Money Trends / Liquidity

Highlights The odds of a continued earnings contraction have not yet fallen to the point that would warrant an overweight stance towards Chinese versus global stocks over the coming 6-12 months. While we maintain Chinese stocks on upgrade watch and may recommend increasing exposure soon, the bottom line for investors is that it is still too early for us to confidently project a sustained uptrend. While most investors attribute the chronic discount of Chinese stocks relative to the global average as being due to a sizeable equity risk premium, our analysis suggests that China’s low payout ratio and mediocre earnings growth are the true causes. This implies that China’s re-rating potential is capped barring a major structural improvement in earnings growth. Investors should pay close attention to the details of a U.S./China currency stability pact that will reportedly be included in any trade deal between the two countries. Such a pact may set up an important natural experiment for CNY/USD, and could be a revelatory event for China’s exchange rate regime. Feature Last week’s FOMC meeting dominated the headlines of the financial press, and for good reason. The Fed surprised investors with a material downgrade to their expected path of the federal funds rate over the next three years, a shift that largely reflected concerns about global growth. The subsequent inversion of the U.S. 10-year / 3-month yield curve in response to the very disappointing euro area flash manufacturing PMI for March confirms that many investors remain convinced that Fed policy is too tight and that easing is likely over the coming year.1 On the positive side, investor concerns that reflationary policy is needed in the U.S. and euro area are likely overblown: the plunge in the euro area PMI at least in part reflects the near-term uncertainty over the possibility of a hard Brexit (which will probably be avoided), whereas the Fed is pausing at a level of real interest rates that is well below real GDP growth, which means that monetary policy is still stimulative for the U.S. economy (Chart 1). Chart 1U.S. Monetary Policy Is Still Stimulative

U.S. Monetary Policy Is Still Stimulative

U.S. Monetary Policy Is Still Stimulative

But Chart 2 highlights that a generalized slowdown in global growth is responsible for at least part of the sharp weakness in Chinese export growth over the past few months, which we had been mostly attributing to a catch-up phase following a (perversely and ironically) beneficial tariff front-running effect that had temporarily boosted trade growth last year. Chart 2Global Weakness At Least Partly Responsible For A Sharp Export Slowdown

Global Weakness At Least Partly Responsible For A Sharp Export Slowdown

Global Weakness At Least Partly Responsible For A Sharp Export Slowdown

Ongoing weakness in the global economy, were it to persist, would imply that China’s external demand outlook is even less encouraging than we had previously assumed. This would raise the stakes for a trade deal with the U.S. to be agreed upon soon, as well as a continued uptrend in the pace of Chinese credit growth. Investors should closely watch the new export orders component of the March NBS manufacturing PMI later this week for signs that exporter sentiment is improving, as well as the overall Caixin PMI to confirm that smaller firms continue to benefit from the PBOC’s targeted easing efforts. When Should Investors Upgrade Chinese Stocks On A Cyclical Basis? In our view, most global investors have been focused on the wrong risk factor for Chinese stocks for the better part of the past year. In the wake of the near-vertical February rise in Chinese domestic stocks, the most common question we have received from clients is whether they should be increasing their cyclical exposure to Chinese stocks in general, and A-shares in particular. In response to the January surge in credit we placed Chinese stocks on upgrade watch in our February 27 Weekly Report,2 but we are not yet ready to recommend an outright cyclical overweight. Investors should be at the ready and aiming, but should not yet fire. In our view, most global investors have been focused on the wrong risk factor for Chinese stocks for the better part of the past year. We have noted in several previous reports that investors have focused nearly exclusively on the U.S.-China trade war since the beginning of 2018, and have largely ignored a slowing domestic economy (Chart 3). Given this, it is not surprising that a sharp improvement in the odds of a deal (which occurred at the beginning of November) has led to a material rally over the past few months versus global stocks. Chart 3The Prospect Of A Trade Deal Has Been The Primary Driver Of China-Related Assets

The Prospect Of A Trade Deal Has Been The Primary Driver Of China-Related Assets

The Prospect Of A Trade Deal Has Been The Primary Driver Of China-Related Assets

In fact, we predicted in our December 5 Weekly Report that positive sentiment about a deal would boost the relative performance of Chinese stocks over the coming few months, and recommended a tactical overweight stance at that time.3 A cyclical (i.e. 6-12 month) overweight, however, is a different story. Sentiment alone rarely drives financial markets over a 1-year time horizon, meaning that investors need to have some degree of confidence that domestic demand will meaningfully improve over the next 12 months to justify a cyclical upgrade. Certainly, we acknowledge that there have been several positive developments pointing to such an outcome. Chinese monetary conditions have become extremely easy, credit is no longer contracting and surged in January, the Caixin PMI rose notably in February, and some form of a trade deal remains the most likely outcome of the ongoing talks. In addition, Chinese stocks still remain significantly below their 2018 peak (Chart 4), meaning that there is still material potential upside if Chinese earnings do not contract. Chart 4Chinese Stocks Still Have Room To Rise If The Earnings Outlook Stabilizes

Chinese Stocks Still Have Room To Rise If The Earnings Outlook Stabilizes

Chinese Stocks Still Have Room To Rise If The Earnings Outlook Stabilizes

A moderate credit expansion appears to be underway, but coincident activity continues to weaken and earnings appear to have more downside. However, there are also several reasons to be cautious cyclically: Chart 5The Past Three Months Imply A Moderate Credit Uptrend

The Past Three Months Imply A Moderate Credit Uptrend

The Past Three Months Imply A Moderate Credit Uptrend

Chart 6Chinese Coincident Economic Activity Continues To Weaken

Chinese Coincident Economic Activity Continues To Weaken

Chinese Coincident Economic Activity Continues To Weaken

Chinese and U.S. policymakers have not only failed to set a date for an agreement to be signed by President’s Xi and Trump, but recent new reports suggest that momentum may be slowing and that a meeting may be postponed until June or later.4 Even if the deal does not fall through, material further delays could cause investors to get anxious and vote with their feet. Such a selloff could be violent, given the extremely sharp rise in domestic stock prices over the past six weeks. The evidence so far points to a moderate expansion in credit (Chart 5), reflecting the fact that policymakers are still somewhat concerned about financial stability and the need to prevent significant further leveraging of the private sector. This means that the odds are not yet in favor of a credit “overshoot” like what occurred in 2015/2016, implying that the pickup in growth is likely to be comparatively weaker this time around. Since 2010, monetary conditions and money & credit growth appear to be the best predictors of investment-relevant Chinese economic activity.5 While a moderate credit expansion appears to be underway, there has been no discernable pickup in money growth.6 This discrepancy likely means that the recent improvement in credit has occurred due to non-bank financial institutions, further suggesting that this economic recovery will probably be less powerful and less broad-based than during past cycles. While a moderate expansion in credit does suggest that China’s economy will bottom at some point in the coming months, coincident economic activity continues to decelerate (Chart 6). A continuation of this trend, particularly if coupled with an investor “crisis of faith” in the trade talks, could lead to a very significant retracement in Chinese equity prices before durably bottoming for the year. Trailing EPS growth is decelerating, but it has yet to contract on a year-over-year basis as would be implied by the net earnings revisions ratio (Chart 7) and the coincident activity indicators shown in Chart 6. Chinese investable EPS fell 30% during the 2015/2016 episode (20% for domestic stocks), implying meaningful further downside even if economic activity does not weaken as significantly over the coming months. Chart 7Net Earnings Revisions Point To More Downside For Earnings

Net Earnings Revisions Point To More Downside For Earnings

Net Earnings Revisions Point To More Downside For Earnings

Chart 8 presents a helpful way for investors to make a net assessment of all of the factors highlighted above. The chart shows our earnings recession model for the MSCI China Index, and shows what is likely to occur if a trade deal causes a full recovery in Chinese exporter sentiment, China’s export-weighted RMB stays roughly at current levels, and the very recent pace of credit growth (Dec-Feb) continues along its trend. Chart 8A Trade Deal And A Moderate Credit Expansion Will Likely Stabilize The Earnings Outlook

A Trade Deal And A Moderate Credit Expansion Will Likely Stabilize The Earnings Outlook

A Trade Deal And A Moderate Credit Expansion Will Likely Stabilize The Earnings Outlook

This scenario, were it to occur, would reduce the odds of a continued earnings contraction to the point that we would be comfortable recommending an overweight stance towards Chinese versus global stocks over the coming 6-12 months. While such a recommendation could come as soon as mid-April, the bottom line for investors is that it is still too early for us to confidently project this outcome. Should Chinese Stocks Be Priced At A Premium Or A Discount To Global Stocks? Most investors attribute the discount applied to Chinese stocks to a high equity risk premium (ERP), but our work paints a different picture. Besides questions about the appropriate cyclical allocation to Chinese stocks, the recent spike in interest among global investors towards A-shares has also led to a renewed focus about the degree to which Chinese stocks are cheap versus the global average. In a world where many financial assets are chronically expensive and Chinese policymakers appear to be responding to weaker economic activity, some investors question whether Chinese stocks deserve to be priced at a discount (Chart 9). Our sense is that most investors attribute the discount to a high equity risk premium (ERP) stemming from the enormous rise in Chinese non-financial corporate debt over the past decade, but our research paints a different picture. Chart 9The Chinese Equity Discount: A High ERP, Or Something More Sinister?

The Chinese Equity Discount: A High ERP, Or Something More Sinister?

The Chinese Equity Discount: A High ERP, Or Something More Sinister?

One way of analyzing the risk premium of an equity market is to use the well-known constant Gordon growth model. Equation 1 below presents the theoretically justified 12-month trailing P/E ratio as a function of the payout ratio, the risk-free rate, the ERP, and the long-term dividend growth rate (which is equal to the long-term earnings growth rate given a constant payout ratio). Equations 2 and 3 re-arrange equation 1 to express the ERP and long-term growth rate, respectively, on the left-hand side of the equation. Equation 1: P0/E0 = (D1/E0)/(rf + ERP – g) Equation 2: ERP = [(D1/E0)/(P0/E0)] + g - rf Equation 3: g = rf + ERP-[(D1/E0)/(P0/E0)] To illustrate the approach, Chart 10 applies equation 2 to the U.S. equity market and compares it with the annual dividend discount model equity risk premium published by Professor Aswath Damodaran from New York University’s Stern School of Business,7 a well-known expert in the theory and practice of asset valuation. While there are some differences in the level of the series owing to slightly different methodologies, the overall profile of the two series is generally similar. Chart 10Our DDM Methodology For The U.S. Generates Results Similar To Other Important Estimates

Our DDM Methodology For The U.S. Generates Results Similar To Other Important Estimates

Our DDM Methodology For The U.S. Generates Results Similar To Other Important Estimates

Proxying the market’s long-term growth expectations in a large, mature economy such as the U.S. is materially easier than is the case in an emerging market such as China. As such, instead of solving for the equity risk premium directly when judging whether China’s discount is “deserved”, we use equation 3 to solve for the implied long-term growth rate given an assumed (and very conservative) ERP range of 2-3%, using the global P/E ratio. In other words, we ask the following question: what kind of earnings growth do Chinese stocks need to achieve over the long run in order to justify the same earnings multiple as the global average, given an equity risk premium of 2-3%? Chart 11 presents the answer to this question, for both the domestic and the investable market. We use domestic 10-year bond yields as the risk-free rate in the case of the A-share market, and U.S. 10-year bond yields in the case of the MSCI China index as a proxy for the global risk-free rate. Finally, in each panel, the dashed horizontal lines denote the actual compound annual growth rate in earnings per share for each market, since the year noted next to each line. Chart 11A Low But Still Difficult L/T Earnings Hurdle Rate To Be Priced In Line With Global Stocks

A Low But Still Difficult L/T Earnings Hurdle Rate To Be Priced In Line With Global Stocks

A Low But Still Difficult L/T Earnings Hurdle Rate To Be Priced In Line With Global Stocks

Two important points are apparent from the chart: The required growth rate for both markets to be priced in line with global stocks are quite low, well below Chinese nominal GDP growth. At first blush, this might suggest that the valuation discount applied to China reflects a sizeable equity risk premium that could shrink over the coming 6-12 months (i.e. a beneficial re-rating of Chinese stocks). Since 2010 or 2011, actual growth rates in EPS are materially above the required growth range in both markets. However, over more recent time horizons, particularly 2013 and later, actual earnings growth has not only been below the range but has also been extremely poor in absolute terms. This is particularly true for the investable market, which has actually recorded negative growth in 12-month trailing EPS since 2014 or 2015. A dividend discount model approach suggests that the Chinese equity market discount is justified, barring a major structural improvement in earnings growth. Chart 12 highlights the problem with China’s stock market in a nutshell. For both the investable and domestic equity markets, the dividend payout ratio is well below the global average. This is a normal circumstance for small companies with high growth potential; firms re-invest a high portion of their earnings back into the company in order to build out their asset base and deliver even higher earnings in the future. Chart 12The Chinese Discount Visualized: A Low Payout Ratio, And Mediocre Earnings Growth

The Chinese Discount Visualized: A Low Payout Ratio, And Mediocre Earnings Growth

The Chinese Discount Visualized: A Low Payout Ratio, And Mediocre Earnings Growth

But panel 2 of Chart 12 shows that relative earnings for Chinese stocks versus the global average have not trended higher over the past decade, meaning that a higher earnings retention ratio among Chinese stocks has not led to a superior earnings profile. In response, global investors have rightly discounted Chinese stocks versus their global peers, a circumstance that is likely to continue unless Chinese earnings growth materially and sustainably improves. Our analysis implies that there is a natural limit to how far Chinese equities can ultimately be re-rated barring a major structural improvement in the economy, a factor that we may eventually have to contend with were we to recommend a cyclical overweight stance. Capped re-rating potential is unlikely to prevent Chinese stocks from trending higher in relative terms if economic fundamentals warrant an uptrend, but it may suggest that the duration or magnitude of the rise may be shorter than many investors hope. A Sino-U.S. Trade Deal: A Natural Currency Experiment In The Making? What explains the link between CNY-USD and the interest rate differential between the two countries? Finally, a brief note on the RMB. Since June 2018, changes in CNY-USD appear to have been closely aligned with the magnitude of proposed tariffs as a share of Chinese exports to the U.S., as would be implied in a simple open economy model with flexible exchange rates. Chart 13shows the levels implied by this framework in a variety of tariff scenarios, calculated based on the percent decline from the peak in the exchange rate in 1H 2018. As noted in our March 13 Weekly Report,8 CNY-USD today is consistent with the current tariff regime, implying potential upside if a trade deal with the U.S. rolls back some of the tariffs that have been imposed. Chart 13A Simple Equilibrium Framework Suggests CNY-USD May Rise Materially Further If Tariffs Are Rolled Back

A Simple Equilibrium Framework Suggests CNY-USD May Rise Materially Further If Tariffs Are Rolled Back

A Simple Equilibrium Framework Suggests CNY-USD May Rise Materially Further If Tariffs Are Rolled Back

However, Chart 14 shows that CNY-USD has been closely correlated with the interest rate differential between the two countries for several years, with the relationship having recently become a leading one. Chart 14 highlights that CNY-USD has moved higher than the rate differential would imply (painting the opposite picture as that shown in Chart 13), suggesting that the currency is more likely to depreciate than appreciate over the coming 6-12 months barring tighter monetary policy in China or outright rate cuts in the U.S. Chart 14Will Policymakers Or Rate Differentials Drive CNY-USD Over The Coming Year?

Will Policymakers Or Rate Differentials Drive CNY-USD Over The Coming Year?

Will Policymakers Or Rate Differentials Drive CNY-USD Over The Coming Year?

The relationship shown in Chart 14 is surprising, and we have struggled to understand the exact dynamics at play. As we highlighted in a September report,9 many global investors take the relationship for granted, given the strong historical link between interest rate differentials and exchange rates in developed countries. However, a major problem that arises in explaining Chart 14 is the fact that uncovered interest rate arbitrage (or the “carry trade”) cannot easily occur or cannot occur at all when one or both countries involved maintains capital controls. It is an important conundrum, and one that we have not been able to solve. From our perspective, there are only two scenarios that explain the close relationship between the exchange rate and interest rate differentials between the two countries: The relationship is causal, implying that capital flows in and out of the country are sufficiently large to enable a carry trade. The two series are correlated because of a third factor related in some way to the other two. In our view, scenario 1 is not likely. Capital is flowing out of China, but at a much slower rate than before,10 and the relationship shown in Chart 14 did not break down following China’s capital crackdown in 2015/2016. Ruling out scenario 1 necessarily implies that scenario 2 is correct. Our best guess concerning the missing third factor is that Chinese policymakers are looking to the rate differential as a guide to set the exchange rate, in order to mimic a market-based exchange rate in support of China’s goals to progressively liberalize (and internationalize) the currency. If true, this implies that China has full control of their exchange rate regardless of the prevailing interest rate differential, but that they are often choosing to follow what the differential implies. This is significant, because if Chinese and U.S. negotiators do agree to a “yuan stability pact” as has been reported in the press, a trade deal may set up an important natural experiment for the currency. In our view, a major upward move in the rate differential is unlikely over the coming year, implying that CNY-USD will persistently deviate from the relationship shown in Chart 14 if President Trump is not inclined to tolerate any real weakness in the RMB over the coming year. While the details of the currency agreement and the trade agreement more generally could allow for some decline in CNY-USD if coupled with an offsetting benefit for the U.S. (such as materially higher U.S. exports to China for some period), our bias is to believe that President Trump does not want to see a stronger dollar over the coming year in the lead-up to the 2020 election. If true, investors should pay close attention to the behavior of CNY-USD, as it is stands to be a revelatory event for China’s exchange rate regime. Jonathan LaBerge, CFA, Vice President Special Reports jonathanl@bcaresearch.com 1 Please see U.S. Bond Strategy and Global Fixed Income Strategy Weekly Reports “The New Battleground For Monetary Policy” and “Forward Guidance On Steroids”, dated March 26, 2019, for a detailed update on our view for Fed rate hikes and how investors should interpret the recent inversion in the yield curve. 2 Please see China Investment Strategy Weekly Report, “Dealing With A (Largely) False Narrative”, dated February 27, 2019, available at cis.bcaresearch.com 3 Please see China Investment Strategy Weekly Report, “2019 Key Views: Four Themes For China In The Coming Year”, dated December 5, 2018, available at cis.bcaresearch.com 4 Please see “Some U.S. Officials Said To See China Walking Back Trade Pledges”, Bloomberg News, dated March 19, 2019, and “Donald Trump-Xi Jinping meeting to end US-China trade war may be pushed back to June, sources say”, South China Morning Post. 5 Please see China Investment Strategy Special Report, “The Data Lab: Testing The Predictability Of China’s Business Cycle”, dated November 30, 2017, available at cis.bcaresearch.com 6 Please see Emerging Markets Strategy Weekly Report, “EM: A Sustainable Rally Or A False Start?”, dated March 7, 2019, available at ems.bcaresearch.com 7 Please see Professor Damodoran’s website for more information on his estimates of the equity risk premium. 8 Please see China Investment Strategy Weekly Report, “China Macro And Market Review”, dated March 13, 2019, available at cis.bcaresearch.com 9 Please see China Investment Strategy Weekly Report, “Moderate Releveraging And Currency Stability: An Impossible Dream?”, dated September 5, 2018, available at cis.bcaresearch.com 10 Please see China Investment Strategy Special Report, “Monitoring Chinese Capital Outflows”, dated March 20, 2019, available at cis.bcaresearch.com Cyclical Investment Stance Equity Sector Recommendations

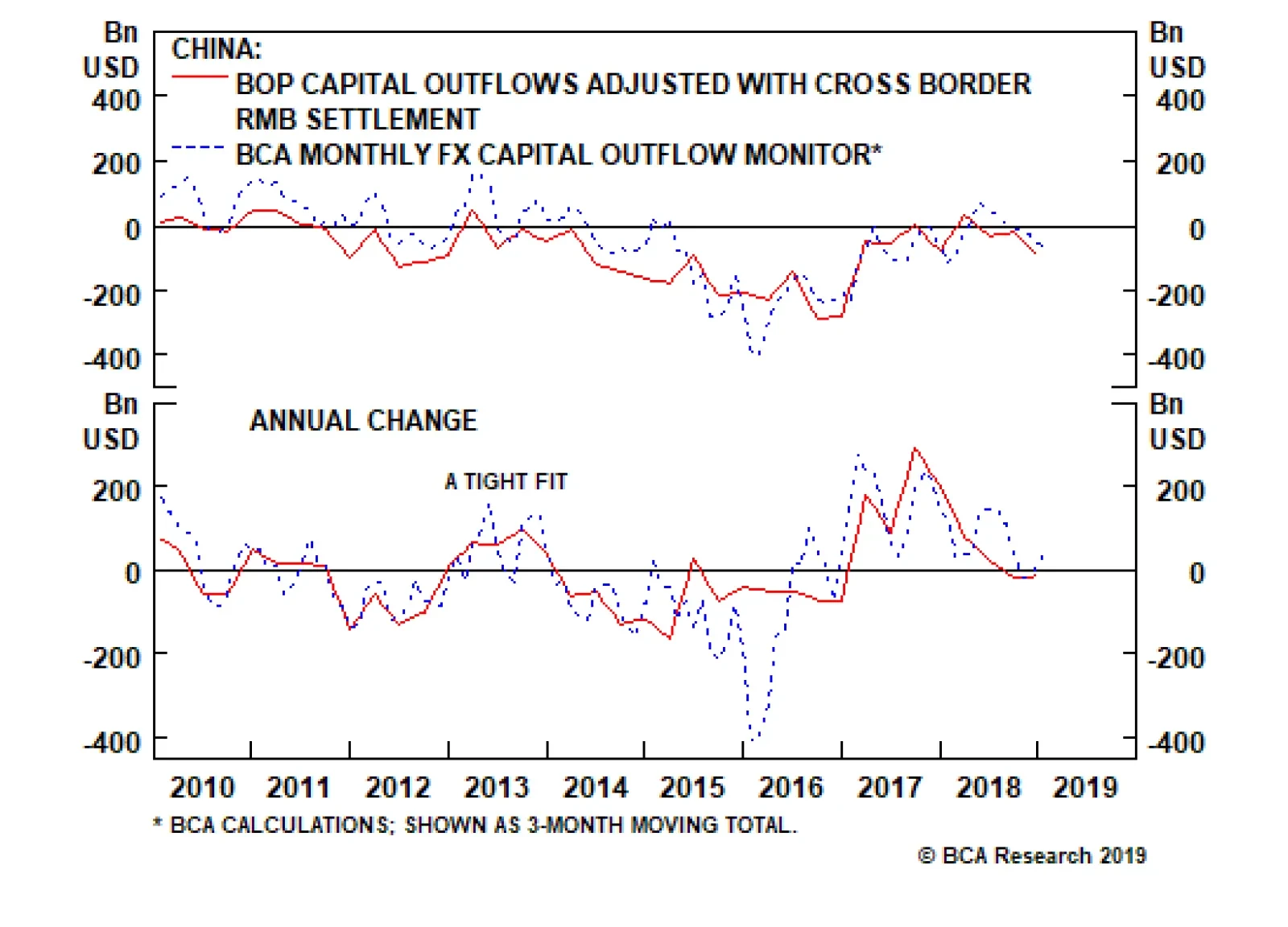

The chart above presents our China Investment Strategy team’s quarterly balance of payments-based capital flow measure (adjusted for cross-border capital flow) with our newly calculated monthly proxy. Divergences between the series exist in level terms, but…

We continue to expect copper prices to increase in the near term, as China’s credit cycle bottoms and DM central banks soften their monetary-policy stance. Fiscal and monetary stimulus in China also will be supportive of base metals prices going forward. The evolution of the Sino - U.S. trade negotiations remains a risk to our view, given how important the outcome of these talks will be for investors’ expectations and sentiment. Markets appear to be discounting a positive outcome. Anything that scuppers these talks – or results in a no-deal outcome – will be a negative for base metals, copper in particular. Our tactical long copper position is up by 1.2% since we initiated it last week. Highlights Energy: Overweight. Russian oil companies are expected to keep production lower until July, when the current OPEC 2.0 production-cutting agreement now in place expires. We expect the deal will be extended to year-end.1 Separately, the risk of a complete shutdown in Venezuela’s oil industry rose significantly, as a power failure in most of the country all but eliminated potable water supplies and significantly reduced oil exports. Base Metals/Bulks: Neutral. High-grade iron-ore prices got a boost this week as Vale was ordered to temporarily suspend exports from its primary port at Guaiba Island terminal in Rio de Janeiro state, according to Metal Bulletin’s Fastmarkets.2 The price-reporting agency’s 62% Fe Iron Ore Index rose $1.46/MT at $85.25/MT Tuesday. Precious Metals: Neutral. Spot gold is back above $1,300/oz, on the back of monetary policy easing among important central banks. This also is supporting base metals globally (see below). Ags/Softs: Underweight. Grain markets continue to drift sideways, awaiting definitive news re Sino - U.S. trade talks, specifically when presidents Xi and Trump will meet to finalize a deal (see below). Separately, wheat and corn inventories are expected to rise on the back of higher supplies and lower exports, the USDA forecast in its latest world supply-demand estimates. Feature Recent data releases confirm our view that global growth will remain weak in 1Q19 and early 2Q19. This will continue to put downward pressure on cyclical commodities – chiefly base metals and oil (Chart of the Week). Chart of the WeekGlobal Growth Slows In 1Q19

Global Growth Slows In 1Q19

Global Growth Slows In 1Q19

The persistence of the slowdown provoked major central banks to adopt a dovish stance in the short-term. This is easily seen in the recent actions by the U.S. Fed, the European Central Bank (ECB), the Bank of Canada (BoC) and the Reserve Bank of Australia (RBA), all of which have communicated a pause in their rate normalization policies.3 At the moment, the frail global growth is partly balanced by expectations of a positive outcome re the ongoing Sino - U.S. trade negotiations (Chart 2). In the coming months, we expect the effect of accommodative DM monetary policy combined with an expansion in China’s credit (more on this below) and fiscal stimulus – i.e., tax cuts announced earlier this month amounting to almost $300 billion (~ 2 trillion RMB) meant to support policymakers’ GDP growth targets – will go a long way toward reversing the earlier contraction. The effect of these policy decisions will be apparent in 2H19. Chart 2China Growth To Hook Higher

China Growth To Hook Higher

China Growth To Hook Higher

China’s Credit Cycle Bottomed In December 2018 The evolution of China’s credit cycle remains a central pillar to our view commodity demand growth in 2H19 will surpass consensus expectations. The massive growth reported in China’s January credit statistics revived investors’ expectations that China’s banks will re-open the credit valves as they did in 2016.4 In our view, this number does signal a bottom in China’s credit cycle, and implies Chinese – and indirectly EM – growth will bottom sometime this year. However, we still are not expecting a complete blowout credit expansion this year. We continue to believe Chinese policymakers will focus on stabilizing credit in 1H19 with moderate increases in supply, and start increasing stimulus in 2H19 or 2020 in order to maximize its effect later in 2020 ahead of the 100th anniversary of the founding of the Chinese Communist Party (CCP) in 2021. The soft February credit number released this week supports this argument.5 China’s Credit Cycle Matters For Base Metals Demand The relationship between China’s credit cycles and base metal prices endures and remains robust. We measure China’s aggregate credit using bank and non-bank claims on non-financial enterprises, households, local and central governments, and non-bank financial institutions. This corresponds to adding outstanding central and local government bonds to China’s Total Social Financing (TSF).6 The annual change in aggregate credit – or its impulses – do not perfectly capture the cycles in global base metal demand. These variables provide interesting signals about the direction and magnitude of movements in credit, however, they do not track base metals’ price cycles accurately and consistently (Chart 3). Chart 3Metals Price Cycles Don't Track Changed In China's Credit

Metals Price Cycles Don't Track Changed In China's Credit

Metals Price Cycles Don't Track Changed In China's Credit

To decompose this variable into its trend and cycle, we use a proxy of the credit cycle constructed using the Hodrick-Prescott and Hamilton filters, and the standardized 12-month credit impulse (Chart 4).7 Chart 4China's Credit Cycle Proxy

China's Credit Cycle Proxy

China's Credit Cycle Proxy

We find that our credit cycle proxy Granger causes base metal prices, import volume and industrial activity (Table 1).8 On average, it leads these variables by 4-6 months (Chart 5). Hence, we believe our credit cycle proxy provides valuable information about future commodity demand in China. Table 1China Credit Cycle Correlations

Bottoming Of China's Credit Cycle Bullish For Copper Over Near Term

Bottoming Of China's Credit Cycle Bullish For Copper Over Near Term

Chart 5

In fact, when regressing copper prices and the LMEX against it, we found that 60% and 58% of the variation in copper prices and the LMEX, can be explained by the linear relationship with our China credit cycle proxy, respectively (Chart 6). Chart 6China's Credit Cycle and Metals Prices

China's Credit Cycle and Metals Prices

China's Credit Cycle and Metals Prices

Given the leading property of China’s credit cycles with respect to industrial activity and metal prices, we included this new proxy in our Global Industrial Activity (GIA) index.9 This improves the correlation of our index with copper prices (Chart 7). Chart 7Credit Cycle Improves BCA's GIA

Credit Cycle Improves BCA's GIA

Credit Cycle Improves BCA's GIA

Currently, our models suggest copper prices should increase in the coming months as China’s credit cycle bottoms and DM central banks soften their monetary policy stance. The evolution of the China-U.S. trade negotiations remains a risk to our view as the outcome will weigh on investors’ expectations and sentiment. China’s Vs. DMs’ Credit Cycles Between 2009 and 2014, China’s credit cycle lagged the U.S. and EU’s broad money cycles (Chart 8). This counter-cyclicality is partly explained by its elevated level of exports to the U.S. and of hard goods to Europe. When the global economic cycle works in China’s favor – i.e., when the Fed and ECB are accommodative or fiscal stimulus is deployed in either or both regions – China’s exports rise as U.S. and EU aggregate demand increases. This typically reduces the need for endogenous fiscal or monetary stimulus within China. Chart 8China's Credit Cycle Lags U.S., EU Money Cycles

China's Credit Cycle Lags U.S., EU Money Cycles

China's Credit Cycle Lags U.S., EU Money Cycles

On the other hand, when the global economic cycle contracts and fiscal and monetary policy ex China becomes a headwind, Chinese policymakers typically need to deploy fiscal and monetary policy to keep growth going, or at least avoid a contraction in their economy. Between 2016 and 2017, DM and China credit cycles aligned and increased simultaneously. Taking into account the 4-to-6-month lag between the time credit supply is increased and commodity demand rises, this created bullish conditions for metals and oil from 2H16 to 1H18, pushing copper prices up by 60%. In 2018, both regions’ cycles rolled over. Base metals markets currently are experiencing the consequences of this contraction in credit availability and tightening of financial conditions generally. Going forward, we expect China will step in to raise domestic demand and offset the impact of the decline in credit availability elsewhere, which is affecting demand for its exports in the short-term. In the medium-term, the U.S. and EU, along with India, do not appear to be inclined to absorb Chinese exports to the extent they did in the past, which means the pivot to domestically generated growth through consumer- and services-led demand is the most viable alternative Chinese policymakers have to keep growth on target. Bottom Line: The dovish turn of major DM central banks combined with a bottoming of China’s credit cycle will support cyclical commodities at the margin in the coming months. During the second half of this year, we expect a more significant pick up in China’s credit, setting the stage for a year-end rally in base metal prices. As a consequence, the impact of China’s credit growth on base metals demand could diminish compared to previous stimulus targeting industrial demand. Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Robert P. Ryan, Chief Commodity & Energy Strategist rryan@bcaresearch.com Footnotes 1 Please see “Russia’s oil companies ready to cut output until July: TASS,” published by reuters.com March 12, 2019. 2 Please see Fastmarkets MB’s Daily Steel, March 12, 2019. 3 Please see “Pervasive Uncertainty, Persuasive Central Banks,” published by BCA Research’s Global Fixed Income Strategy March 12, 2019. It is available at gfis.bcaresearch.com. 4 Please see “China Macro And Market Review,” published by BCA Research’s China Investment Strategy March 13, 2019. It is available at cis.bcaresearch.com. 5 See footnote 4 above. 6 For more details please see “EM: A Sustainable Rally Or A False Start?” published by BCA Research’s Emerging Market Strategy March 7, 2019. It is available at ems.bcaresearch.com. 7 Hamilton notes the HP filter can be problematic. In general, we agree with critics of the filter (i.e. it results in spurious dynamics that are unrelated with the true data-generating process, it has an end-point bias which affects its real-time properties, and it is highly dependent on the parameter selection). However, there are some arguments in support of using the HP filter to proxy the credit cycle. First, as long as there are no clear theoretical foundation for an accurate measurement of the credit cycle, empirical validation should remain the number one criteria by which one selects its proxy. Second, credit cycles vary in duration and this weakens the ability to construct a reliable proxy. The usual parameter used with the HP filter favors short-term cycles (i.e. ~ 2 years) while the Hamilton filter focuses on medium-term cycles (i.e. ~ 5 years). Therefore, both can convey useful information. Third, China’s aggregate credit variable in level has a quasi-linear trend and is roughly approximated by a trend-stationary process with breaks in the trend and constant. Such a process should converge in limit when decomposed using the HP filter. Please see James D. Hamilton (2018), “Why You Should Never Use the Hodrick-Prescott Filter,” The Review of Economics and Statistics, vol 100(5), pages 831-843. and Phillips, Peter C. B. and Jin, Sainan (2015), “Business Cycles, Trend Elimination, and the HP filter,” Cowles Foundation Discussion Paper No. 2005. 8 Granger causality refers to a statistical technique developed by Clive Granger, the 2003 Nobel Laureate in Economics, which is used to determine whether one variable can be said to have caused (or predicted) another variable, given the past performance of each. Using standard econometric techniques, Granger showed one variable can be shown to have “caused” another, and that two-way causality also can be demonstrated (i.e., a feedback loop between the variables can exist based on the historical performance of each). 9 Please see “Oil, Copper Demand Worries Are Overdone,” published by BCA Research’s Commodity & Energy Strategy February 14, 2019. It is available at ces.bcaresearch.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Trades

Image

Highlights Analysis on Indonesia is available below. EM financial markets have diverged from the global growth indicators they have historically correlated with. This raises doubts about the sustainability of this rally. In China, broad bank credit has not accelerated at all, while non-bank credit growth rose sharply in January. The lack of recovery in broad bank credit growth is corroborated by lingering sluggishness in broad money growth. This refutes widespread perception in the global investment community that Chinese banks have re-opened the credit spigots again. Feature The headline news has all been positive for emerging markets over the past two months: The Federal Reserve is going on hold, China is stimulating its economy, the U.S. and China are nearing a trade agreement and risk-on market dynamics are permeating worldwide. Nevertheless, EM stocks have failed to outperform the global equity benchmark (Chart I-1, top panel). Notably, EM relative equity performance rolled over in late December when global share prices bottomed. Chart I-1EM Stocks Have Underperformed DM Ones Since Late December

EM Stocks Have Underperformed DM Ones Since Late December

EM Stocks Have Underperformed DM Ones Since Late December

In absolute terms, EM equities have been attempting to break above their 200-day moving average, but have so far failed to do so decisively (Chart I-1, bottom panel). When a market struggles to break out or outperform amid favorable news flows and buoyant investor sentiment, the odds are that it is facing formidable headwinds under the surface, and is at risk of relapsing. We sense EM currently fits this profile. Needless to say, investor consensus is very bullish on EM, and dominated by the above-mentioned narrative, specifically the Fed turning dovish and China stimulating, which is reminiscent of 2016 when EM staged a cyclical rally. Consequently, investors have rushed to pile into EM stocks and fixed-income. Chart I-2 illustrates that asset managers’ net holdings of EM ETF (EEM) futures have doubled since October 2018. Chart I-2Investor Consensus Is Very Bullish On EM

Investor Consensus Is Very Bullish On EM

Investor Consensus Is Very Bullish On EM

As of mid-February, EMs were by far the most overweight region within global equity portfolios, according to the most recent Bank of America/Merrill Lynch survey. The survey states that net 37% of global equity investors - who participated in the survey - were overweight EM. One of our clients that we met with on the road last week summed it up like this: “Investors have ‘recency bias’.” In other words, investors believe that 2019 will resemble 2016, and in turn have no appetite to bet against Chinese stimulus. We are in accord with this interpretation of investor behavior and the EM/China rally. Yet there are some noteworthy differences between today and 2016. First, in 2016, there was massive stimulus for China’s property market. At the time, the People’s Bank of China (PBoC) monetized the unsold housing stock in Tier-3 and -4 cities via its Pledged Supplementary Lending facility. At present, there is no stimulus for real estate. Second, by early 2016 EM profits had already contracted substantially. EM profits have yet to shrink in the current downtrend. Our thesis is that EM profits will contract this year for reasons we elaborated on in depth in our previous report, Mind The Time Gap. China’s credit and fiscal impulse leads EM/Chinese profits by about 12 months, and the recent improvement in this indicator, if sustained, suggests that a trough in EM/Chinese corporate earnings will only be reached in late 2019 (Chart I-3). Therefore, as EM profits shrink, investors will likely sell EM risk assets. Chart I-3EM Corporate Earnings Are Beginning To Contract

EM Corporate Earnings Are Beginning To Contract

EM Corporate Earnings Are Beginning To Contract

Altogether, these differences with 2016 make us reluctant to chase the current EM rally, and we continue to expect a meaningful reversal in EM risk assets in the months ahead. Monitoring Global Growth We maintain that EM is much more leveraged to global trade and China’s growth than to Fed policy. For a detailed discussion on this matter, please refer to EM: A Replay of 2016 or 2001? report from February 7, 2019. Therefore, the Fed’s dovish turn is not a sufficient reason to buy EM risk assets. To buy EM cyclically, we would need to change our outlook on global trade and Chinese imports. China influences the rest of the world via its imports. A closer look at the indicators that correlate with EM risk assets and commodities do not justify the recent EM rebound. In particular: The import sub-component of China’s NBS manufacturing PMI strongly correlates with EM share prices, excess returns in EM sovereign credit, and industrial metals prices and suggest that investors should fade this rebound (Chart I-4). Chart I-4EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

The Caixin manufacturing PMI for China was up in February, but the NBS manufacturing PMI fell. In turn, manufacturing PMI indexes in Korea, Taiwan, Japan and Singapore are all plunging, with several of them dropping well below the 50 boom-bust mark (Chart I-5). Chart I-5Asian Manufacturing Is Contracting

Asian Manufacturing Is Contracting

Asian Manufacturing Is Contracting

Korean, Taiwanese, Japanese and Singaporean shipments to China were shrinking in January, while their exports to the U.S. were resilient (Chart I-6). This confirms that global trade has been weak due to China, and that there are no signs of its reversal. Chart I-6Asian Exports To China And U.S.

Asian Exports To China And U.S

Asian Exports To China And U.S

Moreover, Korea released its February export data, and its aggregate outbound shipments are contracting (Chart I-7). Chart I-7Korean Exports: Deepening Contraction

Korean Exports: Deepening Contraction

Korean Exports: Deepening Contraction

Further, China’s container freight index – the price to ship containers – has rolled over again after picking-up late last year due to front-loading of shipments to the U.S. which were induced by the U.S. import tariffs. This signals ongoing weakness in global demand, and does not justify the latest rebound in EM financial markets in general and currencies in particular (Chart I-8). Chart I-8Global Trade Is A Risk To EM Currencies

Global Trade Is A Risk To EM Currencies

Global Trade Is A Risk To EM Currencies

Finally, even in the U.S. where manufacturing has been the most resilient globally, the odds point to notable weakness in this sector. Specifically, the continuous underperformance of U.S. high-beta industrial stocks to U.S. overall industrials beckons a further slowdown in American manufacturing (Chart I-9). Chart I-9U.S. Manufacturing Is In A Soft Spot

U.S. Manufacturing Is In A Soft Spot

U.S. Manufacturing Is In A Soft Spot

Bottom Line: Although financial markets are forward-looking, the recent rally has been too fast and has already gone too far. This has created conditions for a material setback as global/China growth will continue to disappoint in the months ahead. China: Credit Versus Money Growth We have been receiving questions from clients as to whether investors should heed to the message from China’s money or credit data, given they are presently sending contradictory messages (Chart I-10). Chart I-10China: Narrow, Broad Money, And Aggregate Credit

China: Narrow, Broad Money, And Aggregate Credit

China: Narrow, Broad Money, And Aggregate Credit

Even though narrow money (M1) has historically been an excellent indicator for China/EM business cycles, the most recent (January) print – M1 annual growth rate registered a record low – was distorted due to technical/seasonal factors, and should be ignored. Specifically, deposits by enterprises plunged in January and household deposits surged as companies paid out bonuses to employees in late January ahead of the Chinese New Year that began on February 5 (Chart I-11). Provided enterprise demand deposits are in M1 but household demand deposits are a part of M2, M1 was artificially depressed in January. It will rebound in February. Chart I-11China: Technical Reasons For M1 Plunge In January

China: Technical Reasons For M1 Plunge In January

China: Technical Reasons For M1 Plunge In January

Broad money provides a more comprehensive picture of money creation in China. As such, it is more relevant to compare broad money with aggregate credit. To compute aggregate credit, we add outstanding central and local government bonds to Total Social Financing (TSF). Chart I-12 illustrates the latest improvement in aggregate credit is not confirmed by either the PBoC’s broad money measure, M2, or our measure, M3 (M3 = M2 plus other deposits plus banks’ other liabilities excluding bonds). We created this M3 measure of broad money supply because in our opinion, M2 has been underestimating the extent of money creation in China in recent years due to financial engineering. Chart I-12The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

As discussed in Box I-1 on pages 12-13, lending or purchasing of securities by banks simultaneously creates money. Therefore, bank broad credit acceleration should be mirrored in a broad money upturn. Does the lack of revival in broad money mean the latest uptick in aggregate credit data has been driven by non-bank credit? Our analysis suggests yes – non-bank credit is responsible for the strong rise in the aggregate credit numbers in January. We deconstructed aggregate credit into broad bank credit and non-bank credit (Diagram I-1). Chart I-13 illustrates that broad bank credit has not accelerated at all, while non-bank credit growth rose in January.

Chart I-

Chart I-13China: Recent Credit Acceleration Is Due To Non-Bank Credit

China: Recent Credit Acceleration Is Due To Non-Bank Credit

China: Recent Credit Acceleration Is Due To Non-Bank Credit

The lack of recovery in broad bank credit growth is corroborated by lingering sluggishness in broad money (both M2 and M3) growth (Chart I-14). Chart I-14Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Consequently, this refutes the widespread perception in the global investment community that Chinese banks have re-opened the credit spigots. Chart I-15demonstrates the annual growth rate of each component of broad bank credit. While mainland banks’ loan growth to enterprises has accelerated, their lending to non-bank financial institutions has continued to shrink. Chart I-15Broad Bank Credit And Its Components

Broad Bank Credit And Its Components

Broad Bank Credit And Its Components

In sum, broad bank credit and broad money have not revived, and their impulses are rolling over, having failed to break above zero (Chart I-14, bottom panel). Bottom Line: The improvement in aggregate credit growth in January was due to credit provided/bonds purchased by non-banks rather than by banks. This does not tell us whether the credit growth acceleration is sustainable. For a more detailed discussion on the differences between money and credit, please refer to Box I-1 on page 12-13. Investors prefer simple narratives, and have readily embraced the story that China has opened up the credit faucets. Broad bank credit data and broad money supply data do not corroborate this thesis. It may change in the months ahead, but our point is that for the moment there is not yet a simple narrative about China’s credit cycle. Investment Implications Even though China’s aggregate credit impulse ticked up in January, the 2011-‘12 and 2015-‘16 episodes signify that its bottoming can last many months. Critically, EM financial markets have historically lagged turning points in the aggregate credit impulse. These time lags have been anywhere between three to 18 months over the past 10 years. Furthermore, in 2012 there was only a minor rebound in EM share prices – not a cyclical rally – in response to the significant rise in China’s aggregate credit impulse (Chart I-16, top panel). Chart I-16Beware Of The Time Lag

Beware Of The Time Lag

Beware Of The Time Lag

Hence, even if January marked the bottom in the aggregate credit impulse – which is plausible in our opinion – EM risk assets will remain at risk based on historical time lags between the aggregate credit impulse and China-related financial markets.1 BOX 1 Why And When Money Supply Differs From Credit The following elaborates on the key differences between broad money supply and aggregate credit. 1. Why and when do broad money and credit diverge? When commercial banks provide loans to or buy bonds (or any other asset) from non-banks, they simultaneously create new money supply/deposits. Broad money supply is the sum of all deposits in the banking system, which is why we use the terms money and deposits interchangeably. When non-bank financial institutions – in China's case financial trust and investment corporations, financial leasing companies, auto-financing companies and loan companies – as well as enterprises and households make loans or buy bonds, they do not create money. Hence, money supply/deposits is mostly equal to net cumulative broad bank credit creation. The difference between aggregate credit and money supply is due to lending activities of non-bank entities (see Diagram I-1 on page 9). Lending, purchasing of bonds, or any other forms of financing by non-bank entities does not change money supply. Thus, aggregate credit is more relevant than money supply to forecast business cycle fluctuations. Apart from the fact that banks still play a very large role in aggregate financing in China, there are a few other reasons why one should not ignore broad money and rely solely on aggregate credit: Banks can extend credit, but might choose not to classify it as loans on their balance sheet for regulatory reasons. Chinese banks did this in the past by booking loans as non-standard credit assets. In any case, when a bank lends to a non-bank it creates new deposits/money, and it is hard to conceal deposits/liabilities. In these cases, broad money supply gives a better signal about the true extent of credit growth than statistics on loans. If under regulatory pressures banks reclassify their non-standard credit assets as loans, the amount of loans will expand, even though no new lending occurs. Yet, money supply/deposits will not change. In this case, loan numbers will give a false signal and money supply will be a better indicator for new credit origination by banks and, thereby, for economic activity. The true measure of Chinese bank loans and credit data were probably disguised over the past several years because banks and non-bank financial institutions were involved in financial engineering. However, in the past two years, the regulatory clampdown forced Chinese commercial banks to unwind some of these structures and properly reclassify items on their balance sheets. Both the masking of credit assets and the ensuing reclassification could have distorted loan and credit data. This is why we use broad money supply as a litmus test to gauge banks’ broad credit origination. Given TSF includes bank loans but does not include banks’ non-standard credit assets, we believe TSF understates the amount of credit in the economy. As a result, we have not been able to calculate an accurate aggregate level of non-bank credit. Only since mid-2017, when under the regulatory clampdown, banks have stopped classifying loans as non-standard credit assets, can the annual growth rate of TSF serve as a meaningful statistic. Hence, we estimate the annual growth rate of non-bank credit only starting in 2018 (please refer to Chart I-13 on page 9). 2. Does the central bank (PBoC) create money by injecting liquidity into the system? Barring lending to or buying assets from non-banks – which does not typically occur outside of quantitative easing (QE) programs – central banks do not create broad money or deposits. Central banks create banking system reserves, which are not part of the broad money supply in any country. Money supply/deposits, the ultimate purchasing power for economic agents, is created solely by commercial banks “out of thin air,” as we have discussed and illustrated in our series of reports on money, credit and savings. 3. Why do we use impulses (second derivatives of money/credit) rather than growth rates? Our goal is to forecast a change in economic activity/capital spending/imports/enterprise revenues – i.e., a change in flow variables. Money and credit are stock variables. Therefore, a change (the first derivative) in outstanding money and credit produces flow variables. The latter measures new credit and money origination in a given period. These are comparable with flow variables like spending, income and profits. To gauge changes in flow variables, i.e., the growth rate of spending, one needs to calculate a change in new money and credit origination – i.e., change in their net flow. In brief, to do an apples-to-apples comparison, one needs to use the second derivative (a change in change) in money and credit – i.e., changes in their flows – to predict changes in flow variables such as GDP/capital spending/imports/enterprise revenues. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com Lin Xiang, Research Analyst linx@bcaresearch.com Indonesia: It Is Not All About The Fed Indonesian stocks have outperformed their emerging market peers significantly in the past few months as the Federal Reserve has turned dovish and U.S. rate expectations have declined. Although U.S. bond yields do strongly and inversely correlate with Indonesian stocks’ relative performance versus the EM equity benchmark (Chart II-1, top panel), we believe there are other factors – such as Chinese growth and commodities prices – that are also important to this market (Chart II-1, bottom panel). Chart II-1Indonesian Stocks: The Fed Versus Commodities

Indonesian Stocks: The Fed Versus Commodities

Indonesian Stocks: The Fed Versus Commodities

In the next several months, slowing Chinese growth, lower commodities prices, and a renewed sell-off in EM markets will take a toll on Indonesian financial markets. Indonesian exports are contracting which will intensify as commodities prices fall and China’s purchases of coal and base metals drop (Chart II-2, top panel). Chart II-2Indonesia: Exports Are Shrinking

Indonesia: Exports Are Plunging

Indonesia: Exports Are Plunging

Indonesia’s current account deficit is already large and will continue widening as the export contraction deepens (Chart II-2, bottom panel). Remarkably, the nation’s commercial banks have been encouraged to keep the credit taps open as the central bank – Bank Indonesia (BI) – has been injecting enormous amounts of liquidity (excess reserves) into the banking system (Chart II-3, top panel). Given these liquidity injections, bank credit and domestic demand growth have remained more resilient than would otherwise have been the case. Chart II-3The Central Bank Is Injecting Liquidity

Indonesia's Central Bank Is Injecting Liquidity

Indonesia's Central Bank Is Injecting Liquidity

Yet, by injecting such enormous amounts of excess reserves into the system, the central bank has more than negated its previous liquidity tightening, resulting from the sales of its foreign exchange reserves in order to defend the rupiah (Chart II-3, bottom panel). The implications of such policy are that these excess reserves could encourage speculation against the rupiah, especially amid weakening global growth and falling commodities prices. Provided foreigners own large portions of Indonesian stocks and local-currency government bonds, a depreciation in the rupiah will produce a renewed selloff in the nation’s financial markets. A final point on Indonesian commercial banks: their net interest margins have been narrowing sharply (Chart II-4, top panel). Chart II-4Commercial Banks' Profits Will Weaken

Commercial Banks' Profits Will Weaken

Commercial Banks' Profits Will Weaken

Moreover, as global growth slows, non-performing loans (NPLs) on the balance sheets of Indonesian banks will rise. In turn, provisioning for bad loans will also increase, and bank earnings will decline (Chart II-4, bottom panel). These dynamics will be bearish for Indonesian commercial banks, which account for 44% of the overall MSCI Indonesia index. Bottom Line: Continue avoiding/underweighting Indonesian stocks and fixed-income markets. We continue shorting the IDR versus the U.S. dollar. Ayman Kawtharani, Associate Editor ayman@bcaresearch.com Footnotes 1 Please note that this represents the Emerging Markets Strategy team’s view and is different from BCA’s house view on global risk assets and global growth. The key point of contention is the outlook for China’s growth. Equity Recommendations Fixed-Income, Credit And Currency Recommendations

Regarding the European luxury goods sector, we often get following question: is it, just like the basic resources sector, a direct play on China’s growth cycle? The answer is no. Recently, the connection between the fortunes of ‘soft’ luxury goods brands like…

Highlights Please note that analysis on India is published below. Even if the recent upturn in the Chinese credit impulse is sustained, there will likely still be a six- to nine-month lag between the impulse’s trough and the bottom in the mainland’s business cycle. EM corporate earnings cycles typically lag Chinese stimulus efforts by about nine months. Therefore, EM profits will be contracting in the first three quarters of 2019. This will short-circuit the current rebound in EM share prices. EM equity valuations are not cheap enough to shield stocks from profit contraction. Feature China’s credit growth was very strong in January. We contend that even if the upturn in the credit impulse proves to be persistent, there will likely be a six- to nine-month lag between its low point and the bottom in the mainland’s business cycle. Chart I-1 demonstrates that the credit impulse leads both nominal manufacturing output growth and the manufacturing PMI’s import subcomponent by roughly nine months. Chinese imports are the most pertinent variable to gauge China’s economic impact on the rest of the world. Chart I-1China: Credit Impulse Leads Business Cycle By Nine Months

China: Credit Impulse Leads Business Cycle By Nine Months

China: Credit Impulse Leads Business Cycle By Nine Months

In the meantime, will financial markets exposed to Chinese growth look through the valley of the ongoing growth deceleration and continue to rally? Or will they experience a major relapse in the coming months? In our opinion, corporate profits will be the key to broader financial market performance. So long as corporate profits do not shrink, investors will likely look beyond weak macro data, and any weakness in stocks will be minor. However, if corporate profits contract in the next nine months, then share prices will plummet anew. EM Profits Are Heading Into Contraction Chart I-2 illustrates that China’s credit impulse leads both EM and Chinese corporate earnings per share (EPS) by at least nine months and that it currently foreshadows EPS contraction in the first three quarters of 2019. Even if the recent upturn in the credit impulse is sustained, EM and Chinese EPS growth will likely bottom only in August – while they are in negative territory. Chart I-2EM EPS Is Beginning To Contract

EM EPS Is Beginning To Contract

EM EPS Is Beginning To Contract

EM corporate earnings growth has already dropped to zero and will turn negative in 2019. Chart I-3A reveals that EPS in U.S. dollar terms are already contracting in six out of 10 sectors – industrials, consumer staples, consumer discretionary, telecom, utilities and health care. Chart I-3AEM EPS By Sector

EM EPS By Sector

EM EPS By Sector

Chart I-3BEM EPS By Sector

EM EPS By Sector

EM EPS By Sector

EPS growth has not yet turned negative for financials, technology, energy and materials (Chart I-3B). Notably, corporate earnings within these four sectors collectively account for 70% of EM total corporate earnings, as shown in Table I-1.

Chart I-

Over the course of 2019, these sectors’ EPS are also set to shrink: Technology (accounts for 20% of MSCI EM corporate earnings): NAND semiconductor prices have been plunging for some time, and DRAM prices are also beginning to drop (Chart I-4). This reflects broad-based weakness in global trade – global auto sales are shrinking for the first time since the 2008 global financial crisis, global semiconductor sales are relapsing and global mobile phones shipments are falling (Chart I-5). Chart I-4Semiconductor Prices Are Falling

Semiconductor Prices Are Falling

Semiconductor Prices Are Falling

Chart I-5Broad-Based Weakness In Global Trade

Broad-Based Weakness In Global Trade

Broad-Based Weakness In Global Trade

Semiconductors accounted for 77% of Samsung’s operating profits in the first three quarters of 2018, suggesting the potential drop in DRAM prices will be devastating for its profits. Next week we will publish a Special Report on Korea and discuss the outlook for both semiconductors and Korean profits in more detail. In addition, the ongoing contraction in Taiwanese exports of electronics parts confirms downside risks to EM tech earnings (please refer to top panel of Chart I-3B). In brief, the ongoing decline in semiconductor prices will bring about EPS contraction in the EM technology sector. Financials/Banks (financials make up 31% of EM corporate earnings): Banks’ profits often correlate with fluctuations in economic activity, because the latter drive non-performing loan (NPL) cycles (Chart I-6). NPL cycles outside Brazil, Russia and India – where the banking systems have already gone through substantial NPL recognition and provisioning – will deteriorate, and push banks to increase their provisions. The latter will be a major drag on EM banks’ profits. Chart I-6EM Banks EPS And Economic Activity

EM Banks EPS And Economic Activity

EM Banks EPS And Economic Activity

Regarding Chinese banks in particular, if the credit revival in January is sustained, it would strongly suggest that the government is resorting to its old, credit-driven growth playbook. Following 10 years of an enormous credit frenzy and a 20-year capital spending boom, it is currently difficult to find many financially viable projects. Hence, a renewed credit binge will once again be associated with further capital misallocation and more NPLs. Many of these projects will fail to generate sufficient cash flow to service debt. NPLs will thus rise considerably and the need to raise capital will dilute the banks’ existing shareholders. Of course, this will happen with a time lag. Chart I-7 shows that the gap between Chinese banks’ EPS and non-diluted profits has once again widened, and that EPS are beginning to contract. Chart I-7Chinese Banks: Earnings Dilution

Chinese Banks: Earnings Dilution

Chinese Banks: Earnings Dilution

Chinese banks could issue perpetual bonds – discussed in great detail in last week’s report – to recapitalize themselves. Nevertheless, this will be negative for existing shareholders. In a nutshell, despite low multiples, share prices of Chinese banks will drop because more credit expansion amid the lingering credit bubble is negative for existing shareholders. The basis is that it will ultimately lead to their dilution. Chinese banks make up 4.5% of the MSCI’s EM equity market cap and 10% of aggregate EM profits. Hence, their EPS contraction will have a non-trivial impact on overall EM EPS. Resource sectors (energy and materials together make 20% of EM corporate earnings): The ongoing slowdown in China will exert renewed selling pressure in commodities markets. As shown in Chart I-9 on page 8, base metals prices lag the turning points in the Chinese credit impulse by several months and are still at risk of renewed price decline. Hence, profits of firms in the materials sector are at risk. Energy companies’ trailing EPS growth is still positive because the late-2018 carnage in oil prices has not yet filtered through to corporate earnings announcements (Chart I-3B on page 3). More importantly, the recent oil price rebound can be attributed to both Saudi Arabia’s output cuts as well as stronger demand – in the form of a surge in Chinese imports of oil and petroleum products. Chart I-8 illustrates that growth rates of China’s intake of oil and related products approached zero when crude prices were rising but has dramatically accelerated following their plunge. This is consistent with China’s pattern of buying commodities on dips. The point is that the upside in oil prices will be capped by China, which will likely moderate its oil purchases going forward, as crude prices have recently rallied. Chart I-8China And Oil

bca.ems_wr_2019_02_21_s1_c8

bca.ems_wr_2019_02_21_s1_c8

Bottom Line: EM profit cycles lag Chinese’s stimulus by about nine months. EM profits will be contracting in the first three quarters of 2019. This will short-circuit the current rebound in EM share prices. China’s Credit Cycles And Financial Markets What has been the relationship between China’s credit cycle and related financial markets over the past 10 years? The time lag between turning points in China’s credit impulse and relevant financial markets can be anywhere from zero to 18 months. Chart I-9 illustrates historical time lags between the Chinese credit impulse on the one hand and EM share prices, base metals prices and the global manufacturing PMI on the other. The time lag has not been consistent over time. Chart I-9Chinese Credit Impulse And Financial Markets: Understanding Time Lags

Chinese Credit Impulse And Financial Markets: Understanding Time Lags

Chinese Credit Impulse And Financial Markets: Understanding Time Lags

In late 2015-early 2016, the rebound in China’s credit impulse led financial markets by six months. At the recent market peak in January 2018, the credit impulse led financial markets and the global manufacturing PMI by about 18 months. In the meantime, in the 2012-13 mini cycle, EM share prices and commodities markets did not rally much, despite the meaningful upturn in China’s credit impulse. Finally, at the 2010-2011 peak, the credit impulse led EM stocks and base metals prices by 12 months. In short, the credit impulse led those financial markets by a few months to as much as a year and a half. Further, not only do time lags to the stimulus vary, but the impact on both economic activity and financial markets varies as well. This is because both economic activity and financial markets are driven by human psychology and behavior; iterations in stimulus, economic activity and financial markets are chaotic and complex in nature and do not follow well-defined patterns. Given the poor state of sentiment among Chinese consumers, business managers and entrepreneurs, more stimulus and more time may be required to turn the mainland’s business cycle this time around. Besides, unlike in previous episodes, there has not been any stimulus for the property market and no tax reductions on auto sales. Finally, although China and the U.S. may strike a deal on trade, it is unlikely to be a comprehensive agreement that is sustainable in the long run. This would be consistent with our Geopolitical Strategy team’s view that China and the U.S. are in a long-term and broad geopolitical confrontation – not a trade war. The trade war and tariffs are just one dimension of this. Hence, Chinese consumers and businesses, as well as the global business community may well look through this potential deal and not significantly alter their cautious behavior, at least for some time. In other words, the genie of geopolitical confrontation is out of the bottle, and the presidents of the U.S. and China are unlikely to succeed in putting it back. Bottom Line: Turning points in China’s credit impulse generally lead financial markets exposed to Chinese growth by several months. Given that the improvement in the credit impulse is both very recent and modest, odds are that China-related plays including EM risk assets will go through a major selloff before putting in a durable bottom.1 EM Equity Valuations In terms of the ability of EM stocks to withstand profit contraction, would cheap valuations not shield share prices from a considerable drop? We do not think EM equities are cheap; their valuations are neutral. Hence, there is no real valuation cushion in EM stocks to help them endure a period of negative EPS growth. We have written frequently about valuations and will touch on the topic only briefly here. Market cap-based multiples indeed appear very low. However, some segments of the EM universe such as Chinese banks and state-owned companies in Russia, Brazil, China and India have had low multiples for years. In other words, they are a value trap and their multiples are low for a reason. We elaborated above why Chinese banks are chronically “cheap”. For many other companies, low multiples are due to structural issues such as the lack of focus on profitability and shareholder value, or the high cyclicality of profits. Many of these stocks have large market caps, which pull down the EM index’s aggregate multiple. To remove market-cap bias, we have calculated 20% trimmed-mean multiples by ranking 50 MSCI EM industry groups (sub-sectors) and cutting off the top and bottom 10%. Then, we calculate the equal-weighted average of the remaining 80% of the sub-sectors. We did this calculation for the following five ratios: trailing P/E, forward P/E, price-to-cash earnings, price-to-book value and price-to-dividend. Then, we combined them into a composite valuation indicator (Chart I-10, top panel). This indicator shows that EM equity valuations are neutral. Chart I-10EM Equity Valuations In Absolute Terms

bca.ems_wr_2019_02_21_s1_c10

bca.ems_wr_2019_02_21_s1_c10

In addition, we calculated the median and equal-weighted composite valuation indicators (Chart I-10, middle and bottom panels). They also remove market cap bias and tell the same message: EM stocks are trading close to their fair value. EM equities are also close to their historical average relative to developed markets (DM). Chart I-11 illustrates relative EM versus DM valuation indicators based on 20%-trimmed mean, median and equal-weighted metrics. Chart I-11EM Equity Valuations Versus DM

bca.ems_wr_2019_02_21_s1_c11

bca.ems_wr_2019_02_21_s1_c11

In sum, EM valuations are not cheap neither in absolute terms, nor relative to DM. According to both measures, valuations are neutral. Hence, valuations will not prevent share prices from falling as profits begin to contract. This is why we continue to recommend a defensive strategy for absolute-return investors, and we continue to underweight EM versus DM within a global equity portfolio. Arthur Budaghyan, Senior Vice President Emerging Markets Strategy arthurb@bcaresearch.com India: Beware Of Rural Growth Lapse Indian share prices are weak and are underperforming the emerging markets benchmark in U.S. dollar terms (Chart II-1, top panel). Small cap stocks are in a full-fledged bear market (Chart II-1, bottom panel). Chart II-1Indian Stocks Are Weak

Indian Stocks Are Weak

Indian Stocks Are Weak

The latest earnings season turned out to be disappointing. Many companies missed their earnings estimates. Chart II-2 shows that net profit margins of listed non-financial companies have turned down and overall EPS growth is weakening. Chart II-2Indian Corporate Profits Are Sluggish

Indian Corporate Profits Are Sluggish

Indian Corporate Profits Are Sluggish

Disappointing corporate earnings are confirmed by macro data as well. Chart II-3A shows that manufacturing production is decelerating and intermediate goods production is contracting. Further, sales of two-wheelers, three-wheelers, passenger and commercial vehicles, as well as tractors, are either slowing or contracting (Chart II-3B). Chart II-3ACyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Chart II-3BCyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

Cyclical Spending Is Decelerating

This weakness emanates from rural areas. The basis is that food prices have been falling since the summer of 2018 – and are deflating for the first time since the early 2000s. This is hurting rural incomes. Several indicators confirm considerable weakness in rural income growth and the latter’s underperformance versus urban income and spending: The top panel of Chart II-4 illustrates that our proxy for spending in rural areas relative to urban areas has deteriorated massively along with the decline in Indian food prices. Chart II-4Rural Spending Is Weaker Than Urban One

Rural Spending Is Weaker Than Urban One

Rural Spending Is Weaker Than Urban One

This measure is calculated as revenue growth of four rural-exposed listed companies minus the revenue growth of four urban-exposed listed companies. In both cases, the companies largely operate in the consumer goods space. Credit growth in rural areas has lagged that of urban areas, explaining the underperformance of rural spending (Chart II-4, bottom panel). Corroborating this, stock prices of these urban-exposed companies have outperformed their rural peers substantially (Chart II-5). Chart II-5Urban-Exposed Stocks Have Outperformed Rural Ones

Urban-Exposed Stocks Have Outperformed Rural Ones

Urban-Exposed Stocks Have Outperformed Rural Ones

Such a slump in rural income is posing a challenge to Modi’s re-election in May. His government – which lost three key state elections in late 2018 – is aware of these ominous trends and is acting boldly to revive income growth in rural areas. The government announced an expansionary budget that appeases rural voters. In particular, the budget aims to strengthen farmers’ support schemes, cut taxes for low- and middle-income earners and introduce a pension scheme for social security coverage of unorganized labor. However, there is a significant risk that the authorities’ fiscal and monetary stimulus are too late to lift growth before May’s elections. According to the past relationship between fiscal spending and India’s business cycle, higher government expenditure growth will only begin to have an effect on the economy in the second half of this year – i.e. after the elections are held (Chart II-6). Hence, the BJP could lose its majority, meaning it would either rule in a minority government or be forced to turn over power to the Congress Party and its allies. Chart II-6Government Expenditures To Lift Growth In H2 2019

Government Expenditures To Lift Growth In H2 2019

Government Expenditures To Lift Growth In H2 2019

Beyond the elections, food prices might be approaching their lows. Well-below average rain will likely result in weak agricultural production and, hence, higher food prices in the second half of 2019 (Chart II-7). Chart II-7Below Trend Monsoon = Food Prices Will Likely Rise

Below Trend Monsoon = Food Prices Will Likely Rise

Below Trend Monsoon = Food Prices Will Likely Rise

Therefore, in the second half of 2019, both fiscal easing and higher food prices will revive rural incomes and spending. In the meantime, monetary easing and credit growth acceleration will support demand in urban areas. Overall, Indian financial markets will likely remain in a risk zone until the elections as economic growth and corporate profits will continue to disappoint. If the opposition Congress Party’s alliance wins the election, Indian stocks and the currency will initially sell off. After this point, Indian assets could offer a buying opportunity because growth will likely revive in the second half of 2019. Bottom Line: For now, we continue to recommend an underweight position in Indian equities relative to the EM equity benchmark. Weakening growth, the very low interest rate differential versus U.S. rates and political uncertainty ahead of the general elections, pose risks of renewed rupee depreciation. A weaker rupee will continue to benefit India’s export-oriented software companies. Therefore, we also reiterate our long Indian software / short EM stocks recommendation. Finally, fixed-income investors should stay with the yield curve steepening trade. The central bank could further cut rates in the near term. However, long-term bond yields will not fall substantially and will likely start drifting higher sooner than later. The widening fiscal deficit, expectations of growth revival in the second half of 2019, and eventually higher food prices and inflation expectations, will all lead to a continuous steepening in the local yield curve. Ayman Kawtharani, Associate Editor ayman@bcaresearch.com Footnotes 1 This is the view of BCA’s Emerging Markets Strategy team and it is different from BCA’s house view on China-related assets and the global business cycle. The primary source of the difference is the outlook for China’s growth. Equity Recommendations Fixed-Income, Credit And Currency Recommendations