Money Trends / Liquidity

As expected, the ECB kept policy on hold on Thursday. In a unanimous decision, it maintained the deposit rate at an all-time high of 4% following 10 consecutive increases. Ultimately, the tone of the communication was on the dovish side. True, the ECB…

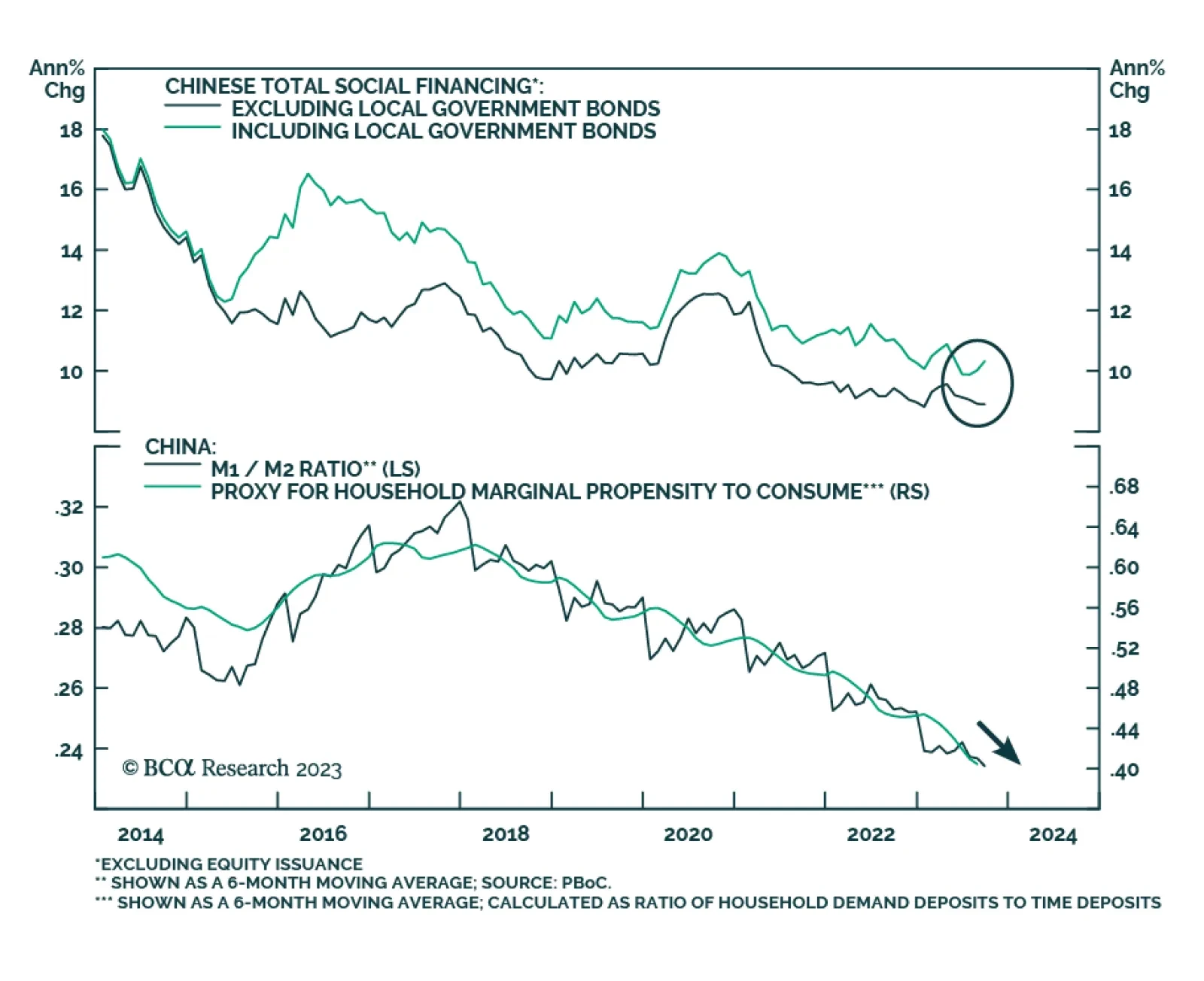

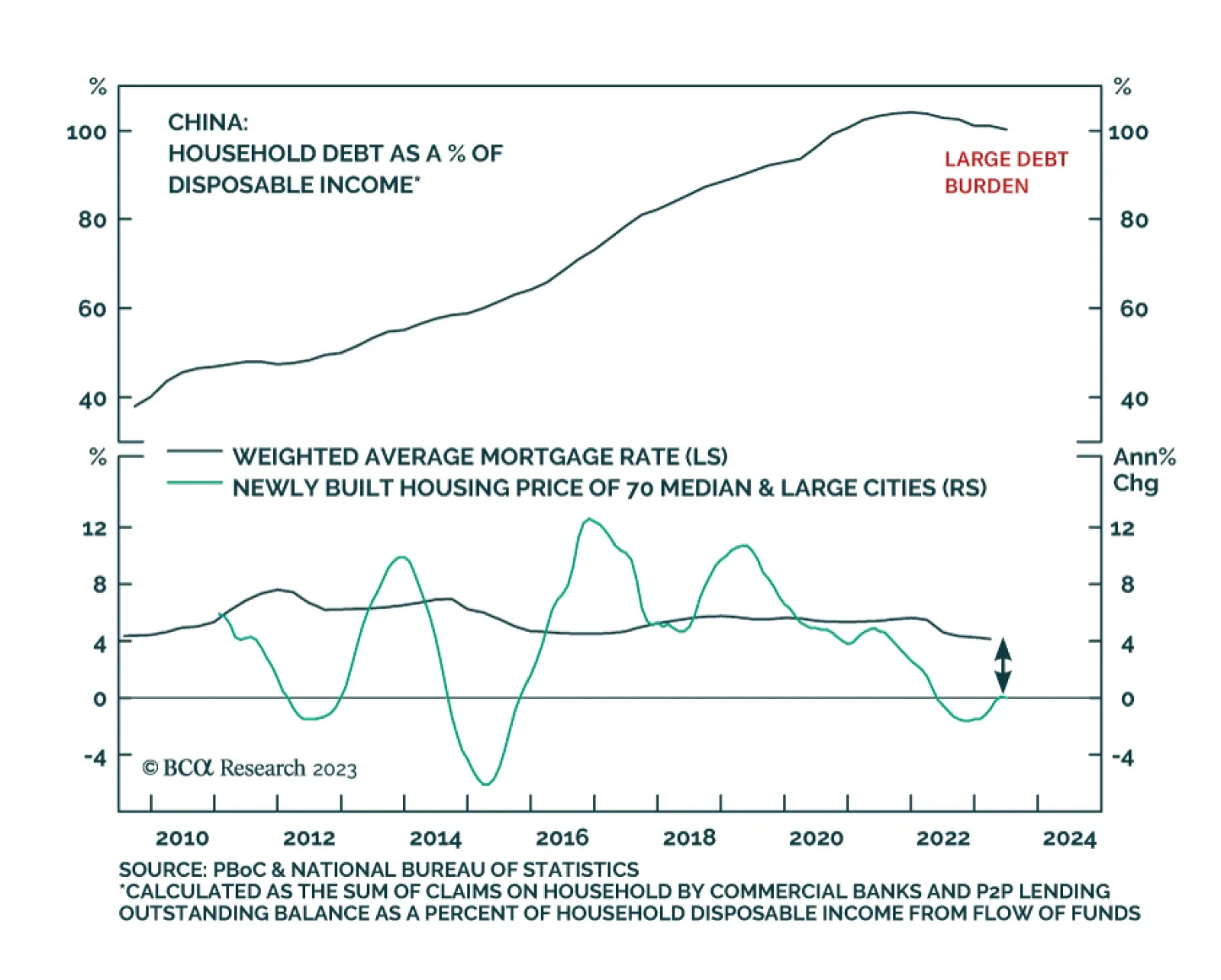

On the surface, Chinese credit data sent a positive signal about the domestic economy. Chinese aggregate social financing totaled CNY 4.1 trillion in September – exceeding both August’s CNY 3.1 trillion and expectations of CNY 3.7 trillion. However,…

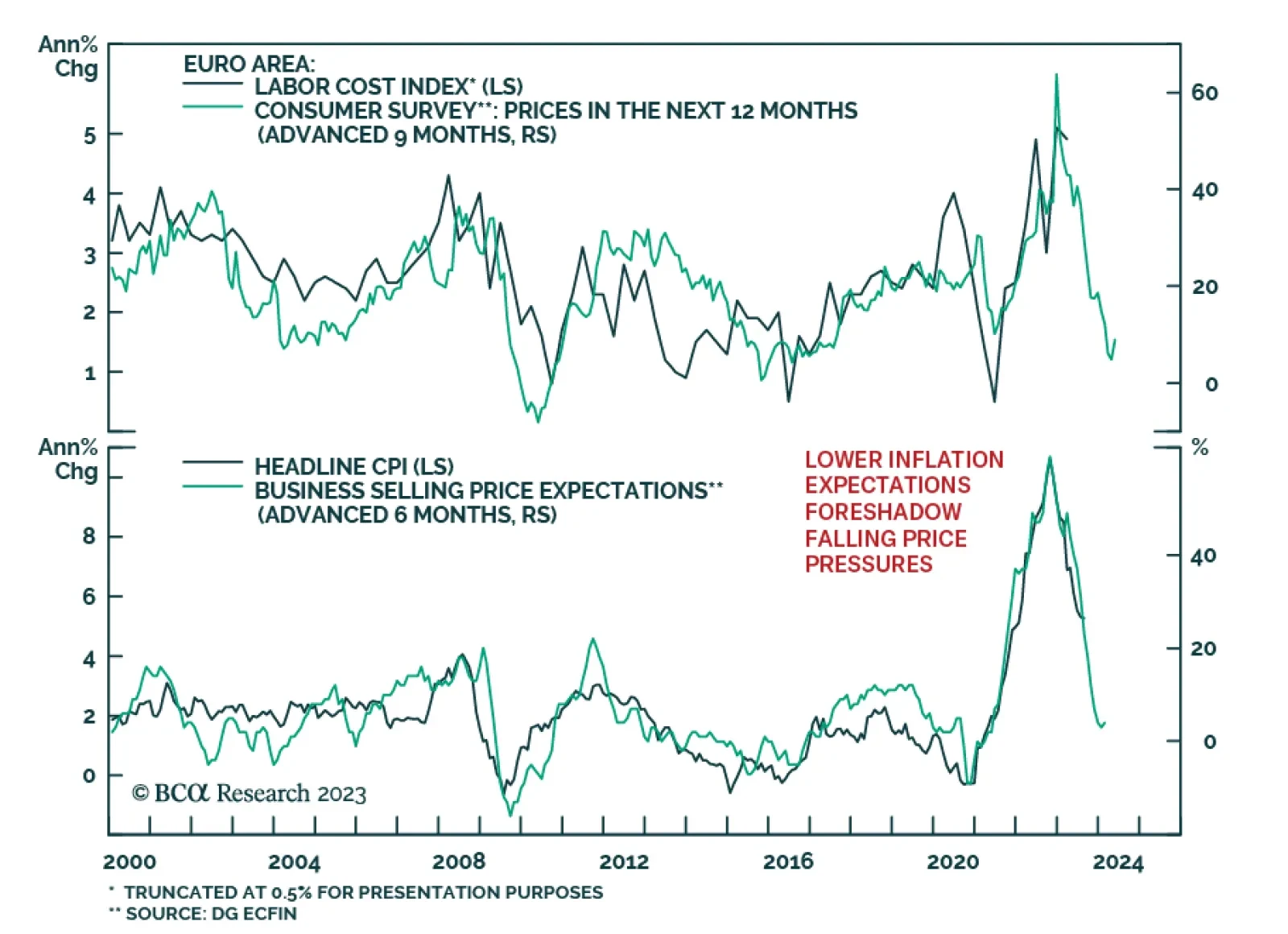

Eurozone headline inflation surprised to the upside in August, confirming the signal from the preliminary German and Spanish releases. The year-on-year gauge was unchanged at 5.3% – surprising expectations of a deceleration to 5.1%. Similarly, the 0.6%…

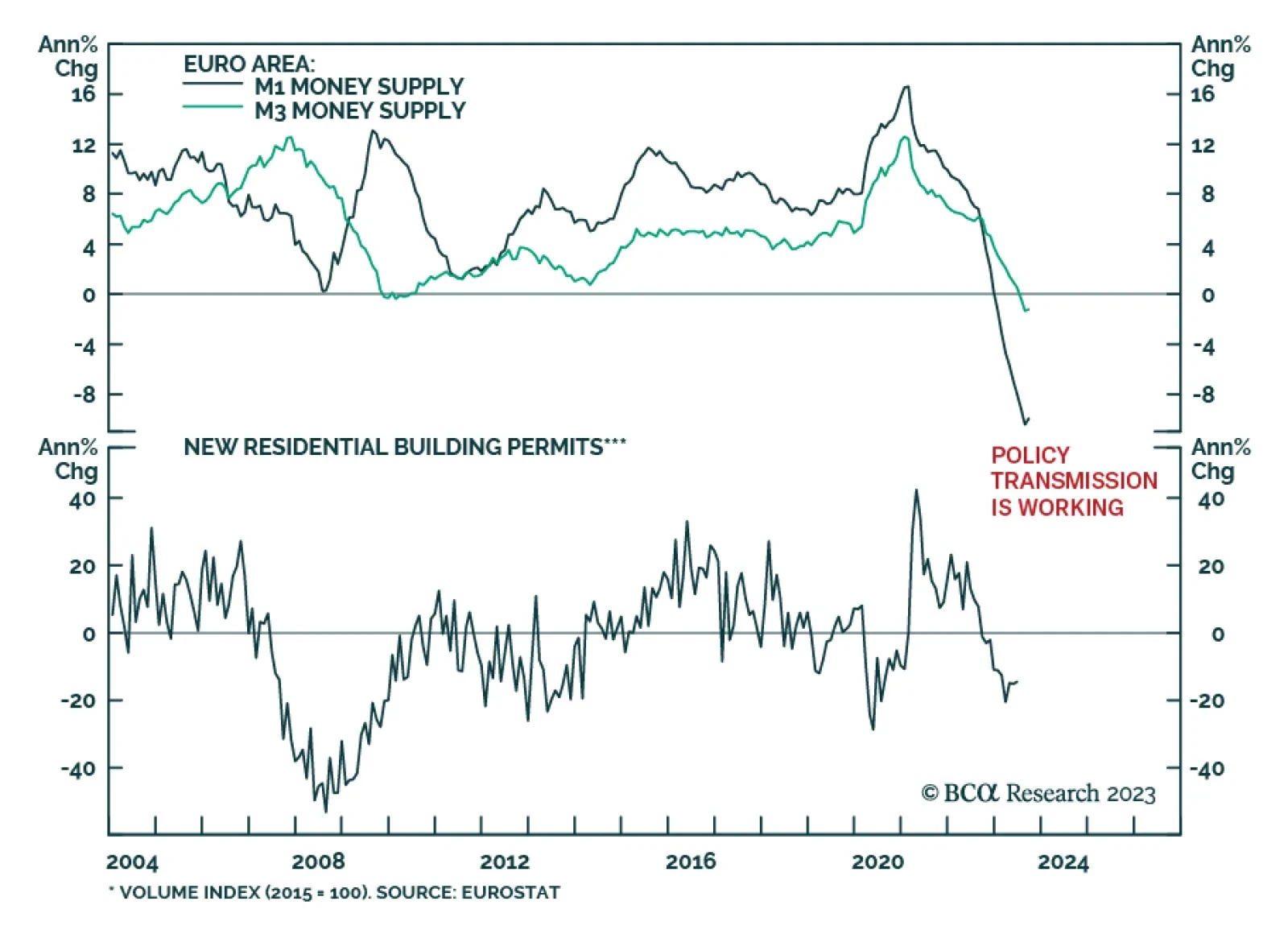

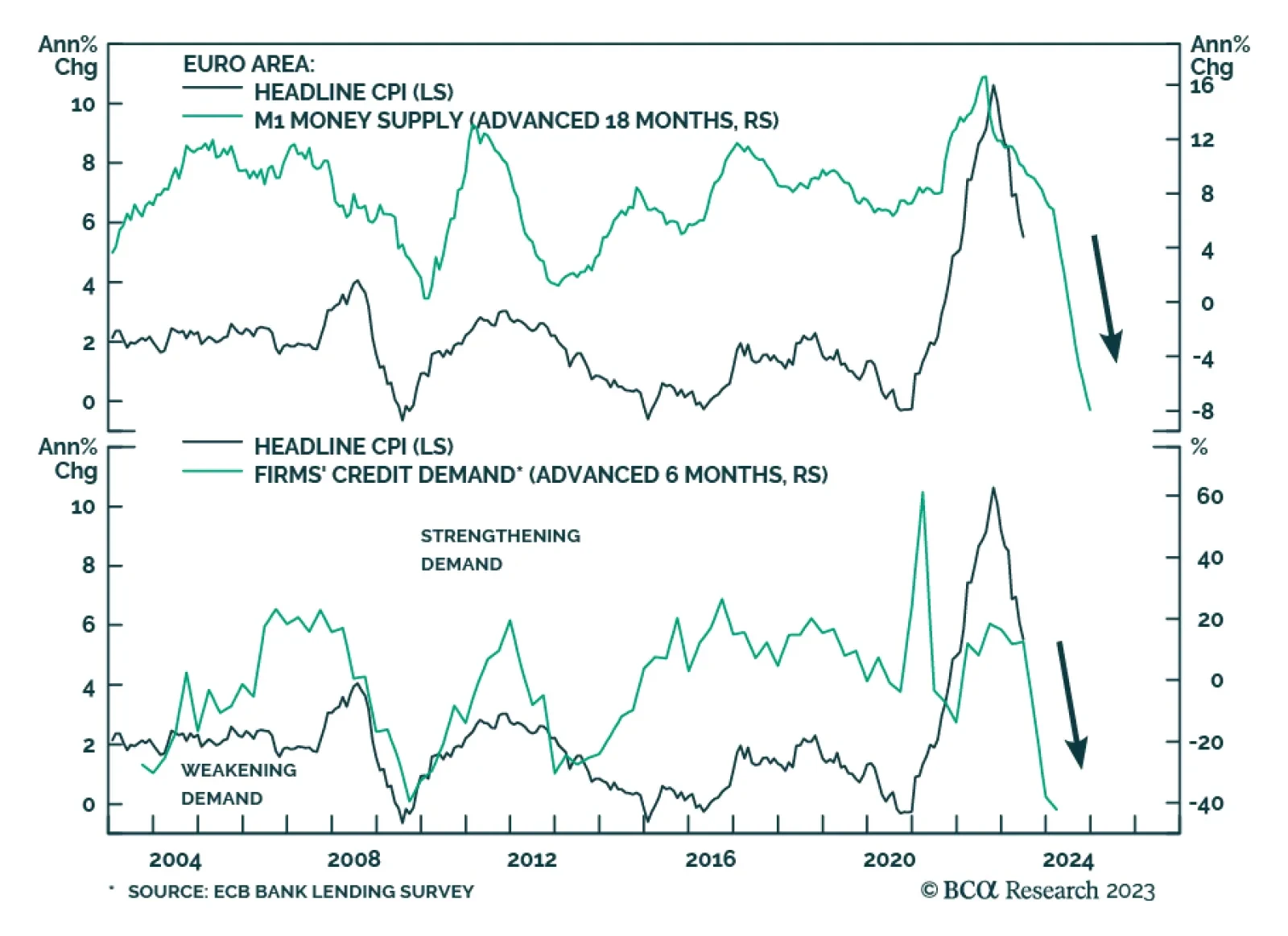

Eurozone money supply data reflect the impact of the ECB’s aggressive tightening campaign on the region’s economy. Data released on Monday showed the July M3 measure of broad money (the sum of M2, repurchase agreements, money market fund shares/units and…

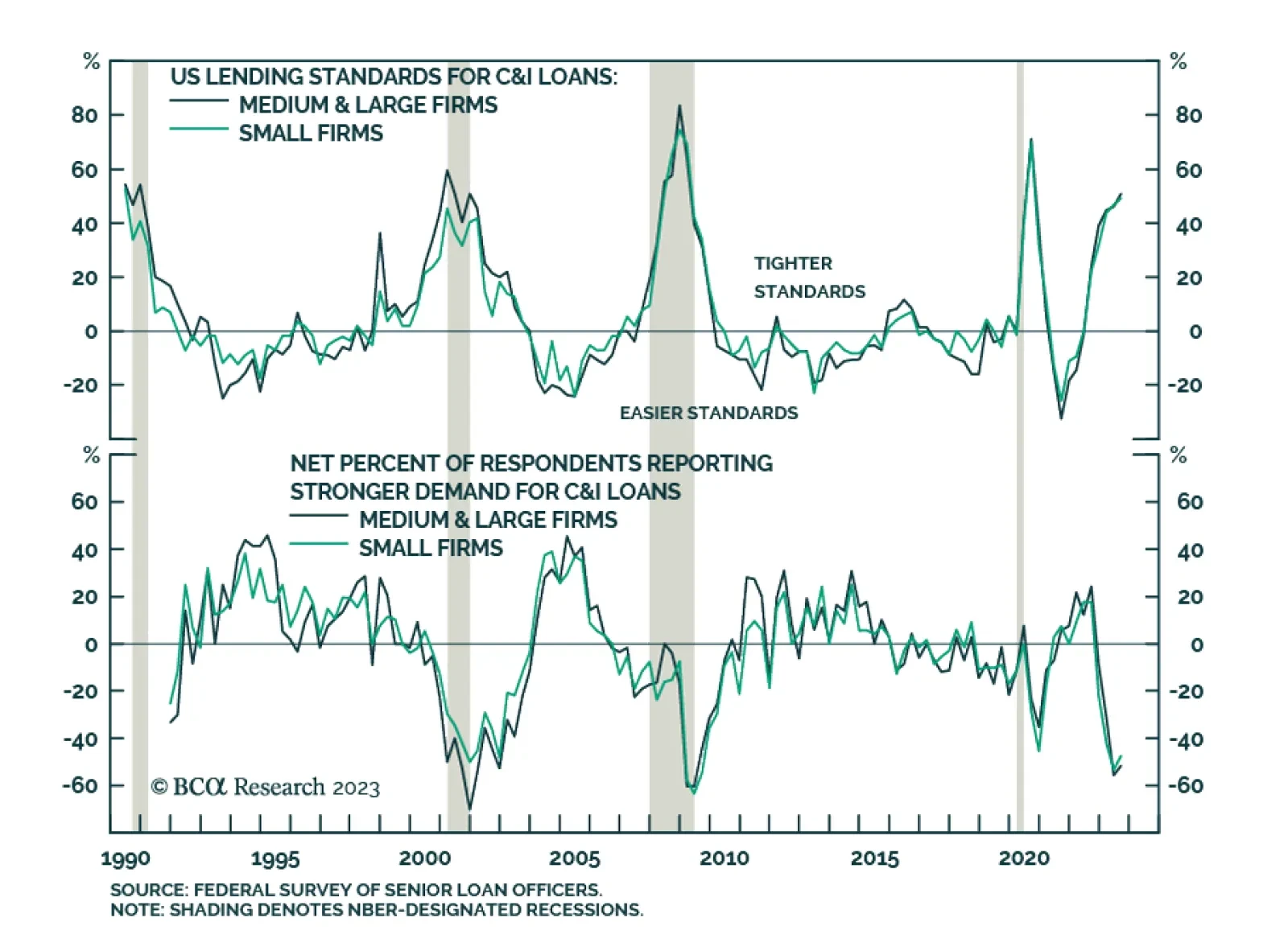

The US Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) reveals that US banks continue to tighten lending standards for commercial and industrial (C&I), commercial real estate (CRE), residential real estate (RRE), home equity lines of credit…

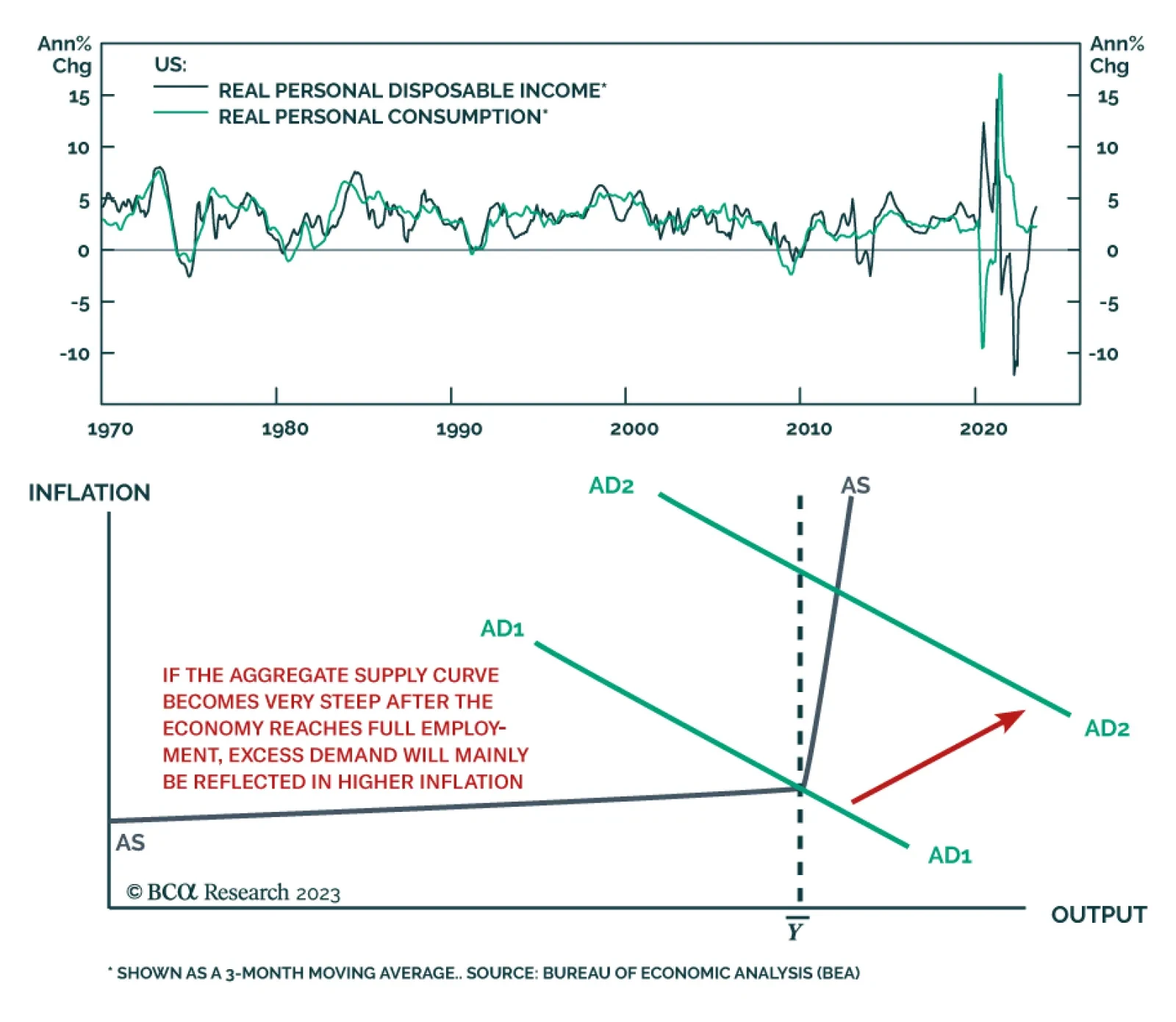

According to BCA Research’s Global Investment Strategy service, it is too early to conclude that the Fed can stop raising rates. Consumption and real income growth are highly correlated. If inflation continues to fall, real wages will rise further. If that…

As expected, the ECB delivered a 25 basis point rate increase on Thursday, raising the policy rate to its 2001 record high of 3.75% and marking its ninth consecutive rate increase. The most important takeaway from the meeting is the absence of forward…

Over the past two months, copper has rallied alongside risk assets and now stands 9% above its late-May trough. Here, the outlook for China’s economy – which accounts for over half of global refined copper usage – is key to whether the red metal will continue…

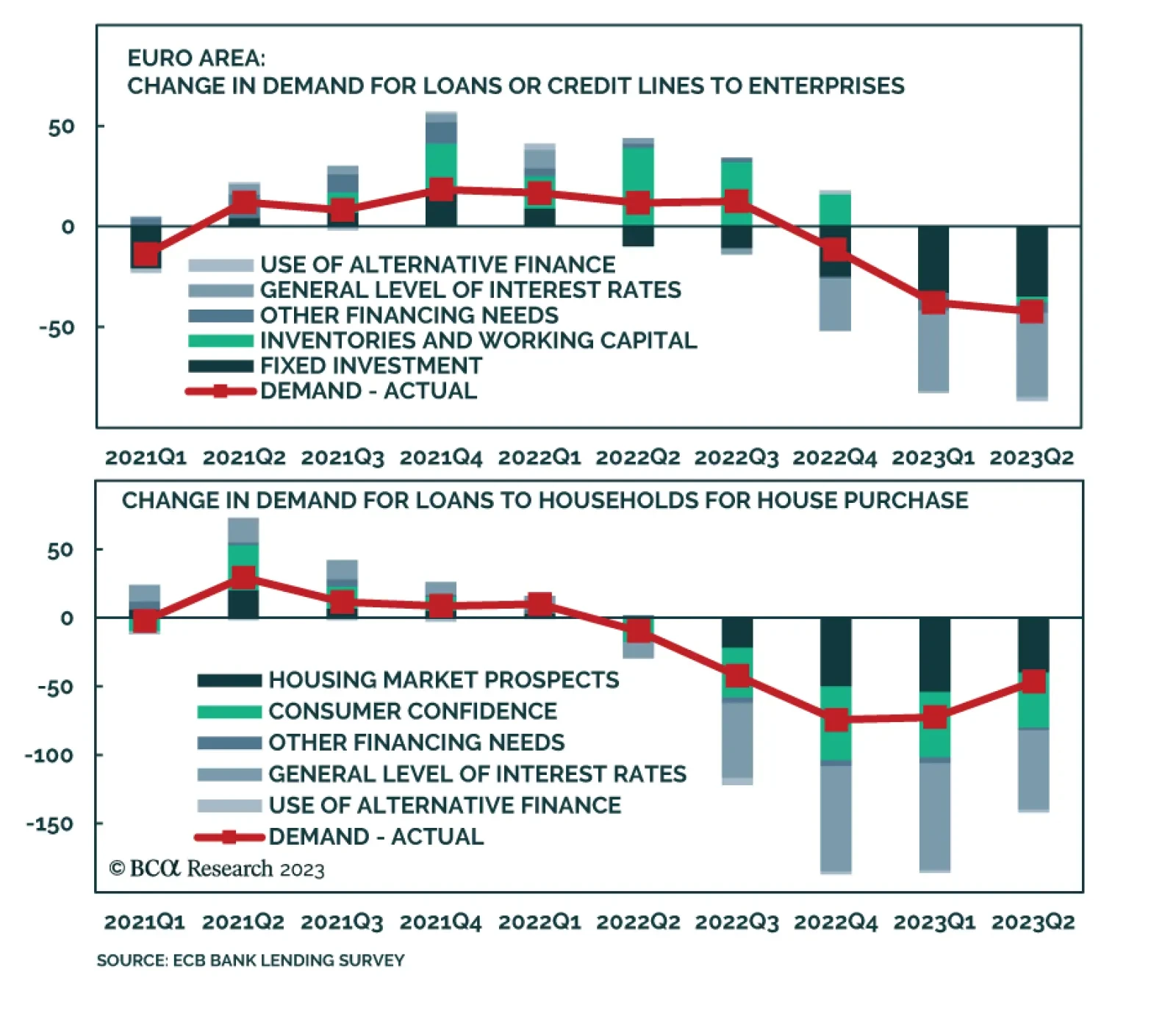

Results of the ECB’s bank lending survey (BLS) show the impact of the central bank’s aggressive tightening cycle on the region’s economy. Uncertainty about the economic outlook, borrower-specific dynamics, lower risk tolerance and higher cost of funding…

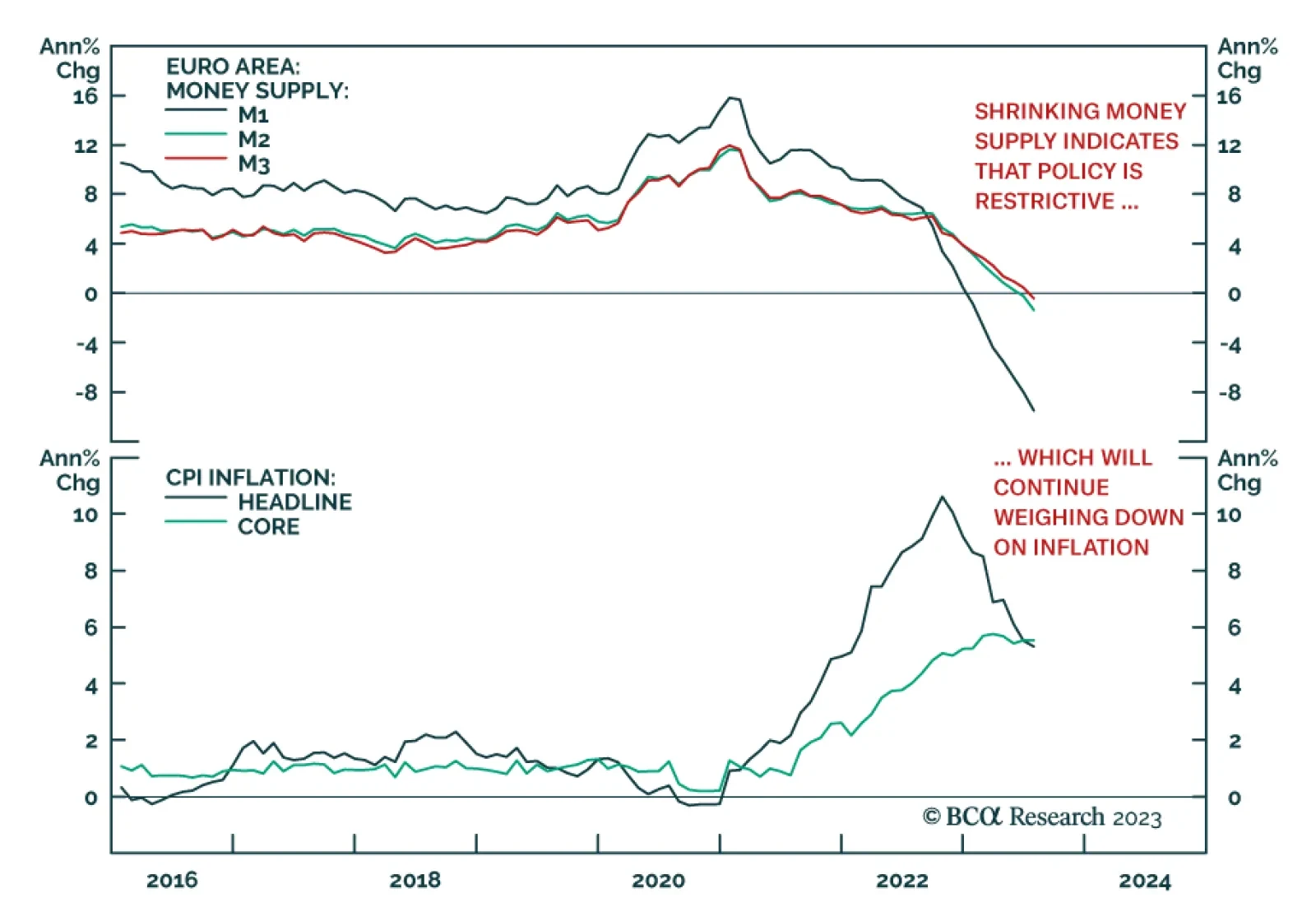

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.