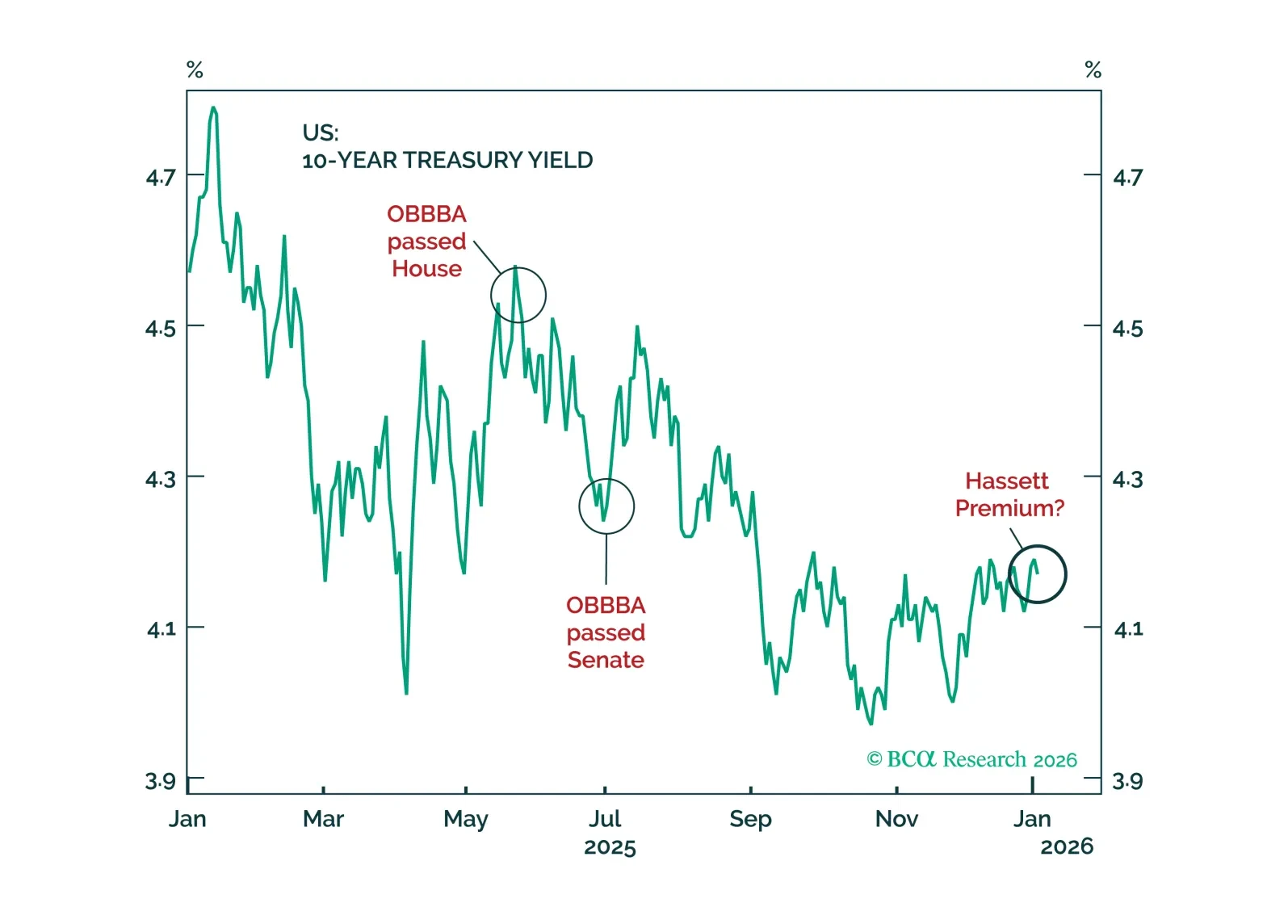

The first week of January is always the most difficult for investment strategists. The annual outlook is usually penned in early December. Ours went to your inbox on December 2, perhaps too early to get a read on the next 12 (really 13!) months. But between the publication of the outlook and the first week of January, rarely does much happen to the economy and the markets that makes a difference, certainly not for the next 12 months. As such, what is there to say but to repeat the overarching view from the annual outlook? This conundrum plagues anyone who attempts to forecast over the 12-month horizon. It is a curious horizon over which to measure one’s performance. Some of our clients swear that they care about it, but most do not in real time. For many strategists, it is often an intellectual crutch, allowing the forecaster to ignore the imminently relevant by focusing on some moving target beyond the near term that they either do not understand, or that moves against them.1 A strategy great for one’s self-preservation, but terrible for the actual team performance! In November 2025, we interrupted our maniacally bullish outlook by warning that we are “shortening our time horizon in 2026.”2 In the aforementioned Annual Outlook, we turned neutral on risk assets on a tactical basis, while holding out hope that the global economy would avoid a recession in 2026.3 Today, we turn tactically bearish on equities, while maintaining our modestly bullish 12-month outlook. Why? As we posited mid-year 2025,4 “if we are not under 4% [Treasury yield] by the end of the year, stocks will suffer.” The S&P 500 has hovered around our 2025 end-of-the-year target of 6,9505 since the end of October. However, it has been unable to break through it. We would posit that the “stickiness” of the US 10-year Treasury yield is the culprit. The peak in S&P 500 was essentially reached at the end of October, just as yields bottomed under 4%. But yields have backed up since then (Chart 1). The three reasons why bonds rallied from May to October are somewhat at risk. Economic weakness. Sure, some of the demand for bonds had to do with general economic malaise, the K-shaped economy, and the subsequent impact this all had on inflation, which for most of 2025 was tamed (after well-known passthrough effects, like tariffs) and well anchored on the long end (Chart 2). And while the strong AI capex surge supported the economy, it did so with no impact on either the labor market or inflation, allowing the Fed to ignore the strong growth numbers and focus on its twin mandate. Tariff certainty. To the surprise of some investors, the April “Liberation Day” led to a vicious bond market selloff. Yields shot up by 47bps from April 4 to April 11 (Chart 3). In our view, this had little to do with inflation. Onerous tariffs are not inflationary, they are disinflationary as they threaten economic growth. As such, bonds ought to have rallied. But they did not for two reasons. The “Howard Lutnick” approach threatened both global demand for US Treasurys and US fiscal discipline. First, punitive tariffs would have led to a global selloff of US government bonds by foes and allies alike, as Japanese Finance Minister Katsunobu Kato threatened that Tokyo was prepared to do on May 1.6 Second, tariffs are – just like any other tax – subject to the Laffer curve, a relationship between tax rates and government revenue. Tariffs set too high would discourage trade and thus lead to diminishing marginal receivables in government revenue. Once President Trump sidelined Commerce Secretary Lutnick – and his sidekick Peter Navarro – from the negotiations, the bond market rallied. With Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer in charge, both the trade and tariff policy of the US became more coherent, giving the bond market comfort that it would not be sacrificed at the altar of neo-McKinley-ist nonsense. Fiscal prudence. The start of the bond rally from May to October 2025 coincided with the passage of the One Big Beautiful Bill Act (OBBBA), which has confused many investors and commentators who mistake President Trump’s populist instincts with effective policy outcomes (Chart 4). President Trump is not a king, nor is his Republican Party made up (completely) of sycophants. As such, the OBBBA that investors got departed massively from their expectation of profligacy (Chart 5). Gone were the vast majority of President Trump’s campaign promises from 2024. Even without the tariff revenue, OBBBA does not add to the budget deficit. We went long duration in June because of our correct assessment of these three dynamics.7 However, since about October, two sources of uncertainty have begun to impede the downward trajectory of yields. First, our colleague Ryan Swift – Chief US Bond Strategist of BCA Research – has articulated that a “Kevin Hassett premium” may be creeping into the markets (Chart 6).8 We think that the negative focus on Hassett is not fair. Our heterodox view is that the Fed has never been independent to begin with.9 Nonetheless, Hassett has now become a totem for the epistemic community that cares about supposed monetary policy orthodoxy. As long as there is a risk of central bank independence eroding, a Hassett premium may be necessary. In our view, President Trump will not erode Fed independence beyond some standard level of erosion that is well within the historical pattern. He will simply do what almost every president in US history has done: cajole the Fed into a more dovish setting than the market and the economy really require. Oh no… the horror. Second, our controversial fiscal view – that OBBBA is not profligate – allowed us to correctly call an epic bond market rally in 2025. However, that call is going to be challenged in 2026. President Trump is openly flirting with fiscal stimulus, calling for both a “tariff rebate”10 and already falling in love with his newfound power to stimulate by cutting tariffs. After cutting tariffs on food items in mid-November,11 he moved on to delay tariffs on furniture.12The real risk to the perceived fiscal position of the US will be the US Supreme Court ruling on tariffs. Expected at some point in January, Polymarket online bookie continues to show just a ~25% probability that the tariffs are upheld. We disagree with Polymarket – and agree with our colleagues on the GeopoliticalStrategy team – that the odds are likely reversed, with 75% probability that tariffs are upheld. However, our conviction is low. If we are wrong, the Supreme Court could imperil the roughly $3 trillion of revenue that tariffs are expected to produce over the next decade. While OBBBA is not really profligate, the bond market will nonetheless riot in the face of US policy incoherence. Tariffs may not be a great way to raise revenue, but they are an effective way to do so. If the Supreme Court invalidates that approach to raising revenue, what other approach is left that the bond market can take seriously?At this point, both the equity and bond markets are on a knife’s edge. We believe that they remain positively correlated, although the relationship is weakening (Chart 7). This is potentially a very confusing time for investors, but we stick to what has worked for us over the past three years. A lot of the good news from 2025 is already priced in. Inflation has surprised to the downside throughout 2025. Geopolitics proved to be an empty risk in 2025. A US-China détente is in place. Trade war uncertainty has crested (Chart 8). The Fed has turned dovish. Growth has surprised to the upside in the third and fourth quarters. Going forward, the risk-reward balance no longer favors a maniacally bullish outlook. In fact, the bond market may need to do some work to push President Trump into a more prudent default policy setting. His chief economic advisor – and Fed Chair candidate – Hassett has already walked back the president’s tariff rebate promise, by stating that Congress would ultimately decide.13 But more work may need to be done by higher yields to dissuade Trump from stimulating ahead of the midterms. A Supreme Court decision could throw all the fiscal forecasts astray. Yes, the president has alternative legislative acts upon which to base his tariff decisions, but they may come under legal attack as well. Much will depend upon the nature of the Supreme Court decision, which is why a careful read will be necessary if a negative ruling is the outcome. While we close our long bond trade for a 2.8% return, we do not intend to short duration. Instead, we retain our steepener trade – long 2-year US Treasury / Short Duration-Matched 10-year US Treasury that we have had since June.14 We also note that rate VOL has collapsed (Chart 9), suggesting that next move may be quite disruptive. Sophisticated investors should gain some exposure to measures of the MOVE index. As for equities, we are turning tactically underweight on a three-month horizon. The fundamental logic behind a positive bond-equity market correlation is that the US economy needs lower borrowing rates if it is to avert a significant slowdown. Payroll growth has broken down (Chart 10) even after seven months of anemic job creation (Chart 11), as our colleague Doug Peta has recently pointed out.15 Sixty-eight percent of US GDP is consumption. Yes, AI capex investment continues apace, but it cannot drive US growth forever. Worryingly, the latest data suggests that AI investment – in terms of its contribution to GDP growth – is beginning to falter (Chart 12). With the cash-fueled economy now depleted, US growth needs to begin transitioning towards more leverage-fueled variety. That cannot happen with yields stuck at above 4%. What could make us turn bullish on global risk assets from here? Aside from US bond yields moving in the opposite direction, there are three bullish vectors we are following. To make sense of these three themes, we rely on a checklist approach. Any one of these themes – US housing recovery, AI capex, or global growth – could lead risk assets higher. As such, we dedicate the rest of this monthly Alpha report to how to monitor each theme. We intend to check these lists often over the rest of this quarter. Housing Re-Leveraging Since 2024, we have warned investors that American policymakers will be tempted to reflate the under-levered US consumer following the next growth slowdown.16 The Trump administration agrees with us, which is why they have been signaling that the White House may declare a “housing emergency” in 2026. What will that mean in terms of policy? We are not sure but think that everything is on the table. From widening the eligibility for assumable/portable mortgages17 to using macroprudential tools to suppress borrowing rates.18Thus far, the administration has hesitated to give any coherent direction. However, the news flow is strong,19 with housing clearly becoming the key macro story for 2026. This makes macro sense. Our assertion that the US is at the end of its fiscal gravy train is supported by longer-term bond market behavior and even voter fatigue with wanton stimulus (Chart 13). With the fiscal lever increasingly stymied by bond market riots and uncooperative legislators in Congress, it is only natural that the President will lean on a mix of dovish monetary policy and macroprudential housing reforms that ease borrowing rates for households. The question that we do not have an answer for, however, is how low do borrowing rates have to go to help the US consumer? For car loans and credit cards, apparently a lot lower, with delinquency rates rising for both (Chart 14). For housing, at least 100bps lower, according to latest survey data (Chart 15). What is concerning in Chart 15 is that survey respondents lost appetite for 5.5-6% mortgage rates over the second half of the year, especially as the savings rate plunged amidst a sluggish labor market. To gauge the success of President Trump’s policy on housing revival, we will be tracking: The spread between 30-year mortgage rates and the 10-year yield (Chart 16).Mortgage applications – both for refinance and purchase (Chart 17).Housing starts and S&P 500 homebuilders (Chart 18).Home improvement and appliances equities (Chart 19).Lumber prices.Our checklist offers a fairly grim reading at the moment. There is simply no evidence that the Trump administration has managed to unlock housing in any way. They will either manage to do so over the next six months via reforms and macroprudential unorthodoxy, or the economy may need to experience a recession before borrowing rates are allowed to fall meaningfully. Bottom Line: Housing policy will be the macro variable to watch in 2026. We are optimistic that, over the course of the next 12 months, the Trump administration will successfully reflate the economy via the housing lever. However, our conviction is low, and our checklist shows little evidence that our view is correct. The AI ChecklistOur luddite AI view is well known to our clients.20 While highly skeptical of AI’s sustained contribution to productivity, we have decided to cozy up to the “House of Cards” that we believe the capex buildout really is.21 There is no reason to fight a mania or a bubble. At least not in its early stages. That said, the AI news flow is not looking good. There have simply not been enough new technological breakthroughs worthy of media attention. One of the latest developments – Google’s Gemini 3 release in mid-November – has already petered out, with many users complaining that the hallucinations of the model remain a significant problem.22 In 2026, we could be pleasantly surprised by positive developments in the AI story. As such, we are following closely several data points to ensure that we are not blindsided by optimism. The US Census Bureau survey of corporate America on AI adoption shows a gap between aspiration and reality. If that gap does not close in 2026, on the side of aspiration, we fear that the AI capex story will begin to wane as a source of positive market inertia (Chart 20).The BCA Productivity Indicator – featured recently in an update of the BCA Research AI productivity checklist23 – is rising but not yet confirming that AI has contributed to a productivity jump experienced by past tech booms (Chart 21). Outside of recessions and their subsequent recoveries, indicator values above 70 are a sign of a legitimate productivity boom. The chart shows that our Q3 estimate of productivity growth implies that the indicator will likely rise to 65. That is not yet above the threshold, but it is getting considerably closer.Corporate profit margins remain high and stable (Chart 22). There is no evidence that AI has boosted those margins. In fact, the promise of AI is that it would boost non-tech profit margins as the new technology is adopted en masse. That is not happening (Chart 23). In fact, ex-tech return on equity is trending lower (Chart 24). Specifically, it will be important to see small- and medium-sized companies that dominate the bulk of employment in most developed economies, adopt AI. Why they have not adopted it already, given price sensitivity, is confusing. A recent Brookings survey (Chart 25) shows that an extremely small percentage of workers identify any significant impact of AI on their productivity. We break the survey up by age groups to illustrate that the pessimistic result is not a product of some “Boomer effect.” It is important from this chart to note that productivity did not decrease significantly, but we are not seeing an AI revolution from this survey, for now.Bottom Line: There is no real evidence that AI adoption is accelerating or that it can sustainably contribute to productivity growth. And yet, the commitment to the capex buildout of data centers continues. A capex buildout built on optimistic enthusiasm about the underlying technology is a boon for multiples. But that could very easily turn into a bust if the underlying technology loses its shine. China Stimulus Checklist Our final checklist has to do with global growth and global stimulus. As we posited in the 2026 Annual Outlook, our global asset allocation view – underweight US relative to the rest of the world (RoW) – depends on the RoW offsetting the end of the US fiscal gravy train with domestic stimulus of its own. Thus far, the IMF Fiscal Monitor is skeptical of our view, with too many “red cells” in Table 1, suggesting that most major economies are not planning to offset the decline in US fiscal thrust over the next 12 months. Germany is doing its part, but few other countries have joined it in an act of coordinated fiscal stimulus. China is the big puzzle to us. It is overly dependent on investment and exports, with the latter driving growth thus far. This is an unsustainable geopolitical position for Beijing, too much of its final demand is domiciled within borders of its adversaries. And yet, Beijing has continued to be aloof of this reality, with little support for its economy on the home front. Our colleague Jing Sima, BCA’s Chief China Strategist, expects government consumption and state investment to step up substantially in 2026.24 A core pillar of Chinese growth – manufacturing capex – has begun to contract sharply (Chart 26). Jing’s China Economic Pressure Indicator (EPI)25 is flirting with levels that have, in the past, nudged Beijing to stimulate (Chart 27). The EPI is weighted towards variables that capture Chinese households’ livelihood and sentiment and all those subcomponents – labor market measures, consumption propensity, retail investor sentiment, and housing sector – are near the pain threshold for the Middle Kingdom. Bottom Line: Jing does not expect major policy action in the first two quarters of 2026. This would be disappointing for global investors. Our bearish USD view may also suffer, given that US fiscal stimulus – such as it is – is frontloaded in 2026. Nonetheless, Chinese policymakers are ultimately going to succumb to the pressure on their economy over the course of 2026. Combined with our view that President Trump will want to nail down the détente with Beijing ahead of the midterms, we expect Chinese assets to have another strong 12 months. We are looking to initiate a long RMB position as a result in anticipation of a considerable divergence between US and Chinese growth over the course of 2026. That said, we will wait for a better opportunity, if Chinese data disappoints in the next few months, dropping the EPI index to a nadir.Introducing “The Age Of Empires Premium”We have been commodity bulls since 2021.26 Underpinning that thesis is our understanding that a multipolar geopolitical environment is a boon for capex and investments.27 When faced with geopolitical uncertainty, countries pursue strategies that increase their resilience in that environment. That effort requires physical structures to be built. Whether that is alternative transportation routes, new energy sources, or industrial plants to create resiliency of supply. Yes, the effort also includes more defense spending, which further aids industrial sectors. But, at the core of the endeavor is an increasing demand for commodities. Our view has been borne out in the performance of industrial metals. Despite an absolute carnage of Chinese real estate demand, metals have held up (Chart 28). Undoubtedly our view has also been aided by the AI capex boom as well. To the litany of commodity bullish factors investors can now also add an “Age of Empires-like” scramble for commodities. To those of you who are unfamiliar with the popular computer game, The Age of Empires, the brief summary is that it is a strategy game built on hoarding of key resources. Players send their villagers out to cut the timber, mine for gold, and till the fields in order to win. President Trump’s unabashed intervention in Venezuela and repeated talk of annexing Greenland break all norms against hoarding of natural resources that may have existed since the end of the Cold War. The premise that all of the world’s commodities are freely traded on the open market – and thus need not be horded – has been upended. While the case of Venezuela is an obvious one, President Trump’s assertion that the US “needs” Greenland is far more jarring.28 Greenland is part of Denmark, a staunch US ally even above and beyond its fellow NATO member states. Whatever commodities are mined in Greenland are freely available for US industrial, tech, and defense use. That, apparently, is not enough for President Trump and his advisors. This is a major norm departure. One that we suspect will lead global powers – but also investors – to begin hoarding physical commodities, creating a geopolitical “Age of Empires Premium” above and beyond supply and demand dynamics. Such non-economic demand has already ensnared precious metals. We suspect that 2026 will see a violent rise in demand for industrial metals as well. At the moment, we are long copper, nickel, and palladium in this space, but may add more to our portfolio soon. The irony of President Trump’s intervention in Venezuela, therefore, is that it was partly motivated by a desire to increase America’s access to critical commodities. The reality, however, is that it has done precisely the opposite. We also disagree with the consensus that oil prices should fall given the opening up of new supply in Venezuela. The 2025 story of oil prices is almost exclusively one of increased OPEC+ supply. As we recently penned in our net assessment of Saudi Arabia, OPEC+ policy may have to be reversed due to Riyadh’s policy priorities and deteriorating fiscal picture.29 Meanwhile, Venezuela is highly unlikely to bring online any new oil barrels in 2026, nor in any conceivable future. As a result, we will initiate a long Brent position, with a tight stop-loss of 3%, with the expectation that Riyadh will eventually succumb to domestic pressures and reverse the max-production OPEC+ policy at some point in 2026. We are also buying energy equipment and services companies, a high-beta play on rising oil prices. To this, investors should also add a “Chuck Norris premium.” Named after the Hollywood macho demi-God of the 1980s, this premium ought to be applied to oil prices now that the US has shown a proclivity to special operations-induced regime change. The capture of Venezuelan President Maduro was a spectacular success. Policymakers rarely bottle up their successes on the shelf. They tend to want to repeat them. We fear that President Trump may decide to try his hand at more such regime change operations, with Iran potentially next in line. If this is the case, we would expect Iran to act much differently than it did in 2025. Last year, we cautioned our clients not to go long oil due to the Israeli and American attacks on Iran. Neither threatened the regime existentially. But an overt attempt to attack the leadership could elicit a much different response from Tehran. Bottom Line: The “Age of Empires Premium” calls for a significant long industrial metals position by global investors. The “Chuck Norris Premium” suggests that oil prices are reaching their bottom, as Saudi Arabia’s domestic politics but also geopolitical risks shift from bearish to bullish for oil prices. We take a dramatically different view on what the US intervention in Venezuela means for commodity prices. Not only is it not bearish for oil prices, it may be epically bullish for industrial metals. Marko PapicChief Strategist,GeoMacro & BCA Accessmarko@bcaresearch.com HousekeepingAs the front section of the Alpha report suggests, we are having to digest a lot of information as we enter 2026. Paradoxically, the constant influx of information is helping us build an “all weather” portfolio that has a strong bias to some of our core views.Let us review some of the core themes that underpinned our trades in 2025 and provide some guidance on how we see these evolving in 2026. Hard assets versus financial assets: This remains in place. Silver, platinum, palladium and gold were some of the best performing assets in 2025. This will continue in 2026, with some rotation into other hard assets that are truly scarce.The equity-bond correlation: The present value of cash flows will continue to rise – if bond yields in the US fall and remain below 4%. They are stubbornly above that level.US exceptionalism: We remain of the view that US exceptionalism is over, and recent events have certainly challenged that. That said, we posited not to fight The Trump. More on this below.EquitiesOur equity view is shifting, aligned with the checklist we are providing in the front section of this Alpha report. We are turning bearish on a three-month horizon. As such, we will start focusing more on trades that have asymmetric returns, rather than playing the directionality of markets. Our S&P target for the end of 2026 is still 7,500, but we have fat tails around that forecast. Twelve months is a long time, and we suspect that we may “round trip” towards that target over the course of the year.Starting with the new bets, buy energy servicing companies in the US that will benefit from President Donald Trump’s bet to “run” Venezuela. These companies are cheap and actively being derated given the weakness in oil prices. Our favorite vehicle to play this is the IEZ ETF. We are also going long Brent at these levels, a hedge against our “Chuck Norris Premium” (the risk of further regime change actions by the president, particularly when it comes to Iran).30For the rest of our equity trades, we are putting on a trailing 5% stop. We still like European and Japanese industrials equities, which will benefit from a capex cycle that rotates from the US towards other markets. Both Europe and Japan will also have an energy dividend from lower LNG prices, that will benefit industrials. The 5% trailing stop on these positions is just prudence, should a market shakeout prove violent in the coming months.On the other side of the equation, we are maintaining a short position in Business Development Companies, via the BIZD ETF. Stubbornly higher yields will prove to be a headwind for these companies, at least in the short term. We still like Canada relative to other developed markets. For one, Canada is a resource play and should continue to do relatively well, given our theme of liking commodities. Another point is our bullishness on the eventual outcome of the USMCA negotiations. Finally, we are looking to buy US homebuilders soon. Any sign that the US consumer is starting to re-lever will be a catalyst to put on this trade. Watch lumber prices carefully, as well as mortgage spreads for signs that this theme is taking hold. Fixed IncomeThere is one major change to our bond trades – we are taking profits on the long 20+ year US Treasury, given the risks that yields could remain stubbornly high for the time being. In the near term, we see the potential for yields to fall more in the UK and are expressing that view by being long December 2026 SONIA futures. We also think the US 2/10 curve continues to steepen and so are keeping that trade on. CurrenciesOur dollar bearish view remains intact, and we are short USD/JPY, USD/CAD and USD/EUR. Long term, the yen is likely to outperform both the euro and CAD, given deep levels of undervaluation. We would also be long any Japanese stocks unhedged, to benefit from yen appreciation. Our long MXN/CHF position continues steady appreciation, and will benefit from an attractive carry, any upside in oil prices (and related plays), and any push by the Swiss National Bank to limit franc strength through intervention, now that monetary policy bullets have been mostly exhausted.CommoditiesWe have been adding to our commodity basket, having bought nickel and copper, in addition to our core palladium holding. We are holding on to these positions. We will be opportunistically exploring other industrial metals to add to our list.On silver, we think the rally is overextended in the short term and so will not be chasing prices higher for now. But we are watching this space closely, given that fundamentals still favor the metal, especially relative to gold. We have been offside on our long Henry Hub natural gas position and are closing that trade today, for a loss of 18.9%. The market has looked through the cold spell that hit part of the northern hemisphere, in anticipation of some warmer days ahead. Natural gas injection levels in the US are also within the norm of the past few years. We will continue to monitor this space closely.See Chart 29 and our Trade Tables for all our trades.