Oil

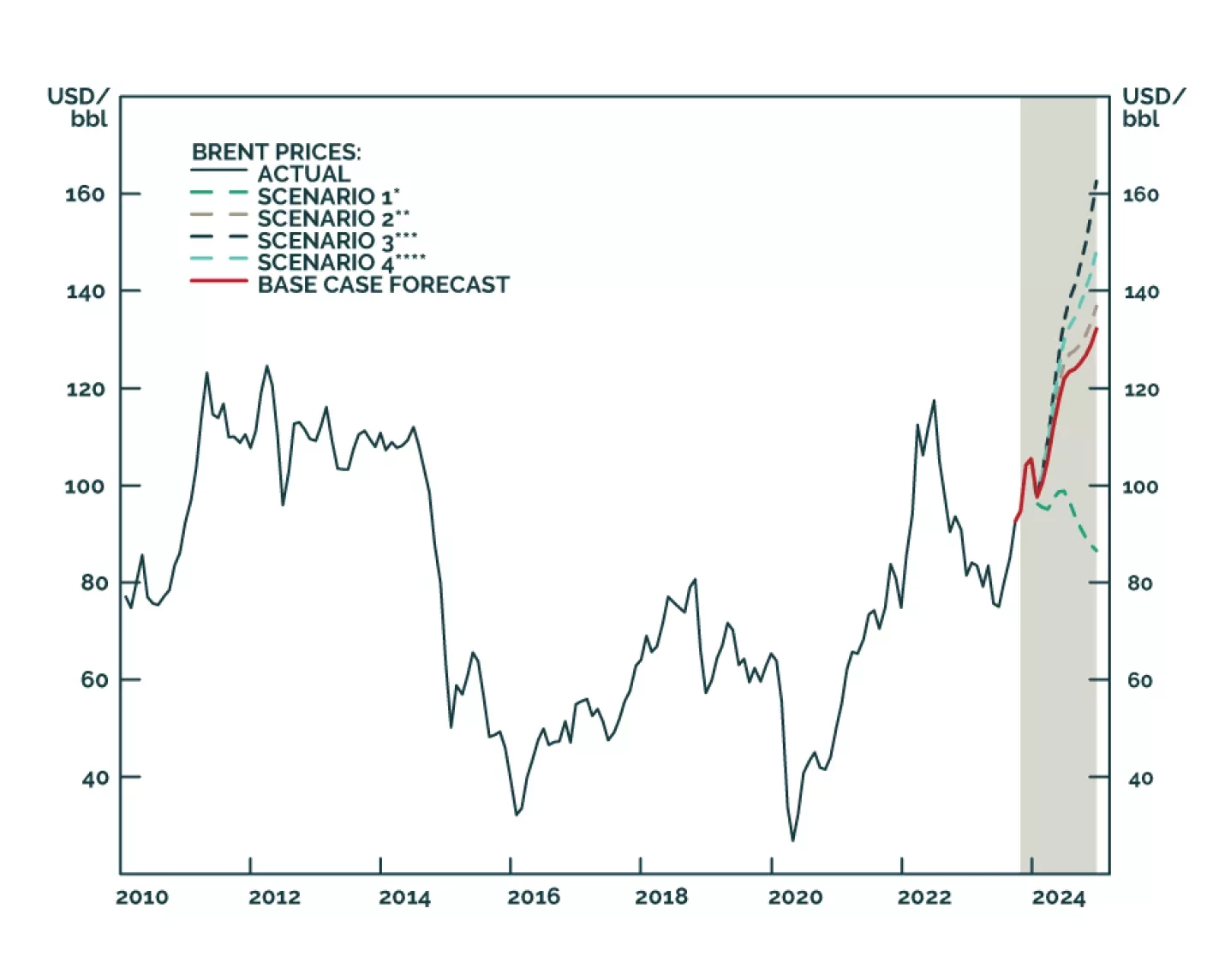

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

The Israeli-Arab crisis is more likely to expand and cause oil disruptions than market consensus holds. Close long dollar trades and go long energy and defense stocks relative to cyclicals.

Hamas’s attack on Israel raises the odds of a wider conflict in the Gulf, which would lead to higher oil prices. Given the response of oil prices Monday, markets appear to be relatively restrained in their assessment of a sharp escalation in prices. However, this is early days in a strategy that is just revealing itself.

Volatility will remain the key dynamic in oil markets in the aftermath of the surprise Hamas attacks against Israel on October 7. The risk of a major oil supply shock has gone up, but meanwhile supply constraints will remain at variance with global growth problems stemming from restrictive monetary policy over the next 12 months. Favor bonds over stocks, large caps over small caps, defense and energy stocks over other cyclicals, and US equities relative to global equities.