Monetary Policy

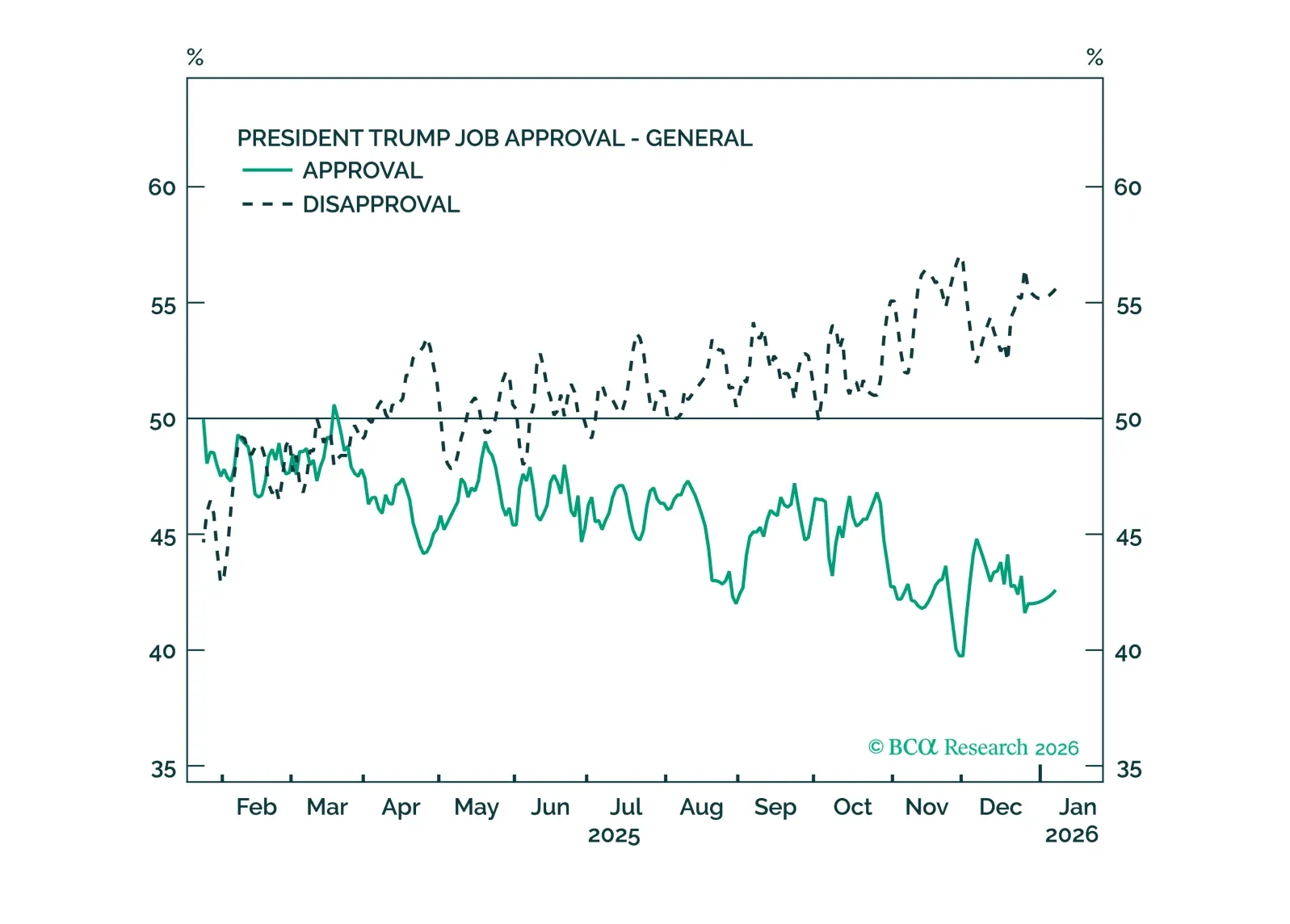

Congress will ultimately limit Trump from acting on his worst impulses, but his efforts to bypass those limits will cause market volatility.

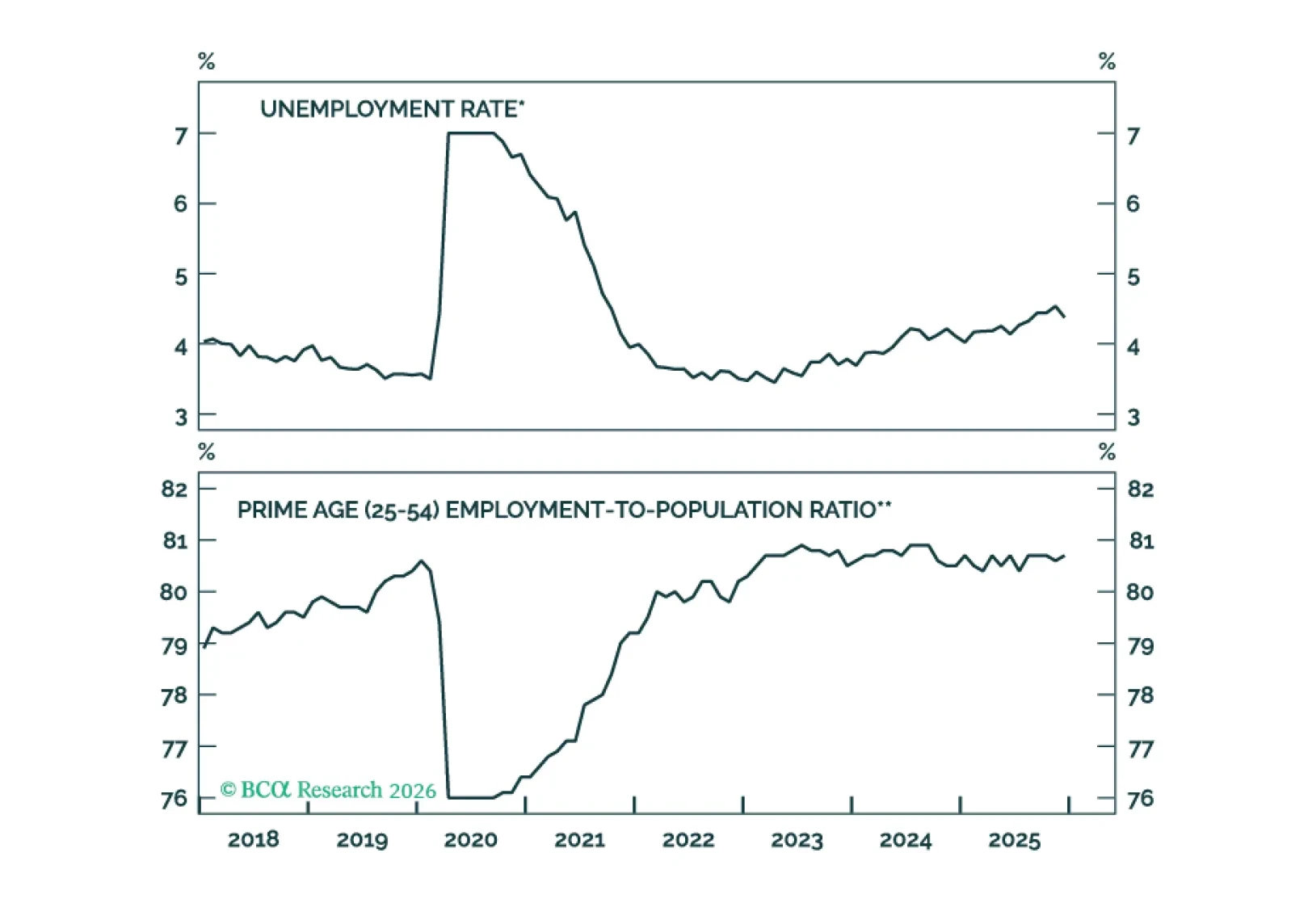

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

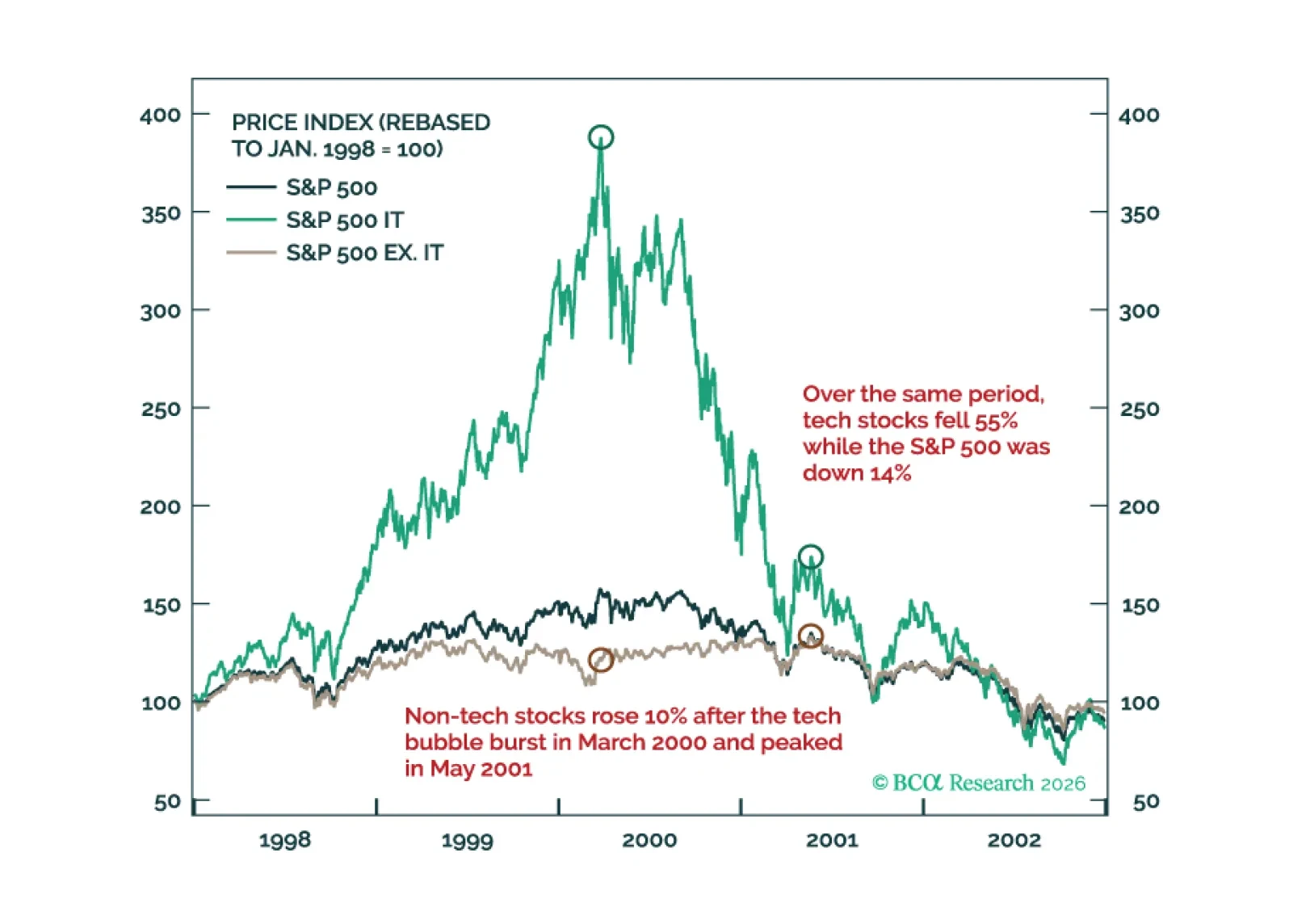

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

We have been surprised that consumption has held up well despite anemic payrolls growth. This brief considers ways that consumption might continue to beat our base-case expectations.

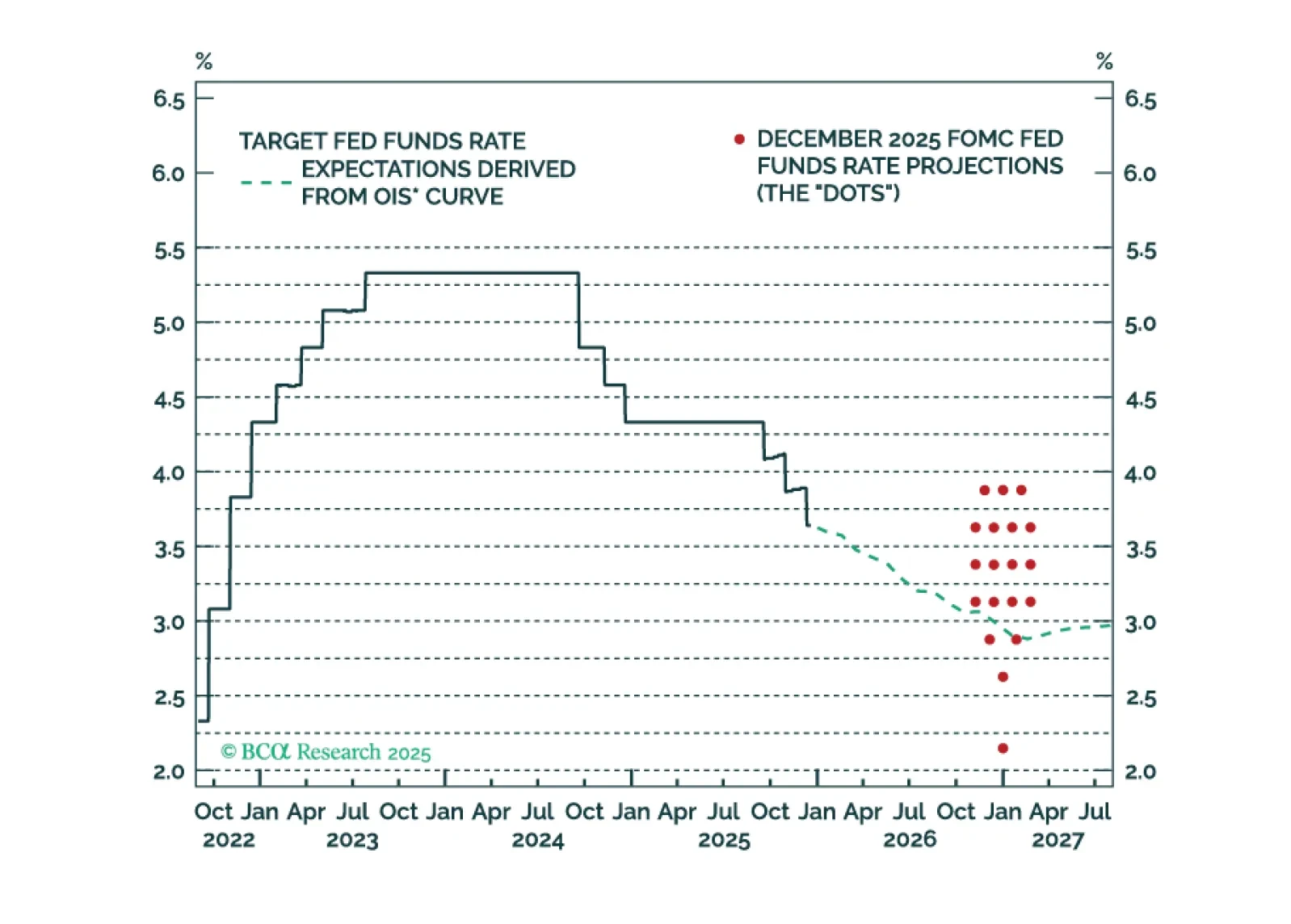

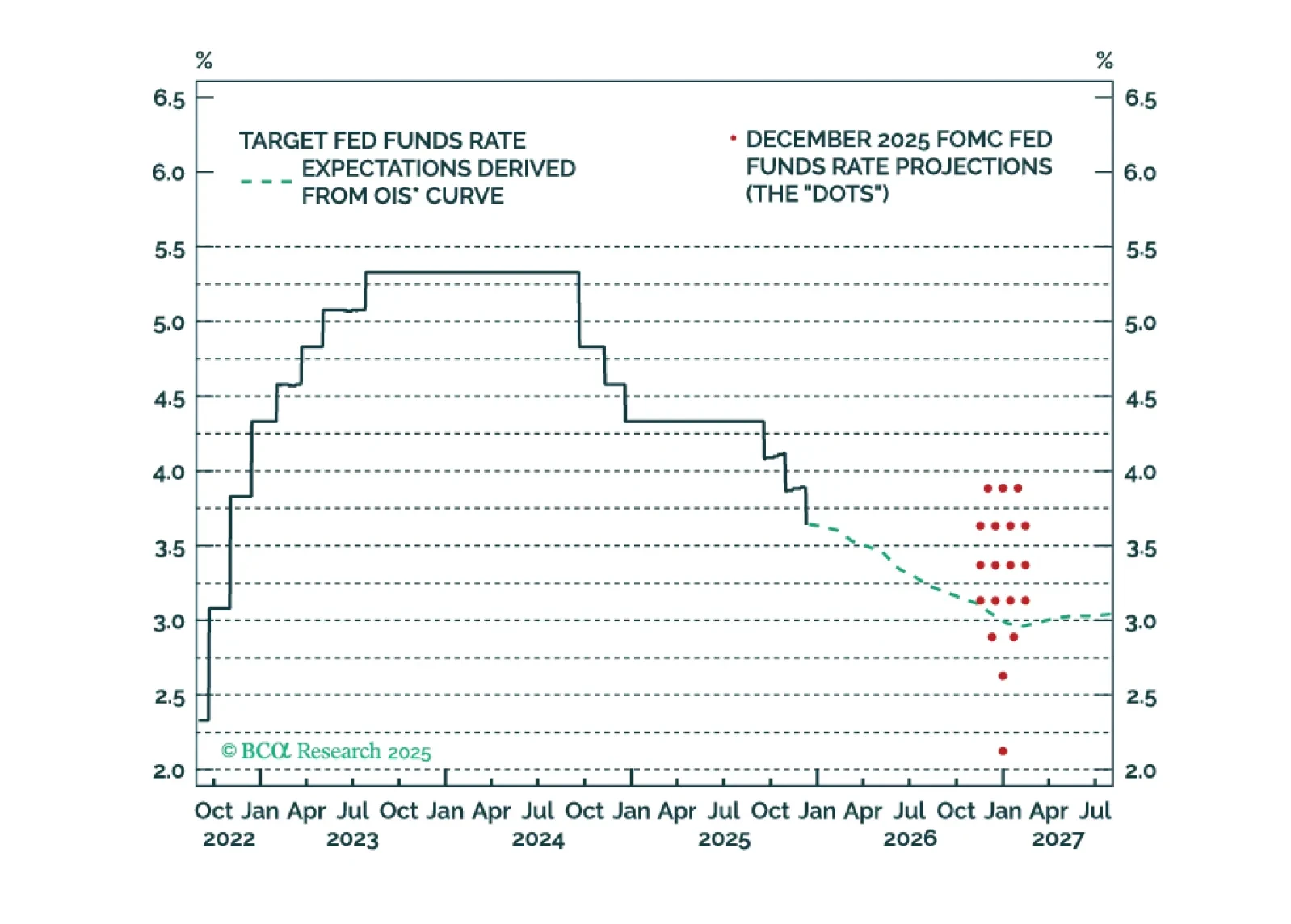

Our outlook for Fed policy in 2026.

Our outlook for Fed policy in 2026.

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

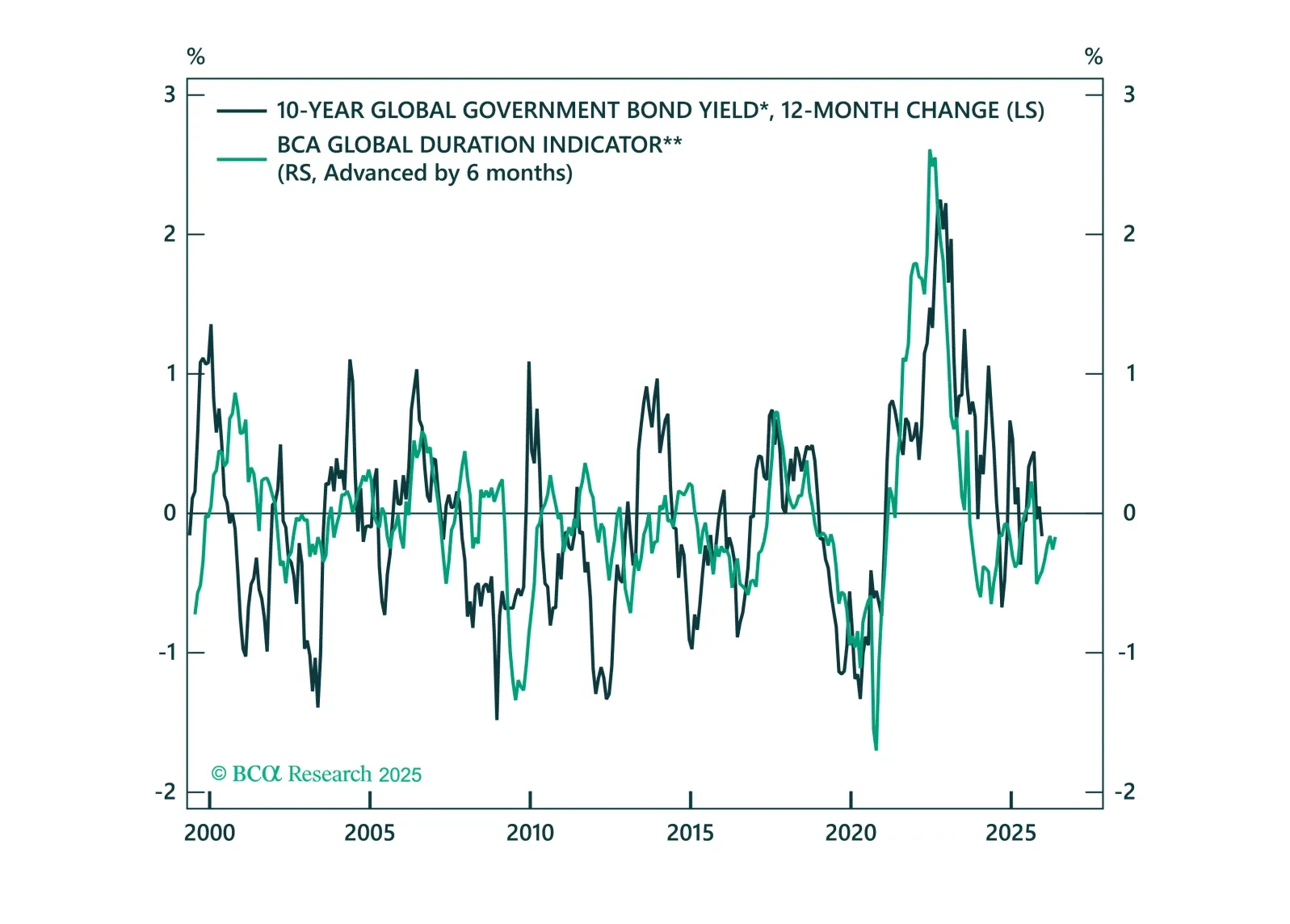

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.

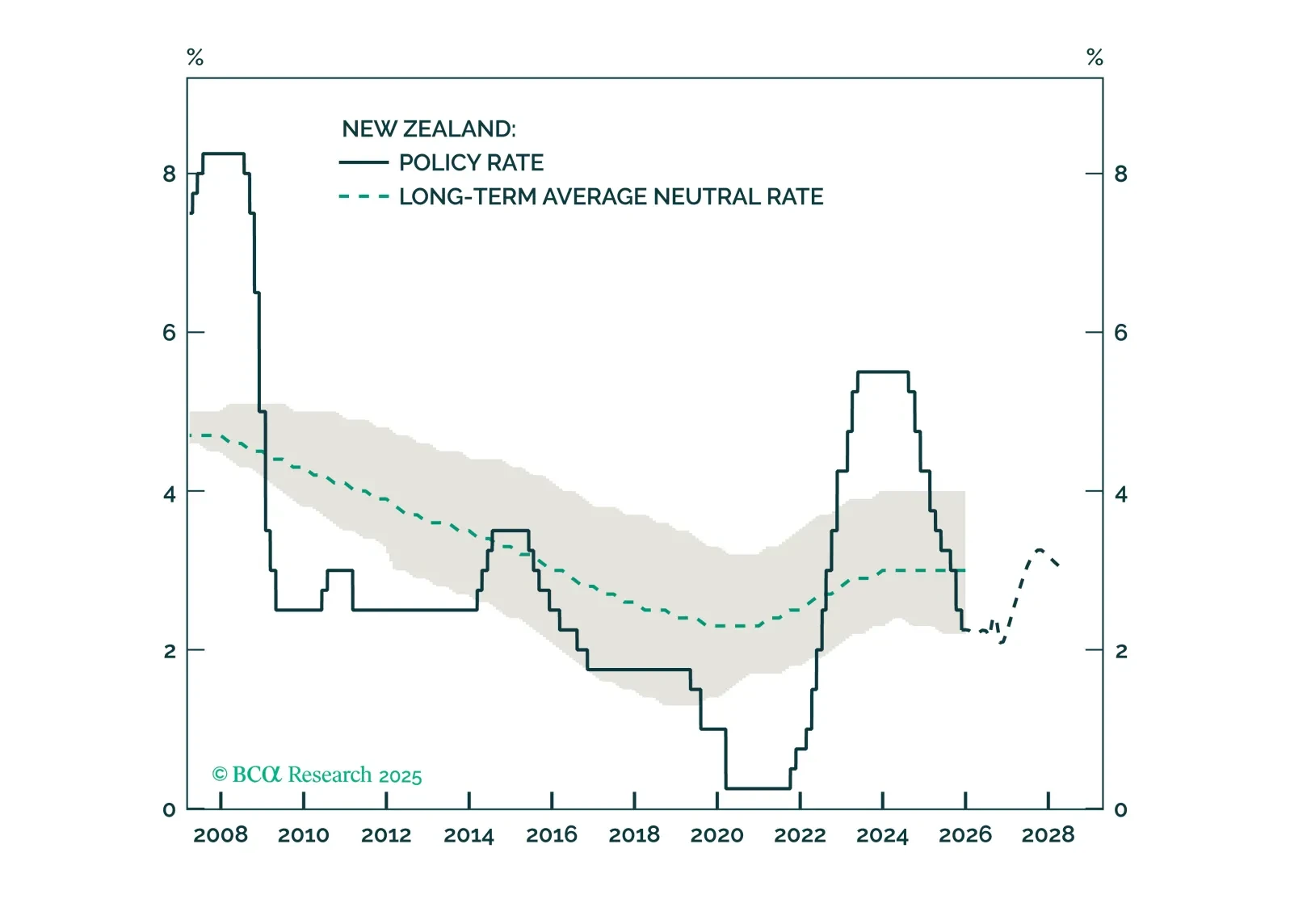

The RBNZ has concluded its aggressive easing blitz. With New Zealand economy finally showing signs of life, both the kiwi and local rates now look ripe for a reversal.

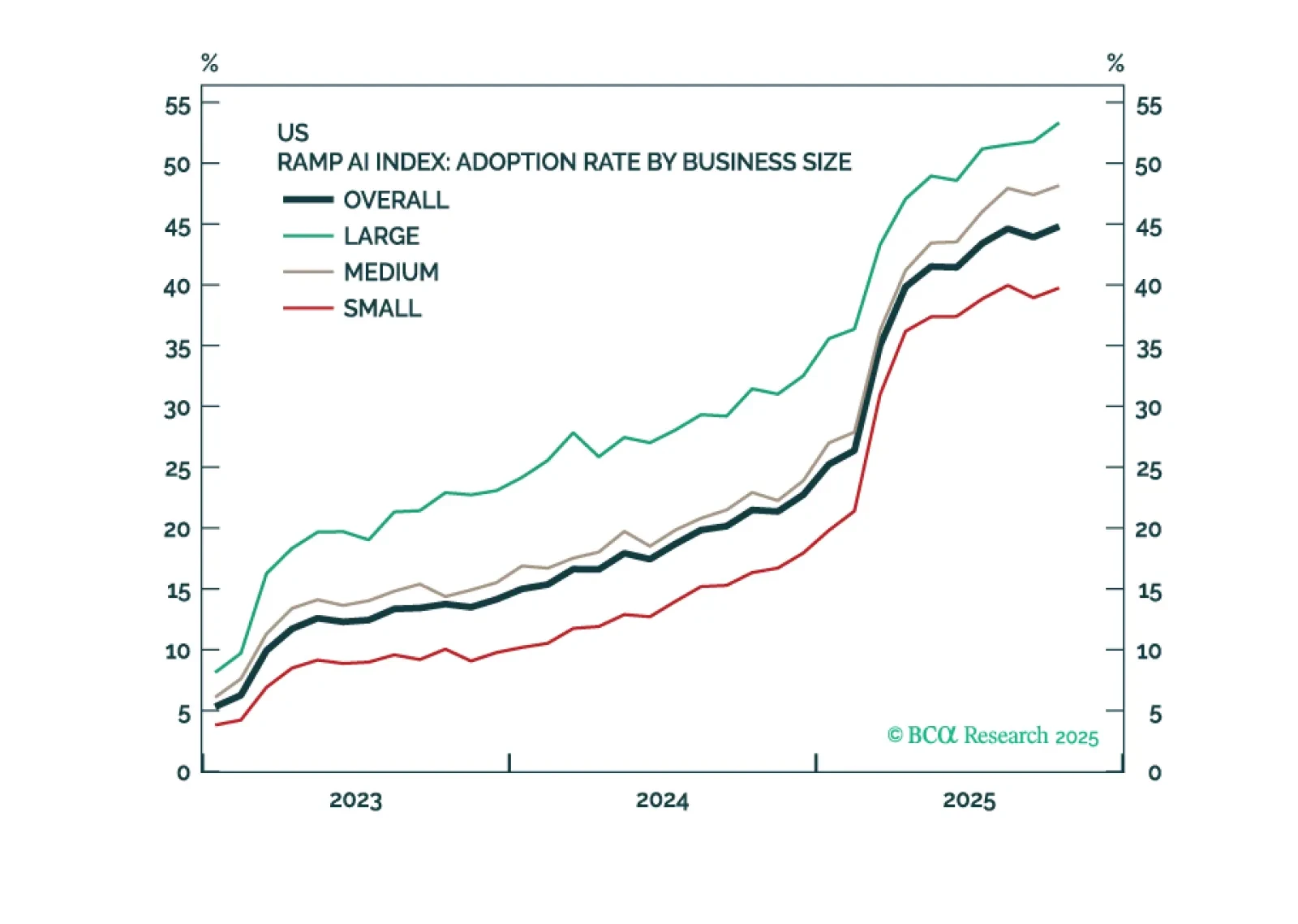

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.