Money Trends / Liquidity

Executive Summary Chinese Onshore Stock Prices And Earnings Are Set To Deteriorate

Chinese Onshore Stock Prices And Earnings Are Set To Deteriorate

Chinese Onshore Stock Prices And Earnings Are Set To Deteriorate

Macro fundamentals indicate that for the time being there is no basis to overweight Chinese onshore stocks (in both absolute terms and relative to global stocks) given the outlook for profit growth contraction in 1H22. We are reluctant to shift our stance on Chinese domestic stocks to overweight in the next 6 to 12 months due to the following non-trivial risks: a subdued recovery in China’s economic activity, a deceleration in fiscal impulse in 2H22, a re-focus on reducing carbon emissions, as well as higher US bond yields and tighter global liquidity conditions. Despite a sharp drop in January, valuations in Chinese onshore stocks are still neutral in absolute terms, and only slightly cheaper than global stocks. As such, Chinese onshore stocks offer little valuation buffer in the wake of any negative surprises. Bottom Line: We maintain our underweight stance on Chinese onshore stocks (in both absolute terms and relative to global equities) due to non-trivial risks in the coming year. Feature China’s stock markets was very weak in the first month of 2022. The domestic equity market tumbled by 8% in January, while the offshore market dropped by 3%. We discussed our view on Chinese investable stocks in last week’s report and recommended that investors go long on investable value stocks versus growth stocks. This week’s report focuses on the onshore market. While we expect the economy to stabilize by mid-year on the back of increased policy support, we are reluctant to move to a cyclical overweight in the next 6 to 12 months, in both absolute terms and relative to their global peers. Near-term challenges in economic fundamentals will continue to weigh on Chinese domestic stocks. Over a cyclical time frame, the main risks to a bullish view on Chinese stocks are fourfold: a potentially subdued economic recovery; a sharp deceleration in fiscal impulse in the second half of the year; a re-acceleration in de-carbonization efforts; as well as higher bonds yields in the US and tighter global financial conditions. Chinese onshore stocks are not as deeply discounted as their offshore peers and, therefore, are less able to counter any negative surprises. Macroeconomics Matter Chart 1Weak Economic Fundamentals Undermine Stock Performance

Weak Economic Fundamentals Undermine Stock Performance

Weak Economic Fundamentals Undermine Stock Performance

China’s economic fundamentals still drive corporate earnings and the country’s domestic stock performance, despite an escalation in monetary policy easing (Chart 1). Current macro fundamentals do not provide a legitimate support for investors to overweight Chinese stocks. The domestic stock market’s rocky start to 2022 underscores extremely fragile sentiment and heightened anxiety among investors. Credit growth bottomed in October last year but has not shown any signs of a strong rebound. Corporate demand for credit remains in the doldrums while turmoil in the housing market has disincentivized households from taking mortgages (Chart 2). The real economy, which in previous business cycles lagged credit growth by about six to nine months, has not responded to policy easing measures. Housing market indicators in January deteriorated further (Chart 3). Moreover, the nation’s counter-COVID measures have disrupted a recovery in the service sector and private consumption. Chart 2Demand For Loans Remains Weak

Demand For Loans Remains Weak

Demand For Loans Remains Weak

Chart 3Housing Sales Weakened Further In January

Housing Sales Weakened Further In January

Housing Sales Weakened Further In January

Chart 4Chinese Onshore Stock EPS Is Set To Deteriorate

Chinese Onshore Stock EPS Is Set To Deteriorate

Chinese Onshore Stock EPS Is Set To Deteriorate

The financial market is forward looking and macro policies have become more market friendly. However, Chart 4 suggests that China's onshore corporate profits are set to deteriorate in the coming six months or so, and investors will likely react negatively to any further weakness in China’s measures of economic activity. Bottom Line: At the moment, China’s domestic economic fundamentals do not support an overweight stance in Chinese stocks. Mindful Of Cyclical Risks Chinese authorities have prioritized stimulating growth through countercyclical measures in 2022. However, we are reluctant to move to a cyclical overweight stance because we see four significant risks to turning bullish towards Chinese stocks (in both absolute and relative terms) in the next 6 to 12 months. These scenarios not only threaten the performance of Chinese stocks relative to global equities but could also prevent Chinese stocks’ absolute performance from trending higher. A subdued recovery in China’s economic activity. When policymakers wait too long to decisively stimulate the economy, business and consumer sentiment as well as the economy can remain downbeat for a prolonged period. For example, in the 2014/15 business cycle, monetary policy started to ease in early 2015, but policymakers hesitated to back down from supply-side reforms. As a result, the economy did not bottom until Q1 2016. Business activity and the financial markets reached their lows only after the authorities opened the “flood irrigation” to the economy by massively stimulating the housing sector (Chart 5). Arguably China’s economy is in a better shape now than in 2014/15 and the ongoing economic slowdown is not the result of a four-year downtrend in industrial activity as was the case prior to 2015’s economic slump (Chart 6). The drop in the A-share market in January was nothing compared with the turmoil in the financial markets seven years ago. Chart 5Economic Activity Picked Up In Q1 2016 Following A Massive Stimulus

Economic Activity Picked Up In Q1 2016 Following A Massive Stimulus

Economic Activity Picked Up In Q1 2016 Following A Massive Stimulus

Chart 6China's Economy In General Is In A Better Shape Now Than In 2014/15...

China's Economy In General Is In A Better Shape Now Than In 2014/15...

China's Economy In General Is In A Better Shape Now Than In 2014/15...

On the other hand, the housing market, which is estimated to account for about 29% of China’s economy, is currently decelerating at the same pace as in 2014/15. Growth in home sales and new projects dropped to their 2015 lows, while real estate inventories are comparable to the 2015 highs (Chart 7). Furthermore, property developers and consumers are even more indebted than during the 2014/15 cycle (Chart 8). Chart 7...But Downward Momentum In Property Market Comparable To 2015

...But Downward Momentum In Property Market Comparable To 2015

...But Downward Momentum In Property Market Comparable To 2015

Chart 8Chinese Real Estate Developers And Households Are More Leveraged Now Than In 2015

Chinese Real Estate Developers And Households Are More Leveraged Now Than In 2015

Chinese Real Estate Developers And Households Are More Leveraged Now Than In 2015

Chart 9Policymakers Will Have To Allow Significant Re-leveraging To Revive The Housing Market

Policymakers Will Have To Allow Significant Re-leveraging To Revive The Housing Market

Policymakers Will Have To Allow Significant Re-leveraging To Revive The Housing Market

As noted in a previous report, unless regulators are willing to initiate more aggressive policy boosts as in 2015/16, the ongoing easing measures will not be sufficient to revive sentiment in the property market. Thus, the property market downtrend will likely extend through 2022 (Chart 9). The IMF recently revised its 2022 growth projection for China from 5.6% to 4.8%. It attributed the sharp downgrade to China’s protracted financial stress in the housing sector and pandemic-induced disruptions related to a zero-tolerance COVID-19 policy. A sub-5% economic expansion in 2022, although still an improvement from the 4.5% average annual rate in 2H21, is subdued and below China’s potential growth. Such a weak economic recovery will weigh on investor sentiment towards Chinese stocks in the coming year. A deceleration in fiscal impulse in 2H22. The impulse in fiscal stimulus - without any intervention - will fall sharply in the second half of the year. The Ministry Of Finance has approved a quota of RMB1.46 trillion in local government special purpose bonds (SPBs), which accounts for more than one-third of the yearly SPB quota, to be issued in Q1 this year. Chart 10Large Amount Of Local Government Debts Due In 2H22

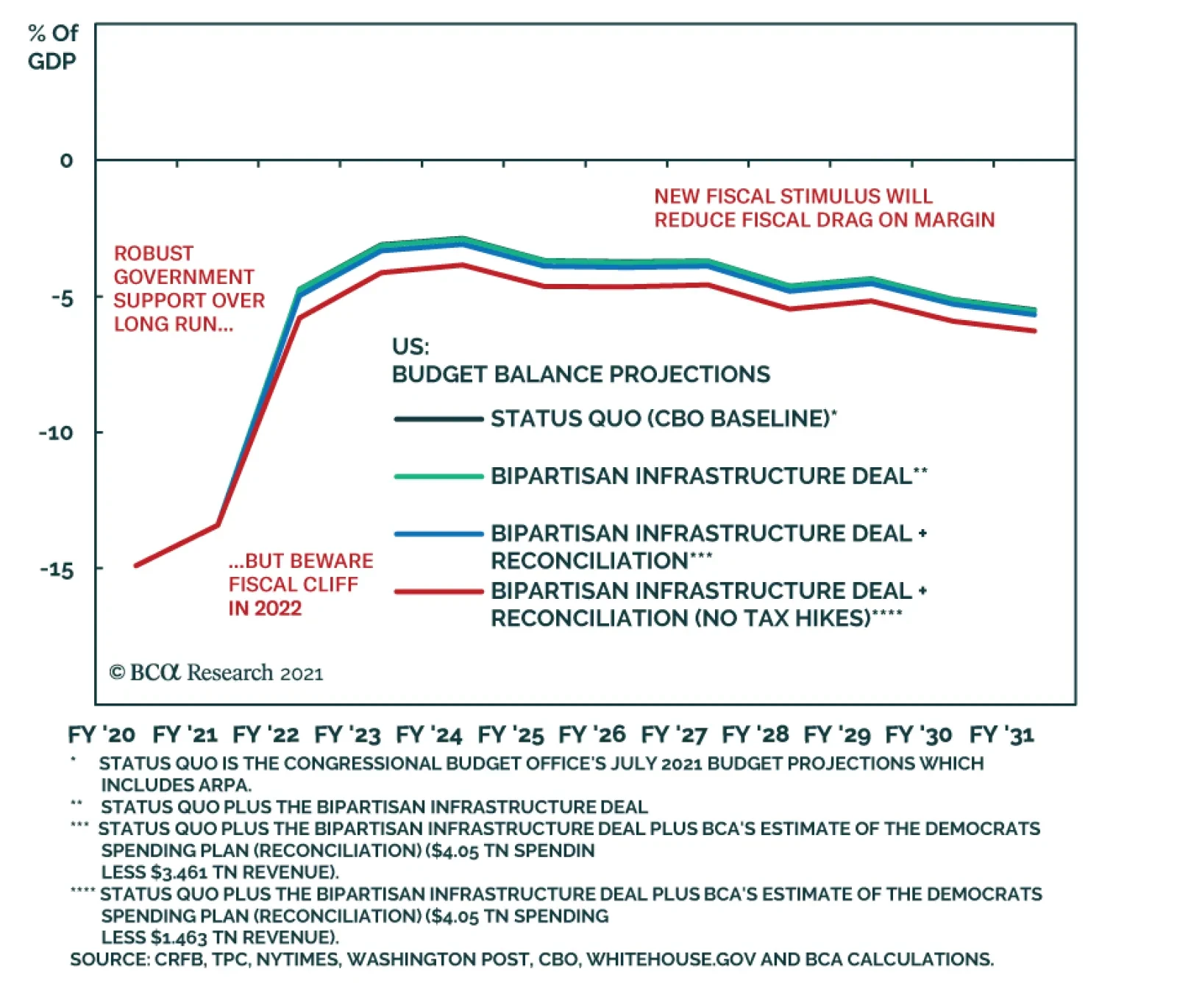

Chinese Onshore Stocks: How Much Upside?

Chinese Onshore Stocks: How Much Upside?

However, the frontloading of SPBs also means that the fiscal impulse will slow significantly in 2H22. Our geopolitical strategists have noted that a total of RMB2.7 trillion worth of local government bonds (LGB) will reach maturity this year, with RMB2.2 trillion coming due after June 2022 (Chart 10). The number of maturing LGBs in 2H22 will be only slightly smaller than those in all of 2021; in 2021 42% of LGBs issued were re-financing bonds to pay off existing local government debts, undermining real fiscal support for the economy. Furthermore, authorities have not loosened their grip on implicit local government debts (Chart 11). These so-called shadow banking debts through local government financing vehicles (LGFVs) are an important source of funding for investments in infrastructure projects. If the central government does not reverse its efforts to curb hidden debts while explicit fiscal stimulus also wanes, then we will likely see a sharp deceleration in fiscal support in 2H22. Lastly, we think Chinese policymakers are still serious about preventing “flood irrigation” type of stimulus, and will not opt for it unless the economic slowdown is much sharper. In Q1 2019 stock prices jumped sharply, boosted by an above-expectation pace of local government SPB issuance and credit expansion. However, following the public spat between Premier Li Keqiang and the PBoC over whether the January 2019 credit spike represented “flood irrigation-style” stimulus, policymakers quickly scaled back credit expansion in Q2 and onshore stock prices ended the year 5% lower than in Q1 (Chart 12). Chart 11Authorities Have Kept Tight Grip On Shadow Banking Activity

Authorities Have Kept Tight Grip On Shadow Banking Activity

Authorities Have Kept Tight Grip On Shadow Banking Activity

Chart 12Policymakers Scaled Back Stimulus And Took The Wind Out Of Onshore Stocks In 2019

Policymakers Scaled Back Stimulus And Took The Wind Out Of Onshore Stocks In 2019

Policymakers Scaled Back Stimulus And Took The Wind Out Of Onshore Stocks In 2019

Carbon emission reduction targets are still viable. In the current 14th Five-Year Plan (2021-2025), the cumulative targets reduction in energy consumption intensity is 13.5%.1 Last year’s energy crisis slowed the de-carbonization process and energy consumption intensity fell by 2.7% in 2021, missing the official annual target of 3%. To meet the de-carbonization target by 2025, energy consumption intensity will have to be lowered by at least 2.7% per year in the next four years. If energy- and carbon-intensive infrastructure activity picks up sharply in 1H22, then policymakers will have to renew their vigilance to constrain carbon-intensive activities later this year. The de-carbonization target has become a key parameter for assessing the performance of local governments, and meeting de-carbonization targets is particularly important given the rotation of local officials will be completed in late 2022. Furthermore, the initiative to reduce energy intensity reflects China’s commitment to move to a green economy. Given the important political events in both China and the US in the fall of 2022, meeting the annual de-carbonization target will be an important projection of China’s international image and will likely play a role in US-China negotiations. Chart 13Prior To The Pandemic, Chinese Stocks Had Little Correlation With US Treasury Yields

Prior To The Pandemic, Chinese Stocks Had Little Correlation With US Treasury Yields

Prior To The Pandemic, Chinese Stocks Had Little Correlation With US Treasury Yields

Higher bond yields in the US and tighter global liquidity conditions. Historically, Chinese onshore stocks have exhibited a loose cyclical correlation with US government bond yields (Chart 13). Nonetheless, if US bond yields rise more than global investors expect and to a level that is economically restrictive, then capital expenditures and household consumption in the US will weaken. This, in turn, will weigh down global trade and Chinese exports of manufactured goods. Against the backdrop of escalating US bond yields, Chinese onshore stocks may passively outperform their US counterparts because China’s A-share market is heavily weighted in value stocks. However, A-share prices in absolute terms will not be immune to heightened volatility in the global financial markets. The risk-off sentiment across global bourses will discourage portfolio flows into emerging economies including China. On a monthly basis, foreign portfolio net inflows account for less than 1% of the onshore equity market trading volume, but in recent years foreign portfolio inflows have increasingly influenced China’s onshore market sentiment and prices (Chart 14). China’s domestic household savings will not provide much support to stock prices this year. Chinese households have increasingly invested in the domestic equity market in the past few years, given that the authorities have been vigilant in containing price inflation in the property market.2 While we think Chinese consumers will continue rotating investment from property to financial market, household savings growth has fallen sharply since mid-2021, which means there have been less available funds to invest in the stock market (Chart 15). Chart 15Chinese Households' Quickly Diminishing Dry Powder

Chinese Households' Quickly Diminishing Dry Powder

Chinese Households' Quickly Diminishing Dry Powder

Chart 14Foreign Investors Have Become More Influential In The Chinese Onshore Market

Foreign Investors Have Become More Influential In The Chinese Onshore Market

Foreign Investors Have Become More Influential In The Chinese Onshore Market

Bottom Line: For the time being, the significant risks described above make us reluctant to turn bullish on Chinese stocks in both absolute and relative terms. Investment Conclusions There are few upsides related to Chinese onshore stocks in the next 6 to 12 months. However, there are two risks to our underweight stance on Chinese onshore stocks: First, we cannot rule out the possibility that Chinese policymakers will go “all in” for economic stability and allow a significant credit overshoot. In this scenario, a strong pickup in credit growth will produce a rebound in profit growth and support share prices in absolute terms and relative to global equities. Secondly, recent gyrations in global financial markets, coupled with China’s sluggish domestic economy, have triggered shakeouts in the onshore equity markets. The pullback in stock prices has helped to shed some excesses in Chinese stock valuations. Chart 16In Very Optimistic Scenario Chinese Stocks Would Have Some Upside Potential Vs. Global

In Very Optimistic Scenario Chinese Stocks Would Have Some Upside Potential Vs. Global

In Very Optimistic Scenario Chinese Stocks Would Have Some Upside Potential Vs. Global

If the stimulus in the next 6 to 12 months returns Chinese corporate profit growth to their 2021 peaks, then Chinese stock prices (in absolute terms) will also approach or go back to their early-2021 highs. Chart 16 highlights that reverting to these levels would imply a return of about 10-15% for domestic stocks in both absolute and relative price terms. We think China’s potential to command a higher multiple than global stocks is capped, barring a major structural improvement in earnings growth. However, Chart 16 (bottom panel) shows that Chinese onshore stocks at their height early last year were still cheaper than their global counterparts. Therefore, in a scenario where Beijing does “whatever it takes” to stimulate its economy, we will have no strong reasons to argue against a return of domestic forward multiples and a strong earnings growth back to levels seen in early-2021. Jing Sima China Strategist jings@bcaresearch.com Footnotes 1 Energy consumption intensity refers to energy consumption per unit of GDP. 2 There was a sharp jump in demand in 2020 for investment products from households; mutual funds in China raised money at a record pace, bringing in over 2 trillion yuan ($308 billion), which is more than the total amount in the previous four years. Strategic Themes Cyclical Recommendations Tactical Recommendations

BCA Research is proud to announce a new feature to help clients get the most out of our research: an Executive Summary cover page on each of the BCA Research Reports. We created these summaries to help you quickly capture the main points of each report through an at-a-glance read of key insights, chart of the day, investment recommendations and a bottom line. For a deeper analysis, you may refer to the full BCA Research Report. Executive Summary China’s Property Bust To Dwarf Japan’s

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

China’s confluence of internal and external risks will continue to weigh on markets in 2022. Internally China’s property sector turmoil is one important indication of a challenging economic transition. The Xi administration will clinch another term but sociopolitical risks are underrated. Externally China faces economic and strategic pressure from the US and its allies. The US is distracted with other issues in 2022 but US-China confrontation will revive beyond that. China will strengthen relations with Russia and Iran, though it will not encourage belligerence. It needs their help to execute its Eurasian strategy to bypass US naval dominance and improve its supply security over the long run. China will ease monetary and fiscal policies in 2022 but it has no interest in a massive stimulus. Policy easing will be frontloaded in the first half of the year. Featured Trade: Strategically stay short the renminbi versus an equal-weighted basket of the dollar and the euro. Stay short TWD-USD as well. Recommendation INCEPTION Date Return SHORT TWD / USD 2020-06-11 0.5% SHORT CNY / EQUAL-WEIGHTED BASKET OF EURO AND USD 2021-06-21 -3.9% Bottom Line: Beijing is easing policy to secure the post-pandemic recovery, which is positive for global growth and cyclical financial assets. But structural headwinds will still weigh on Chinese assets in 2022. China’s Historic Confluence Of Risks Global investors continue to clash over China’s outlook. Ray Dalio, founder of Bridgewater Associates, recently praised China’s “Common Prosperity” plan and argued that the US and “a lot of other countries” need to launch similar campaigns of wealth redistribution. He warned about the US’s 2024 elections and dismissed accusations of human rights abuses by saying that China’s government is a “strict parent.”1 By contrast George Soros, founder of the Open Society Foundations, recently warned against investing in China’s autocratic government and troubled property market. He predicted that General Secretary Xi Jinping would fail to secure another ten years in power in the Communist Party’s upcoming political reshuffle.2 Geopolitics can bring perspective to the debate: China is experiencing a historic confluence of internal (political) and external (geopolitical) risk, unlike anything since its reform era began in 1979. At home it is struggling with the Covid-19 pandemic and a difficult economic transition that began with the Great Recession of 2008-09. Abroad it faces rising supply insecurity and an increase in strategic pressure from the United States and its allies. The implication is that the 2020s will be an even rockier decade than the 2010s. In the face of these risks the Chinese Communist Party is using the power of the state to increase support for the economy and then repress any other sources of instability. Strict “zero Covid” policies will be maintained for political reasons as much as public health reasons. Arbitrary punitive measures will put pressure on the business elite and foreigners. The geopolitical outlook is negative over the long run but it will not worsen dramatically in 2022 given America’s preoccupation with Russia, Iran, and midterm elections. Bottom Line: Global investor sentiment toward China will remain pessimistic for most of the year – but it will turn more optimistic toward foreign markets, especially emerging markets, that sell into China. China’s Internal Risks Chart 1China's Demographic Cliff

China's Demographic Cliff

China's Demographic Cliff

By the end of 2021, China accounted for 17.7% of global economic output and 12.1% of global imports. However, the secular slowdown in economic growth threatens to generate opposition to the single-party regime, forcing the Communist Party to seek a new base of political legitimacy. Most countries saw a drop in fertility rates in the third quarter of the twentieth century but China’s “one child policy” created a demographic cliff (Chart 1). At first this generated savings needed for national development. But now it leaves China with excess capacity and insufficient household demand. Across the region, falling fertility rates have led to falling potential growth and falling rates of inflation. Excess savings increased production relative to consumption and drove down the rate of interest. The shift toward debt monetization in the US and Japan, in the post-pandemic context, is now threatening this trend with a spike in inflation. China is also monetizing debt after a decade of deflationary fears. But it remains to be seen whether inflation is sustainable when fertility remains below the replacement rate over the long run, as is projected for China as well as its neighbors (Chart 2). China’s domestic situation is fundamentally deflationary as a result of chronic over-investment over the past 40 years. China’s gross fixed capital formation stands at 43% of GDP, well above the historic trend of other major countries for the past 30 years (Chart 3). Chart 2Will Inflation Decouple From Falling Fertility?

Will Inflation Decouple From Falling Fertility?

Will Inflation Decouple From Falling Fertility?

Chart 3Over-Investment Is Deflationary, Not Inflationary

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Like other countries, China financed this buildup of fixed capital by means of debt, especially state-owned corporate debt. While building a vast infrastructure network and property sector, it also built a vast speculative bubble as investors lacked investment options outside of real estate. The growth in property prices has tracked the growth in private non-financial sector debt. The downside is that if property prices fall, debt holders will begin a long and painful process of deleveraging, just like Japan in the 1990s and 2000s. Japan only managed to reverse the drop in corporate investment in the 2010s via debt monetization (Chart 4). Chart 4Japan’s Property Bust Coincided With Debt Deleveraging

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Chart 5China's Debt Growth Halts

China's Debt Growth Halts

China's Debt Growth Halts

Looking at the different measures of Chinese debt, it is likely that deleveraging has begun. Total debt, public and private, peaked and rolled over in 2020 at 290% of GDP. Corporate debt has peaked twice, in 2015 and again in 2020 at around 160% of GDP. Even households are taking on less debt, having gone on a binge over the past decade (Chart 5). In short China is following the Japanese and East Asian growth model: the stark drop in fertility and rise in savings created a huge manufacturing workshop and a highly valued property sector, albeit at the cost of enormous private and considerable public debt. If the private sector’s psychology continues to shift in favor of deleveraging, then the government will be forced to take on greater expenses and fund them through public borrowing to sustain aggregate demand, maximum employment, and social stability. The central bank will be forced to keep rates low to prevent interest rates from rising and stunting growth. China’s policymakers are stuck between a rock and a hard place. New regulations aimed at controlling the property bubble (the “three red lines”) precipitated distress across the sector, emblematized by the failure of the world’s most indebted property developer, Evergrande. Other property developers are looking to raise cash and stay solvent. Property prices peaked in 2015-16 and are now dropping, with third-tier cities on the verge of deflation (Chart 6). Chart 6China's Property Crisis Weighs On Construction

China's Property Crisis Weighs On Construction

China's Property Crisis Weighs On Construction

As the property bubble tops out, Chinese policymakers are looking for new sources of productivity and growth. Chart 7Productivity In Decline

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Productivity growth is subsiding after the export and property boom earlier in the decade, in keeping with that of other Asian economies. And sporadic initiatives to improve governance, market pricing, science, and technology have not succeeded in lifting total factor productivity (Chart 7). The initial goal of the Xi administration’s reforms, to rebalance the economy away from manufacturing toward services, has stumbled and will continue to face headwinds from the financial and real estate sectors that powered much of the recent growth in services (Chart 8). Chart 8China’s Structural Transition Falters

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Indeed the Communist Party is rediscovering the value of export-manufacturing in the wake of the pandemic, which led to a surge in durable goods orders as global consumers cut back on services and businesses initiated a new cycle of capital expenditures (Chart 9). The party encouraged the workforce to shift out of manufacturing over the past decade but is now rethinking that strategy in the face of the politically disruptive consequences of deindustrialization in the US and UK – such that the state can be expected to recommit to supporting manufacturing going forward (Chart 10). Policymakers are emphasizing economic self-sufficiency and “dual circulation” (import substitution) as solutions to the latent socioeconomic and political threat posed by disillusioned former manufacturing workers. Chart 9China Turns Back To Exports

China Turns Back To Exports

China Turns Back To Exports

Chart 10De-Industrialization Will Be Halted

De-Industrialization Will Be Halted

De-Industrialization Will Be Halted

Even beyond ex-manufacturing workers, the country’s economic transition risks generating social instability. The middle class, defined as those who consume from $10 to $50 per day in purchasing power parity terms, now stands at 55% of total population, comparable to where it stood when populist and anti-populist political transformations occurred in Turkey, Thailand, and Brazil (Chart 11). China’s middle class may not be willing or able to intervene into the political process, but the government is still concerned about the long-term potential for discontent. Otherwise it would not have launched anti-corruption, anti-pollution, and anti-industrial measures in recent years. These measures vary in effectiveness but they all share the intention to boost the government’s legitimacy through social improvements and thus fall in line with the new mantra of “common prosperity.” For decades the ruling party claimed that the “principle contradiction” in society arose from a failure to meet the people’s “material needs,” but beginning in 2021 it emphasized that the principle contradiction is the people’s need for a “better life.” Real wages continue to grow but the pace of growth has downshifted from previous decades. The bigger problem is the stark rise in inequality, here proxied by skyrocketing housing prices. Hong Kong’s inequality erupted into social unrest in recent years even though it has a much higher level of GDP per capita than mainland China (Chart 12). In major cities on the mainland, housing prices have outpaced disposable income over the past two decades. Youth unemployment also concerns the authorities. Chart 11Social Instability A Genuine Risk

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Bottom Line: The Chinese regime faces historic social and political challenges as a result of a difficult structural economic transition. The ongoing emphasis on “common prosperity” reveals the regime’s fear of social instability. The underlying tendency is deflationary, though Beijing’s use of debt monetization introduces a long-term inflationary risk that should be monitored. Chart 12Causes Of Hong Kong Unrest Also Present In China

Causes Of Hong Kong Unrest Also Present In China

Causes Of Hong Kong Unrest Also Present In China

China’s External Risks Geopolitically speaking, China’s greatest challenge throughout history has been maintaining domestic stability. Because China is hemmed in by islands that superior foreign powers have often used as naval bases, it is isolated as if it is a landlocked state. A stark north-south division within its internal geography and society creates inherent political tension, while buffer regions are difficult to control. Hence foreign powers can meddle with internal affairs, undermine unity and territorial integrity, and exploit China’s large labor force and market. However, in the twenty-first century China has the potential to project power outward – as long as it can maintain internal stability. Power projection is increasingly necessary because China’s economy increasingly depends on imports of energy, leaving it vulnerable to western maritime powers (Chart 13). Beijing’s conversion of economic into military might has also created frictions with neighbors and aroused the antagonism of the United States, which increasingly seeks to maintain the strategic anchor in the western Pacific that it won in World War II. Chart 13Import Dependency A Strategic Security Threat

Import Dependency A Strategic Security Threat

Import Dependency A Strategic Security Threat

As China’s influence expands into East Asia and the rest of Asia, conflicts with the US and its allies are increasingly likely, especially over critical sea lines of communication, including the Taiwan Strait. China’s reinforcement of its manufacturing prowess will also provoke the United States, while the US’s erratic attempts to retain its strategic position in Asia Pacific will threaten to contain China. Yet the US cannot concentrate exclusively on countering China – it is distracted by internal politics and confrontations with Russia and Iran, especially in 2022. China will strengthen relations with Russia and Iran. As an energy importer, China would prefer that neither Russia nor Iran take belligerent actions that cause a global energy shock. But both Moscow and Tehran are essential to China’s Eurasian strategy of bypassing American naval dominance to reduce its supply insecurity. And yet, in 2022 specifically, the US and China are both concerned about maintaining positive domestic political dynamics due to the midterm elections and twentieth national party congress. This includes a desire to reduce inflation. Hence both would prefer diplomacy over trade war, with regard to each other, and over real war, with regard to Ukraine and Iran. So there is a temporary overlap in interests that will discourage immediate confrontation. China might offer limited cooperation on Iranian or North Korean nuclear and missile talks. But the same domestic political dynamics prevent a significant improvement in US-China relations, as neither side will grant trade concessions in 2022, and the underlying strategic tensions will revive over the medium and long run. Bottom Line: China faces historic external risks stemming from import dependency and conflict with the United States. In the short run, the US conflicts with Russia and Iran might lead to energy shocks that harm China’s economy. Japan never recovered its rapid growth rates after the 1973 Arab oil embargo. In the long run, while Washington has little interest in fighting a war with China, its strategic competition will focus on galvanizing allies to penalize China’s economy and to substitute away from China, in favor of India and ASEAN. China’s Macro Policy In 2022: Going “All In” For Stability In last year’s China Geopolitical Outlook, we maintained our underweight position on Chinese equities and warned that Beijing’s policy tightening posed a significant risk to global cyclical assets – and yet we concluded that policymakers would avoid overtightening policy to the extent of spoiling the global recovery. This view prevailed over the course of 2021. Policymakers tightened monetary and fiscal policy in the first half of the year, then started loosening up in the summer. Chinese equities crashed but global equities powered through the year. In December 2020, at the Central Economic Work Conference, policymakers stated that China would “maintain necessary policy support for economic recovery and avoid sharp turns in policy” in 2021. In the event they did the minimal necessary, though they did avoid sharp turns. For 2022, the key word is “stability.” At the Central Economic Work Conference last month, the final communique mentioned “stability” or “stabilize” 25 times (Table 1). Hence the main objective of Chinese policymakers this year is to prioritize both economic and social stability ahead of the twentieth national party congress. Authorities will avoid last year’s tight policies. Table 1Key Chinese Policy Guidance 2021-22

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

China’s quarterly GDP growth slipped to just 4% in Q4 2021, from rapid recovery growth of 18.3% in Q1 2021. Considering the low base effect of 2020, the average growth of 2020 and 2021 ranged from 5-5.5% (Chart 14). This growth rate is in line with the pre-pandemic trajectory of 2015-2019. In Jan 2022, the IMF cut China’s 2022 growth forecast to 4.8%, while the World Bank lowered its forecasts to 5.1%. Considering the two-year average growth and government’s goal of “all in for stability,” we see an implicit GDP target of 5-5.5%. Chart 14Breakdown Of China’s GDP Growth

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Does this target matter? Although China stopped announcing explicit GDP growth targets, understanding the implicit target helps investors predict the turning point in macro policy. Due to robust global demand, net exports are now making a sizable contribution to GDP growth. However, due to the high base effect of 2021, there is limited room for exports to grow in 2022. Hence economic growth has to rely on final consumption expenditure and gross capital formation. Yet as a result of policy tightening, gross capital formation’s contribution to GDP has decreased significantly, from positive in H1 2021 to a rare negative contribution to GDP in the second half. At the same time, the contribution from final consumption expenditure also slipped over the course of 2021, due to worsening Covid conditions, one of the three pressures stated by the government. What does that mean? It means that loosening up macro policies is the pre-condition for stabilizing growth and the economy. Just like the officials said (see Table 1), the Chinese economy is “facing triple pressure from demand contraction, supply shocks, and weakening expectations,” so that “all sides need to take the initiative and launch policies conducive to economic stability.” Bottom Line: It is reasonable to expect accommodative fiscal and monetary policies in 2022, at least until the party congress ends. In fact, authorities have already started to make these adjustments since Q4 2021. China Avoids Monetary Overtightening Credit growth can be seen as an indicator for gross capital formation. In the second half of 2021, China’s total social financing (total private credit) growth plunged below 12% (Chart 15), the threshold we identified for determining whether authorities overtightened policy. Correspondingly, gross capital formation’s contribution to GDP dropped into the negative zone (see Chart 14 above). However, money growth did not dip below the threshold, and authorities are now trying to boost credit growth. Starting from December 2021, the market has seen marginally positive news out of the People’s Bank of China: December 15, 2021: The PBOC conducted its second reserve requirement ratio (RRR) cut in 2021. The 50 bps cut was expected to release $188 billion in liquidity to support the real economy. December 20, 2021: The PBOC conducted its first interest rate cut since April 2020 by cutting 1-Year LPR by 5 bps on December 20 (Chart 16). Chart 15China's Money And Credit Growth Hits Pain Threshold

China's Money And Credit Growth Hits Pain Threshold

China's Money And Credit Growth Hits Pain Threshold

Chart 16China Monetary Policy Easing

China Monetary Policy Easing

China Monetary Policy Easing

January 17, 2022: The PBOC cut the interest rate on medium-term lending facility (MLF) loans and 7-day reverse repurchase (repos) rate both by 10 bps. January 20, 2022: The PBOC further lowered the 1-year LPR by 10 basis points and cut the 5-year LPR by 5 basis points, the first cut since April 2020. Chart 17China Policy Easing Will Boost Import Volumes

China Policy Easing Will Boost Import Volumes

China Policy Easing Will Boost Import Volumes

The timing and size of the last two rate cuts came as a surprise to the market, signaling more comprehensive easing than was expected (confirming our expectations).3 The market saw a clear turning point: Chinese authorities are now fully aware of the need to loosen up monetary policy to counter intensifying downward pressure on the economy. Incidentally, the fine-tuning of the different lending facilities suggests the government aims to lower borrowing costs and stimulate the market without over-heating the property sector again. PBOC officials claim there is still some space for further cuts, though narrower now, when asked about if there is any room to further cut the RRR and interest rates in Q1. They added that the PBOC should “stay ahead of the market curve” and “not procrastinate.”4 Recent movements have validated this point. Going forward, M2 growth should stay above 8%. Total social financing growth should move up above our “too tight” threshold, although weak sentiment among private borrowers could force authorities to ease further to ensure that credit growth picks up. If the government is still committed to fighting housing speculation, as before, then we could see a smaller adjustment to the 5-Year LPR in the future. Otherwise the government is taking its foot off the brake for stability reasons, at least temporarily. Bottom Line: China will keep easing monetary policy in 2022, at least in the first half. This will result in an improvement in Chinese import volumes and ultimately emerging market corporate earnings, albeit with a six-to-12-month lag (Chart 17). China Avoids Fiscal Overtightening China will also avoid over-tightening fiscal policy in 2022. In December the government stressed the need to “maintain the intensity of fiscal spending, accelerate the pace, and moderately advance infrastructure investment.” In 2021, local government bond issuance did not pick up until the second half of the year. Considering the time lag of construction projects, it was too late for local government investment to stimulate the economy. By Q3 2021, local government bond issuance had just completed roughly 70% of the annual quota. By comparison, in 2018-2020, local governments all completed more than 95% of the annual quota by the end of September each year (Chart 18A). Chart 18AChina: No Pause In Local Bond Issuance In H1 2022

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Chart 18BChina: No Pause In Local Bond Issuance In H1 2022

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

There are several reasons behind the slow pace last year. The central government refused to pre-approve and pre-authorize the quota for bond issuance at the beginning of the year in 2021, in order to restore discipline after the massive 2020 stimulus measures. The quota was not released until after the Two Sessions in March, which means local government bond issuance did not pick up until April 2021, causing a 3-month vacuum in local government fiscal support (see Chart 18B). In contrast, for 2019 and 2020, the central government pre-authorized the bond issuance quota ahead of time to try to provide fiscal support evenly throughout the year. Starting from 2020, the central government strengthened supervision and evaluation of local government investment projects, again to instill discipline. Previously local governments could easily issue general-purpose bonds and the funds were theirs to spend. But now local governments are required to increase the transparency of their investment projects and mainly finance these projects via special-purpose bonds, i.e. targeted money for authorized projects (Table 2). In 2021 local governments were less willing to issue bonds. At the April 2021 Politburo meeting, the central government vowed to “establish a disposal mechanism that will hold local government officials accountable for fiscal and financial risks.” This triggered risk-aversion. Beijing wanted to prevent a growth “splurge” in the wake of its emergency stimulus, like what happened in 2008-11. The fiscal turning point came in the second half of the year. The central government called for accelerating local government bond issuance several times from July to October. The pace significantly picked up in the second half of 2021 and Q4 accounted for a significant portion of annual issuance (Chart 18). As a result, fixed asset investment and fiscal impulse should pick up in Q1 2022. Thus, unlike last year, authorities are trying to avoid a sharp drop in the fiscal impulse. The Ministry of Finance has already frontloaded 1.46 trillion yuan ($229 billion) from the 2022 special purpose bonds quota. This amount is part of the 2022 annual local government bond issuance quota, with the rest to be released at the Two Sessions in March. Pulling these funds forward indicates the rising pressure to stabilize economic growth in Q1 this year. That being said, investors should differentiate easing up fiscal policy and “flood-like” stimulus in the past. The government still claims it will “contain increases in implicit local government debts.” In fact, pilot programs to clean up implicit debts have already started in Shanghai and Guangdong. This means, China will not reverse past efforts on curbing hidden debts. Hence fiscal support will be more tightly controlled in future, like water taps in the hands of the central government. The risk of fiscal tightening is backloaded in 2022. The tremendous amount of local government bonds issued in Q4 2021 will start to kick in early 2022. These will combine with the frontloaded special purposed bonds. Fiscal impulse should tick up in Q1. However, fiscal impulse might decelerate in the second half. A total of $2.7 trillion yuan worth of local government bonds will reach maturity this year, with $2.2 trillion yuan reaching maturity after June 2022 (Table 3). This means that in the second half, local governments will need to issue more re-financing bonds to prevent insolvency risk, thus undermining fiscal support for the economy. And this last point underscores the threat of economic and financial instability that China faces over the long run. Table 2Breakdown Of China Local Government Bond Issuance

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Bottom Line: Stability is the top priority in 2022. China will continue to easy up monetary and fiscal policy in H1, to combat the economic downward pressure ahead of the twentieth national party congress (Chart 19). Policy tightening risk is backloaded. Structural reforms will likely subside for now until the Xi administration re-consolidates power for the next ten years. Table 3China: Local Government Debt Maturity Schedule

China Geopolitical Outlook 2022

China Geopolitical Outlook 2022

Chart 19Policy Support Expected For 20th Party Congress

Policy Support Expected For 20th Party Congress

Policy Support Expected For 20th Party Congress

Note: An error in an earlier version of this report has been corrected. Chinese fixed asset investment in Chart 19 is growing at 0.1%, not 57.6% as originally shown. The chart has been adjusted. Matt Gertken Chief Geopolitical Strategist mattg@bcaresearch.com Yushu Ma Research Associate yushu.ma@bcaresearch.com Footnotes 1 See Bei Hu and Bloomberg, “Ray Dalio thinks the U.S. needs more of China’s common prosperity drive to create a ‘fairer system,’” Fortune, January 10, 2022, fortune.com. 2 See George Soros, “China’s Challenges,” Project Syndicate, January 31, 2022, project-syndicate.org. 3 The 5-year LPR had remained unchanged after the December 2021 cut. At that time, only the 1-Year LPR was cut by 5bps. Furthermore, the different magnitudes of the January 20 LPR cut also have some implications. The 1-Year LPR mostly affects new and outstanding loans, short-term liquidity loans of firms, and consumer loans of households. In comparison, the 5-Year LPR has a larger impact, affecting the borrowing costs of total social financing, including mortgage loans, medium- to long-term investment loans, etc. The MLF rate was cut by 10 basis points on January 17; in theory the LPR should also be cut by the same size. However, the 5-Year LPR adjustments was very cautious and was only cut by 5 bps, smaller than the MLF cut and the 1-Year LPR cut. The 5-year LPR serves as the benchmark lending rate for mortgage loans. 4 To combat the negative shock caused by the initial outburst of COVID-19, altogether China lowered the MLF and 1-year LPR by 30 bps and 5-year LPR by 15 bps in H1 2020. This also suggests that there is still room for future interest rate cuts or RRR cuts in the coming months. Strategic Themes Open Tactical Positions (0-6 Months) Open Cyclical Recommendations (6-18 Months)

Dear client, In lieu of our weekly bulletin next week, I will be hosting a webcast on Friday, January 28 at 11:00 am EST, to discuss recent dollar trends. I hope you all tune in. Kind regards, Chester Ntonifor Highlights While not often discussed, it is well known that the dollar is expensive. It is true that valuations tend to matter less until they trigger a tipping point. Such inflections usually coincide with huge external imbalances, especially generated by an overvalued exchange rate. The US dollar could be stepping into such a paradigm - the DXY is 1.5 standard deviations above fair value, at the same time as the goods trade deficit is hitting record lows, and real interest rates are deeply negative. More importantly, there has been limited precedence to such a dollar configuration. Historically, it has required much higher real interest rates, or an improving balance of payments backdrop, to justify such lofty valuations. Our trading model shows that selling a currency when it is expensive and buying it when it is cheap generates excess returns over time. Within our valuation ranking, the cheapest currencies are JPY, SEK and NOK. On a terms-of-trade basis, the AUD stands out as a winner. Feature Chart 1High Dollar Valuation And Ultra-Low Real Rates Is Unprecedented

High Dollar Valuation And Ultra-Low Real Rates Is Unprecedented

High Dollar Valuation And Ultra-Low Real Rates Is Unprecedented

Valuations usually get little respect when it comes to medium-term currency movements. This has been especially the case over the last few years, where the macroeconomic environment has been by far the biggest driver of the US dollar. The bull market in the dollar from 2011 to 2020 coincided with higher real interest rates in the US, relative to the rest of the developed world. In fact, since 2008, no developed market central bank has been able to hike rates by more than 200bps, except for the US Federal Reserve. Our report last week focused on why aggressive interest rate increases by the Federal Reserve could be bullish for the US dollar in the short term, but eventually set the stage for depreciation. In this report, we argue that valuations will also become a more important factor for currency strategy over the next 1-2 years (Chart 1). The Dollar And The External Balance The framework to understand currencies and the external balance is straightforward - a rising trade deficit (imports > exports) requires a lower exchange rate to boost competitiveness in the manufacturing sector, or less spending to reduce the trade deficit. Reduced domestic spending is unlikely in most developed economies, given ample pent-up demand and loose fiscal policy. Therefore, the natural adjustment mechanism for countries running wide trade deficits will have to be the exchange rate. Within a broad spectrum of developed and emerging market currencies, the US dollar stands out as overvalued on a real effective exchange rate basis (Chart 2A and 2B). It is true that valuations tend to matter less until they trigger a tipping point. Such inflections usually occur with a shift in animal spirits, coinciding with huge external imbalances.

Chart 2

Chart 2

In the US, these imbalances are already starting to trigger a shift. The US trade deficit is deteriorating, with the goods deficit hitting a record low of -$98bn in November. Over the last few years, it has become increasingly difficult to fund this widening trade deficit via foreign purchases of US Treasuries (Chart 3). Meanwhile, as we highlighted last week, substantial equity inflows over the last few years have started to roll over. In a nutshell, the basic balance in the US (the sum of the current account and foreign direct investment) is deteriorating at an accelerated pace (Chart 4). The US current account deficit for Q3 came in at -$214.8 billion, the widest in over a decade. This has reversed a lot of the improvement in the basic balance since the Global Financial Crisis. The dollar tends to decline on a multi-year basis when the basic balance peaks and starts deteriorating. Chart 4Deteriorating Balance Of Payments Dynamics US Balance Of Payments

Deteriorating Balance Of Payments Dynamics US Balance Of Payments

Deteriorating Balance Of Payments Dynamics US Balance Of Payments

Chart 3It Is Becoming Increasingly Difficult To Fund The Widening Deficit

It Is Becoming Increasingly Difficult To Fund The Widening Deficit

It Is Becoming Increasingly Difficult To Fund The Widening Deficit

Fiscal policy is likely to become tighter in the next couple of years, easing the domestic spending constraint for the exchange rate. That said, fiscal policy will remain loose compared to pre-pandemic levels and relative to underlying employment conditions. This has historically led to a deterioration in the external balance and pulled the real effective exchange rate of the dollar down (Chart 5). Chart 5The Dollar And The Budget Deficit

The Dollar And The Budget Deficit

The Dollar And The Budget Deficit

Real Interest Rates And The Dollar It is remarkable that at a time when real rates are the most negative in the US, the dollar is as overvalued as it has been in decades on a simple PPP model. This is a perfect mirror image of the dollar configuration at the start of the bull market in 2010, where the dollar was cheap and real rates were more supportive (Chart 1). According to economic theory, a currency should adjust to equalize returns across countries. This is a no-arbitrage condition. In the early 80s, an overvalued dollar was supported by very positive real rates. The subsequent dollar declines thereafter also coincided with falling real interest rates. In fact, over the last decade, it has been an anomaly that the dollar is so strong despite relative real interest rates being so negative (Chart 6). Our view remains that the terminal interest rate for the US should be higher than what is currently discounted in the 10-year Treasury yield. According to the overnight index swap curve, the Fed will not hike interest rates past 1.75%. This is much lower than past cycles and will keep real interest rates low. This does not justify an expensive greenback. Our shorter-term interest rate model also shows the DXY as slightly expensive, even though short-term interest rates have moved in favor of the dollar over the past year (Chart 7). Chart 6The Level Of Relative Real Yields Also Matters

The Level Of Relative Real Yields Also Matters

The Level Of Relative Real Yields Also Matters

Chart 7Our Timing Model Suggests ##br##A Pullback

Our Timing Model Suggests A Pullback

Our Timing Model Suggests A Pullback

Other Considerations While real effective exchange rates and purchasing power parity models are among our favorite valuation gauges, they are not foolproof. Countries with structurally higher inflation (and so a higher real effective exchange rate), could also have higher productivity. According to the Balassa-Samuelson Hypothesis, competitiveness in the tradeable goods sector will boost wages across all sectors of the economy, leading to higher prices. This argument particularly resonates with proponents that suggest the US is a fast-growing economy, and so will tend to run a current account deficit, like Australia during the commodity boom of the early 2000s. Meanwhile, the US earns more on its overseas assets than it spends on its liabilities, suggesting that the funding gap will eventually close. Unfortunately, the overvaluation of the dollar has not been due to higher relative productivity in the US, especially when compared to other economies. Across a broad spectrum of developed and emerging market economies, the dollar is expensive according to our productivity models. The Chinese RMB (which is much overvalued on a PPP basis) is closer to fair value when productivity is taken into consideration (Chart 8).

Chart 8

Meanwhile, the sizeable US deficit is not completely offset by its positive investment balance (Chart 9). This is occurring at a time when many faster growing countries (such as China for example) are generating current account surpluses (Chart 10A and 10B). In a nutshell, whether one looks at relative price levels, relative productivity trends, or relative real returns on government assets, the dollar is expensive. Chart 9The Positive Income Balance Has Not Helped The Us Investment Position

The Positive Income Balance Has Not Helped The Us Investment Position

The Positive Income Balance Has Not Helped The Us Investment Position

Chart 10

Chart 10

Conclusion Last summer, we introduced a trading model for FX valuation enthusiasts. We used both our in-house purchasing power parity models (PPP) and our intermediate-term timing models as valuation tools. Since the 2000s, both valuation models have outperformed a buy-and-hold currency strategy with much lower volatility (Chart 11). Currency valuation tends to matter over the longer term, while the macro environment tends to dominate short-term currency trading. Given that the dollar has been overvalued for the last three to five years, the above analysis suggests we might be entering this “longer-term” tipping point where valuations will start to matter more going forward. Within our valuation ranking, the cheapest currencies are JPY, SEK and NOK. On a terms-of-trade and productivity basis, the AUD stands out as a winner. This is being reflected in a record-high basic balance surplus (Chart 12). In our trade tables, we went long AUD at 70 cents, and will upgrade this to a high conviction bet on signs that currency volatility is ebbing. Chart 11A Trading Rule Solely Based On Valuation

A Trading Rule Solely Based On Valuation

A Trading Rule Solely Based On Valuation

Chart 12AUD And Balance Of Payments

AUD And Balance Of Payments

AUD And Balance Of Payments

Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Trades & Forecasts Strategic View Tactical Holdings (0-6 months) Forecast Summary

Highlights The most important question is whether the Fed will hike interest rates by more than what is currently discounted in markets, or less. More hikes will trigger a set of cascading reactions. US bond yields will initially jump, boosting the dollar. But this process could also undermine growth stocks, and the US equity market leadership. Equity portfolio flows have been more important in financing the US trade deficit, than Treasury purchases, since 2020. Hence, a reversal in these flows will undermine a key pillar of support for the dollar. On the flip side, less rate hikes will severely unwind higher interest rate expectations in the US vis-a-vis other developed markets, especially in the euro area and Japan. This means we could be witnessing a shift in the dollar, where upside is capped, and downside is substantial. Feature Chart 1The Dollar In 2021

The Dollar In 2021

The Dollar In 2021

The two most important drivers of the dollar over the last few months have been the spread between US interest rates and other developed markets, as well as the relative performance of US equities (Chart 1). Rising interest rate expectations in the US have led to substantial speculative flows into the US dollar. The outperformance of the US equity market has also coincided with notable portfolio inflows into US equities in 2021. This cocktail of macro drivers has pinned the US dollar in a quandary. If rates rise substantially in the US, and that undermines the US equity market leadership, the dollar could suffer. If US rates rise by less than what the market expects, record high speculative positioning in the dollar will surely reverse. The Dollar And The Equity Market The traditional relationship between the dollar and the equity market was negative for most of the first half of the pandemic. Monetary easing by the Federal Reserve stimulated global financial conditions setting the stage for an epic bull market. The correlation between the S&P 500 and the DXY index was a near perfect inverse correlation for much of 2020 (Chart 2). Chart 3US Equity Portfolio Inflows Have Been Substantial Since 2020

US Equity Portfolio Inflows Have Been Substantial Since 2020

US Equity Portfolio Inflows Have Been Substantial Since 2020

Chart 2The Dollar In ##br##2020

The Dollar In 2020

The Dollar In 2020

The big change in 2021 is that this correlation has shifted, as the Fed has pivoted on monetary policy. This means that investors have been betting on higher stock prices in the US, as well as higher interest rates. In short, portfolio flows into US equities have surged (Chart 3). For the long-duration US equity market, higher interest rates could push it to a tipping point, where it starts to underperform other developed market bourses. This will reverse these equity portfolio flows, hurting the dollar in the process. Profits, Interest Rates And The Dollar The key driver of equity markets is profits in the short run, with valuation starting to matter over the longer run. This in turn becomes the key driver of cross-border equity flows. These flows help dictate currency movements. For much of the previous decade, US profits did much better than overseas earnings. For this reason, the US equity market outperformed, pulling the dollar up, as foreign equity purchases accelerated (Chart 4). The post-pandemic era has seen inflation rising across the world, changing the paradigm for US profits. High inflation, and consequently, higher bond yields, have been synonymous with an underperformance of US profits (Chart 5). Banks profit from higher rates, as they benefit from rising net interest margins. Materials, energy, and industrial stocks, benefit from higher inflation via rising commodity prices that boost their pricing power. In a nutshell, rising inflation tends to be better for value stocks and cyclicals, sectors that are underrepresented in the US. This means portfolio flows into US equities, one of the key drivers of the capital account surplus, could be on the cusp of a substantial reversal. Chart 4The Dollar And Relative Profits

The Dollar And Relative Profits

The Dollar And Relative Profits

Chart 5Bond Yields And Relative Profits

Relative Profits And Bond Yields

Relative Profits And Bond Yields

Second, valuation in the US has become extended as interest rates have fallen. More importantly, US valuations have been more sensitive to changes in interest rates, compared to other developed markets (Chart 6). This is because the US stock market has become increasingly overweight long duration sectors, like technology and healthcare. Higher rates will undermine the valuation premium these sectors command. This will cause the US equity market to derate relative to other cyclical bourses. Chart 6Relative Multiples And Bond Yields

Relative Multiples And Bond Yields

Relative Multiples And Bond Yields

The key point is that the US equity market has been the darling of the last decade, and leadership is at risk from higher rates, via a reset in both relative valuation and relative profits. So, while the US market could perform well in 2022, higher rates could undermine its relative performance to overseas bourses. This will curtail equity portfolio inflows, as capital tends to gravitate to markets with higher expected returns. The Dollar And Relative Interest Rates Over the long term, bond flows are the overarching driver of the currency market. Most market participants expect the Fed to be among the most hawkish in 2022. This is clear in the pricing of the Eurodollar versus Euribor December 2022 contract, or just the relative path of two-year US bond yields versus other markets. This in turn has helped drive speculative positioning in the US dollar towards record highs (Chart 7). Correspondingly, US Treasury inflows have accelerated in recent months, even though real interest rates have not risen that much (Chart 8). In level terms, the trade deficit (that hit a record low of -US$80bn in November) is being helped financed by renewed foreign interest in US Treasurys. Chart 8Interest Rates And Treasury Flows

Interest Rates And Treasury Flows

Interest Rates And Treasury Flows

Chart 7Record Dollar Speculative Positions

Record Dollar Speculative Positions

Record Dollar Speculative Positions

We see two major contradictions in the pricing of US interest rates, relative to other developed markets. First, rising inflation is a global phenomenon and not specific to the US. If inflation proves sticky, other central banks will turn a tad more hawkish to defend their policy mandates. If inflation subsides, the Fed might not be as aggressive in tightening policy as the market expects. This will unwind speculative long positions in the dollar. It will also slow portfolio inflows into US Treasuries. Second, the reality is that outside the ECB and the BoJ, most other developed market central banks have already tightened monetary policy ahead of the Fed. The ability of any central bank to tighten policy will depend on the health of the labor market, and the potential for a wage inflation spiral. One data point that has caught our attention is the participation rate across G10 economies - it is notable that the US has one of the lowest participation rates (Chart 9A). Given that many countries have seen their participation rate recover to pre-pandemic levels, it suggests upside in the US rate. This will be especially the case if fiscal stimulus, which could wane, has been a key reason why the US participation rate has stayed low. In a nutshell, the low participation rate in the US could be a reason the Fed lags market expectations for aggressive rate increases this year. On the flip side, a higher participation rate in places like Canada, Norway, and Australia, could allow their central banks to normalize policy faster than the market expects. There has been a loose correlation between relative changes in the participation rate, and relative changes in inflation across G10 economies (Chart 9B). Chart 9BThe US Relative Participation Rate And Relative Inflation

The US Relative Participation Rate And Relative Inflation

The US Relative Participation Rate And Relative Inflation

Chart 9AUS Labor Force Participation Is Low, But Improving

US Labor Force Participation Is Low, But Improving

US Labor Force Participation Is Low, But Improving

Finally, relative monetary policy tends to be driven by relative growth. US growth remains robust but has been rolling over relative to other developed markets (Chart 10). This is occurring at a time when China is easing monetary policy, which tends to buffet non-US growth. Higher non-US growth could also tip the bond and currency market narrative that the Fed will tighten much faster than other G10 central banks. Chart 10Non-US Growth Is Improving, Relative To US Growth

Non-US GROWTH Is Improving, Relative To US Growth

Non-US GROWTH Is Improving, Relative To US Growth

Conclusion The above analysis suggests we could be entering a paradigm shift in the dollar, where any response by the Fed could eventually trigger the same outcome. Higher rates than the market expects will initially boost the US dollar. But this process will also undermine the US equity market leadership, reversing substantial portfolio inflows in recent years. On the flip side, fewer rate hikes will severely unwind higher rate expectations in the US vis-a-vis other developed markets. Our concluding thoughts from our 2022 outlook, which are consistent with our views herein, were as follows: The DXY could touch 98 in the near term but will break below 90 over the next 12-18 months. An attractiveness ranking reveals the most appealing currencies are JPY, SEK, and NOK, while the least attractive are USD and NZD. Policy convergence will be a key theme at the onset of 2022. Stay long EUR/GBP and AUD/NZD as a play on this theme. Look to buy a currency basket of oil producers versus consumers. We went long the AUD at 70 cents. Terms of trade are likely to remain a tailwind for the Australian dollar. The AUD will benefit specifically in a green revolution. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Trades & Forecasts Strategic View Tactical Holdings (0-6 months) Forecast Summary

Highlights We introduce a novel concept called the ‘wealth impulse’, which describes the counterintuitive relationship between wealth and economic growth. To the extent that GDP growth is impacted by wealth, the impact comes not from the level of wealth or from the change in wealth, but from the change in the increase in wealth – which we define as the wealth impulse. The global wealth impulse has entered a downcycle, which tends to last 1-2 years. Previous downcycles in the wealth impulse in 2010-11, 2013-14, and 2018-19 all coincided with US economic growth falling to, or remaining at, below-trend. A similar pattern could emerge through 2022-23. Previous downcycles in the wealth impulse also coincided with strong down-legs in the 30-year T-bond yield. This supports our view that while the long bond yield could rise by a further 40-50 bps, the recent spike in yields is simply a tactical countertrend move within a broader structural downtrend, which remains intact. Fractal trading watchlist: Bitcoin, the euro, EUR/CZK, semiconductors, and Polish 10-year bonds. Feature Feature ChartThe 'Wealth Impulse' Has Peaked

The 'Wealth Impulse' Has Peaked

The 'Wealth Impulse' Has Peaked

The post-pandemic synchronized boom in global house prices and global stock markets has caused an unprecedented windfall in household wealth. Albeit, it is a windfall that is highly concentrated in the top fraction of the world’s households. Many commentators claim that this unprecedented wealth windfall will boost economic growth in 2022-23 through the so-called ‘wealth effect’. However, these claims belie a basic misunderstanding about how wealth impacts economic growth. In this short Special Report, we introduce a novel concept called the ‘wealth impulse’, which describes the true relationship between wealth and economic growth. Using this concept of the wealth impulse we explain why, somewhat counterintuitively, wealth will be a headwind rather than a tailwind to growth in 2022-23 (Chart I-1). It Is The ‘Impulse’ Of Wealth That Drives Growth, And The Impulse Has Peaked In accounting terms, wealth is a stock. By contrast, GDP is a change in a stock, or flow, meaning that GDP growth is a change in a flow. It follows that, to the extent that GDP growth is impacted by wealth, it must also come from the change in the flow of wealth: in other words, not from the level of wealth and not from the change in wealth, but from the change in the increase in wealth. We define this as the ‘wealth impulse’ (Charts 1-2-Chart 1-5) Chart I-2The Level Of Real Estate Wealth Has Surged…

The Level Of Real Estate Wealth Has Surged...

The Level Of Real Estate Wealth Has Surged...

Chart I-3…But The Impulse Is Fading

...But The Impulse Is Fading

...But The Impulse Is Fading

Chart I-4The Level Of Stock Market Wealth Has Surged…

The Level Of Stock Market Wealth Has Surged...

The Level Of Stock Market Wealth Has Surged...

Chart I-5...But The Impulse Is Fading

...But The Impulse Is Fading

...But The Impulse Is Fading

To be clear, your stock of wealth will also generate a flow through dividends, rents, and interest income. And the higher the level of your wealth, the larger this flow will be – Bill Gate’s flow is much larger than Joe Sixpack’s flow. But given that these income flows are dwarfed by the capital gains flows, they will play second fiddle for all-important spending growth. If all of this sounds somewhat convoluted, let’s illuminate the concept with a simple example. Say that your starting wealth of $1000 increased by $100 in 2020, and by another $100 in 2021. In this case, you have effectively gained a constant additional ‘capital gain’ flow to your income flow. Let’s say you spent a constant tenth of these capital gain flows. What would be the growth in your spending? The counterintuitive answer is zero. As there is no change in these capital gain flows, the wealth impulse would be zero, and there would be no growth in your spending: it would be $10 in 2020 and $10 in 2021. To get economic growth from the wealth effect, the increase in your wealth in 2021 would have to be greater than the $100 increase in 2020. Let’s say the increase was $150. In this case, the wealth impulse would be 50 percent and your spending would grow from $10 to $15.1 Now let’s say that after this $150 increase in 2021, your wealth increased by $200 in 2022. Given that the 2022 increase was greater than the 2021 increase, the wealth impulse would be positive, and your spending would grow. But what about the rate of growth? The counterintuitive answer is that economic growth would slow, because the wealth impulse has declined to 33 percent (200/150) in 2022 from 50 percent (150/100) in 2021. To the extent that GDP growth is impacted by wealth, it must come from the change in the increase in wealth, which we define as the ‘wealth impulse’. Finally, let’s say that your wealth increased by a further $150 in 2023. In this case, the wealth impulse would turn negative, to -25 percent (150/200). The counterintuitive thing is that, despite an increase in wealth, your spending would contract. In fact, this is precisely what is happening in the real world. The wealth impulse peaked in the second half of 2021, and has entered a downcycle. Significantly, downcycles in the wealth impulse tend to last 1-2 years, and end up in deeply negative territory. Hence, contrary to what the commentators are claiming, the ‘wealth effect’ tailwind to growth is already fading, and is highly likely to become a headwind through 2022-23. Creating A Composite Wealth Impulse By far the largest component of household wealth is real estate, meaning the value of our homes. Significantly, through the past decade, global real estate prices have become highly synchronized and correlated. Hence, we can derive a real estate wealth impulse from a reliable monthly US house price index, such as the S&P/Case-Shiller Home Price Index. One rejoinder is that real estate wealth should be measured net of the mortgage debt that is owed on our homes. However, as the wealth impulse is a change of a change in wealth, and the mortgage debt changes very slowly, it does not really matter whether we calculate the impulse from gross or net real estate wealth. Either way, the impulse is fading. The wealth impulse peaked in the second half of 2021, and has entered a downcycle. The other significant component of household wealth comes from the exposure to equities. Hence, we can derive an equity wealth impulse using a broad equity index such as the MSCI All Country World. Significantly, the equity wealth impulse also peaked in 2021 and has already fallen to zero. We can then create a ‘composite’ wealth impulse which combines real estate and equities in the three to one proportion that households hold these two main assets. Unsurprisingly, this composite wealth impulse is also fading fast (Chart I-6). Chart I-6The Composite Wealth Impulse Has Peaked

The Composite Wealth Impulse Has Peaked

The Composite Wealth Impulse Has Peaked

One final issue relates to the periodicity of calculating the wealth impulse. All the analysis so far has related to the 1-year impulse: that is, the 1-year change in the 1-year increase in wealth. This periodicity should match the time that it takes for wealth changes to impact household behaviour. Based on theoretical and empirical evidence, the optimal periodicity is indeed around a year – especially as we also assess the change in our incomes and taxes over a year. But what if households react faster to the change in their wealth? We can address this by looking at the 6-month wealth impulse: that is, the 6-month change in the 6-month increase in wealth. These 6-month impulses for both real estate wealth and composite wealth are already deeply in negative territory (Chart I-7 and Chart I-8). Chart I-7The 6-Month Real Estate Wealth Impulse Has Turned Negative

The 6-Month Real Estate Wealth Impulse Has Turned Negative

The 6-Month Real Estate Wealth Impulse Has Turned Negative

Chart I-8The 6-Month Composite Wealth Impulse Has Turned Negative

The 6-Month Composite Wealth Impulse Has Turned Negative

The 6-Month Composite Wealth Impulse Has Turned Negative

What Does A Wealth Impulse Downcycle Mean? There are several drivers of economic growth and the wealth impulse is a marginal player amongst these drivers. Still, while the wealth impulse may not be the overarching cause of growth, it does have the potential to amplify the growth cycle in either direction. Downcycles in the wealth impulse have coincided with strong down-legs in the 30-year T-bond yield. In this regard, it is notable that in the post-GFC era, upcycles in the wealth impulse have coincided with accelerations in US economic growth. Whereas downcycles in the wealth impulse through 2010-11, 2013-14, and 2018-19 have all coincided with growth falling to, or remaining at, below-trend. A similar pattern could emerge through 2022-23, in stark contrast to what many commentators are predicting (Chart I-9). Chart I-9Wealth Impulse Downcycles Coincide With Fading Or Sub-Par Growth

Wealth Impulse Downcycles Coincide With Fading Or Sub-Par Growth

Wealth Impulse Downcycles Coincide With Fading Or Sub-Par Growth

Unsurprisingly, the post-GFC downcycles in the wealth impulse have also coincided with strong down-legs in the 30-year T-bond yield. This supports our view that while the long bond yield could rise by a further 40-50 bps, the recent spike in yields is simply a tactical countertrend move. The broader structural downtrend in the long bond yield remains intact (Chart I-10). Chart I-10Wealth Impulse Downcycles Coincide With Down-Legs In The 30-Year T-Bond Yield

Wealth Impulse Downcycles Coincide With Down-Legs In The 30-Year T-Bond Yield

Wealth Impulse Downcycles Coincide With Down-Legs In The 30-Year T-Bond Yield

Fractal Trading Watchlist From this week, we are pleased to introduce a new section: a fractal trading ‘watchlist’, which will highlight investments that are approaching, but not yet at, points of fractal fragility that presage upcoming turning points. This will help to prepare future trades. In the starting watchlist, we highlight potential upcoming buying opportunities for bitcoin, the trade-weighted euro, and EUR/CZK, and an upcoming selling opportunity for semiconductors versus technology. Catching our eye this week though is the very aggressive sell-off in Polish government bonds relative to their peers. Inflation has surged everywhere, including in Poland, but the inflation rate in Poland remains below that in the US. This means that the massive underperformance of Polish bonds seems overdone, confirmed by an extremely fragile 260-day fractal structure (Chart I-11). Chart I-11The Underperformance Of Polish Bonds Is Overdone

The Underperformance Of Polish Bonds Is Overdone

The Underperformance Of Polish Bonds Is Overdone

Accordingly, the recommended trade would be to overweight Polish 10-year bonds versus US 10-year T-bond (or German 10-year bunds), setting the profit-target and symmetrical stop-loss at 8 percent. Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List

Fractal Trading Watch List