Packaged Foods

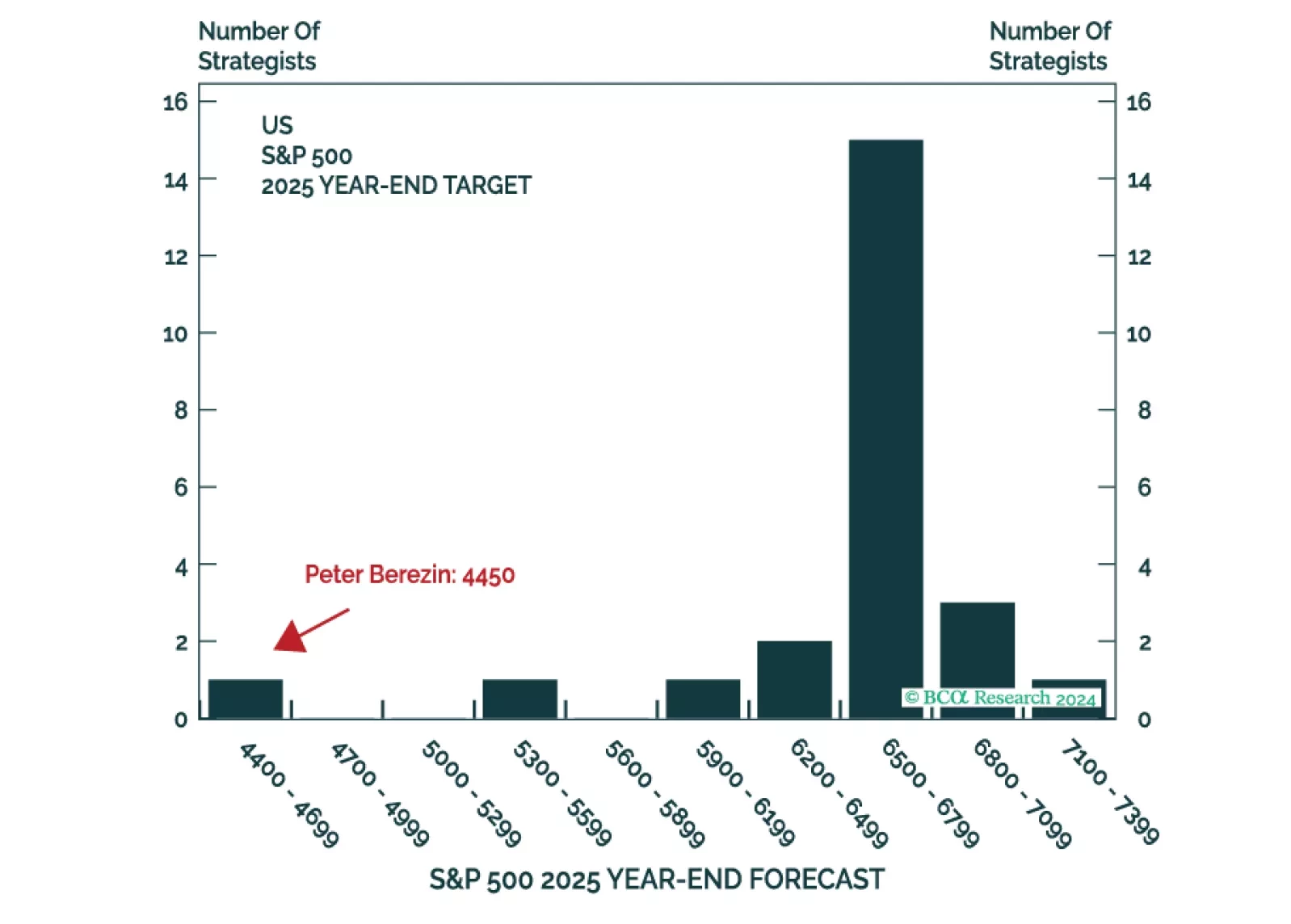

This is the time of the year when strategists are busy sending out their annual outlooks. Here on the Global Investment Strategy team, we decided to go one step further. Rather than pontificating about what could happen in 2025, we decided to harness the power of the multiverse to tell you what did happen (in at least one highly representative timeline).

Next week, please join me for a Webcast on Tuesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets.

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2025. We will be back in the first week of January with our MacroQuant Model Update.

High food and fertilizer prices could morph into food crises in several developing nations. A Special Report from our Emerging Markets Strategy team reckons that Lebanon, Egypt, Kenya, Peru, Pakistan, and Sri Lanka are most at-risk of slipping into a food…

Neutral Following up from last week’s report, we heed the message from our research to be wary of staples stocks at the depth of the recession and downgrade the S&P packaged foods index to neutral. Food & beverage store retail sales now garner 17% of total retail sales - a percentage last hit in the early 1990s. As a result, relative share price momentum came close to accelerating by triple digits on a short-term rate of change basis (middle panel). While such euphoria is warranted, we reckon that most if not all the good news is already reflected in prices, especially given the early signs of a possible reopening of the US economy some time next month. Importantly, sell side analyst optimism has climbed above the previous peak observed in late-2015/early-2016 when industry 12-month forward EPS were slated to outshine the broad market by over 10% (bottom panel). Bottom Line: Trim the S&P packaged foods index to neutral. This downgrade also pushes the S&P consumer staples sector to neutral. The ticker symbols for the stocks in this index are: BLBG: S5PACK – MDLZ, SJM, KHC, CPB, MKC, CAG, TSN, GIS, HSY, HRL, K, LW. For additional details please refer to our most recent Weekly Report.

Highlights Portfolio Strategy Our conservative dividend growth assumptions especially for the next three years – largely mimicking the GFC experience – result in an SPX 3,000 fair value target. Relative performance already reflects the jump in demand for packaged foods. A firm US dollar and an ongoing profit margin squeeze at a time when relative valuations have returned to the historical mean compel us to downgrade the S&P packaged foods index to neutral. An upward trending demand profile, a fortress of a balance sheet, exemplary recession resilience, and sustained M&A activity, all warrant an overweight stance in the S&P software index. Recent Changes Trim the S&P packaged foods index to neutral today, which pushes the S&P consumer staples sector to a benchmark allocation. Boost the S&P software index to overweight today, which lifts the S&P tech sector to a benchmark allocation. Table 1 Feature The SPX jumped to a five-week high last week, on the back of news that the economy will gradually reopen next month. In other news, GILD’s remdesivir drug showed some positive early signs in fighting off the coronavirus, sparking an impressive late-week rally in the SPX. From a macro perspective, flush monetary liquidity and extremely easy fiscal policy remain the dominant market forces. While we remain confident that equities will be higher on a 9-12 month cyclical time horizon, we believe that the easy money since the March 23 lows has already been made and a consolidation phase now looms. Thus, monetizing some of these gains would make sense at the current juncture. Keep in mind that the SPX, junk spreads and the CBOE’s put/call ratio have returned to their respective means since 2018 (horizontal lines denote the historical averages, Chart 1). Tack on the stiff resistance that the S&P 500 will face near the 50-day and 100-week moving averages, and a lateral move is likely in the coming weeks. Meanwhile, in our seminal report “SPX 3,000?” on July 10, 2017 we introduced our SPX dividend discount model (DDM) when we first came up with the SPX 3,000 target.1 It is now custom to update our DDM every April when the previous year’s annual S&P 500 dividend payment is finalized from the Standard & Poor’s. Chart 1Consolidation Mode Chart 2Dividends Rule As a reminder, we have been and remain very conservative in our DDM assumptions. Again this year we assume that no buybacks will occur, a long held assumption of ours, i.e. we pencil in a steady divisor in the coming five-year time frame. 2025 is our terminal year when dividend growth settles at 6.6%, 60bps below the long-term average (bottom panel, Chart 2). Our 8.2% discount rate mirrors the corporate junk bond yield historical average. This year we use two different dividend growth approaches: our own estimates and alternatively the S&P 500 dividend futures derived growth. In the spirit of conservatism, we pick the lowest point hit in early April across the different dividend futures expirations. Tables 2 & 3 summarize the results. In the dividend futures derived approach, SPX fair value is close to 2,110. Granted, such dividend contractions for two years running (33% in 2020 and 14% in 2021, Table 2) are extreme and highly unlikely. Moreover, dividend futures have since rebounded violently. However, we stick with them to derive our worst case SPX value. Table 2SPX Dividend Discount Model: Using S&P Dividend Futures Growth Assumptions Our own dividend growth estimates result in an SPX 3,000 fair value target (Table 3). While our assumptions are not as dire as the nadir in dividend futures, they are slightly more conservative than the GFC experience. As a reminder, in the aftermath of the GFC dividends contracted by 20% in 2009 and then recovered rising by 1% and 16% in 2010 and 2011, respectively (please click here if you would like to receive our DDM and insert your own assumptions). Table 3SPX Dividend Discount Model: Using USES Dividend Growth Assumptions Building up on this analysis, we want to identify sectors that are at risk of a dividend cut, and thus pose the greatest threat to our SPX dividend projections. Table 4 shows the 2019 sectorial dividends, profits, and the payout ratio along with indebtedness. While during the Great Recession financials cut their handsome dividends, the current recession is not a financial crisis and we doubt the financials sector will cut their dividends, at least not as aggressively as in the GFC (Table 5). Table 4S&P 500 GICS1 Sector Dividend Analysis Table 5The GFC S&P 500 GICS1 Sector Dividend Experience Energy is a clear standout, but neither XOM nor CVX will forego their dividend aristocrat status (minimum 25 consecutive years of rising dividends) and chop their dividends. In other words, these Oil Majors will do everything in their power including raising debt to ever so modestly increase their dividends and maintain their aristocrat status. Thus, $24bn of energy sector related dividends are safe or 55% of the overall energy sector’s dividend. Keep in mind that the energy sector increased their dividends in the GFC (Tables 4 & 5). Industrials (GE is no longer a big dividend payer), materials, real estate and select consumer discretionary are sore spots, but not large enough to undermine the SPX (Table 4). Tech, health care and consumer staples are in excellent shape and judging by JNJ’s and COST’s recent dividend hikes, these sectors that enjoy mostly pristine balance sheets may even increase their payouts as they did during the GFC (Tables 4 & 5). While utilities and telecom services are debt saddled, their defensive stature and stable cash flow streams along with their history of steady dividend payments also do not pose a real threat to the SPX’s dividend (Tables 4 & 5). This leaves financials as the key sector to monitor for a possible large inflicted wound to the SPX dividend. In the most adverse scenario where the Fed instructs banks to eliminate their dividends, as the BoE and the ECB recently did in Europe, then the SPX dividend will contract, but only by 15%, ceteris paribus. This is because last year the tech sector had the highest dividend weight in the SPX and also because the financials sector’s dividend weight has fallen from 30% in 2007 to 15% in 2019 (Tables 4 & 5). Netting it all out, we are comfortable with our dividend growth assumptions especially for the next three years – largely mimicking the GFC experience – and resulting in an SPX 3,000 fair value target. The path of least resistance for the SPX remains higher on a 9-12 month cyclical time horizon. However, given that the easy SPX gains from the March 23, 2020 lows – when we turned cyclically bullish2 – have been made, opportunistic/nimble investors could monetize at least a part of these massive one-month returns. As aforementioned the SPX may face resistance near the 50-day moving average where it attempts to consolidate its recent gains. This week we are downgrading a defensive group to neutral and boosting a deep cyclical group to an above benchmark allocation. Turning Stale Following up from last week’s report, we heed the message from our research to be wary of staples stocks at the depth of the recession and downgrade the S&P packaged foods index to neutral. This move also pushes the S&P consumer staples sector down to a benchmark allocation from previously overweight. While this defensive index had been severely bruised from the accounting scandal at Kraft/Heinz, it has really flexed its safe haven muscles year-to-date. We use this opportunity to trim exposure down to neutral as we deem that this relative advance has run out of steam, despite the once in a lifetime jump in a number of key demand indicators. Chart 3 shows that food & beverage store retail sales now garner 17% of total retail sales a percentage last hit in the early 1990s. Impressively, not only did industry sales rise in absolute terms, but also overall retail sales suffered a severe setback accentuating last month’s spike. Similarly, food output hit a high mark last month, outpacing overall industrial production that came to a standstill. Food products resource utilization also soared, outpacing overall capacity utilization by 10% (bottom panel, Chart 3). As a result, relative share price momentum came close to accelerating by triple digits on a short-term rate of change basis (Chart 4). While such euphoria is warranted, we reckon that most if not all the good news is already reflected in prices, especially given the early signs of a possible reopening of the US economy some time next month. Importantly, sell side analyst optimism has climbed to a similar height observed in late-2015/early-2016 when industry 12-month forward EPS were slated to outshine the broad market by over 10% (bottom panel, Chart 4). Chart 3Demand Boost… Chart 4…Is Already Baked In Worrisomely, despite the rising demand profile, operating margins have been drifting lower over the past decade and a further profit margin squeeze remains a high probability outcome (Chart 5). Finally, on the food export front, the rising US dollar is warning that volumes will remain in check in coming quarters (greenback shown inverted, middle panel, Chart 6). All of this is reflected in valuations that have returned to the 25-year mean with packaged food manufacturers now trading at a 9% forward P/E premium to the broad market (bottom panel, Chart 6). Chart 5Margin Trouble Chart 6Past Expiry Date In sum, relative performance already reflects the jump in demand for packaged foods. A firm US dollar and an ongoing profit margin squeeze at a time when relative valuations have returned to the historical mean compel us to downgrade the S&P packaged foods index to neutral. Bottom Line: Trim the S&P packaged foods index to neutral, today for a loss of 20% since inception. This downgrade also pushes the S&P consumer staples sector to neutral for a loss of 11% since inception. The ticker symbols for the stocks in this index are: BLBG: S5PACK – MDLZ, SJM, KHC, CPB, MKC, CAG, TSN, GIS, HSY, HRL, K, LW. Boost Software To Overweight We recently monetized over 50% relative gains in our overweight in the S&P software index, but today we are compelled to lift this heavyweight tech sub-index back to an overweight stance. One key reason for our renewed bullishness is that for the second time in the past 15 months, software stocks managed to eke out relative gains when the broad market fell peak-to-trough 20% and 35% in late-2018 and in Q1/2020, respectively (Chart 7). This resilience on the way down confirms both the defensive stature of this services tech subgroup and simultaneously our long held belief that when growth is scarce investors will flock to secular growth stocks. Chart 7Recession Proof As a result and following up from our recent data processing upgrade, another defensive services tech group, we are compelled to augment exposure to the S&P software index to overweight. Last week we showed that the tech sector (along with financials and consumer discretionary) best the broad market from the recessionary troughs onward, signaling that the key software sub group will likely lead the recovery.3 Software investment is on a multi decade upward trajectory and is slated to rise further in coming quarters as overall spending takes the back seat, but defensive software capex remains resilient (Chart 8). Not only do corporate executives upgrade software in downturns as these upgrades yield near instantaneous return on investment and are immediately productivity enhancing, but also the push to cloud-based services will only accelerate during the ongoing recession (bottom panel, Chart 8). Tack on that the global coronavirus social distancing measures are also boosting demand for remote working services specifically, and software sales will continue to grind higher (Chart 9). Chart 8Capex Market Share Gains Chart 9Rising Demand Buoys Sales Meanwhile, industry M&A remains robust and both the number of deals are still rising at a brisk rate and the premia paid remain near historically high levels (Chart 10). Contrary to a slew of corporations that have announced dividend cuts and equity buyback suspensions, pristine software balance sheets underscore that shareholder friendly activities will remain in place, if not accelerate, during the current recession (bottom panel, Chart 10). Chart 10What’s Not To Like? Chart 11Model Says Buy Our macro-based software EPS growth model does an excellent job in capturing all these moving forces and it is signaling that industry profits will continue to expand at a healthy pace for the rest of the year, in marked contrast to the broad market’s expected profit contraction (Chart 11). Adding it all up, an upward trending demand profile, a fortress of a balance sheet, exemplary recession resilience, and sustained M&A activity, all bode well for an earnings-led outperformance phase in the S&P software index. Bottom Line: Boost the S&P software index to overweight, today. This upgrade also lifts the S&P tech sector to neutral for a loss of 5% since inception. The ticker symbols for the stocks in this index are: BLBG: S5SOFT – MSFT, ADBE, CRM, ORCL, INTU, NOW, ADSK, ANSS, SNPS, CDNS, FTNT, PAYC, CTXS, NLOK. Anastasios Avgeriou US Equity Strategist anastasios@bcaresearch.com Footnotes 1 Please see BCA US Equity Strategy Weekly Report, “SPX 3,000?” dated July 10, 2017, available at uses.bcaresearch.com. 2 Please see BCA US Equity Strategy Weekly Report, ““The Darkest Hour Is Just Before The Dawn”” dated March 23, 2020, available at uses.bcaresearch.com. 3 Please see BCA US Equity Strategy Weekly Report, “Fight Central Banks At Your Own Peril” dated April 14, 2020, available at uses.bcaresearch.com. Current Recommendations Current Trades Strategic (10-Year) Trade Recommendations Size And Style Views June 3, 2019 Stay neutral cyclicals over defensives (downgrade alert) January 22, 2018 Favor value over growth May 10, 2018 Favor large over small caps (Stop 10%) June 11, 2018 Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V).

However, the S&P packaged foods sub-index has not participated in the rebound. These exports-oriented stocks have been held back by trade and currency headwinds. Still, we remain constructive on the index as those handicaps could evaporate as suddenly as…

Consumer staples stocks have been staging a recovery late in the year, buoyed by an exceptionally strong consumer. However, the S&P packaged foods sub-index has not participated in the rebound, held back by trade and currency headwinds in this export market-exposed sector. Still, we remain constructive on the index as those headwinds could evaporate as suddenly as they came, leaving a very solid domestic demand backdrop to lift the stocks into outperformance territory. Indeed, the environment looks exceptionally healthy; food retailers have been riding a five-year rising tide of sales (second panel). Further, consumers have been boosting their food consumption, which has historically been a good leading indicator of top line growth (third panel). In the context of a strong dollar providing a meaningful offset to packaging and raw food commodity prices, margin expansion looks particularly potent. Despite the bright outlook, the S&P packaged foods index remains deeply discounted, trading well below its eight-year average earnings multiple as well as the market multiple (bottom panel). We think investors should pick this one out of the bargain bin; stay overweight. The ticker symbols for the stocks in this index are: BLBG: S5PACK - MDLZ, KHC, GIS, TSN, K, MKC, HSY, CAG, SJM, HRL, CPB.

Overweight Not only have investors shunned consumer staples stocks in general, but the S&P packaged foods sub-index has also suffered, even trailing the broad staples sector. We are not willing to throw in the towel in this staples sub-index that offers hidden value. A number of leading industry demand indicators are firming and suggest that a top line growth period is in the cards. Food and beverage exports are rising at a healthy clip, despite the U.S. dollar's year-to-date appreciation, and so are domestic consumer outlays (second panel). Importantly, relative to overall spending, real (volume) food and beverage spending is expanding smartly (third panel). Add on tame raw food commodity costs, especially compared with broad commodity price inflation and relative EPS will overwhelm extremely depressed analysts' expectations (relative grain prices shown inverted, bottom panel). Bottom Line: Stay overweight the S&P packaged foods index; please see Monday's Weekly Report for more details. The ticker symbols for the stocks in this index are: BLBG: S5PACK - MDLZ, KHC, GIS, TSN, K, CAG, HSY, MKC, SJM, HRL, CPB.

Highlights Portfolio Strategy A rare buying opportunity has emerged in the S&P consumer staples index, especially for long-term oriented capital. The bearish story is already baked into current valuations, and industry green-shoots are flying under the radar. Similarly, the bearish packaged foods narrative is well ingrained in depressed relative valuations, whereas the budding recovery in industry final demand is severely underappreciated. This offers investors a compelling entry point to this unloved and under-owned consumer products subgroup. Recent Changes There are no changes to our portfolio this week Table 1 Feature The S&P 500 digested receding geopolitical risks last week, and continued to consolidate recent gains. Stocks are poking at the upper end of the 10% trading range in place since early-February, and internal equity dynamics suggest that a breakout in a bullish fashion is in store for later in the summer, as we first posited in late April.1 Chart 1 shows our Equity Market Internal Dynamics Indicator (EMIDI) that does an excellent job capturing the shifting internal forces that drive market returns. This coincident-to-leading market Indicator comprising economically sensitive sectors and portfolio biases is signaling that the path of least resistance is higher for the SPX. Similar to the EMIDI, the Value Line Arithmetic Index (an equal weighted broad-based stock market index) broke out to fresh all-time highs and the Value Line Geometric Index (a gauge of median stock prices) is following closely behind (third & fourth panels, Chart 2). Market darling AAPL is making a run at a $1tn valuation, spearheading the tech-laden NASDAQ Composite that remains on a pattern of hitting higher highs (top panel, Chart 2). Equity buying power is also evident in the breakout of Thomson/Reuters' "Most Shorted Stocks Index" (second panel, Chart 2). All of this suggests that before long the SPX will follow the uptrend and vault to all-time highs, a message corroborated by the record highs in the broad market's advance/decline (A/D) line (bottom panel, Chart 2). Chart 1Breakout... Chart 2...Looming An enticing macro backdrop continues to underpin equities. The latest ISM manufacturing report confirmed the IHS Markit U.S. manufacturing PMI release that we highlighted in our Report two weeks ago2: the U.S. is firing on all cylinders and has the potential to pull global growth out of its recent lull. In particular, the reacceleration in the ISM new orders-to-inventories ratio suggests that equities will gain steam in the coming months (second panel, Chart 3). Another source of upbeat news was the backlog subcomponent of the May ISM manufacturing survey. Unfilled orders hit a 14-year high, just shy of the all-time record. Historically, backlogs have been an excellent leading indicator of SPX revenue growth and the current message is that S&P 500 top line growth is on a solid footing (bottom panel, Chart 3). The Fed acknowledged this mini economic overheating last week, and the FOMC slightly bumped its median expectation to a total of four hikes in calendar 2018. Moreover, fiscal easing will continue to gain thrust as the year progresses and the cash repatriation will also provide an assist to the stock market. We are modeling between $650bn-to-$800bn in equity retirement for calendar 2018. Chart 4 depicts our estimates and if the historical correlation between share buybacks and equity prices holds, then there is more upside to stocks in the back half of the year. Nevertheless, retail investors are replenishing cash coffers according to the American Association of Individual Investors (AAII), rather than actively participating in the latest market run up. At the margin, this beefing up of retail investor dry powder represents a headwind to additional equity market gains. We heed the message from this traditionally leading Indicator and in order for our cyclical (9-12 month horizon) sanguine equity market view to pan out, individual investors will have to drawdown their cash balances (AAII cash shown inverted, Chart 5). Chart 3Macro Tailwinds Chart 4Corporate Underpinnings... Chart 5...But Retail Investor Has To Participate This week we are revisiting a broad defensive sector and one of its key subcomponents. What To Do With Staples Investors have deserted consumer staples stocks at a dizzying speed, and valuations have cratered to a multi-decade low, according to our composite Valuation Indicator (Chart 6). Technicals are also as washed out as can be, as staples equities have been sold off indiscriminately. Other sentiment and breadth measures confirm that this safe haven sector has lost its allure: the A/D line is probing multi-year lows, EPS breadth is waning and groups with a positive 52-week rate of change and trading above the 40-week moving average have all but disappeared (Chart 7). Chart 6Buy Into Weakness Chart 7Bombed Out Sentiment Our sense is that this consumer staples wholesale liquidation provides a great buying opportunity, especially for longer-term oriented capital with a time horizon of at least 2-3 years. Even on a shorter-term outlook, a bounce seems likely from extremely depressed levels, as relative share prices may find support close to the pre-Great Recession trough (top panel, Chart 7). From a cyclical perspective we continue to view this defensive sector as a hedge to our overall portfolio position that sustains a pro-cyclical bent. Importantly, the bearish consumer staples case is well discounted in bombed out valuations. The stock-to-bond ratio is weighing on this fixed income proxy sector that sports a dividend yield on a par with the 10-year Treasury (top & second panels, Chart 8). Moreover, subsiding volatility bodes ill for relative share prices; the opposite is also true (bottom panel, Chart 8). On the demand front, once again the uninspiring non-cyclical spending backdrop is well entrenched in sinking relative share prices. Relative staples retail sales - both compared to discretionary and to total sales - are deflating as is typical in the late stages of the business cycle (top & second panels, Chart 9). Chart 8Bearish Narrative Baked In Chart 9Lack Of Demand... Such waning demand has weighed on industry selling prices at a time when executives are making labor additions, blowing out our wage bill proxy. As a result, profits margins are suffering a squeeze (Chart 10). However, there are some pockets of strength hidden beneath the surface. While non-discretionary demand is losing share versus overall outlays, spending on essentials as a percentage of disposable income is gaining steam. True, this could be a pre-cursor to recession, but our interpretation is that latent staples-related buying power may make a comeback from a still very depressed level and kick-start industry sales growth (bottom panel, Chart 9). Other industry green-shoots are also surfacing. Consumer staples exports are on a slingshot recovery path, expanding by a low double digit growth rate, defying the year-to-date trade-weighted U.S. dollar appreciation (second panel, Chart 11). In fact, given the defensive stature of this index, any additional greenback gains will boost relative profits especially in the first half of 2019 (third panel, Chart 11). Chart 10...Weighing On Margins... Chart 11...But Green-Shoots Surfacing Finally, CEO confidence of non-durable industries is far outpacing the broad animal spirit recovery according to The Conference Board, and this relative Chief Executive euphoria has historically been positively correlated with share price momentum, underscoring that better times lie ahead for consumer staples stocks (bottom panel, Chart 11). Adding it up, a rare buying opportunity has emerged in the S&P consumer staples index, especially for long-term oriented capital. The bearish story is already baked into current valuations, and industry green-shoots are flying under the radar. Tack on impressive industry return on equity and this index appears extremely undervalued (bottom panel, Chart 6). Bottom Line: Were we not already overweight the S&P consumer staples index, we would not hesitate to lift exposure to above benchmark. Appetizing Packaged Foods Not only have investors shunned consumer staples stocks in general, but the S&P packaged foods sub-index has also suffered, even trailing the broad staples sector. As a reminder, within consumer products we are overweight packaged foods and household products but maintain a below-benchmark allocation to soft drinks. Packaged foods relative share prices have returned to the mid-2000s level offering a compelling entry point for fresh capital, especially longer-term oriented money (top panel, Chart 12). Part of the reason that these stocks are under-owned boils down to their defensive characteristics. These safe-haven equities pay handsome, steadily growing and secure dividends. Thus, when the bond market's selloff gains steam, investors flock to deep cyclical stocks and trim fixed income proxied equities, and vice versa. Moreover, the Warren Buffett induced M&A premia have now fully reversed from this group, with the base effect weighing on relative performance (bottom panel, Chart 12). Nevertheless, we are not willing to throw in the towel in this staples sub-index that offers hidden value. A number of leading industry demand indicators are firming and suggest that a top line growth period is in the cards. Food and beverage exports are rising at a healthy clip, despite the U.S. dollar's year-to-date appreciation, and so are domestic consumer outlays (second panel, Chart 12). The industry's shipments-to-inventories ratio is sending a similar message, jumping to a level last seen four years ago (third panel, Chart 12. Importantly, relative to overall spending, real (volume) food and beverage spending is expanding smartly. Add on tame raw food commodity costs, especially compared with broad commodity price inflation and relative EPS will overwhelm extremely depressed analysts' expectations (relative grain prices shown inverted, bottom panel, Chart 13). Chart 12Budding Demand Recovery... Chart 13...Should Aid Top Line Growth This encouraging demand backdrop is showing up in industry pricing power. Rising food manufacturing shipments are underpinning food producers' selling prices (second panel, Chart 14), and coupled with the contained crude food input costs suggest that packaged foods margins will continue to expand (middle panel, Chart 14). Even down the supply chain, food manufacturers' appear to be making significant headway, a harbinger at least of a profit margin relief phase. While channel captains food retailers have been dictating pricing terms to food suppliers for the better part of the past five years, industry producer prices are now on an even keel with CPI foods, a good proxy of what super markets are charging the consumer (fourth panel, Chart 14). Any additional pricing power gains will represent a boost to industry margins and, thus, profitability. Finally, firming demand is also showing up on industry operating metrics: factory activity is running red hot with resource utilization rates vaulting to multi-decade highs and industry hours worked picking up momentum (third panel, Chart 15). While CEOs have expanded the labor footprint and wage inflation is a cause for concern (bottom panel, Chart 15), a simple industry productivity proxy (industrial production divided by employment) shows that profits should enjoy a lift in the coming quarters. Chart 14Margins Can Expand Further Chart 15Brisk Factory Activity Netting it out, the bearish packaged foods narrative is well ingrained in depressed relative valuations (bottom panel, Chart 14), whereas the budding recovery in industry final demand is severely underappreciated, offering investors a compelling entry point to this unloved and under-owned consumer products subgroup. Bottom Line: Stay overweight the S&P packaged foods index. The ticker symbols for the stocks in this index are: BLBG: S5PACK - MDLZ, KHC, GIS, TSN, K, CAG, HSY, MKC, SJM, HRL, CPB. Anastasios Avgeriou, Vice President U.S. Equity Strategy anastasios@bcaresearch.com 1 Please see BCA U.S. Equity Strategy Weekly Report, "Lifting SPX Target," dated April 30, 2018, available at uses.bcaresearch.com. 2 Please see BCA U.S. Equity Strategy Weekly Report, "Unwavering," dated June 4, 2018, available at uses.bcaresearch.com. Current Recommendations Current Trades Size And Style Views Favor value over growth Favor large over small caps

The S&P packaged foods index has enjoyed a solid Q1 earnings season; results have bested forecasts, leading to some of the highest positive earnings revisions of the past decade (top panel). Robust demand growth, both domestic and international, combined with resilient pricing power (second panel) have pushed sales higher, while costs have been mostly contained. The market has looked through the results to some clouds on the horizon and taken the index down with it. First, food commodities, like nearly all commodity groups, are seeing prices rise; this takes time to filter through earnings, but eventually profits will feel the pinch. More importantly, recent U.S. dollar appreciation will likely crimp sales in the key export market (third panel), as well as sap foreign earnings growth via translation. While some caution is warranted with the headwinds facing the industry, the massive valuation de-rating the index has seen (bottom panel) seems to be an excessive overreaction, particularly in the context of the healthy demand backdrop. Accordingly, we reiterate our outperform recommendation. The ticker symbols for the stocks in this index are: BLBG: S5PACK - MDLZ, KHC, GIS, TSN, K, HSY, CAG, SJM, MKC, CPB, HRL.

This week has seen the beleaguered packaged foods index finally catch a bid, driven by exceptional earnings at two of the larger constituents, MDLZ and K. Both highlighted organic volume growth and a better pricing backdrop as the key drivers of top line outperformance. This corroborates with both the overall industry picture (second panel) and our rationale for moving the index to overweight earlier this year (see our Weekly Report of 23 May, 2017 for more details). We continue to expect that a durable top line recovery will expand packaged foods margins. In the context of the significant restructuring the industry has undertaken over the past year and early margin improvements (third panel), packaged foods manufacturers should see outsized earnings growth. Adding on a mouth-watering valuation (bottom panel) makes this index looks particularly appetizing. Stay overweight. The ticker symbols for the stocks in this index are: BLBG: S5PACK - MDLZ, KHC, GIS, TSN, K, HSY, CAG, SJM, MKC, CPB, HRL.