Money Trends / Liquidity

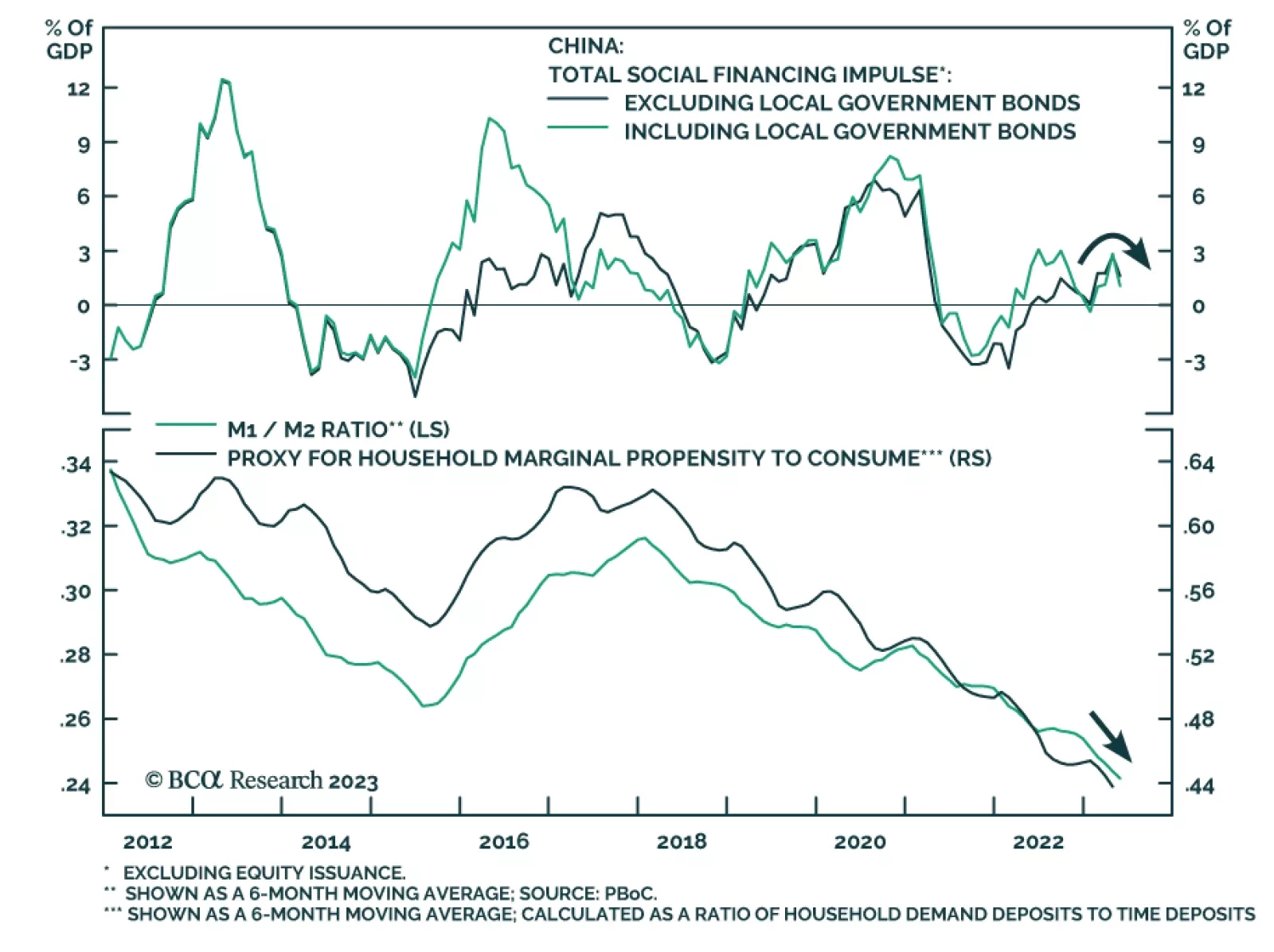

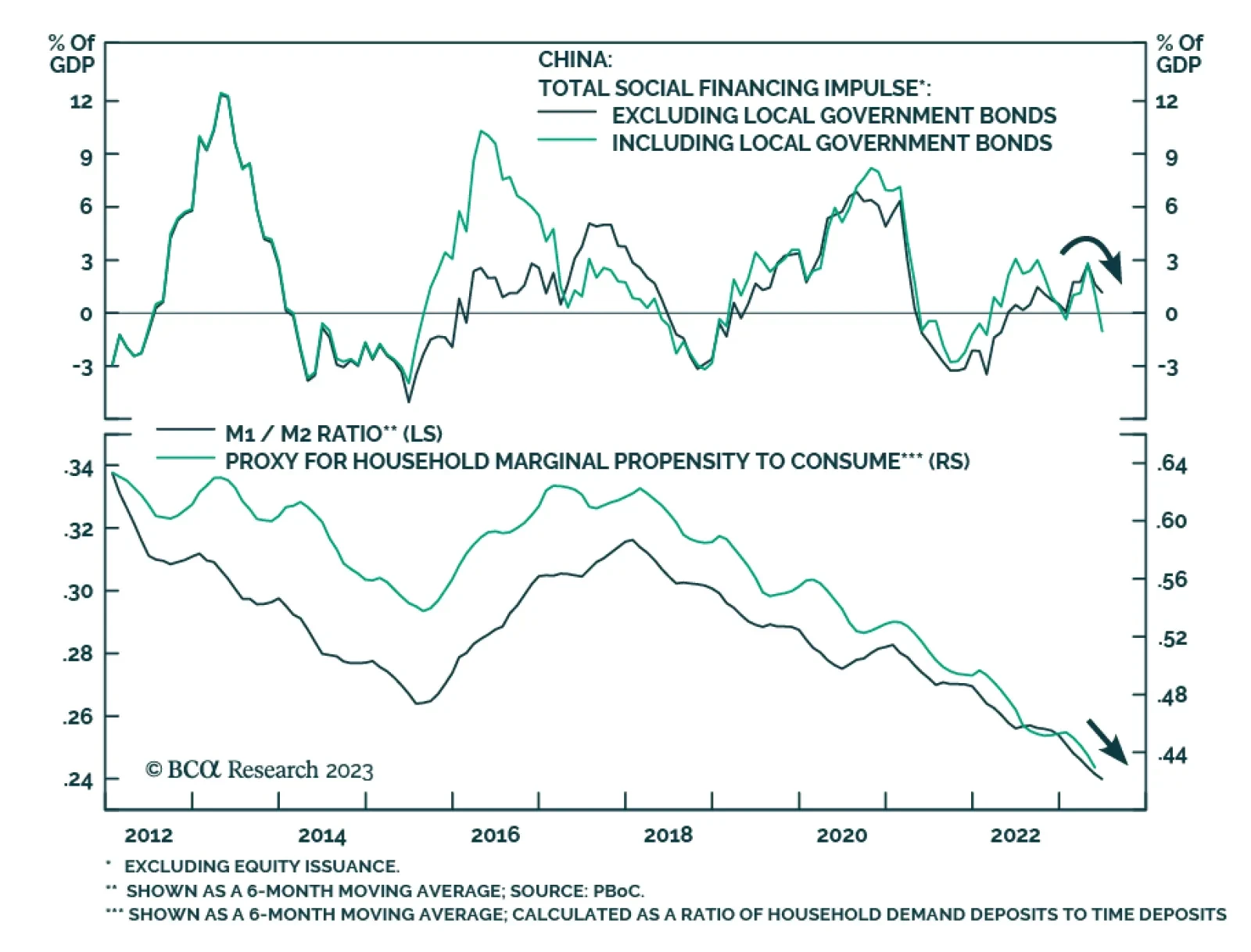

The combination of a global manufacturing recession and tight/tightening policy is raising a red flag for global non-TMT stocks. In China, households are entering a liquidity trap, and deflationary pressures are heightening. Authorities need to reduce interest rates considerably and allow the currency to depreciate. By doing so, China will export its deflation to the rest of the world.

Assuming yesterday’s policy rate hike is a sign that Turkey is finally veering towards orthodox economic policies; should investors rush in?

This week’s report examines three potential catalysts that could push Treasury yields meaningfully higher within the next few months. We also consider the rebuild of the Treasury’s cash holdings and its implications for the Fed’s balance sheet policy and financial markets.

China is facing a risk of deflation. Marginal interest rate cuts and targeted stimulus will be insufficient to boost China’s growth given the current deflationary mindset and the danger is that the economy may be entering a liquidity trap. Deflation is bullish for government bonds, but negative for equity prices. Chinese share prices will continue to decline.

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.

Policymakers will likely continue to stimulate domestic demand via targeted measures and piecemeal stimulus. Yet, the economy will disappoint unless Beijing provides “irrigation-style” stimulus. The latter is not our base case scenario.