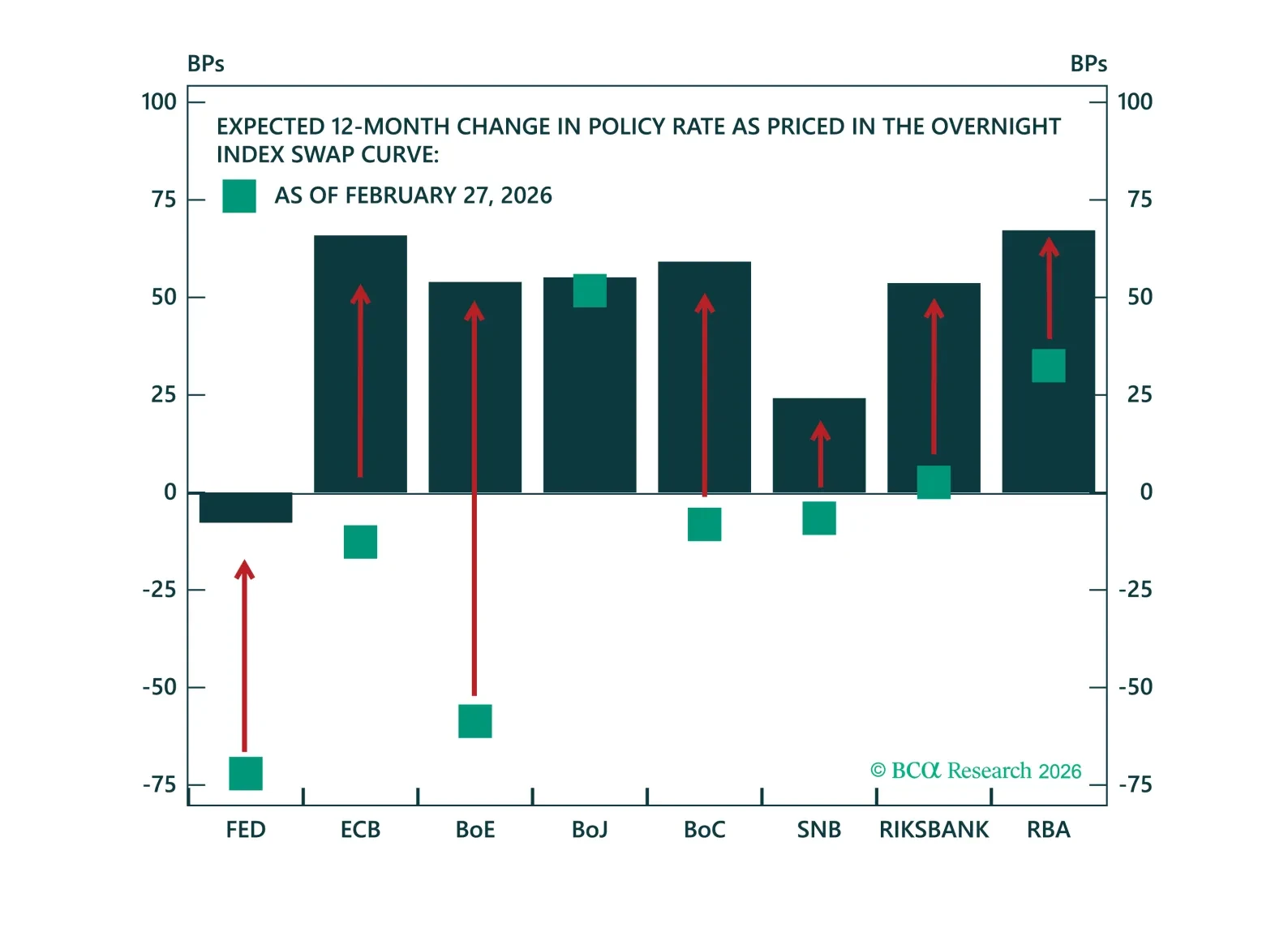

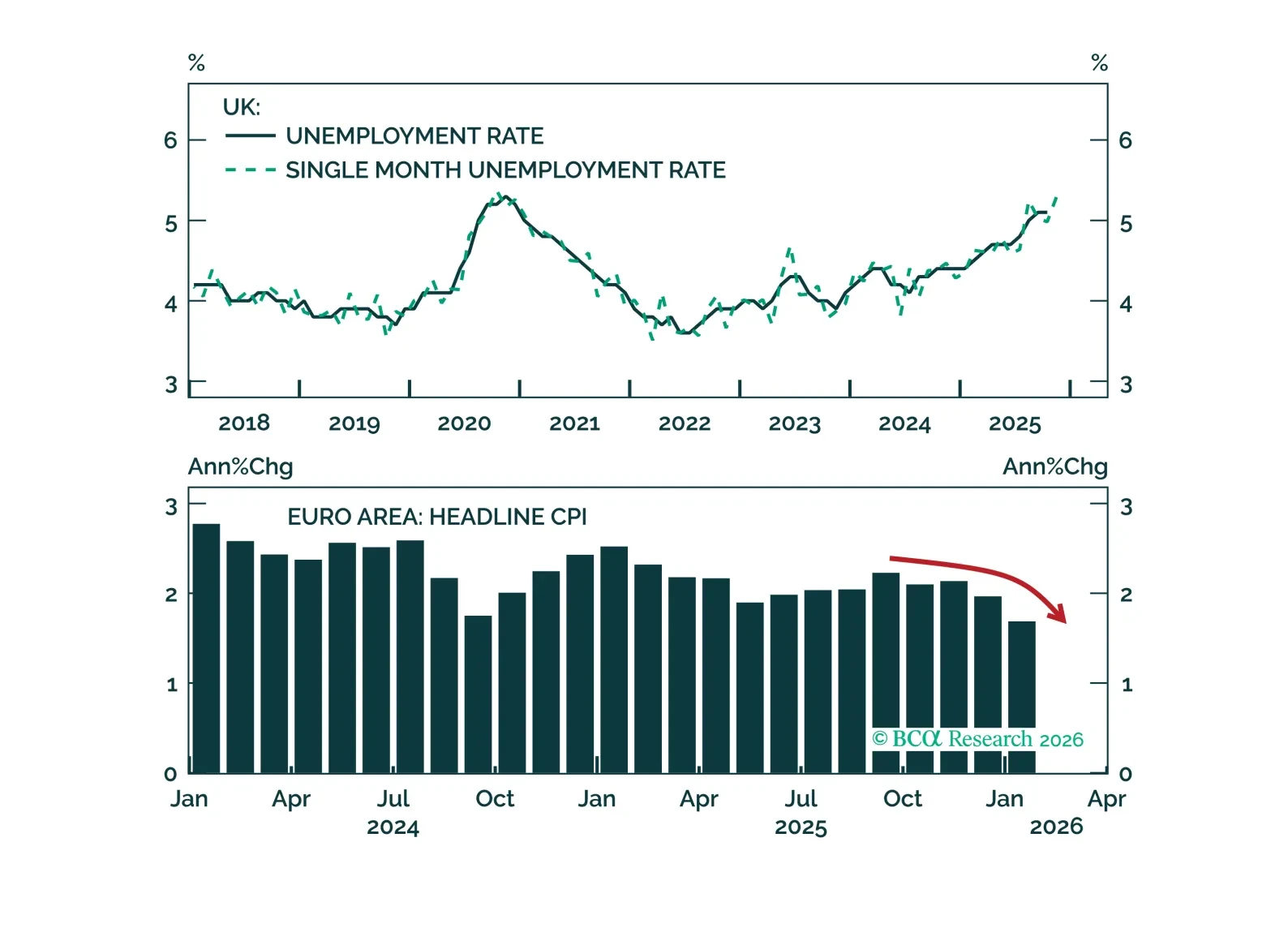

This week’s central bank meetings are a good reminder that monetary policy can still surprise. The Bank of England sounded more dovish, and the European Central Bank sounded complacent about the inflation undershoot. Meanwhile, the Reserve Bank of Australia hiked rates earlier this week. Investors should remain overweight UK Gilts, position for more ECB easing by going long the September 2026 3-month Euribor futures, and fade further rate hikes priced in Australia.

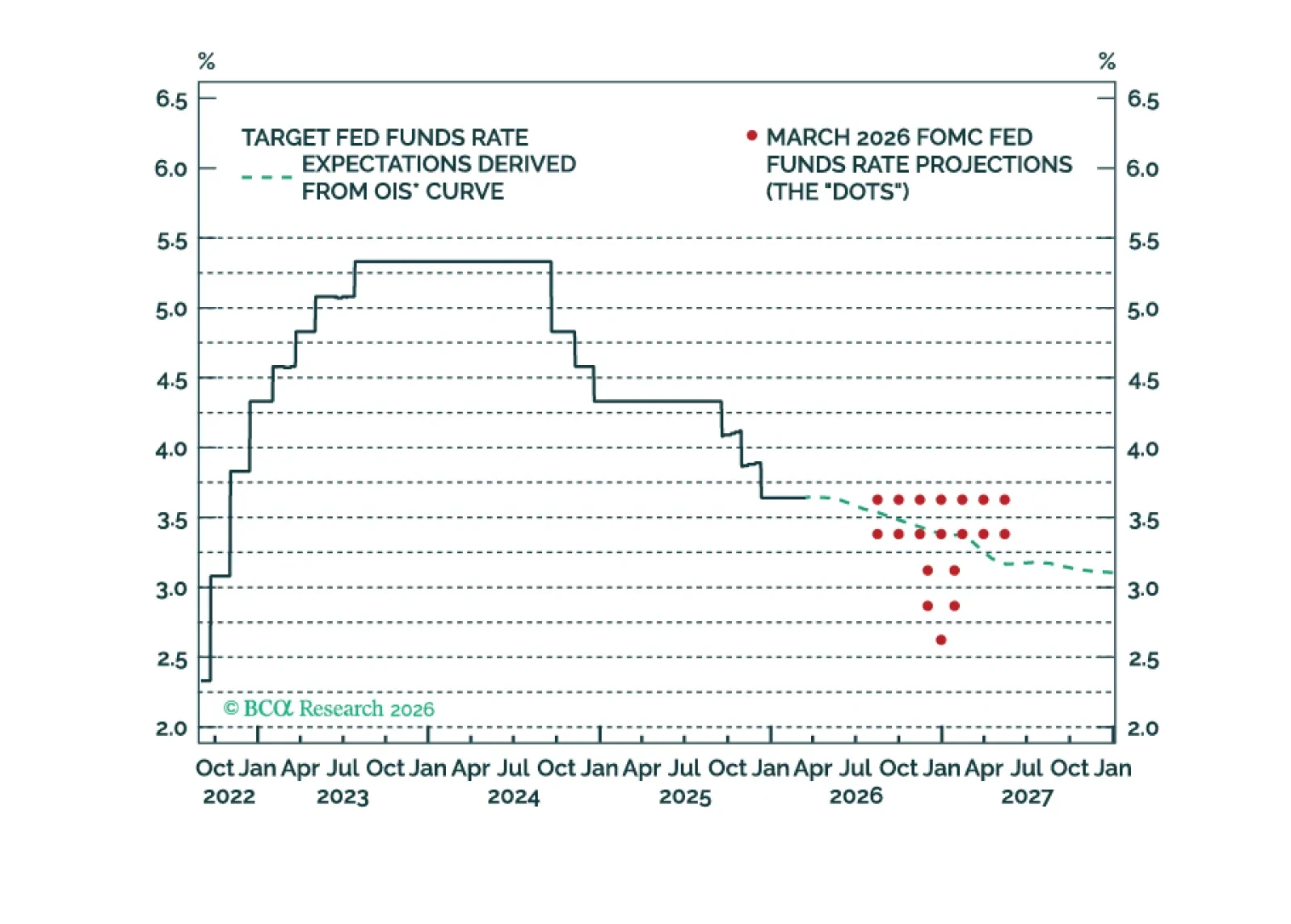

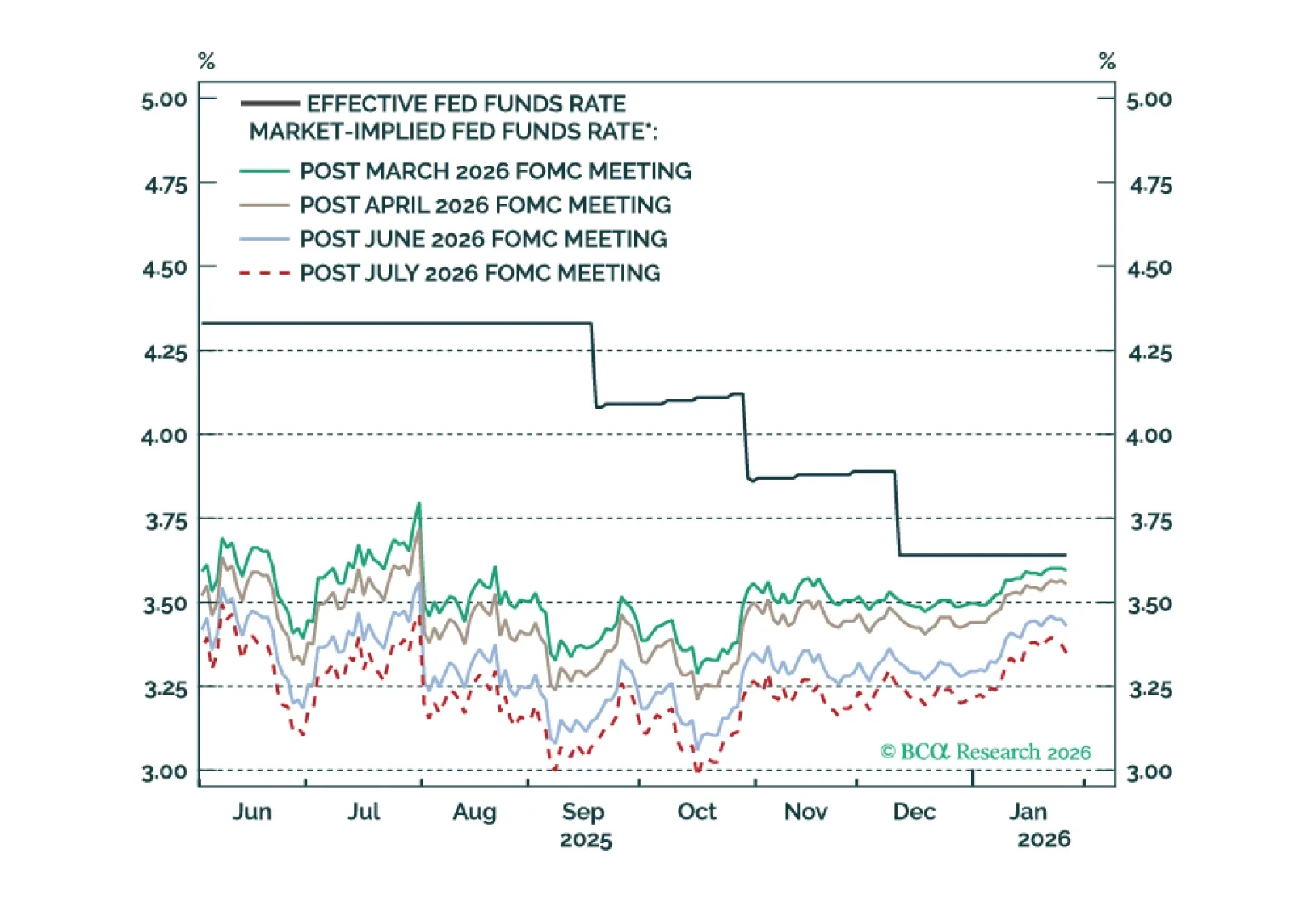

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

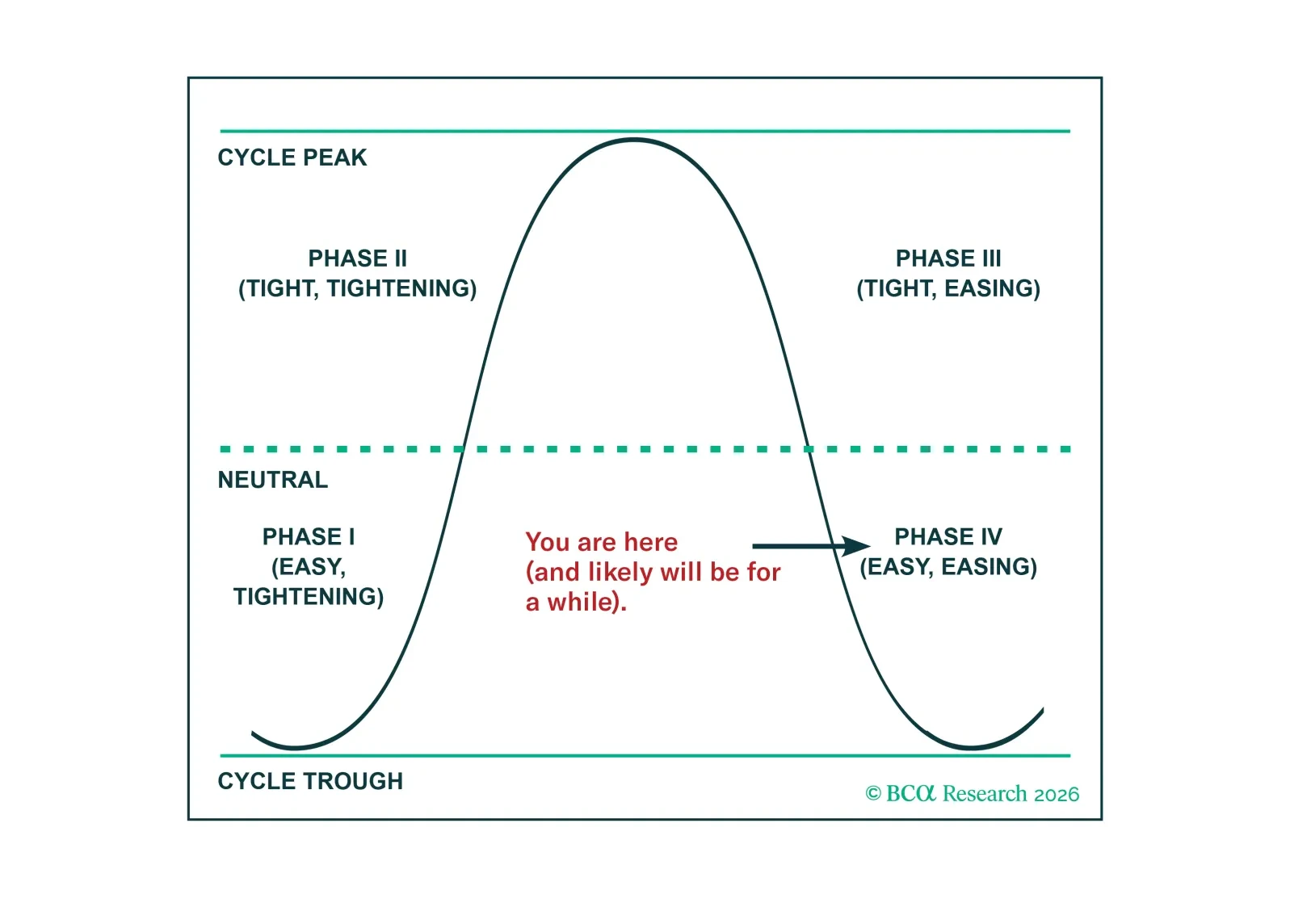

With the Fed looming larger on investors’ radar screens, we revisit our fed funds rate cycle analysis. We expect that the current easing-while-already-easy phase will be less rewarding than normal for the S&P 500 because multiples have already expanded to very elevated levels.

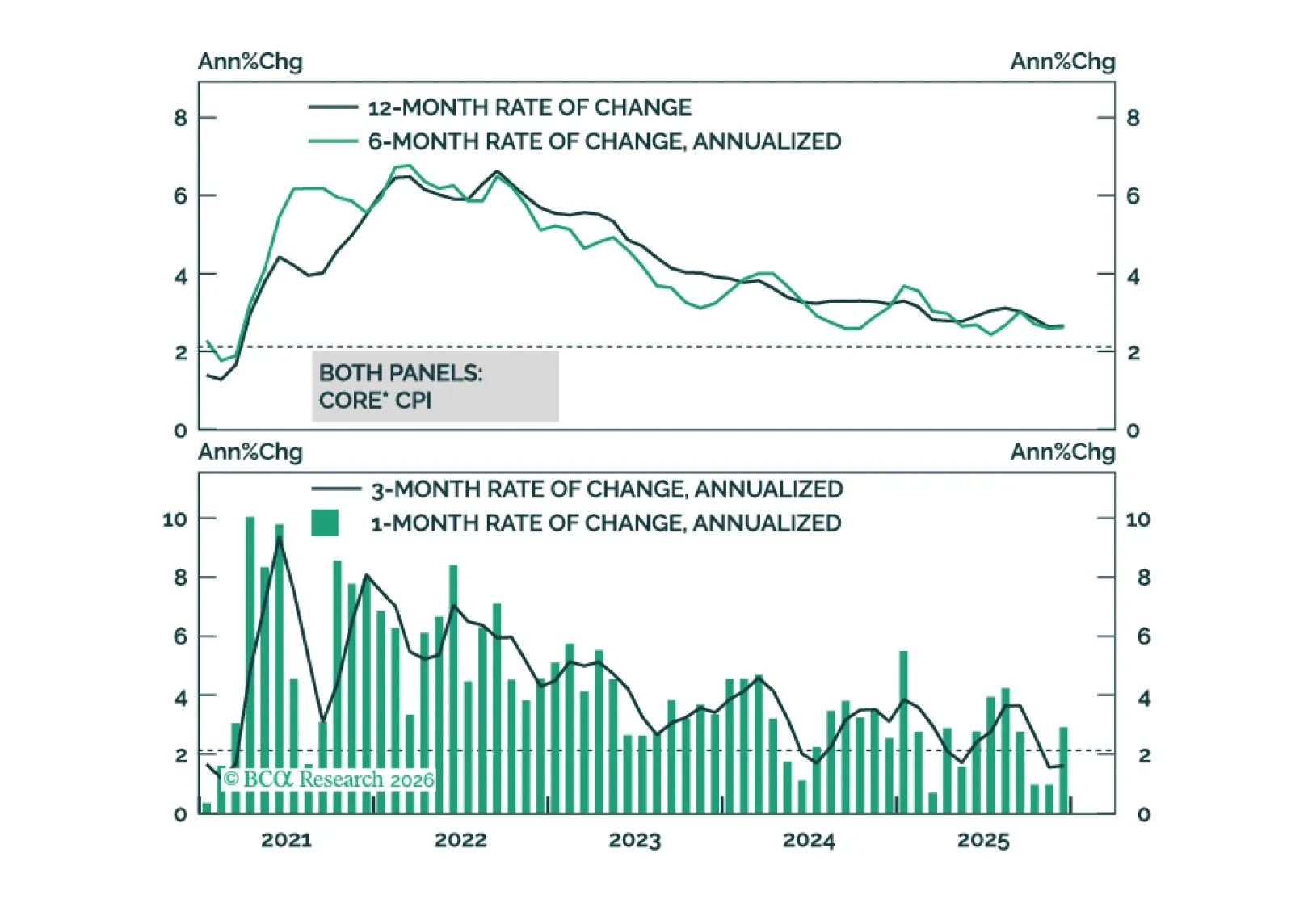

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.